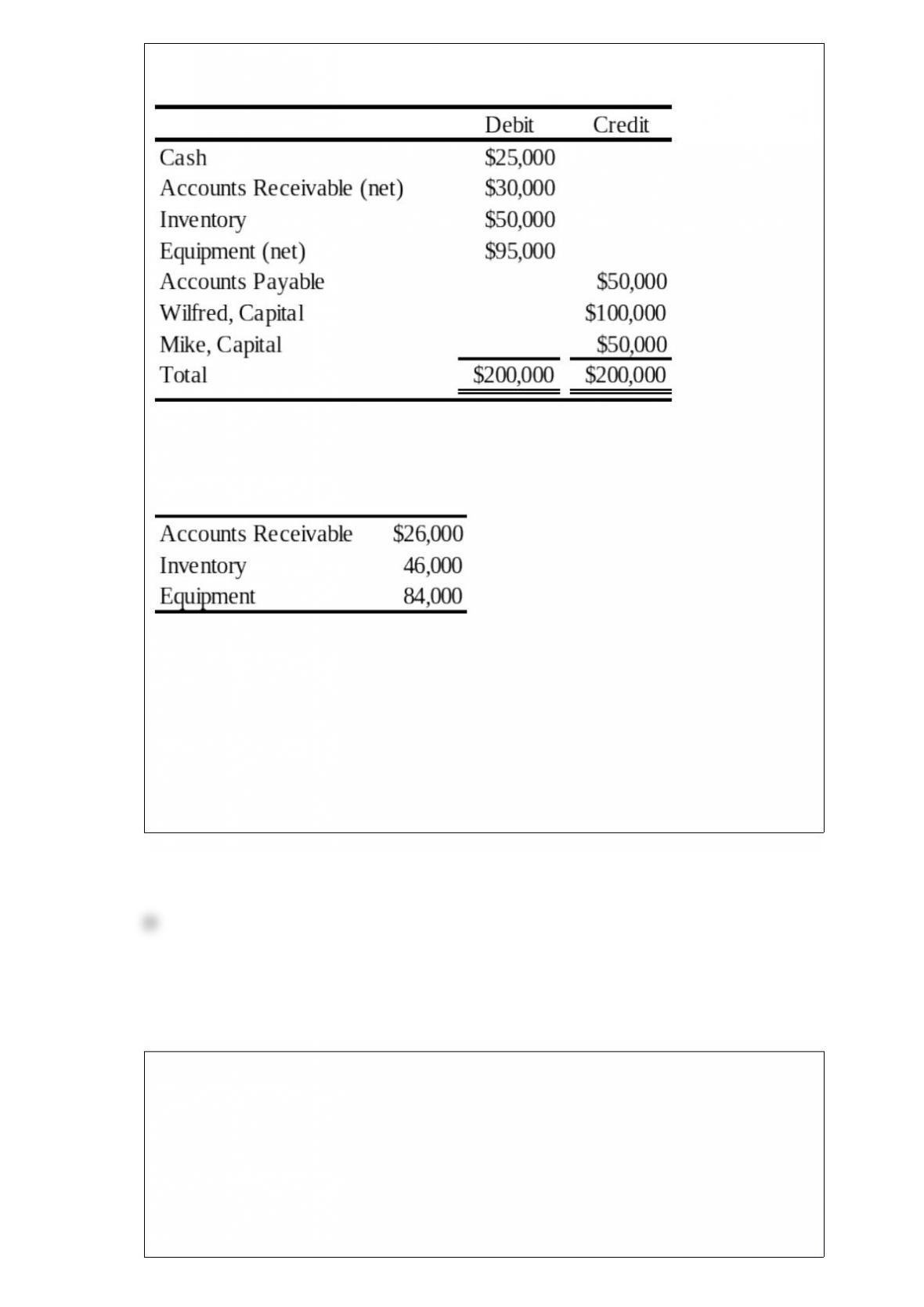

The trial balance of WM Partnership is as follows:

Wilfred and Mike decide to incorporate their partnership. The partnership’s books will

be closed, and new books will be used for W & M Corporation. The following

additional information is available:

1) The estimated fair values of the assets follow:

2)All assets and liabilities are transferred to the corporation.

3) The common stock is $10 par. Wilfred and Mike receive a total of 10,000 shares.

4) The partners share profits and losses in the ratio 7:3.

Based on the preceding information, the journal entry on the partnership’s books to

record distribution of stock to prior partners will include a debit to Mike, Capital for:

A. $38,010.

B. $31,500.

C. $42,000.

D. $44,300.

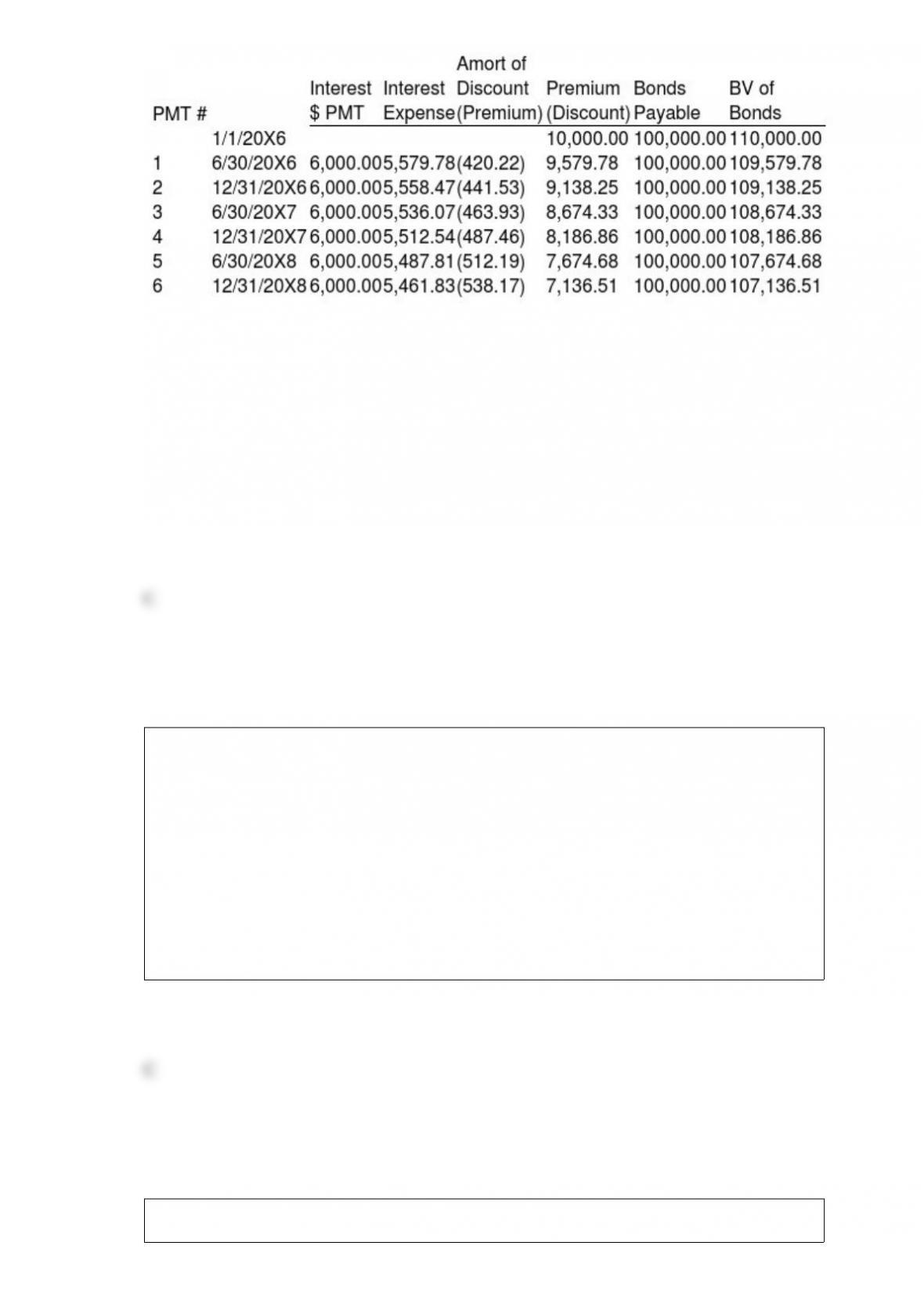

Hunter Corporation holds 80 percent of the voting shares of Moss Company. On

January 1, 20X8, Moss purchased $100,000 par value 12 percent Hunter bonds from

Cruse Corporation for $115,000. Hunter originally issued the bonds to Cruse on January

1, 20X6, for $110,000. The bonds have an 8-year maturity from the date of issue and

pay interest semiannually on June 30 and December 31 each year. Moss’ reported net

income of $65,000 for 20X8, and Hunter reported income (excluding income from

ownership of Moss’s stock) of $90,000. Hunter’s partial bond amortization schedule is

as follows:

Based on the information given above, what gain or loss on the retirement of bonds should

be reported in the 20X8 consolidated income statement?

A. $6,326 gain

B. $6,813 gain

C. $6,813 loss

D. $6,326 loss

A debt service fund of Clifton received $100,000 from its general fund during the fiscal

year ended June 30, 20X9. The cash was used to pay matured interest on Clifton’s

general obligation bonds, which were issued to finance construction of a new municipal

building. On the statement of revenues, expenditures, and changes in fund balance

prepared for the debt service fund for the year ended June 30, 20X9, the amount

received from the general fund should be reported as:

A. revenue.

B. a reduction of expenditures.

C. another financing source.

D. matured interest payments.

Sun Corporation owns 60 percent of Moon Company’s voting shares. On January 1,

20X4, Moon sold bonds with a par value of $400,000 when the market rate was 6

percent. Sun purchased one-third of the bonds; the remainder was sold to nonaffiliates.

The bonds mature in 15 years and pay an annual interest rate of 5 percent. Interest is

paid semiannually on June 30 and December 31.

Based on the information given above, what amount of interest expense will be

eliminated in the preparation of the 20X5 consolidated financial statements?

A. $7,224

B. $7,259

C. $14,516

D. $21,775

For a less-than-wholly-owned subsidiary, goodwill under the parent theory:

A. exceeds goodwill under the proprietary theory.

B. exceeds goodwill under the entity theory.

C. is less than goodwill under the entity theory.

D. is less than goodwill under the proprietary theory.

On June 30, 20X8, String Corporation incurred a $220,000 net loss from disposal of a

business component. Also, on June 30, 20X8, String paid $60,000 for property taxes

assessed for the calendar year 20X8. What amount of the preceding items should be

included in the determination of String’s net income or loss for the six-month interim

period ended June 30, 20X8?

