Chapter 16 – Partnerships: Liquidation

Copyright © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not

authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded,

distributed, or posted on a website in whole or part.

CHAPTER 16

PARTNERSHIPS: LIQUIDATION

ANSWERS TO QUESTIONS

Q16-1 The major causes of a dissolution are:

a.

Withdrawal or death of a partner

b.

The specified term or task of the partnership has been completed

c.

All partners agree to dissolve the partnership

d.

An individual partner is bankrupt

e.

By court decree:

i.

the partnership cannot achieve its economic purpose

(typically defined as seeking a profit)

ii.

a partner seriously breaches the partnership agreement

that makes it impracticable to continue the partnership

business

iii.

It is not practicable to carry on the partnership in conformity

with the terms of the partnership agreement

Q16-2 The UPA 1997 states that a partnership’s liabilities to individual partners have

Q16-3 The implications that arise for partners X and Y are that both of the partners may

be required to contribute a portion of their capital balances or personal assets to satisfy

Q16-4 In an “at will” partnership (one without a partnership agreement that states a

definite time period or specific undertaking for the partnership), a partner may simply

Q16-5 A lump-sum liquidation of a partnership is one in which all assets are converted

into cash within a very short time, creditors are paid, and a single, lump-sum payment is

Q16-6 A deficit in a partner’s capital account (relating to an insolvent partner) is

ratio.

Q16-7 The DEF Partnership is insolvent because the liabilities of the partnership

($61,000) exceed the assets of the partnership ($55,000). The liabilities of the

Chapter 16 – Partnerships: Liquidation

16-3

Q16-15* The process of incorporating a partnership begins with all partners deciding to

incorporate the business. At the time of incorporation, the partnership is terminated and

C16-1 Cash Distributions to Partners

The key issue is that must be resolved in the partnership liquidation is that Bull desires

cash to be distributed as it becomes available, while Bear wishes no cash to be

distributed until all assets are sold and the liabilities are settled.

Chapter 16 – Partnerships: Liquidation

C16-2 Cash Distributions to Partners

Assuming strict use of UPA 1997:

Once a partnership enters liquidation, loans receivable from partners are treated as any

other asset of the partnership and partnership loans payable to individual partners are

treated as any other liability of the partnership. Thus, these accounts with partners do not

Chapter 16 – Partnerships: Liquidation

C16-2 (continued)

Assuming a practical approach:

Although UPA 1997 specifically states that partnership debt is considered equal to

outside debt, most loans from partners are subordinated to outside debt. Typically this is

done at the request of the outside creditors. In addition, loans to/from partners are

Chapter 16 – Partnerships: Liquidation

16-6

C16-3* Incorporation of a Partnership

a. Comparison of balance sheets

The partnership’s balance sheet will report the assets and liabilities at their book values

while the corporation’s balance sheet will report the fair values of these items at the point

of incorporation. The incorporation of the partnership results in a new accounting entity,

According to GAAP, a partnership’s income statement should not include distributions to

the partners as expenses. These distributions include interest on partners’ capital,

salaries to partners, bonuses to partners, and any residual distributions made as part of

the profit distribution agreement. Flexibility is allowed for partnerships to prepare non–

GAAP financial statements if the partners feel the non-GAAP statements provide for

Chapter 16 – Partnerships: Liquidation

16-7

C16-4 Sharing Losses during Liquidation

a. Liquidation loss allocation procedures in the Uniform Partnership Act of 1997:

Section 401 of the Uniform Partnership Act of 1997 specifies that “Each partner is

entitled to an equal share of the partnership profits and is chargeable with a share of the

partnership losses in proportion to the partner’s share of the profits.”

agree at this point in time, it may be best not to move forward with the formation of the

partnership. Simply putting off an important issue is not going to eliminate its possible

importance later in time. While not discussing the issue now removes a possibly

contentious issue from the discussion, it does not solve the problem.

