Chapter 10 – Additional Consolidation Reporting Issues

P10-28 Deferred Tax Assets and Liabilities in a Consolidated Balance Sheet

Deferred Tax Asset

$8,000

Tax Rate

÷ 0.40

Book-Tax Difference (future deductible difference)

Amount related to Vacation Payable

Remainder related to Allowance for Doubtful Accounts

20,000

(15,000)

5,000

Deferred Tax Liability

$6,000

Tax Rate

÷ 0.40

Book-Tax Difference (future taxable difference) related to Equipment

15,000

Tax basis of Accounts Receivable = $55,000 (50,000 book value + 5,000 book-tax difference

related to the allowance)

Deferred Tax Asset

$1,000

Tax Rate

÷ 0.40

Book-Tax Difference (future deductible difference) related

to Allowance for Doubtful Accounts

2,500

Deferred Tax Liability

$2,000

Tax Rate

÷ 0.40

Book-Tax Difference (future taxable difference) related to Equipment

5,000

Tax basis of Accounts Receivable = $14,500 (12,000 book value + 2,500 book-tax difference

P10-28 (continued)

As stated in the problem, all other items have no book-tax differences.

b. The fair value of the DTAs and DTLs will be the tax-effected differences between the tax

bases and the book bases of Harmony’s identifiable assets and liabilities.

Harmony Corporation

Fair Value

Tax Basis

Difference

Tax-

effected

Cash

$ 8,000

$ 8,000

0

0

Accounts Receivable, net

12,000

14,500

2,500

1,000

Inventory

10,000

7,000

(3,000)

(1,200)

Equipment, net

40,000

20,000

(20,000)

(8,000)

Patent

20,000

0

(20,000)

(8,000)

Accounts Payable

$ 13,000

$ 13,000

0

0

Long Term Debt

8,000

8,000

0

0

Total DTA = 1,000 related to Accounts receivable

Total DTL = 17,200 related to Inventory, Equipment and Patent

c. Consolidation entries:

Peace

=

Common

Stock

+

Retained

Earnings

Book value at

acquisition date

30,000

20,000

10,000

Basic Consolidation Entry

Common Stock

20,000

Retained Earnings

10,000

Investment in Harmony Co.

30,000

P10-28 (continued)

Excess Value (Differential) Calculations:

Peace

=

Inventory

+

Equip

+

Patent

+

Goodwill

–

DTL

Beginning Balance

30,000

3,000

15,000

20,000

7,200

(15,200)

