Chapter 02 – REPORTING INTERCORPORATE INTERESTS

2-9

DESCRIPTIONS OF CASES, EXERCISES, AND PROBLEMS

C2-1A

20 min.

LO 2-2,

LO 2-3

E

Choice of Accounting Method

The criteria used in determining significant influence are reviewed. Students also

must specify when investment income will be greater under the cost method and

when it will be greater under the equity method. They should also explain why

the use of the equity method becomes more appropriate as the percentage of

ownership increases.

C2-2

30 min.

LO 2-2,

LO 2-3

M

Intercorporate Ownership

Students are required to research current authoritative pronouncements and

develop a memorandum to management supporting the use of either the cost or

equity method in accounting for the company’s investment. They should support

their findings with citations and quotations from the appropriate literature.

C2-3A

30 min.

LO 2-2,

LO 2-3

M

Application of the Equity Method

Students must review authoritative pronouncements to determine whether the

company should utilize the cost or equity method subsequent to the sale of part of

its investment. Students must prepare a memorandum to the controller and

outline and support their opinion.

C2-4

25 min.

LO 2-6,

LO 2-7

M

Need for Consolidation Process

An effective answer to this case requires an understanding of which balances

must be eliminated in order to avoid misstating the consolidated balance sheet

totals.

C2-5

25 min.

LO 2-1

M

Account Presentation

Students must research authoritative literature to determine the proper way of

combining account balances from different subsidiaries. A memorandum that

reports findings and provides the necessary supporting references is required.

C2-6

25 min.

LO 2-6,

LO 2-7

M

Consolidating an Unprofitable Subsidiary

An unprofitable venture is currently consolidated with a profitable entity without

separately disclosing the loss. Students must research the issue to determine if

disclosure is necessary, and describe what type of disclosures will be necessary in

the financial statement notes or the management discussion. Reference to

authoritative literature must be included in a memorandum to the treasurer.

E2-1

15 min.

LO 2-2,

LO 2-3

E

Multiple-Choice Questions on Use of Cost and Equity Methods

[AICPA Adapted]

Six multiple-choice questions deal with basic applications of the cost and equity

methods and when each should be used.

Chapter 02 – REPORTING INTERCORPORATE INTERESTS

2–10

E2-2

5 min.

LO 2-4

M

Multiple Choice Questions on Intercorporate Investments

Two multiple-choice questions deal with conceptual issues related to the cost and

equity methods.

E2-3

15 min.

LO 2-3

M

Multiple-Choice Questions on Applying Equity Method

[AICPA Adapted] Four multiple-choice questions focus primarily on the

computation of equity method income.

E2-4

20 min.

LO 2-4

E

Cost versus Equity Reporting

Students must compute the income to be reported for three years under the (a)

cost method and (b) the equity method. Liquidating dividends exist for the cost

method.

E2-5

10 min.

LO 2-2,

LO 2-3

E

Acquisition Price

Given the net income and dividend payments of an investee for a three-year

period and the ending balance in the investment account on the investor’s books,

the acquisition price paid by the investor is computed under cost and equity

method reporting.

E2-6

20 min.

LO 2-2,

LO 2-3

M

Investment Income

The investor’s income is computed for a four-year period using both the cost and

equity methods. Journal entries for the final year are recorded under both

methods. Dividends in excess of earnings are paid in the third year.

E2-7

15 min.

LO 2-3

E

Investment Value

Calculation of the investment account balance is required for three consecutive

years.

E2-8A

5 min.

LO 2-2,

LO 2-3

E

Income Reporting

Separate recognition of an extraordinary gain reported by the investee is required

on an investor’s books.

E2-9

15 min.

LO 2-4,

LO 2-5

M

Fair Value Method

Net income has to be calculated under three methods – cost, equity, and fair

value methods.

E2-10

15 min.

LO 2-3,

LO 2-5

M

Fair Value Recognition

Journal entries are required for all transactions occurring during the year of

purchase assuming that the investor utilizes (1) the equity method and (2) the fair

value method.

Chapter 02 – REPORTING INTERCORPORATE INTERESTS

2–11

E2-11A

15 min.

LO 2-3,

LO 2-5

M

Investee with Preferred Stock Outstanding

Journal entries must be given for the investor under the equity method. Preferred

stock information is provided.