A. $250,000

B. $220,000

C. $140,000

D. $280,000

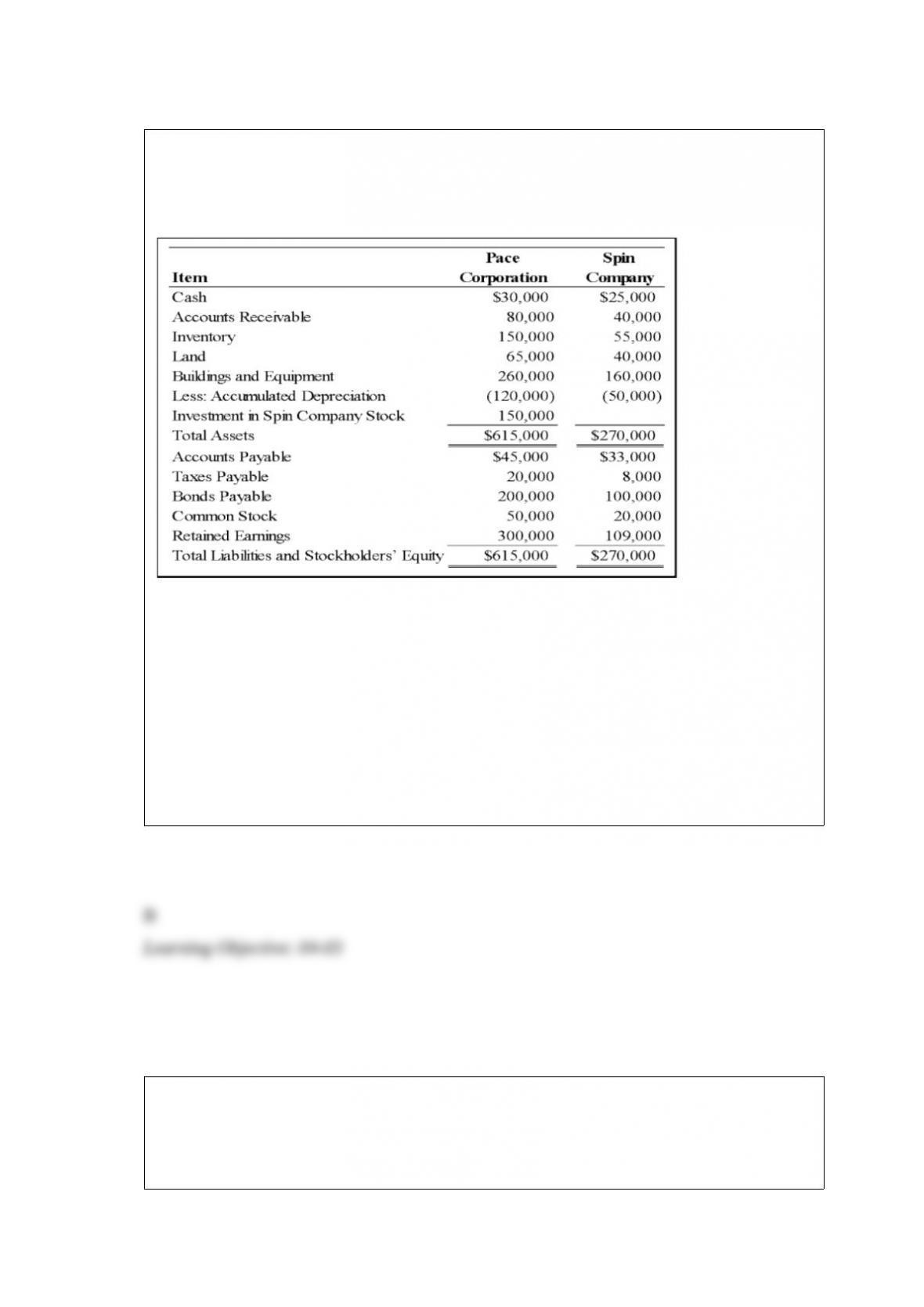

Pace Corporation acquired 100 percent of Spin Company’s common stock on January 1,

20X9. Balance sheet data for the two companies immediately following the acquisition

follow:

At the date of the business combination, the book values of Spin’s net assets and

liabilities approximated fair value except for inventory, which had a fair value of

$60,000, and land, which had a fair value of $50,000. The fair value of land for Pace

Corporation was estimated at $80,000 immediately prior to the acquisition.

Based on the preceding information, what is the differential associated with the

acquisition?

A. $15,000

B. $21,000

C. $6,000

D. $10,000

On January 2, 20X8, Johnson Company acquired a 100% interest in the capital stock of

Perth Company for $3,100,000. Any excess cost over book value is attributable to a

patent with a 10-year remaining life. At the date of acquisition, Perth’s balance sheet

contained the following information:

Perth’s income statement for 20X8 is as follows:

The balance sheet of Perth at December 31, 20X8, is as follows:

Perth declared and paid a dividend of 20,000 FCU on October 1, 20X8. Spot rates at

various dates for 20X8 follow:

Assume Perth’s revenues, purchases, operating expenses, depreciation expense, and

income taxes were incurred evenly throughout 20X8.

Refer to the above information. Assuming the U.S. dollar is the functional currency,

what is the balance in Johnson’s investment in foreign subsidiary account at December

31, 2008?

