Chapter 06 – Intercompany Inventory Transactions

E6-13 Consolidated Balance Sheet Worksheet

a.

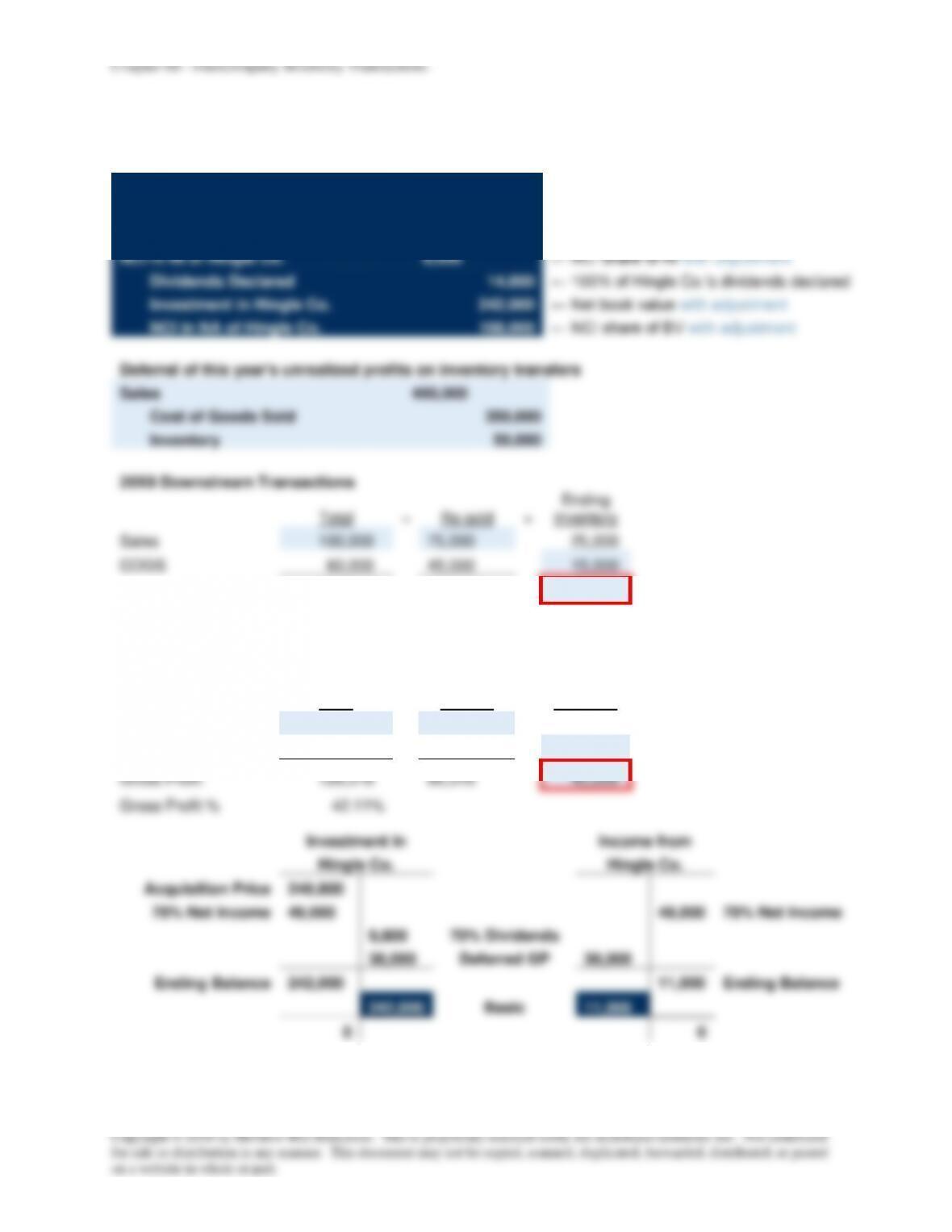

Equity Method Entries on Doorst Corp.’s Books:

Investment in Hingle Co.

49,000

Income from Hingle Co.

49,000

Record Doorst Corp.’s 70% share of Hingle Co.’s 20X8 income

Cash

9,800

Investment in Hingle Co.

9,800

Record Doorst Corp.’s 70% share of Hingle Co.’s 20X8 dividend

Income from Hingle Co.

