Chapter 3 – THE REPORTING ENTITY AND CONSOLIDATION OF LESS-THAN-WHOLLY-OWNED

SUBSIDIARIES WITH NO DIFFERENTIAL

CHAPTER 3

THE REPORTING ENTITY AND CONSOLIDATION OF LESS-THAN-

WHOLLY-OWNED SUBSIDIARIES WITH NO DIFFERENTIAL

IMPORTANT NOTE TO INSTRUCTORS

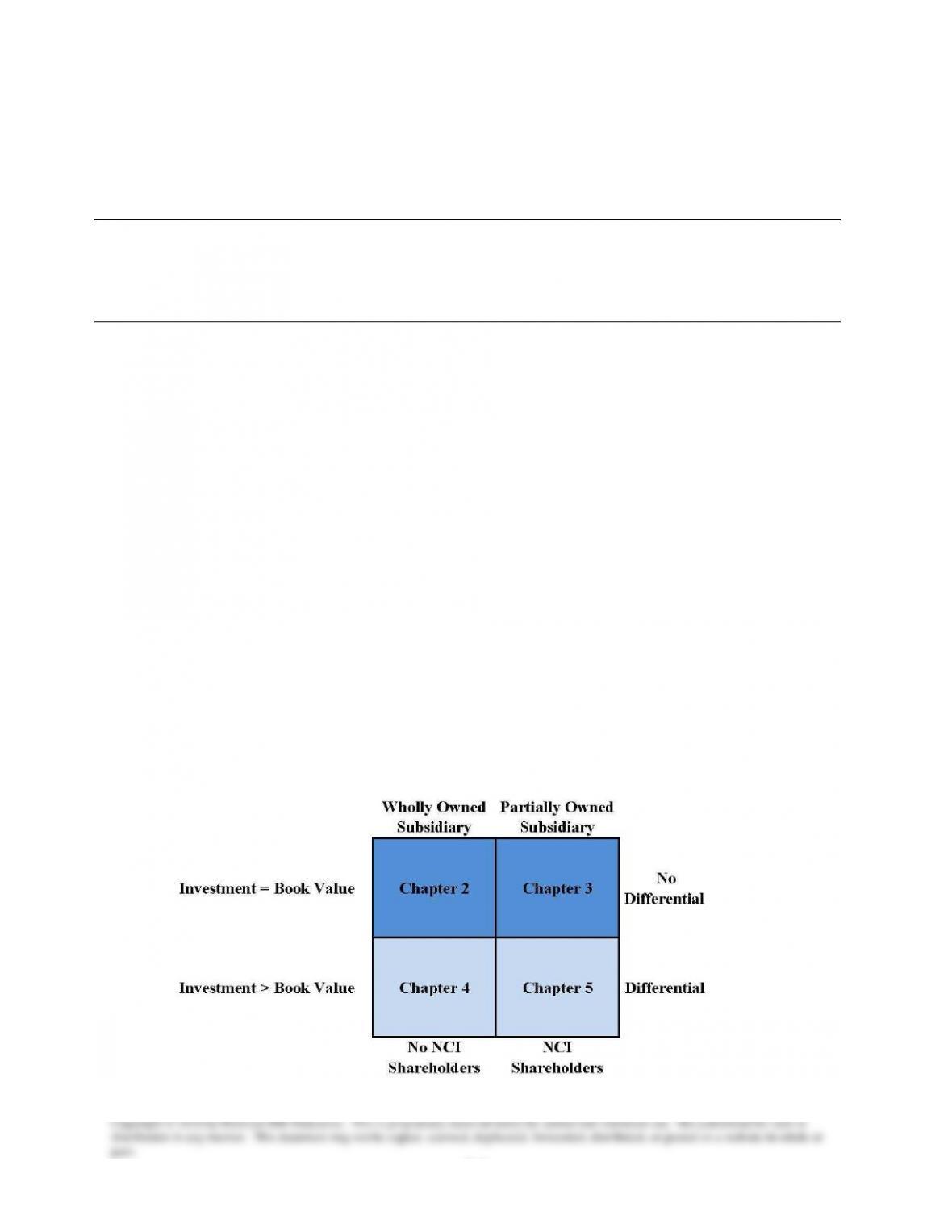

The 11th edition uses a building block approach to our coverage of consolidation in

chapters 2 through 5. Chapter 2 introduces our coverage of consolidation in the most basic

setting when the subsidiary is either created or purchased at an amount equal to the book value of

the subsidiary’s underlying net assets.