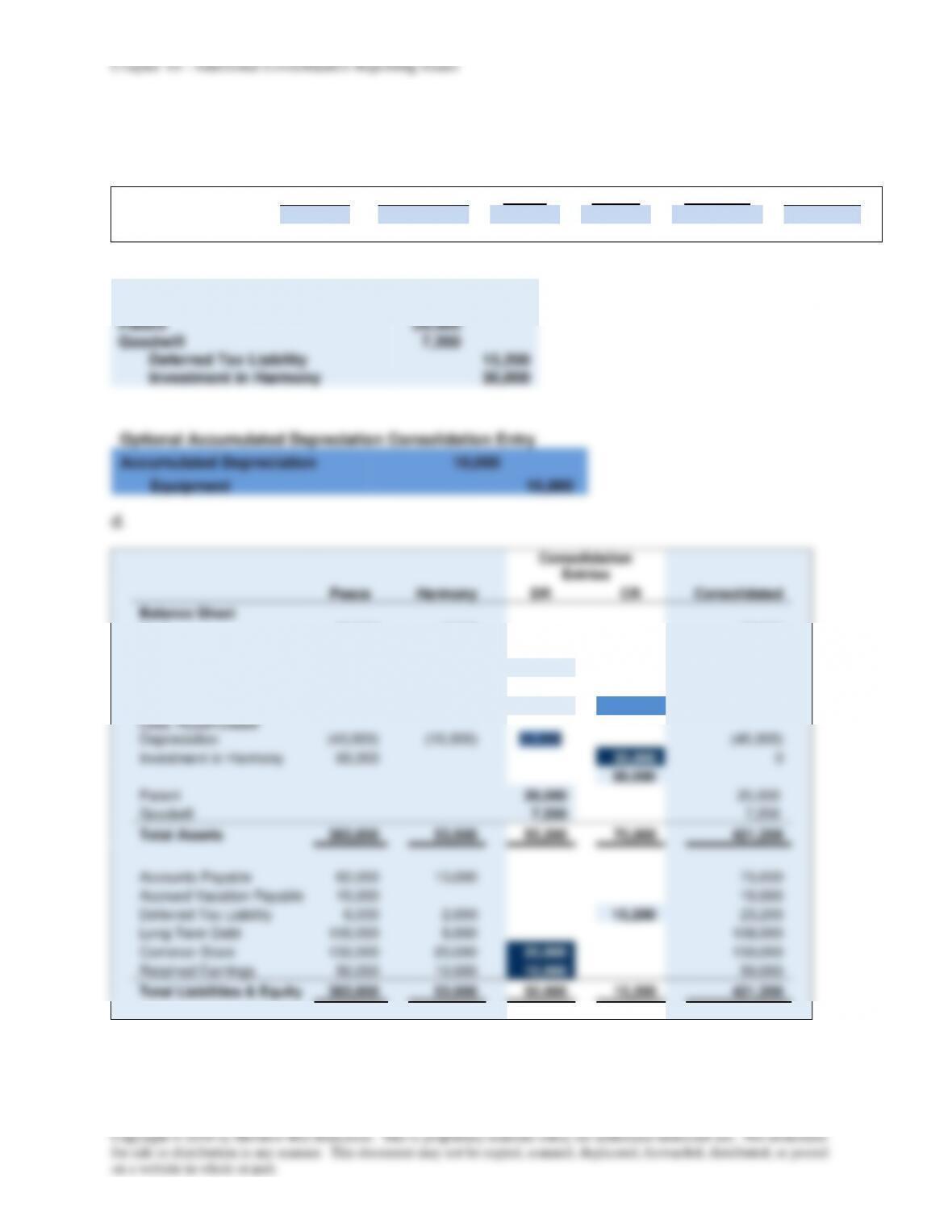

Excess Value (Differential) Reclassification Entry:

Inventory

3,000

Equipment

15,000

Patent

20,000

Goodwill

7,200

Deferred Tax Liability

15,200

Investment in Harmony

30,000

Optional Accumulated Depreciation Consolidation Entry

Accumulated Depreciation

10,000

Equipment

10,000

Peace

Harmony

Consolidation

Entries

DR

CR

Consolidated

Balance Sheet

Cash

30,000

8,000

38.000

Accounts Receivable

50,000

12,000

62,000

Inventory

75,000

7,000

3,000

85,000

Deferred Tax Asset

8,000

1,000

9,000

Equipment

200,000

35,000

15,000

10,000

240,000

Less: Accumulated

Depreciation

(40,000)

(10,000)

10,000

(40,000)

Investment in Harmony

60,000

30,000

0

30,000

Patent

20,000

20,000

Goodwill

7,200

7,200

Total Assets

383,000

53,000

55,200

70,000

421,200

Accounts Payable

62,000

13,000

75,000

Accrued Vacation Payable

15,000

15,000

Deferred Tax Liability

6,000

2,000

15,200

23,200

Long Term Debt

100,000

8,000

108,000

Common Stock

150,000

20,000

20,000

150,000

Retained Earnings

50,000

10,000

10,000

50,000

Total Liabilities & Equity

383,000

53,000

30,000

15,200

421,200

P10-29 Tax Allocation in Consolidated Balance Sheet

Consolidation entries (not required):

Book Value Calculations:

NCI

30%

+

Acme

Powder

70%

=

Common

Stock

+

Retained

Earnings

Ending book value

120,000

280,000

150,000

250,000

Adjustment to Basic Consolidation Entry

NCI

Acme

Powder

Ending Book Value

120,000

280,000

– Gross profit deferral, net of taxes (up)

(3,600)

(8,400)

– Gross profit deferral, net of taxes (down)

(15,000)

– Gain on Assets Sale, net of taxes (up)