A. $3,303,400

B. $3,294,500

C. $3,323,400

D. $3,314,500

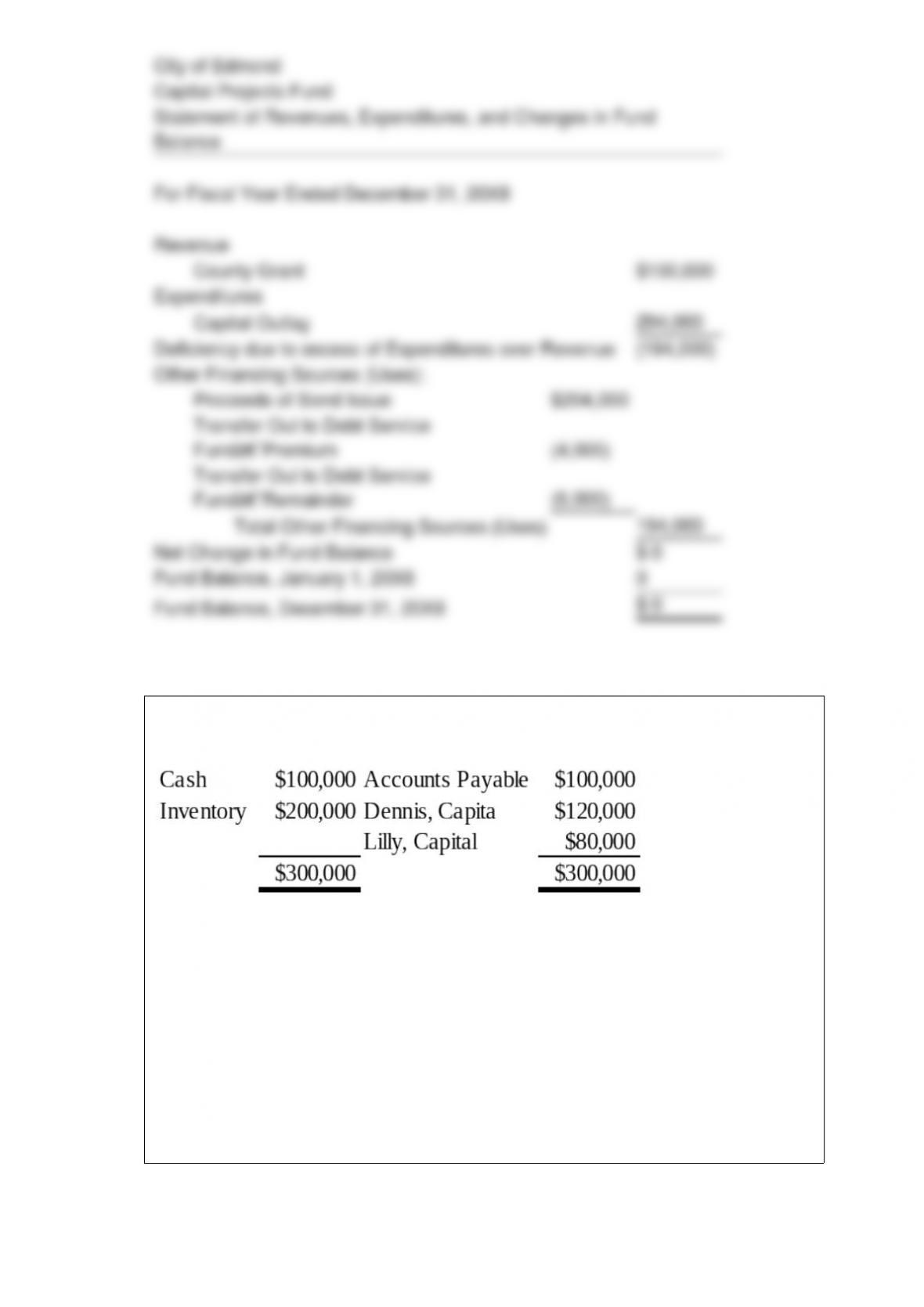

The City of Edmond established a capital projects fund for the construction of a reading

room for the City Library. The estimated cost of the construction is $300,000. On

January 1, 20X8, an 8 percent, $200,000 bond issue was sold at 102. At that date, the

county board provided a $100,000 grant. On March 3, 20X8, the premium from

issuance of the bonds was transferred to the debt service fund established to repay the

bond principal and interest. On March 1, 20X8, a general contractor’s bid was accepted

to construct the facility at a cost of $270,000. The construction was completed on

October 5, 20X8; its actual cost was $285,000. The city council approved payment of

the total actual cost of $285,000. In addition to the $285,000, $9,000 was spent to make

the facility ready for use. On November 3, 20X8, the city council gave the final

approval for both these payments. After all bills were paid, the remaining fund balance

was transferred to the debt service fund.

Required

a. Prepare entries for the capital projects fund for 20X8.

b. Prepare a statement of revenues, expenditures, and changes in fund balance for 20X8

for the capital projects fund.

Partners Dennis and Lilly have decided to liquidate their business. The following

information is available:

Dennis and Lilly share profits and losses in a 3:2 ratio. During the first month of

liquidation, half the inventory is sold for $60,000, and $60,000 of the accounts payable

is paid. During the second month, the rest of the inventory is sold for $45,000, and the

remaining accounts payable are paid. Cash is distributed at the end of each month, and

the liquidation is completed at the end of the second month.

Refer to the information provided above. Using a safe payments schedule, how much

cash will be distributed to Dennis at the end of the first month?

A. $64,000

B. $60,000

C. $24,000

D. $36,000

Which of the following characteristics would render the operating unit “reportable”?

The operating unit comprises at least:

A. 5 percent of the assets of a company as a whole.

B. 10 percent of the revenues of the company as a whole.

C. 50 percent of the long term debt of the company as a whole.

D. 20 percent of the operating profit of the company as a whole.

The transactions listed in the following questions occurred in a private, not-for-profit

hospital during 20X8. For each transaction, indicate its effect on the hospital’s statement

of operations for the year ended December 31, 20X8.

Transaction: Expended 50 percent of the contributions restricted for research in the

previous item.

Effect on Statement of Operations:

A. Increases operating income.

B. Decreases operating income.

C. The transaction is reported on the statement of operations, but there is no effect on

operating income.

