Chapter 07 – Intercompany Transfers of Noncurrent Assets and Services

E7-2 (continued)

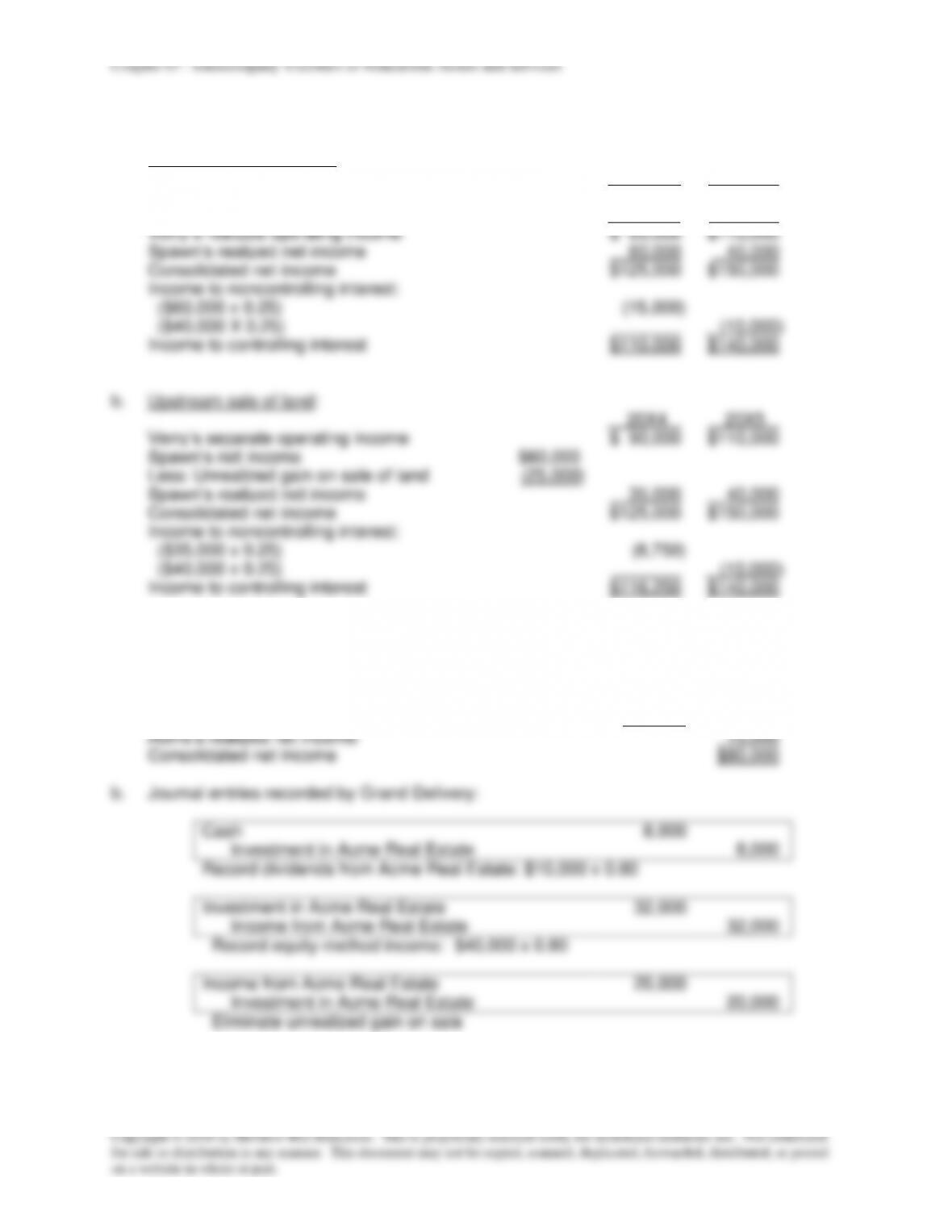

5.

b –

Reported net income of Gold Company

$ 45,000

Reported gain on sale of equipment

$15,000

Intercompany profit realized in 20X6

(5,000)

(10,000)

Realized net income of Gold Company

$ 35,000

Proportion of stock held by

noncontrolling interest

x .40

Income assigned to noncontrolling interests

$ 14,000

6.