10,000

Investment in Hingle Co.

10,000

Eliminate the deferred gross profit from downstream sales in 20X8

Income from Hingle Co.

28,000

Investment in Hingle Co.

28,000

Eliminate the deferred gross profit from upstream sales in 20X8

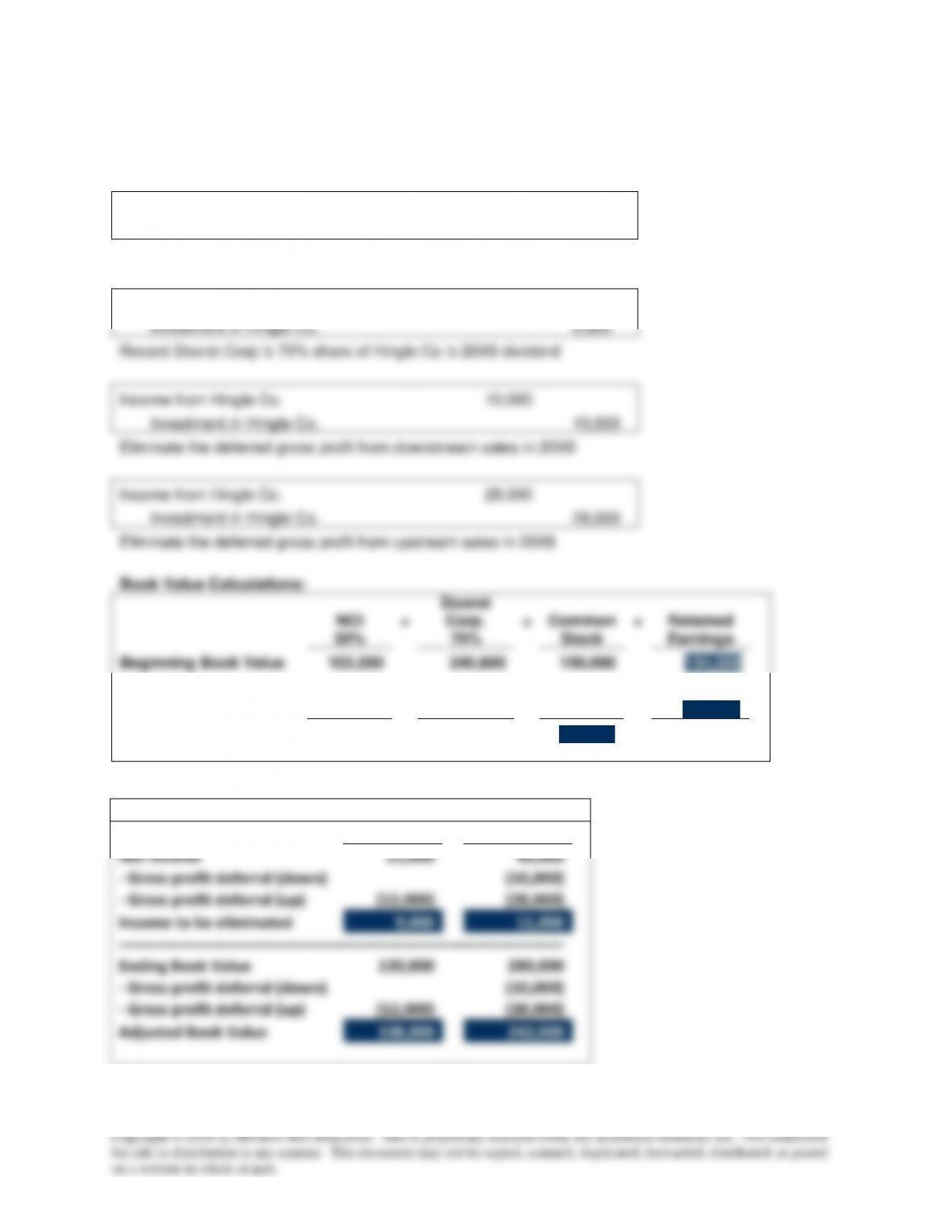

Book Value Calculations:

NCI

30%

+

Doorst

Corp.