Luna’s argument of equality for responsibility of a failure of the partnership is humanistic,

for continued success. Furthermore, this method would be disadvantageous to a partner

who leaves capital accumulations in the partnership.

c. Another method of allocating losses:

The partners could agree to share all profits and losses in the 4:3:2 ratio or select a

specific loss sharing ratio in the event of liquidation. The important point is that the

Chapter 16 – Partnerships: Liquidation

16-8

C16-5 Analysis of a Court Decision on a Partnership Liquidation

This case asks questions about the Mattfield v Kramer Brothers court case decided by the

Montana Supreme Court on May 31, 2005. The court case is a really interesting

presentation of some of the major types of problems that can occur in a family partnership.

1995. In 1997, Raymond Sr. (the father) died which resulted in the four brothers, including

Don, discussing the distribution of their father’s interest in the partnership. On December 9,

1998, Ray and Doug offered to purchase Don’s interest in the partnership but Don rejected

the offer. On May 23, 2000, Don filed a suit demanding a formal accounting of the

partnership, liquidation of its assets, and distribution of real property held by the partners as

Chapter 16 – Partnerships: Liquidation

16-9

C16-5 (continued)

c. Bill Kramer’s economic interest in partnership. Bill disassociated from the partnership in

1985, soon after it was formed. The information presented in the court’s decision does not

state if Bill received a buyout from the partnership. In addition, Bill received a partial interest

from the estate of his father. The appeal motion included Bill as one of the defendants.

the authority to bind the partnership. The remaining partners could also have a new

partnership agreement, this time in writing, to provide written evidence that they are

continuing the business. The important thing is that the remaining partners have sufficient

documentation and evidence of Don’s partnership interest as of the date he disassociated.

e. Request for Ray’s and Doug’s personal tax returns. This was probably an effort to

agreement, but there are other interesting items in the court case. Students are probably not

aware of the five-year statute of limitations on claims. The court’s decision that Don’s

relocation to San Francisco in July 1994 was a wrongful disassociation is interesting

because, as a result of a car accident, Don was not able to fully participate in the

partnership. The issue of when the five-year statute of limitations period began is interesting

Chapter 16 – Partnerships: Liquidation

E16-1 Multiple-Choice Questions on Partnership Liquidations

1.

c –

Joan

Charles

Thomas

Total

Profit ratio

40%

50%

10%

100%

Prior capital

160,000

45,000

55,000

260,000

Loss on sale

of inventory

(24,000)

(30,000)

(6,000)

(60,000)