Chapter 3 explains how the basic consolidation process changes when the parent

company owns less than 100 percent of the subsidiary. Chapter 4 shows how the consolidation

process differs when the parent company acquires the subsidiary for an amount greater (or less)

than the book value of the subsidiary’s net assets. Finally, Chapter 5 presents the most complex

consolidation scenario (where the parent owns less than 100 percent of the subsidiary’s

outstanding voting stock and the acquisition price is not equal to the book value of the

subsidiary’s net assets). In order to facilitate this new approach, we emphasize that this edition

includes consolidation entries used in consolidation to facilitate the elimination of the investment

in a subsidiary in two steps: (1) first the book value portion of the investment and income from

the subsidiary are eliminated and (2) then the differential portion of the investment and income

from subsidiary are eliminated with separate entries. We believe that this approach is more

intuitive for students.

Chapter 03 – THE REPORTING ENTITY AND CONSOLIDATED FINANCIAL STATEMENTS

3-2

OVERVIEW OF CHAPTER 3

Chapter 3 is the second in a series of chapters that focuses on the preparation of

consolidated financial statements. The first portion of the chapter contains a discussion of the

usefulness of consolidated statements and when it is appropriate to prepare them. It then

identifies the stakeholders who are likely to find consolidated statements useful. It also discusses

some limitations of consolidated financial statements. The chapter also identifies and explains

(1) conditions needed to establish and exercise control and (2) other consolidation criteria.

Chapter 3 next explains the computation and presentation of the non-controlling interest.

It also discusses combined financial statements.

The Additional Considerations portion of the chapter presents three theories of

consolidation: the proprietary theory, the parent company theory, and the entity theory. The

chapter illustrates the effects of different approaches to the preparation of consolidated financial

statements and discusses current practice

The chapter also explains and illustrates how consolidation differs when the parent

company owns less than 100 percent of the subsidiary.

The chapter next introduces special purpose and variable interest entities and explains

how accounting guidance and standards related to SPEs and VIEs currently differ between U.S.

GAAP and IFRS.

Finally, Appendix 3A provides a brief presentation of the consolidation of variable

interest entities.

LEARNING OBJECTIVES

When students finish studying this chapter, they should be able to:

LO 3-1 Understand and explain the usefulness and limitations of consolidated financial

statements.

LO 3-2 Understand and explain how direct and indirect control influence the

consolidation of a subsidiary.

LO 2-3 Understand and explain differences in the consolidation process when the

subsidiary is not wholly owned.

LO 3-4 Make calculations for the consolidation of a less-than-wholly-owned subsidiary.

LO 3-5 Prepare a consolidation worksheet for a less-than-wholly-owned subsidiary.

LO 3-6 Understand and explain the purpose of combined financial statements and how

they differ from consolidated financial statements.

LO 3-7 Understand and explain rules related to the consolidation of variable interest

entities.

LO 3-8 Understand and explain differences in consolidation rules under U.S. GAAP and

IFRS.

Chapter 03 – THE REPORTING ENTITY AND CONSOLIDATED FINANCIAL STATEMENTS

3-3

SYNOPSIS OF CHAPTER 3

The Reporting Entity and the

Consolidation of Less-than-Wholly–Owned Subsidiaries with No Differential

The Collapse of Enron and the Birth of a New Paradigm

LO 3-1 Understand and explain the usefulness and limitations of consolidated financial

statements.

The Usefulness of Consolidated Financial Statements

Limitations of Consolidated Financial Statements

Subsidiary Financial Statements

LO 3-2 Understand and explain how direct and indirect control influence the

consolidation of a subsidiary.

Consolidated Financial Statements: Concepts and Standards

Traditional View of Control

Indirect Control

Ability to Exercise Control

Differences in Fiscal Periods

Changing Concept of the Reporting Entity

LO 3-3 Understand and explain differences in the consolidation process when the

subsidiary is not wholly owned.

Noncontrolling Interest

Computation and Presentation of Noncontrolling Interest

LO 3-4 Make calculations for the consolidation of a less-than-wholly-owned subsidiary.

The Effect of a Noncontrolling Interest

Consolidated Net Income

Consolidated Retained Earnings

Worksheet Format

LO3- 5 Prepare a consolidation worksheet for a less-than-wholly-owned subsidiary.