70%

=

Common

Stock

+

Retained

Earnings

Beginning Book Value

103,200

240,800

150,000

194,000

+ Net Income

21,000

49,000

70,000

– Dividends

(4,200)

(9,800)

(14,000)

Ending Book Value

120,000

280,000

150,000

250,000

Adjustment to Basic Consolidation Entry

NCI

Doorst Corp

Net Income

21,000

49,000

– Gross profit deferral (down)

(10,000)

– Gross profit deferral (up)

(12,000)

(28,000)

Income to be eliminated

9,000

11,000

———————————————————-—————————

Ending Book Value

120,000

280,000

– Gross profit deferral (down)

(10,000)

– Gross profit deferral (up)

(12,000)

(28,000)

Adjusted Book Value

108,000

242,000

108,000

242,000

Copyright © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized

for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

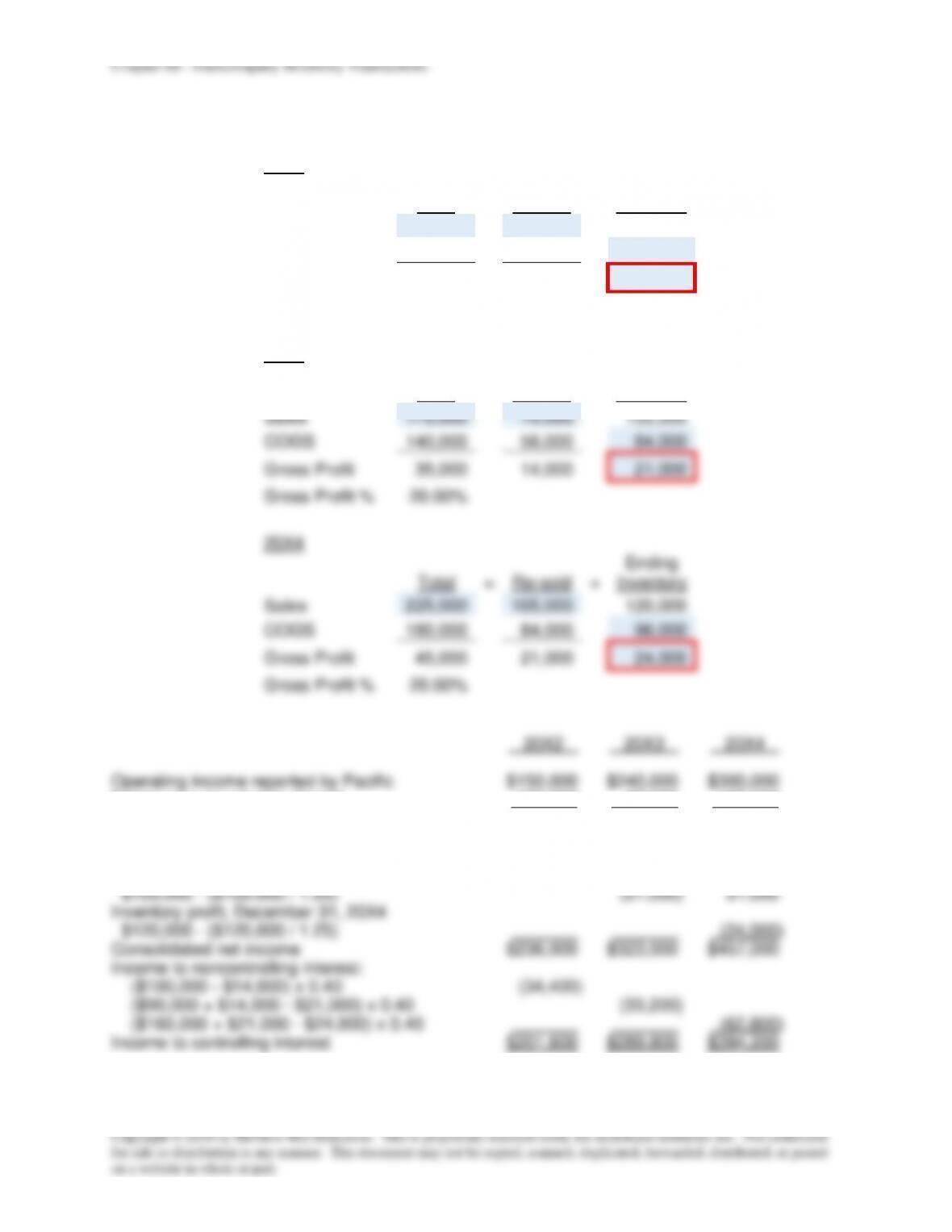

P6-17 Consolidated Income Statement Data

a.