(9,000)

(21,000)

Adjusted Book Value

107,400

235,600

108,000

242,000

Deferred Gain Calculations:

Total

=

Acme

Powder’s

share

+

NCI’s

share

Upstream GP Deferral (net of taxes)

(12,000)

(8,400)

(3,600)

Downstream GP Deferral (net of taxes)

(15,000)

(15,000)

Upstream Gain on Asset Sale (net of taxes)

(30,000)

(21,000)

(9,000)

Total

(57,000)

(44,400)

(12,600)

Basic Consolidation Entry

Common Stock

150,000

← Common Stock

Retained Earnings

250,000

← Beginning balance in RE

Income from Brown Co.

44,400

← Acme Powder’s share GP Deferrals – Gain

NCI in NI of Brown Co.

12,600

← NCI share of GP Deferral – Gain

Investment in Brown Co.

235,600

← Acme Powder’s share of BV with adjustments

NCI in NA of Brown Co.

107,400

← NCI share of BV of net assets with adjustments

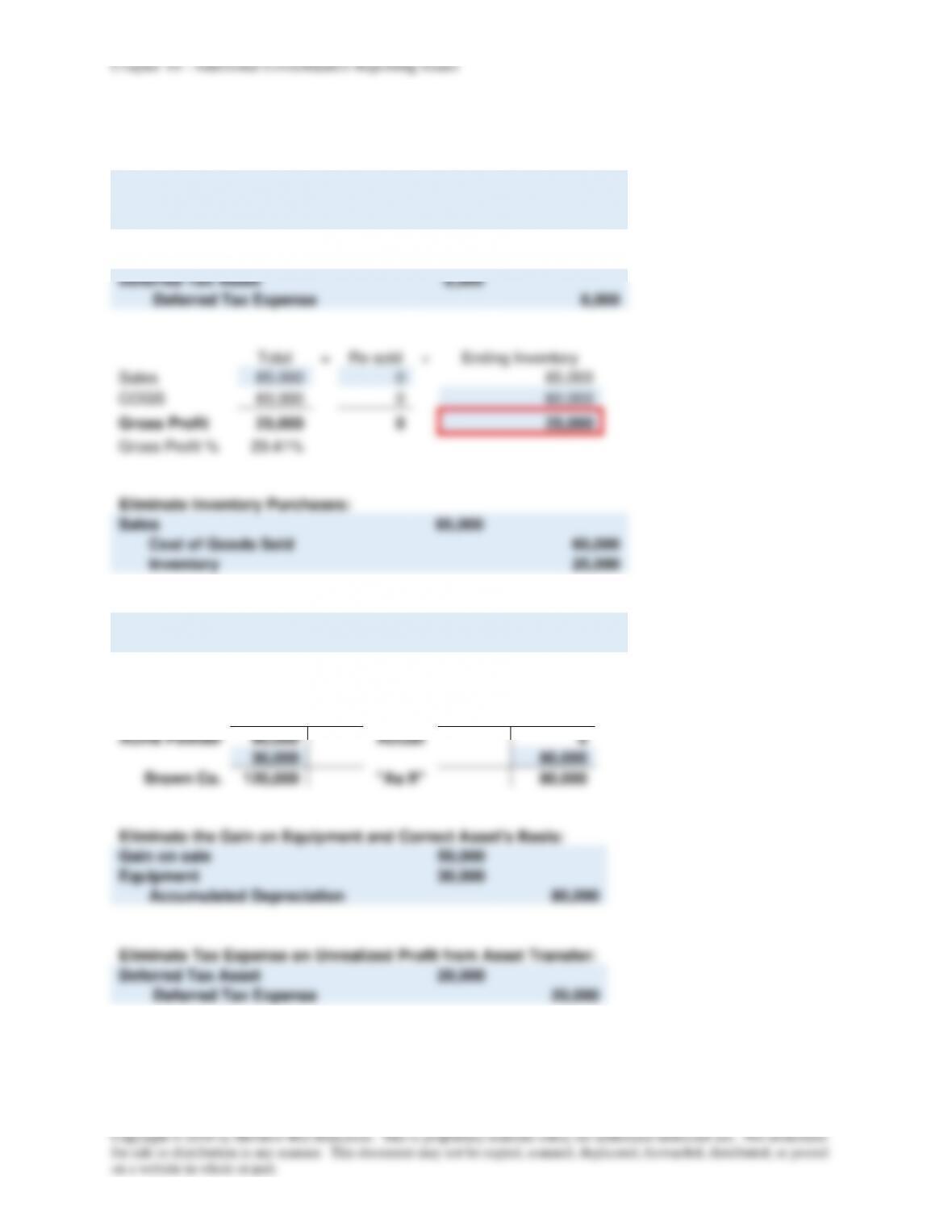

Total

=

Re-sold

+

Ending Inventory

Sales

70,000

0

70,000

COGS

50,000

0

50,000

Gross Profit

20,000

0

20,000

Gross Profit %

28.57%

P10-29 (continued)

Eliminate Inventory Purchases:

Sales

70,000

Cost of Goods Sold

50,000

Inventory

20,000

Eliminate Tax Expense on Unrealized Profit on Inventory Transfer:

Deferred Tax Asset

8,000

Deferred Tax Expense

8,000

Total

=

Re-sold

+

Ending Inventory

Sales

85,000

0

85,000

COGS

60,000

0

60,000

Gross Profit

25,000

0

25,000

Gross Profit %

29.41%

Eliminate Inventory Purchases:

Sales

85,000

Cost of Goods Sold

60,000

Inventory

25,000

Eliminate Tax Expense on Unrealized Profit on Inventory Transfer:

Deferred Tax Asset

10,000

Deferred Tax Expense

10,000

Equipment

Accumulated

Depreciation

Acme Powder

90,000

Actual

0

30,000

80,000

Brown Co.

120,000

“As If”

80,000

Eliminate the Gain on Equipment and Correct Asset’s Basis:

Gain on sale

50,000

Equipment