Consolidated Balance Sheet with a Less-Than-Wholly-Owned Subsidiary

80 Percent Ownership Acquired at Book Value

Consolidation Subsequent to Acquisition – 80 Percent Ownership Acquired at Book

Value

Initial Year of Ownership

Second and Subsequent Years of Ownership

Chapter 03 – THE REPORTING ENTITY AND CONSOLIDATED FINANCIAL STATEMENTS

3-4

LO 3-6 Understand and explain the purpose of combined financial statements and how

they differ from consolidated financial statements.

Combined Financial Statements

LO 3-7 Understand and explain rules related to the consolidation of variable interest

entities.

Special-Purpose and Variable Interest Entities

Variable Interest Entities

LO 3-8 Understand and explain differences in consolidation rules under U.S. GAAP and

IFRS.

IFRS Differences in Determining Control of VIEs and SPEs

Appendix 3A:

Consolidation of Variable Interest Entities

NOTES ON POWERPOINT SLIDES

We have attempted to provide PowerPoint slides that will be useful to a broad set of users. Since

instructors often have different styles and preferences, we have attempted to include slides that

will accommodate different approaches and that can be adapted to classes with different levels of

preparation. For example, some instructors prefer to introduce the material before students have

read the chapter. We have tried to facilitate these types of introductory discussions by including

slides that replicate key points from the chapter. Other instructors expect students to have read

the chapter and attempted homework problems before coming to class. As a result, they may not

find it useful to review all of the topics in the chapter or to include slides that simply review

many of the details they expect students to study before class. However, instructors following

this approach often like to use sample exercises and problems built into the slides that allow

them to have extended discussions or to facilitate group interaction in class.

If instructors elect to spend two class periods on the same subject, they might find a combination

of both styles to be useful by first introducing foundational material before students have read

the chapter and studied the topic, followed by an extended discussion the next class period after

students have read the chapter and attempted homework problems.

We have tried to develop slides that can facilitate a flexible approach to allow instructors to

select the slides that best match their objectives and style for class discussions. This is the reason

we are including over 100 slides for some chapters in the text. We do not expect all instructors

to use all slides, but the slide files should help support different teaching approaches and allow

instructors to select the subset of slides that best matches their specific discussion objectives.

Chapter 03 – THE REPORTING ENTITY AND CONSOLIDATED FINANCIAL STATEMENTS

3-5

The slides are organized by learning objective. We have included a slide at the beginning of

each learning objective to show where the new material begins. Instructors may or may not want

to use these learning objective slides in class. We provide them primarily as a way of organizing

the material. We also include short multiple choice questions at the end of most learning

objectives. Some instructors find it useful to pause periodically during class to assess students’

level of understanding. For this reason, we include several “practice quiz questions” that can be

used throughout class discussions to engage students, help them focus on key points, or to

facilitate group interaction. Finally, we provide longer exercises and problems that many

instructors find useful in assessing understanding and encouraging group learning.

LO 3-1 Understand and explain the usefulness and limitations of consolidated financial

statements.

• Slides 3-8 summarize basic concepts related to LO 3-1.

• Instructors should choose slides from this LO that they deem most important to

emphasize to their students

LO 3-2 Understand and explain how direct and indirect control influence the consolidation of

a subsidiary.

• Slides 12-20 summarize basic concepts related to LO 3-2.

• Instructors should choose slides from this LO that they deem most important to

emphasize to their students

LO 3-3 Understand and explain differences in the consolidation process when the subsidiary

is not wholly owned.

• Slides 24-29 emphasize the need for full (as opposed to proportional) consolidation

and where the noncontrolling interest should be reported in the financial statements.

• Instructors should choose slides from this LO that they deem most important to

emphasize to their students

LO 3-4 Make calculations for the consolidation of a less-than-wholly-owned subsidiary.

• Slide 33 explains that the only change in the procedures for consolidation in chapter 3

(relative to chapter 2) relate to the fact that we don’t own 100% of the subsidiary.

• Slide 34-35 explains how procedures for preparing the basic consolidation entry

differ when the subsidiary is not wholly owned.

• Slides 36-41 summarize the basic concepts related to LO 3-4.

• Slides 44-47 contain a group of individual exercise to help students understand these

differences. We generally use this exercise in small groups to walk students through

the book value calculations leading up to the basic consolidation entry. The only

difference from chapter 2 is that the investment account only includes 70% of the

book value and the remaining 30% is assigned to the NCI shareholders. We give

students approximately 5 minutes to try to fill in the amounts in the table on slide 44

while working with their groups. With slide 45, we show students the answer to the

book value calculations, link the beginning and ending balances in the investment

account in the table to the T-account, and then ask students to prepare the basic

consolidation entry. We give students 3-4 minutes to work on this in their groups.