$180,000 = $550,000 + $450,000 – $820,000

b.

January 1, 20X2: $25,000 = $75,000 – $50,000

December 31, 20X2: $15,000 = $180,000 + $210,000 – $375,000

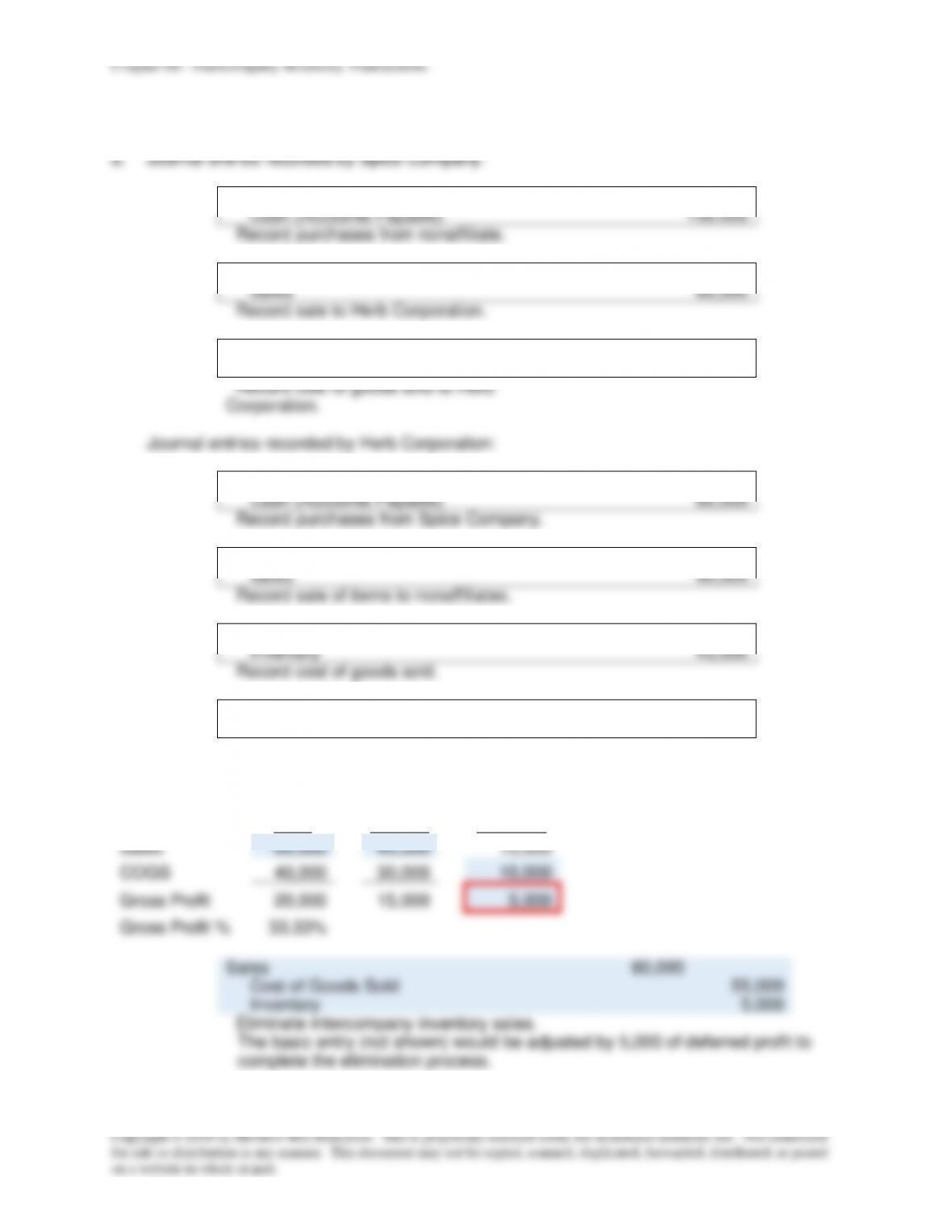

c.

Investment in Bitner

15,000

NCI in NA of Bitner

10,000

Cost of Goods Sold

25,000

Eliminate beginning inventory profit.