E2-12A

15 min.

LO 2-2,

LO 2-3

M

Other Comprehensive Income Reported by Investee

Journal entries must be given for the investor. Operating income and other

comprehensive income reported by the investee is provided.

E2-13A

10 min.

LO 2-2,

LO 2-3

E

Other Comprehensive Income Reported by Investee

The investee records an operating loss in the first year and a gain in the second

year. Dividends are paid in both years. It also reports other comprehensive

income in the second year. The balance in the investor’s equity-method

investment account is given at the end of the second year. The purchase price

must be calculated.

E2-14

20 min.

LO 2-7

M

Basic Consolidation Entry

Consolidation entry is required assuming acquisition of 100% of an investee’s

stock.

E2-15

25 min.

LO 2-6,

LO 2-7

E

Balance Sheet Worksheet

A simple balance sheet worksheet following the business consolidation is

required. An entry for elimination of the investment account and the

stockholders’ equity balances of the subsidiary is needed.

E2-16

40 min.

LO 2-3,

LO 2-7

M

Consolidation Entries for Wholly Owned Subsidiary

Students must prepare journal entries for an acquisition using the equity method.

Consolidation entries to prepare consolidated financial statements are required.

E2-17

15 min.

LO 2-3,

LO 2-7

E

Basic Consolidation Entries for Fully Owned Subsidiary

Journal entries recorded by the parent company and the consolidation entries

needed to prepare consolidated statements at the end of the first year of

ownership are required for a fully-owned subsidiary.

P2-18

20 min.

LO 2-2,

LO 2-3

H

Retroactive Recognition

Students must show the journal entries to be recorded on an investor’s books

assuming that an increase in the percentage ownership over the past three years

requires retroactive application of the equity method.

P2-19

20 min.

LO 2-4,

LO 2-5

M

Fair Value Method

Investment income and the balances in the investment account are to be

calculated for three years, assuming the cost method, the equity method, and the

fair value method.

Chapter 02 – REPORTING INTERCORPORATE INTERESTS

2–12

P2-20

15 min.

LO 2-5

M

Fair Value Journal entries

All journal entries made by the investor are required for two years, assuming the

usage of the fair value method.

P2-21A

25 min.

LO 2-5

H

Other Comprehensive Income Reported by Investee

An investee reports other comprehensive income during the period. Students

must compute the equity-method income reported for the year, the increase in the

balance in the investment account for the year, the amount of other

comprehensive income reported by the investee, and the market value of the

securities reported as available-for-sale by the investee at the end of the year.

P2-22A

45 min.

LO 2-3,

LO 2-7

H

Equity-Method Income Statement

An income statement and a retained earnings statement for both the investee and

investor must be prepared. The investee has discontinued operations, an

extraordinary item, and a cumulative adjustment from a change of accounting

principle. This problem presents a good review of income statement disclosures

for the investee and the resulting disclosures needed in the financial statements of

the investor.

P2-23

30 min.

LO 2-3,

LO 2-6,

LO 2-7

M

Consolidated Worksheet at End of the First Year of Ownership (Equity

Method) Students are asked to prepare journal entries on a parent company’s

books at the time of an acquisition and then to prepare a consolidation worksheet

at the end of the first year.

P2-24

30 min.

LO 2-3,

LO 2-6,

LO 2-7

M

Consolidated Worksheet at End of the Second Year of Ownership (Equity

Method) As a continuation of P2-23, students are asked to prepare equity method

journal entries on a parent company’s books related to the subsidiary and then to

prepare a consolidation worksheet at the end of the second year.

P2-25

35 min.

LO 2-3,

LO 2-6,

LO 2-7

M

Consolidated Worksheet at End of the First Year of Ownership (Equity

Method) Students are asked to prepare journal entries on a parent company’s

books at the time of an acquisition and then to prepare a consolidation worksheet

at the end of the first year.

P2-26

35 min.

LO 2-3,

LO 2-6,

LO 2-7

M

Consolidated Worksheet at End of the Second Year of Ownership (Equity

Method) As a continuation of P2-25, students are asked to prepare equity method

journal entries on a parent company’s books related to the subsidiary and then to

prepare a consolidation worksheet at the end of the second year.

Chapter 02 – REPORTING INTERCORPORATE INTERESTS

2–13

P2-27B

30 min.