Chapter 03 – THE REPORTING ENTITY AND CONSOLIDATED FINANCIAL STATEMENTS

3-6

LO 3-5 Prepare a consolidation worksheet for a less-than-wholly-owned subsidiary.

• Slides 49-78 summarize the basic concepts related to LO 3-5.

• Slides 57-66 provide a comprehensive example of a consolidation with no differential

where the parent owns less the 100% of the voting shares outstanding. On slide 58,

we ask students to go through the book value calculations in their groups. On slide

59, we show students the answer to these calculations and then ask students to

prepare the basic consolidation entry. We give students 3-4 minutes to work on this in

their groups. On slide 61, we show students the basic consolidation entry and ask

them to complete the worksheet. We give students about 10 minutes to work through

the worksheet. We usually remind students that the big change is that there are two

extra lines in the income statement section for dividing total consolidated net income

between the NCI and CI (controlling) shareholders.

LO 3-6 Understand and explain the purpose of combined financial statements and how they

differ from consolidated financial statements.

• Slides 80-81 summarize basic concepts related to LO 3-6.

• Instructors should choose slides from this LO that they deem most important to

emphasize to their students

LO 3-7 Understand and explain rules related to the consolidation of variable interest entities.

• Slides 85-100 summarize the concepts related to LO 3-7.

• Slides 85-90 introduce the reason for changes in the traditional “voting control”

requirements for consolidation and define SPEs and VIEs. Specifically, these slides

use the Enron example to introduce the reason for the change in accounting standards

to capture previously unconsolidated entities. Slide 85 notes the decline in stock price

at the time Arthur Andersen announced the restatement in October of 2001. We note

that the diagram in slide 89 is too complex to describe in detail. We merely use it to

illustrate that many of the transactions in which Enron was engaged were very

complex. We also note that one of the problems was that some of these entities were

not “arm’s length” to Enron because they had officers who were also officers of

Enron. We use the table in slide 90 to illustrate how significant the raptor transactions

were to Enron (approximately 1/3 of reported earnings).

• Slides 91-92 provide a more detailed definition of VIEs.

• Slide 93 is highly animated. Instructors should avoid going too deep into details. We

use this example to illustrate that considering lease characteristics is not enough. A

company must also determine whether it has an unusual investment relationship with

the leasing company that might indicate that ABC Corp. (in this example) has an

ownership interest based on residual risks and benefits. A primary beneficiary

according to ASC 810 is a variable interest that absorbs a majority of the expected

loss or receives a majority of the expected residual return of the VIE. If ABC were to

guarantee the building’s value or they were to receive (by contract) any value of the

building over the $100k, they would be the primary beneficiary, and would have to

consolidate Leasing Corp. Interestingly, before ASC 810, ABC Corp. probably would

not have had to consolidate this arrangement.

Chapter 03 – THE REPORTING ENTITY AND CONSOLIDATED FINANCIAL STATEMENTS

3-7

• Slides 94-97 provide additional details about VIEs and requirements for the primary

beneficiary to consolidate a VIE.

• Slides 98-101 can be used as an individual or group exercise. This is a good example

to illustrate relationships that could result in a company being named the primary

beneficiary of a VIE. We usually diagram the facts on the board as we read through

them with students and ask if there is anything here that would raise a red flag for the

students.

LO 3-8 Understand and explain differences in consolidation rules under U.S. GAAP and

IFRS.

• Slides 107-110 summarize basic concepts related to LO 3-8. We usually do not go

into a lot of detail here. We merely point out the differences mentioned here and

quickly point them out on the three summary slides (46-48) without pausing for

discussion.

• Instructors should choose slides from this LO that they deem most important to

emphasize to their students

TEACHING IDEAS

1. Students may be asked to explain why companies do not consolidate all subsidiaries.

Then, they could be asked to choose a large company with many subsidiaries and

investments and to find examples of investments that are not consolidated. (For example,

large insurance groups often have many consolidated subsidiaries. In addition, some

have affiliated but non-consolidated mutual companies.)

2. Students may be asked to prepare a written memo on how a company could have de facto

(in fact) control over another company without having de jure (majority of voting stock)

control. Students could discuss alternative financing arrangements with very restrictive

covenants, purchase of virtually all of another company’s productive output, leasing

arrangements, and other related affiliations. The FASB continues to have a consolidations

project on its agenda. Some countries allow for consolidation based on de facto control.