136,000

15,000

49,000

200,000

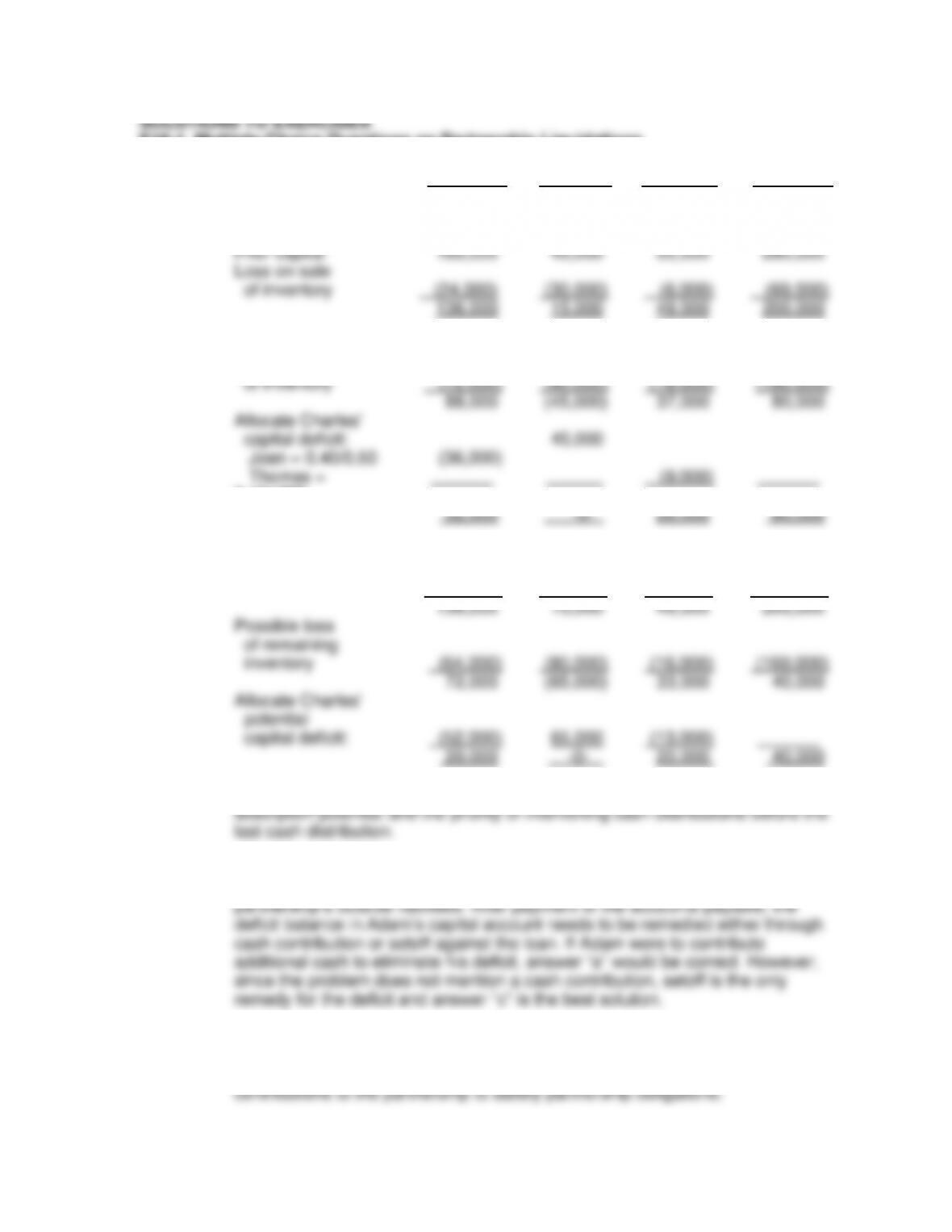

2.

a –

Prior capital

160,000

45,000

55,000

260,000

Loss on sale

of inventory

(72,000)

(90,000)

(18,000)

(180,000)

88,000

(45,000)

37,000

80,000

Allocate Charles’

capital deficit:

45,000

Joan = 0.40/0.50

(36,000)

Thomas =

0.10/.050

(9,000)

52,000

-0-

28,000

80,000

3.

d –

Prior capital

160,000

45,000

55,000

260,000

Loss on sale

of inventory

(24,000)

(30,000)

(6,000)

(60,000)

136,000

15,000

49,000

200,000

Possible loss

of remaining

inventory

(64,000)

(80,000)

(16,000)

(160,000)

72,000

(65,000)

33,000

40,000

Allocate Charles’

potential

capital deficit:

(52,000)

65,000

(13,000)

20,000

-0-

20,000

40,000

4.

d –

The safe payments computations include consideration of the partners’ loss

absorption potential and the priority of intervening cash distributions before the

last cash distribution.

5.

c –

The loan payable to Adam has the same legal status as the partnership’s other

liabilities according to the UPA of 1997, but is likely subordinated to the

partnership’s outside liabilities. After payment of the accounts payable, the

deficit balance in Adam’s capital account needs to be remedied either through

cash contribution or setoff against the loan. If Adam were to contribute

additional cash to eliminate his deficit, answer “a” would be correct. However,

since the problem does not mention a cash contribution, setoff is the only

remedy for the deficit and answer “c” is the best solution.

6.

d –

Partnership creditors have first claim to partnership assets

7.

a –

After the settlement of accounts, partners are required to make additional

contributions to the partnership to satisfy partnership obligations.