c –

Operating income reported by Top Corporation

$ 85,000

Net income reported by Gold Company

45,000

$130,000

Less: Unrealized gain on sale of equipment

($15,000 – $5,000)

(10,000)

Consolidated net income

$120,000

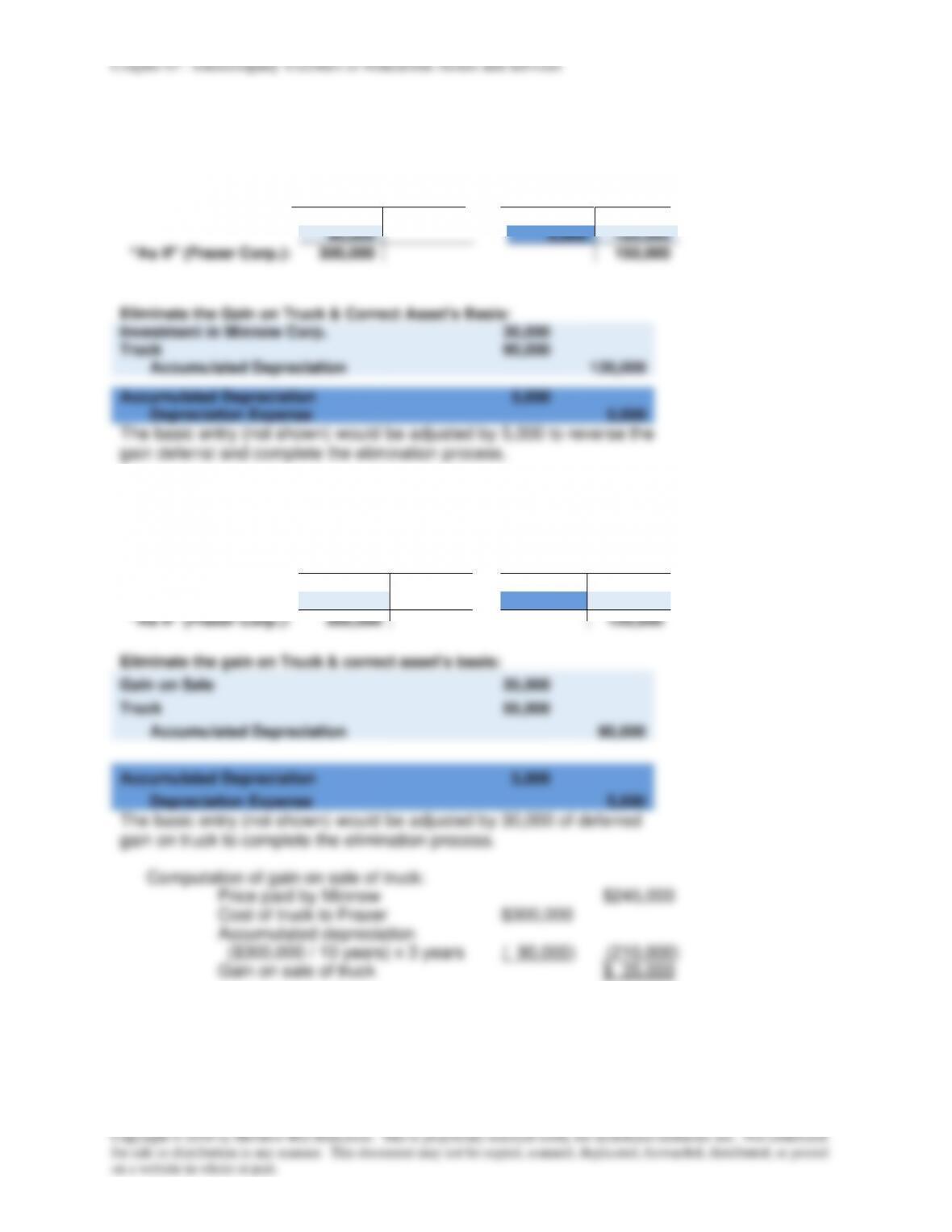

E7-3 Consolidation Entries for Land Transfer

a.

Consolidation entry, December 31, 20X4:

Gain on Sale of Land

10,000

Land

10,000

The basic entry (not shown) would be adjusted by 10,000 of deferred gain

on land to complete the elimination process.