D. The transaction is not reported on the statement of operations.

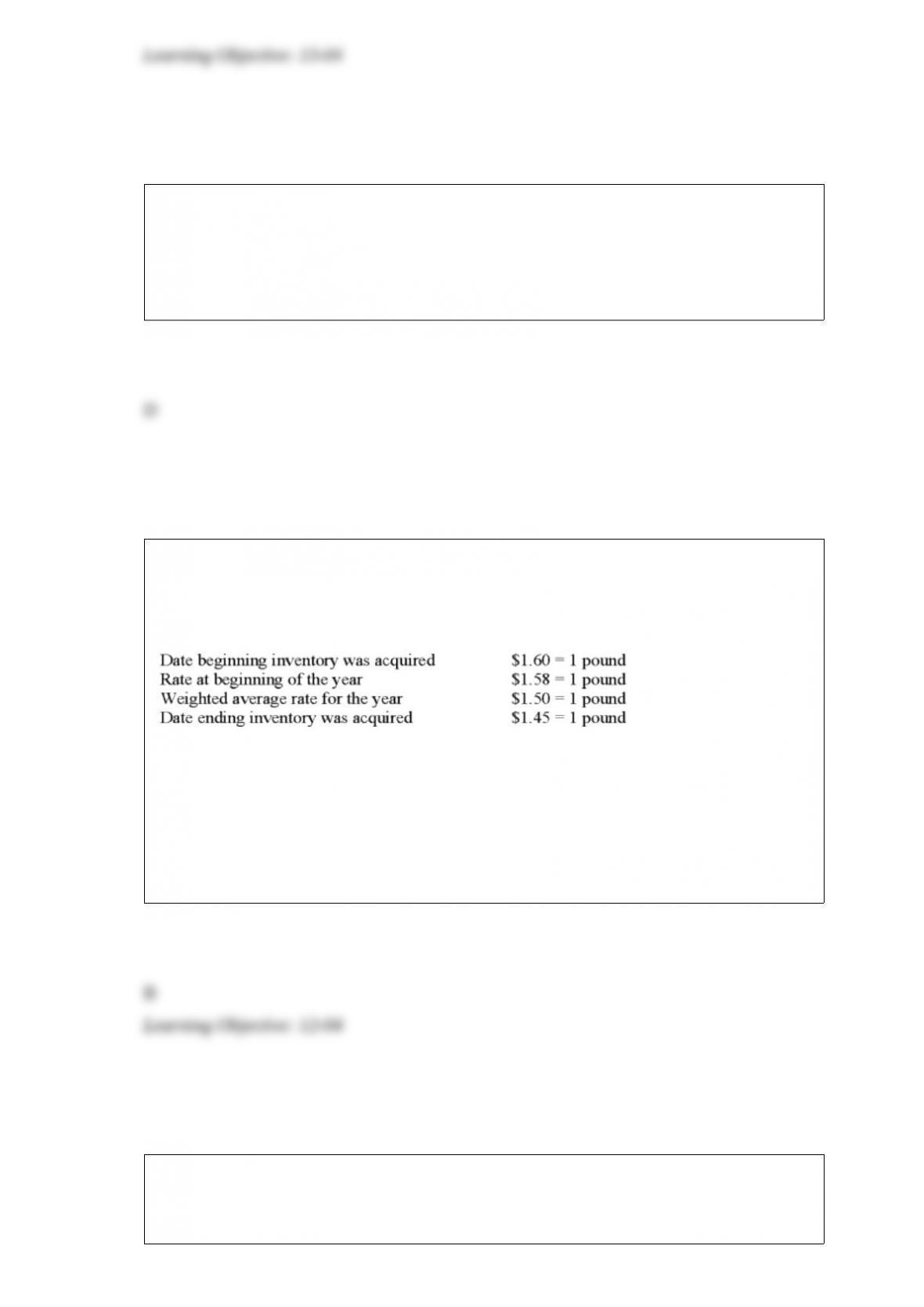

South Company is a subsidiary of North Company and is located in Malaysia, where

the currency is the ringgit. Data on South’s inventory and purchases are as follows:

Inventory, January 1, 20X4 30,000 ringgits

Purchases during 20X4 80,000 ringgits

Inventory, December 31, 20X4 20,000 ringgits

The beginning inventory was acquired during the fourth quarter of 20X3, and the

ending inventory was acquired during the fourth quarter of 20X4. Purchases were made

evenly during 20X4. Exchange rates were as follows:

Fourth quarter of 20X3 1 ringgit = $0.319

January 1, 20X4 1 ringgit = $0.318

Average during 20X4 1 ringgit = $0.315

Fourth quarter of 20X4 1 ringgit = $0.313

December 31, 20X4 1 ringgit = $0.31

Based on the preceding information, the translation of cost of goods sold for 20X4,

assuming that the Malaysian ringgit is the function currency is

A. $28,350

B. $28,480

C. $28,540

D. $28,470

Detroit based Auto Corporation, purchased ancillaries from a Japanese firm on

December 1, 20X8, for 1,000,000 Yen, when the spot rate for Yen was $.0095. On

December 31, 20X8, the spot rate stood at $.0096. On January 10, 20X9 Auto paid

1,000,000 Yen acquired at a rate of $.0094. Auto’s income statements should report a

foreign exchange gain or loss for the years ended December 31, 20X8 and 20X9 of:

On January 1, 20X8, Ramon Corporation acquired 75 percent of Tester Company’s

voting common stock for $300,000. At the time of the combination, Tester reported

common stock outstanding of $200,000 and retained earnings of $150,000, and the fair

value of the noncontrolling interest was $100,000. The book value of Tester’s net assets

approximated market value except for patents that had a market value of $50,000 more

than their book value. The patents had a remaining economic life of ten years at the date

of the business combination. Tester reported net income of $40,000 and paid dividends

of $10,000 during 20X8.

Based on the preceding information, which of the following is an consolidating entry

needed to prepare a full set of consolidated financial statements at December 31, 20X8:

A. Choice A

B. Choice B

C. Choice C

D. Choice D

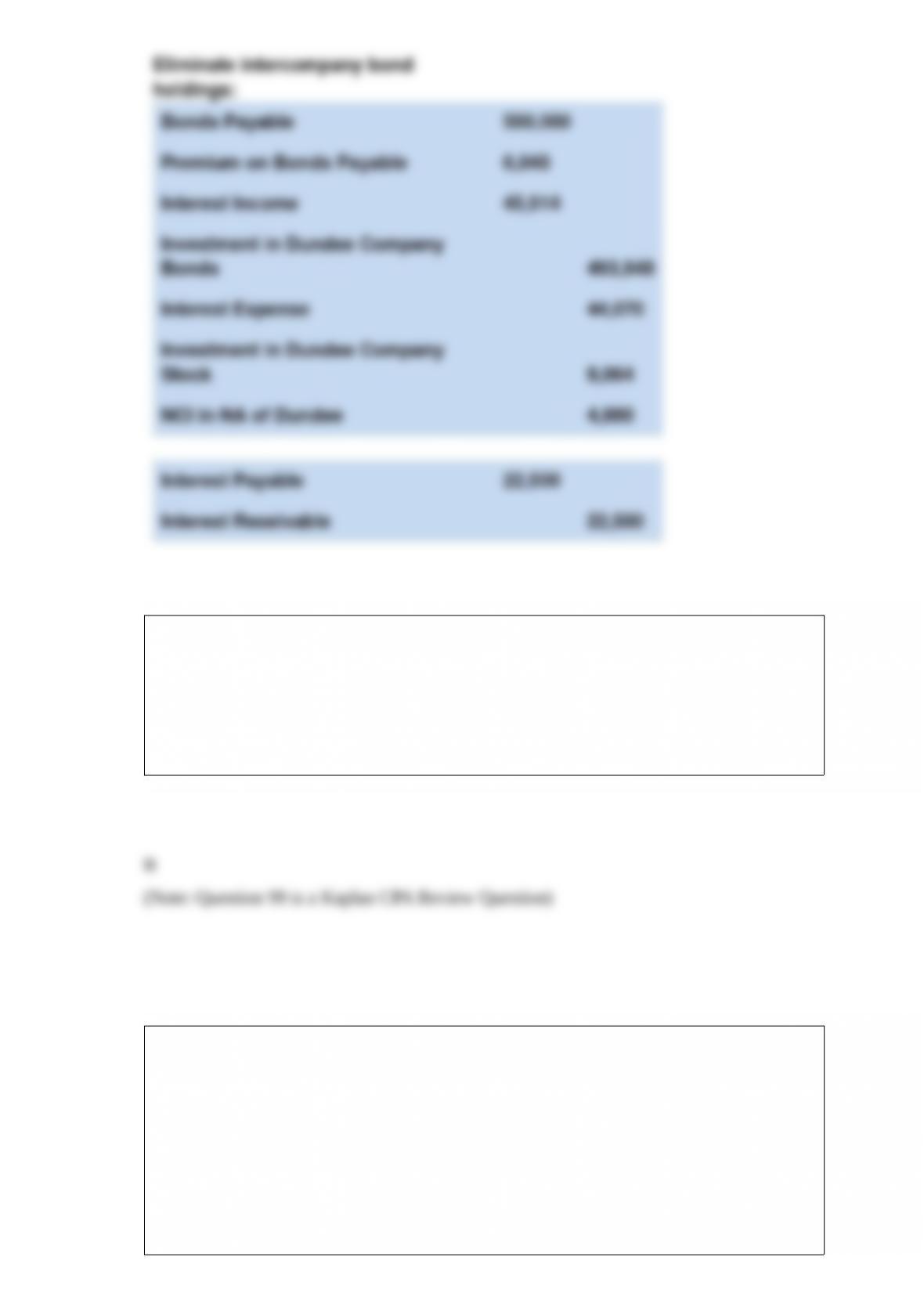

Master Corporation owns 85 percent of Servant Corporation’s voting shares. On

January 1, 20X8, Master Corporation sold $200,000 par value 8 percent bonds to

Servant when the market interest rate was 5 percent. The bonds mature in 10 years and

pay interest semiannually on June 30 and Dec 31.

Based on the information given above, in the preparation of the 20X8 consolidated

financial statements, interest income will be:

A. debited for $12,293 in the consolidating entries.

B. credited for $12,293 in the consolidating entries.

C. debited for $16,000 in the consolidating entries.

D. credited for $16,000 in the consolidating entries.

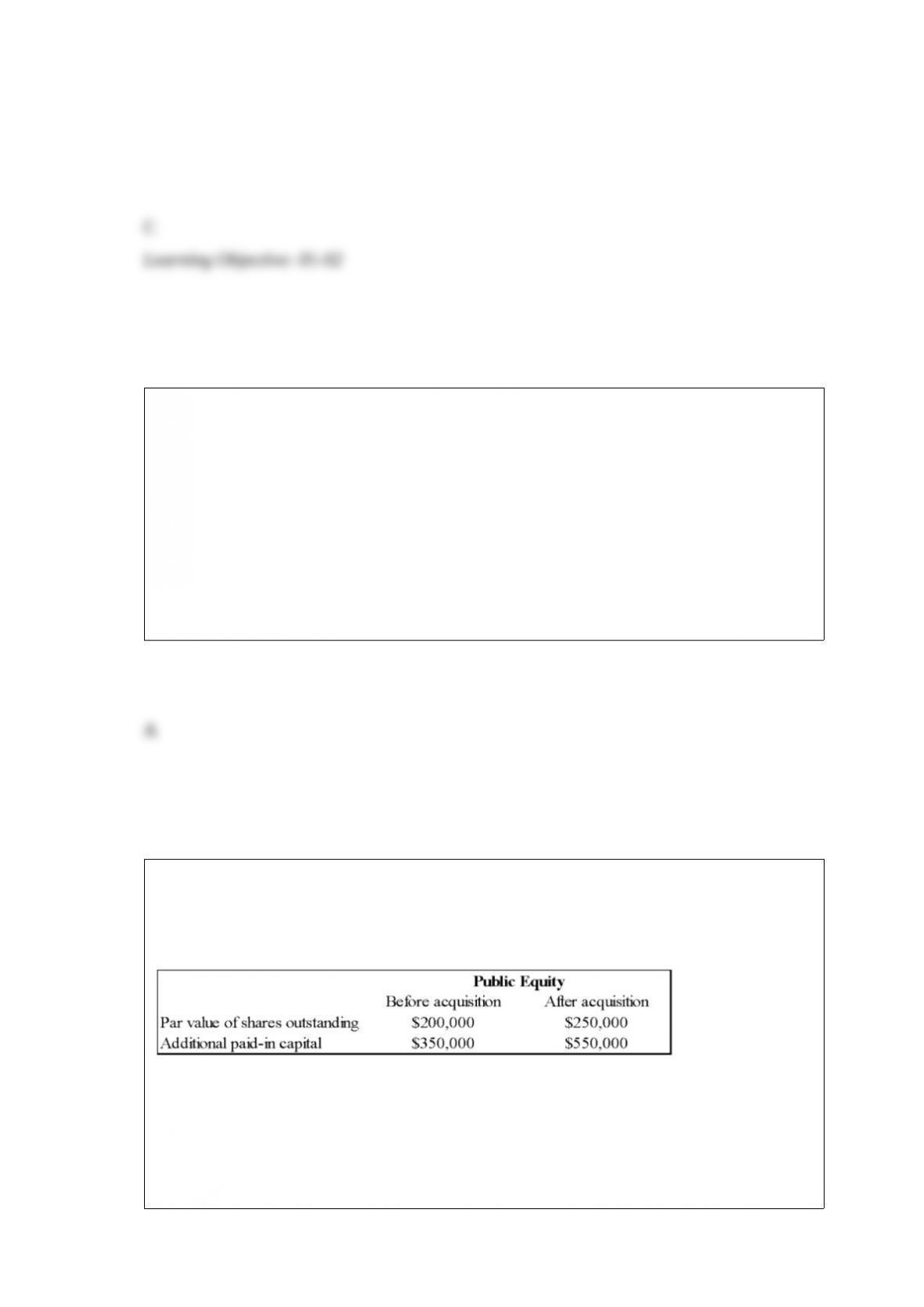

Public Equity Corporation acquired Lenore Company through an exchange of common

shares. All of Lenore’s assets and liabilities were immediately transferred to Public

Equity. Public’s common stock was trading at $20 per share at the time of exchange.

Following selected information is also available.

Based on the preceding information, what is the fair value of Lenore’s net assets, if

goodwill of $56,000 is recorded?

A. $306,000

B. $244,000

C. $194,000

D. $300,000

Company X acquires 100 percent of the voting shares of Company Y for $275,000 on

December 31, 20X8. The fair value of the net assets of Company X at the date of

acquisition was $300,000. This is an example of a(n):

A. positive differential.

B. bargain purchase.

C. extraordinary loss.

D. revaluation adjustment.

On January 1, 20X6, Interstate Corporation acquired 70 percent of Catapult Company’s

common stock for $210,000 cash. The fair value of the noncontrolling interest at that

date was determined to be $90,000. Data from the balance sheets of the two companies

included the following amounts as of the date of acquisition:

Interstate Catapult

Cash $50,000 $15,000

Accounts Receivable 70,000 25,000

Inventory 30,000 20,000

Land 150,000 80,000

Buildings and Equipment 250,000 200,000

Less: Accumulated Depreciation (70,000) (20,000)

Investment in Catapult Co. 210,000

Total Assets $690,000 $320,000

Accounts Payable $40,000 $10,000

Bonds Payable 150,000 40,000

Common Stock 300,000 90,000

Retained Earnings 200,000 180,000

Total Liabilities and Equity $690,000 $320,000

At the date of the business combination, the book values of Catapult’s assets and

liabilities approximated fair value except for inventory, which had a fair value of

$30,000, and land, which had a fair value of $95,000.

Based on the preceding information, what amount of total inventory will be reported in

the consolidated balance sheet prepared immediately after the business combination?

A. $20,000

B. $30,000

C. $50,000

D. $60,000

At any time, the remaining appropriating authority available to the fund managers is

equal to:

A. Appropriations minus Expenditures

B. Appropriations minus (Encumbrances + Expenditures)

C. Appropriations minus (Encumbrances – Expenditures)

D. Appropriations minus Encumbrances

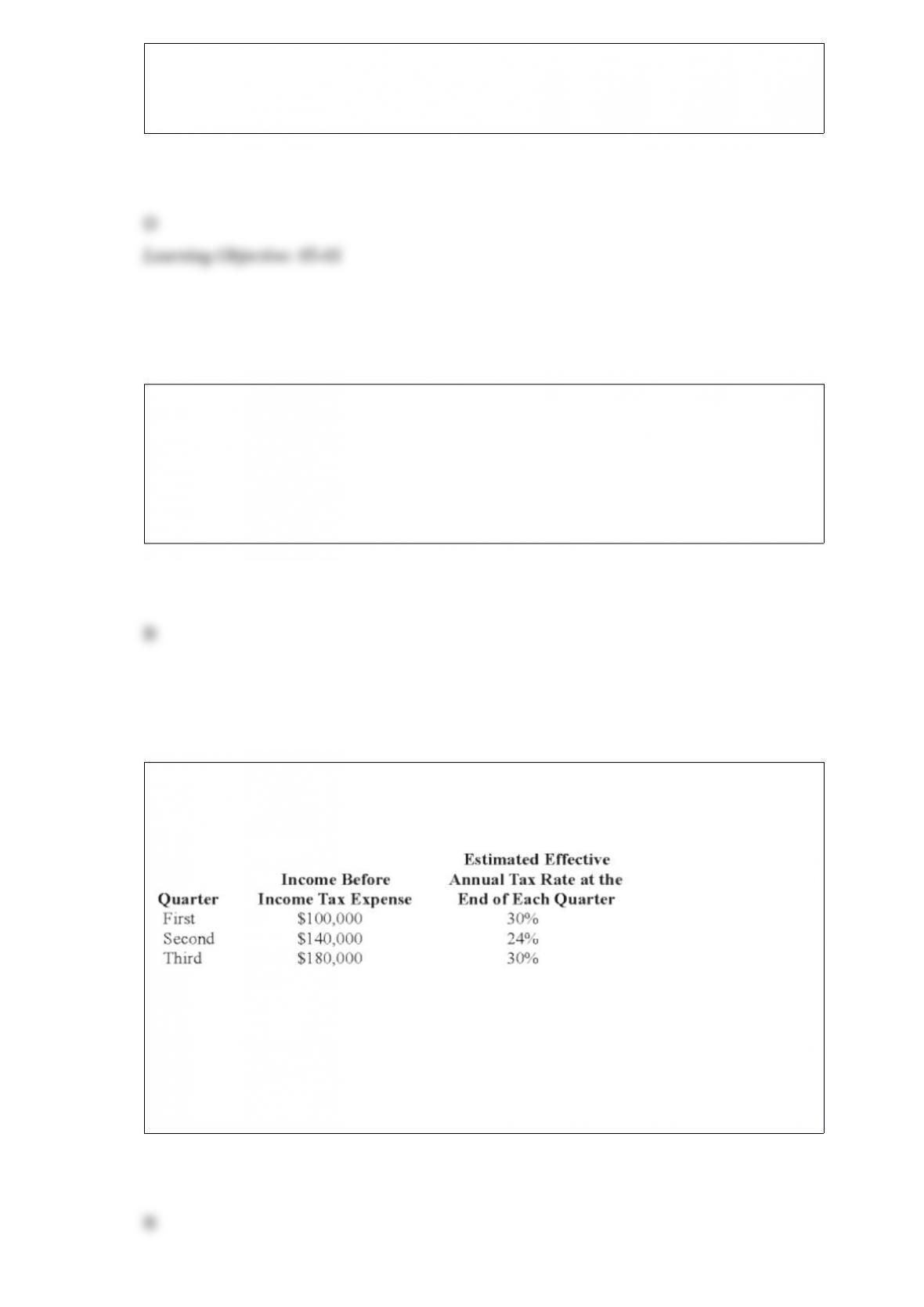

Denver Company, a calendar-year corporation, had the following actual income before