Students could be asked to evaluate the potential difficulties of deciding which

controlling company should consolidate the controlled company in a case in which an

investing company (X) has a majority ownership of the voting stock of the controlled

company (Z), but a third party (Y) has de facto control of the controlled company (Z).

Can company Z be consolidated by both companies X and Y?

3. Students could be asked to choose a large consolidated entity that holds an interest in a

special purpose entity or entities. Students can choose a company or conduct a keyword

web search. Students should then describe how the company accounts for the entity and

what disclosures it makes regarding the investment.

Chapter 03 – THE REPORTING ENTITY AND CONSOLIDATED FINANCIAL STATEMENTS

3-8

DESCRIPTIONS OF CASES, EXERCISES, AND PROBLEMS

C3-1

12 min.

LO 3-5

E

Computation of Total Asset Values

In answering this case, each of the major items that will cause total assets

reported in the consolidated balance sheet to differ from the sum of the assets

reported by the individual companies should be discussed. This case is a good

test of basic understanding of the consolidation process.

C3-2

30 min.

LO 3-3,

LO 3-7

M

Accounting Entity [AICPA Adapted]

[AICPA Adapted] Some students have little understanding of the concept of an

accounting entity. This question deals with the concept of an entity and draws

attention to the fact that there are many accounting entities that are not legal

entities.

C3-3

35 min.

LO 3-3,

LO 3-6

M

Joint Venture Investment

Students are to explain how Dell and CIT could avoid consolidating the entity.

They are expected to describe the joint venture treatment employed by Dell in the

latest financial statements. They should also verify if Dell currently employs off-

balance sheet financing.

C3-4

20 min.

LO 3-1

E

What Company is That?

Students are required to identify some of the well-known brand names from

Viacom’s subsidiaries, ConAgra Foods, and Yum! Brands.

C3-5

25 min.

LO 3-1

M

A

Subsidiaries and Core Businesses

Students must acquire information about subsidiaries owned by General Electric,

Sears Roebuck, and PepsiCo and evaluate whether meaningful information can

be provided when businesses that are considerably different in nature are

consolidated.

C3-6

25 min.

LO 3-8

M

International Consolidation Issues

Students must explain requirements by the IFRS for consolidated financial

statements, treatment of negative goodwill, and treatment of goodwill

impairment.

Chapter 03 – THE REPORTING ENTITY AND CONSOLIDATED FINANCIAL STATEMENTS

3-9

C3-7

20 min.

LO 3-7

E

Off-Balance Sheet Financing and VIEs

Students must explain the meaning of off-balance sheet financing as well as

describe techniques used. Examples of legitimate uses of variable interest

entities must be given. They should also explain how VIEs can be used to

manage earnings to meet financial reporting goals.

C3-8

25 min.

LO 3-6

M

Consolidation Differences among Major Companies

Students must research the subsidiaries of Union Pacific and Exxon Mobil.

Identify if Exxon Mobil consolidates all of its majority-owned subsidiaries, and

whether it consolidates any entities in which it does not hold majority ownership.

Methods used to account for investments in the common stock of companies in

which it holds less than majority ownership should also be discussed.

E3-1

15 min.

LO 3-1,

LO 3-2

E

Multiple-Choice Questions on Consolidation Overview [AICPA Adapted]

Four multiple-choice questions deal primarily with the issue of when

consolidated statements should be prepared.

E3-2

15 min.

LO 3-7

E

Multiple-Choice Questions on Variable Interest Entities

Four multiple-choice questions address issues related to variable interest and

special purpose entities.

E3-3

15 min.

LO 3-5

E

Multiple-Choice Questions on Consolidated Balances [AICPA Adapted]

Three multiple-choice questions deal with a variety of basic issues related to the

consolidation process.

E3-4

12 min.

LO 3-2,

LO 3-3

E

Multiple-Choice Questions on Consolidation Overview [AICPA Adapted]

Four multiple-choice questions deal with a variety of basic issues related to the

consolidation process.

E3-5

15 min.

LO 3-5

E

Balance Sheet Consolidation

Students must calculate four balance sheet amounts immediately after acquisition

of 100% of the outstanding voting stock of an entity. These include total assets

on the parent’s balance sheet and total assets, liabilities, and stockholders equity

of the consolidated entity.

E3-6

15 min.

LO 3-5

M

Balance Sheet Consolidation with Intercompany Transfer

Students must calculate four totals immediately after acquisition of 100% of the

outstanding voting stock of an entity. These include total assets on the parent’s

balance sheet and total assets, liabilities, and stockholders equity of the

consolidated entity.