30,000

Accumulated Depreciation

80,000

Eliminate Tax Expense on Unrealized Profit from Asset Transfer:

Deferred Tax Asset

20,000

Deferred Tax Expense

20,000

P10-29 (continued)

a.

Acme

Powder

Brown

Co.

Consolidation

Entries

DR

CR

Consolidated

Balance Sheet

Cash

44,400

20,000

64,400

Accounts Receivable

120,000

60,000

180,000

Inventory

170,000

120,000

20,000

245,000

25,000

Land

90,000

30,000

120,000

Buildings and Equipment

500,000

300,000

30,000

830,000

Less: Accumulated

Depreciation

(180,000)

(80,000)

80,000

(340,000)

Investment in Brown Co.

235,600

0

235,600

0

Deferred Tax Asset

8,000

38,000

10,000

20,000

Total Assets

980,000

450,000

68,000

360,600

1,137,400

Accounts Payable

70,000

20,000

90,000

Wages Payable

80,000

30,000

110,000

Bonds Payable

200,000

0

200,000

Common Stock

100,000

150,000

150,000

100,000

Retained Earnings

530,000

250,000

250,000

44,400

530,000

70,000

12,600

85,000

50,000

50,000

8,000

60,000

10,000

20,000

NCI in NA of Brown Co.

107,400

107,400

Total Liabilities & Equity

980,000

450,000

605,000

312,400

1,137,400

P10-29 (continued)

b.

Acme Powder Corporation and Subsidiary

Consolidated Balance Sheet

December 31, 20X9

Cash

$ 64,400

Accounts Receivable

180,000

Inventory

245,000

Land

120,000

Buildings and Equipment

$830,000

Less: Accumulated Depreciation

(340,000)

490,000

Deferred Tax Asset

38,000

Total Assets

$1,137,400

Accounts Payable

$ 90,000

Wages Payable

110,000

Bonds Payable

200,000

Stockholders’ Equity:

Controlling Interest:

Common Stock

$100,000

Retained Earnings

530,000

Total Controlling Interest

$630,000

Noncontrolling Interest

107,400

Total Stockholders’ Equity

737,400

Total Liabilities and Stockholders’ Equity

$1,137,400