LO 2-2,

LO 2-6,

LO 2-7

M

Consolidated Worksheet at End of the First Year of Ownership (Cost

Method) This problem uses the same data as provided in P2-23 except that it

assumes the parent uses the cost method for subsidiary investments. Students are

asked to prepare journal entries on a parent company’s books at the time of an

acquisition and then to prepare a consolidation worksheet at the end of the first

year.

P2-28B

30 min.

LO 2-2,

LO 2-6,

LO 2-7

M

Consolidated Worksheet at End of the Second Year of Ownership (Cost

Method) This problem uses the same data as provided in P2-24 except that it

assumes the parent uses the cost method for subsidiary investments. As a

continuation of P2-27, students are asked to prepare any cost method journal

entries on a parent company’s books related to the subsidiary and then to prepare

a consolidation worksheet at the end of the second year.

OTHER RESOURCES

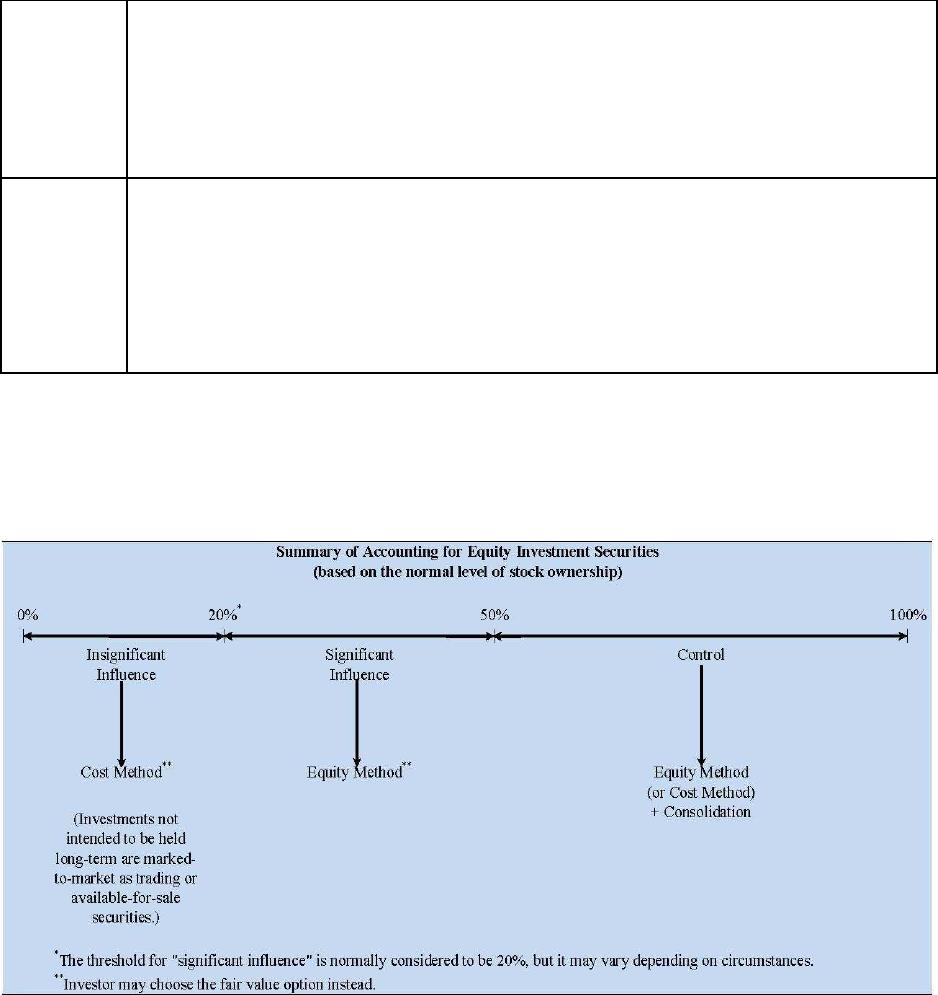

Level of Ownership and Accounting and Reporting

Chapter 02 – REPORTING INTERCORPORATE INTERESTS

2–14

Chapter 2

Investment Example

On July 1, 20X8, A Company purchases a 20 percent ownership interest in B Company for $500.