Sales

180,000

Cost of Goods Sold

165,000

Inventory

15,000

Eliminate intercompany sale of inventory.

The basic entry (not shown) would be adjusted by 15,000 of deferred profit

and by 25,000 to reverse the gross profit deferral from the prior year to

complete the elimination process.

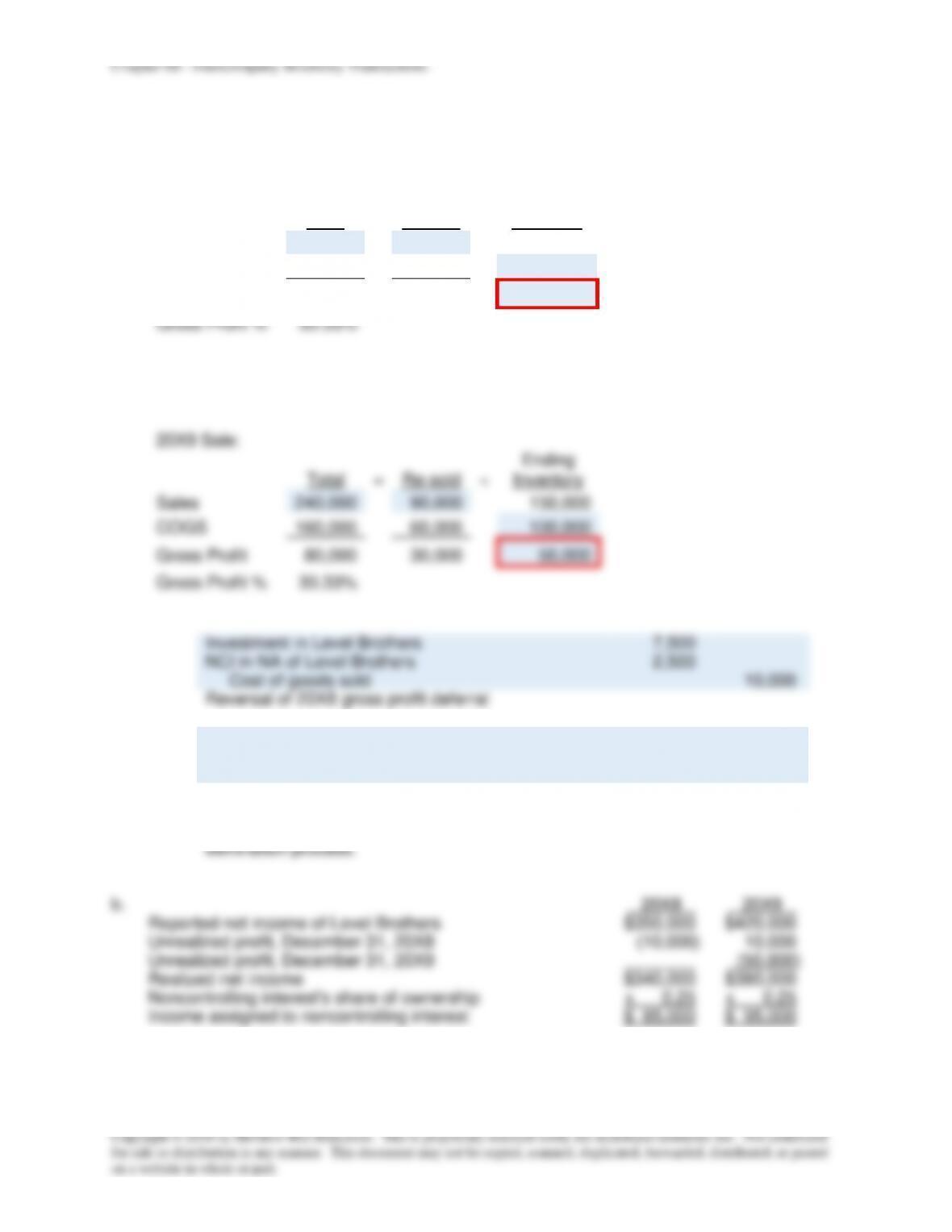

d.

Reported net income of Bitner Company

$ 90,000

Prior-period profit realized in 20X2

25,000

Unrealized profit on 20X2 sales

(15,000)

Realized income

$100,000

Proportion held by noncontrolling interest

x 0.40

Income assigned to noncontrolling interest

$ 40,000