Consolidation entry, December 31, 20X5:

Investment in Lowly

10,000

Land

10,000

The basic entry (not shown) would complete the elimination process.

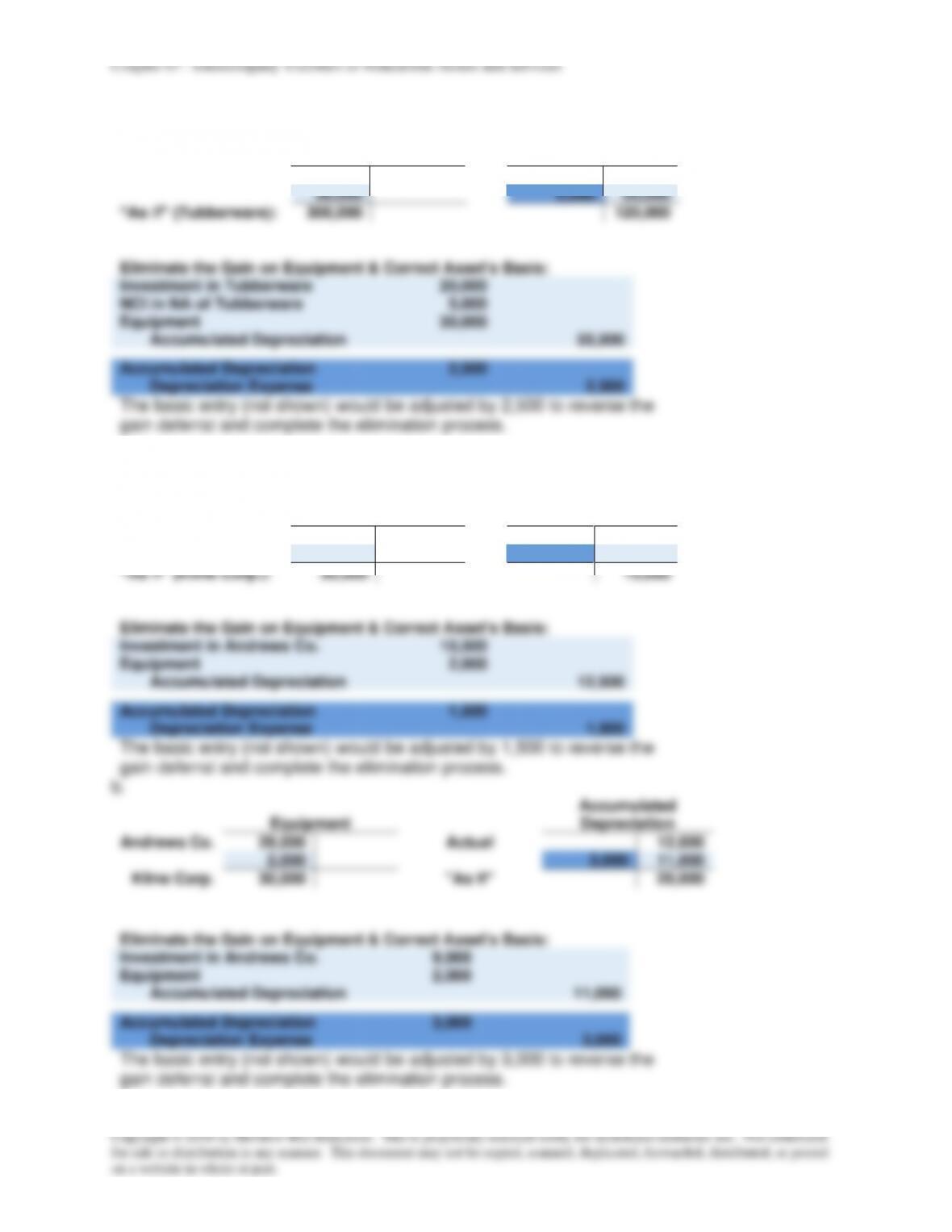

b.

Consolidation entry, December 31, 20X4:

Gain on Sale of Land

10,000

Land

10,000

The basic entry (not shown) would be adjusted by 10,000 of deferred gain

on land to complete the elimination process.

Consolidation entry, December 31, 20X5:

Investment in Lowly

6,000

NCI in NA of Lowly

4,000

Land

10,000