At this date, the book value of B’s assets is $2,000 and the fair value of B’s depreciable assets is

$300 greater than book value. Depreciable assets have a remaining economic life of 10 years.

Goodwill is not amortized.

B Company reports net income of $400 for the year, earned evenly throughout the year.

Dividends of $300 are declared and paid on December 31.

A. Assume that A Company is able to exert significant influence over B Company.

B. Assume that A Company is unable to exert significant influence over B Company.

A. EQUITY METHOD

Changes in Investment Account and Calculation of End of Period Balance:

Income from Equity Investment:

$40

Less: Amortization (3)

$37

Income from Investment

7/1/X8

B’s BOOK VALUE ON 7/1/X8 $2,000

Investment cost $500

Book value ($2,000 x .20) (400)

Excess of Cost over B.V. $100

Revalue asset (300 x 0.20) 60

(Depreciated over 10 years)

Goodwill $40

Original Cost $500

Plus: Income from Investment 40

($400 x 0.20 x 0.5 years)

Less: Amortization (3)

[($60/10years) x 0.5 years]

Less: Dividends (60)

$477

Chapter 02 – REPORTING INTERCORPORATE INTERESTS

2–15

B. COST METHOD

Dividend on December 31:

Total

20%

Income from 7/1 to 12/31

$200

$40

Dividend on December 31

(300)

(60)

Preacquisition earnings distributed

$(100)

$(20)

(Return of Investment Capital)

Changes in Investment Account and Calculation of End of Period Balance:

Original Cost: $500

Less: Return of Capital (20)

Ending Balance $480

Income from Equity Investment:

Dividend Income $40

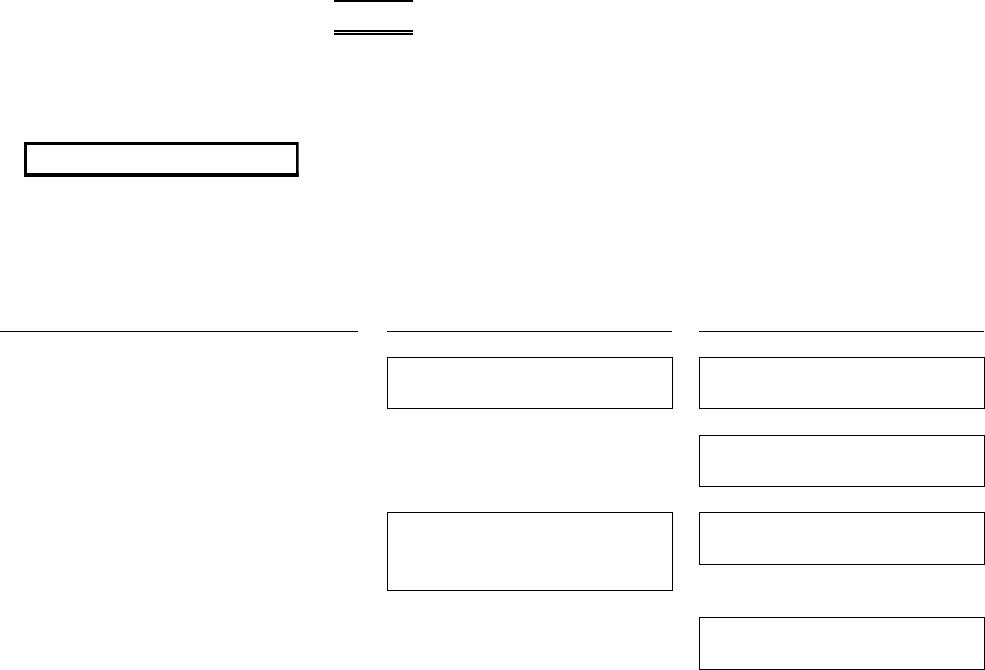

COMPARISON OF COST AND EQUITY METHODS

Transaction

COST METHOD

EQUITY METHOD

1.) Acquired stock

Investment

500

Investment

500

Cash

500

Cash

500

2.) Investee reports income

— no entry —

Investment

40

Income-Invest.

40

3.) Investee declares cash dividends

Cash

60

Cash

60

Div. Income

40

Investment

60

Investment

20

4.) Amortization of differential

— no entry —

Income-Invest.

3

Investment

3