income tax expense and estimated effective annual income tax rates for the first three

quarters in 20X8:

Denver’s income tax expense in its interim income statement for the third quarter should

be:

A. $126,000.

B. $68,400.

C. $62,400.

D. $54,000.

Transferable interest of a partner includes all of the following except:

A. the partner’s share of the profits and losses of the partnership.

B. the right to receive distributions.

C. the right to receive any liquidating distribution.

D. the authority to transact any of the partnership’s business operations.

The British subsidiary of a U.S. company reported cost of goods sold of 75,000 pounds

(sterling) for the current year ended December 31. The beginning inventory was 10,000

pounds, and the ending inventory was 15,000 pounds. Spot rates for various dates are as

follows:

Assuming the pound is the functional currency of the British subsidiary, the translated

amount of cost of goods sold that should appear in the consolidated income statement

is:

A. $108,750.

B. $112,500.

C. $114,300.

D. $125,700.

A private, not-for-profit hospital received a donation of medicine from the Xengen

Pharmaceutical Company on February 13, 20X2. The cost of the medicine to the

company was $34,000, and its market value was $76,000. Thirty percent of the

medicine was used by the hospital during the year ended June 30, 20X2. On the

hospital’s statement of operations for the year ended June 30, 20X2, the contribution of

medicine would increase operating revenues by

A. $23,800.

B. $34,000.

C. $53,200.

D. $76,000.

Grum Corp., a publicly-owned corporation, is subject to the requirements for segment

reporting. In its income statement for the year ended December 31st, Grum reported

consolidated revenues of $50,000,000, operating expenses of $47,000,000, and net

income of $3,000,000. Operating expenses include payroll costs of $15,000,000.

Grum’s combined identifiable assets of all industry segments at December 31st, were

$40,000,000. In its year-end financial statements, Grum would be most likely to

disclose major customer data if sales to any single customer amounted to at least:

A. $1,500,000

B. $300,000

C. $5,000,000

D. $4,000,000

On December 31, 20X8, Mercury Corporation acquired 100 percent ownership of

Saturn Corporation. On that date, Saturn reported assets and liabilities with book values

of $300,000 and $100,000, respectively, common stock outstanding of $50,000, and

retained earnings of $150,000. The book values and fair values of Saturn’s assets and

liabilities were identical except for land which had increased in value by $10,000 and

inventories which had decreased by $5,000.

Based on the preceding information, what amount of goodwill will be reported if the

acquisition price was $195,000?

A. $0

B. $40,000

C. $15,000

D. $35,000

Dundee Company issued $1,000,000 par value 10-year bonds at 102 on January 1,

20X5, which Mega Corporation purchased. The coupon rate on the bonds is 9 percent.

Interest payments are made semiannually on July 1 and January 1. On Jan 1, 20X8,

Perth Company purchased $500,000 par value of the bonds from Mega for $492,200.

Perth owns 65 percent of Dundee’s voting shares.

Required:

a. What amount of gain or loss will be reported in Dundee’s 20X8 income statement on

the retirement of bonds?

b. Will a gain or loss be reported in the 20X8 consolidated financial statements for

Perth for the constructive retirement of bonds? What amount will be reported?

c. How much will Perth’s purchase of the bonds change consolidated net income for

20X8?

d. Prepare the worksheet consolidating entry or entries needed to remove the effects of

the intercorporate bond ownership in preparing consolidated financial statements at

December 31, 20X8.

e. Prepare the worksheet consolidating entry or entries needed to remove the effects of

the intercorporate bond ownership in preparing consolidated financial statements at

December 31, 20X9.

Reporting requirements of other not-for-profit entities (ONPOs) are similar to those of

which of the following entities?

A. A public university

B. A voluntary health and welfare organization

C. An enterprise fund of a state or local government

D. A hospital operated by a county government

Master Corporation owns 85 percent of Servant Corporation’s voting shares. On

January 1, 20X8, Master Corporation sold $200,000 par value 8 percent bonds to

Servant when the market interest rate was 5 percent. The bonds mature in 10 years and

pay interest semiannually on June 30 and Dec 31.

Based on the information given above, what amount of investment in bonds will be

eliminated in the preparation of the 20X8 consolidated financial statements?

A. $243,060

B. $200,000

C. $246,767

D. $156,940

The balance in Newsprint Corp.’s foreign exchange loss account was $10,000 on

December 31, 20X8, before any necessary year-end adjustment relating to the

following:

(1) Newsprint had a $15,000 debit resulting from the restatement in dollars of the

accounts of its wholly owned foreign subsidiary for the year ended December 31, 20X8.

(2) Newsprint had an account payable to an unrelated foreign supplier, payable in the

supplier’s local currency unit (LCU) on January 15, 20X9. The U.S. dollar–equivalent

of the payable was $50,000 on the December 1, 20X8, invoice date and $53,000 on

December 31, 20X8.

Based on the information provided, in Newsprint’s 20X8 consolidated income

statement, what amount should be included as foreign exchange loss in computing net

income, if the U.S. dollar is the functional currency and the remeasurement method is

appropriate?

A. $15,000

B. $10,000

C. $25,000

D. $28,000