The general fund of the Town of Dean levied property taxes of $3,000,000 for the fiscal

year beginning on January 1, 20X8. It was estimated that 1% of the levy would be

uncollectible. During the period January 1, 20X8, through December 31, 20X8,

$2,960,000 of the property tax levy was collected. At December 31, 20X8, Dean

estimated that $10,000 of property taxes levied in 20X8 would be collected during the

first 60 days of 20X9. What amount of property tax revenue should be reported by the

general fund for the year ended December 31, 20X8?

A. $2,960,000

B. $3,000,000

C. $2,970,000

D. $2,990,000

Sphinx Co. (Sphinx) records its transactions in U.S. dollars. A sale of goods resulted in

a receivable denominated in Japanese yen, and a purchase of goods resulted in a

payable denominated in Euros. Sphinx recorded a foreign exchange transaction gain on

collection of the receivable and an exchange transaction loss on the settlement of the

payable. The exchange rates are expressed as so many units of foreign currency to one

dollar. Did the number of foreign currency units exchangeable for a dollar increase or

decrease between the contract and settlement dates?

Yen exchangeable for $1 Euros exchangeable for $1

A. Decrease Increase

B. Increase Increase

C. Decrease Decrease

D. Increase Decrease

Dividends paid to noncontrolling shareholders:

I. are reported as a cash outflow in the consolidated cash flow statement.

II. represent funds that are no longer available to the consolidated entity.

III. are reported in the consolidated retained earnings statement.

A. Observation I alone is true.

B. Observation III alone is true.

C. Observations I and II are true.

D. Observations I, II, and II are true.

An internal service fund had the following transactions during the year ended June 30,

20X9, its first year of existence:

(1) Received $1,000,000 contribution from the general fund.

(2) Acquired fleet of cars for $950,000, paying cash.

(3) Billed departments in other funds $500,000 for using cars.

(4) Incurred operating costs, exclusive of depreciation, of $240,000.

(5) Depreciation expense amounted to $250,000.

Refer to the above information. On the internal service fund’s balance sheet on June 30,

20X9, total net assets should be reported at:

A. $1,000,000.

B. $1,010,000.

C. $1,250,000.

D. $910,000.

All of the following are true statements when measuring hedge effectiveness except:

A. Effectiveness means there is an approximate offset with the range of 80% to 125%

of the changes in the fair value of the cash flows

B. Effectiveness means there is an approximate offset in fair value to the risk being

hedged.

C. A Company may elect to choose from several different measures for assessing hedge

effectiveness.

D. Effectiveness must be assessed at least annually when the company reports their

annual financial statements.

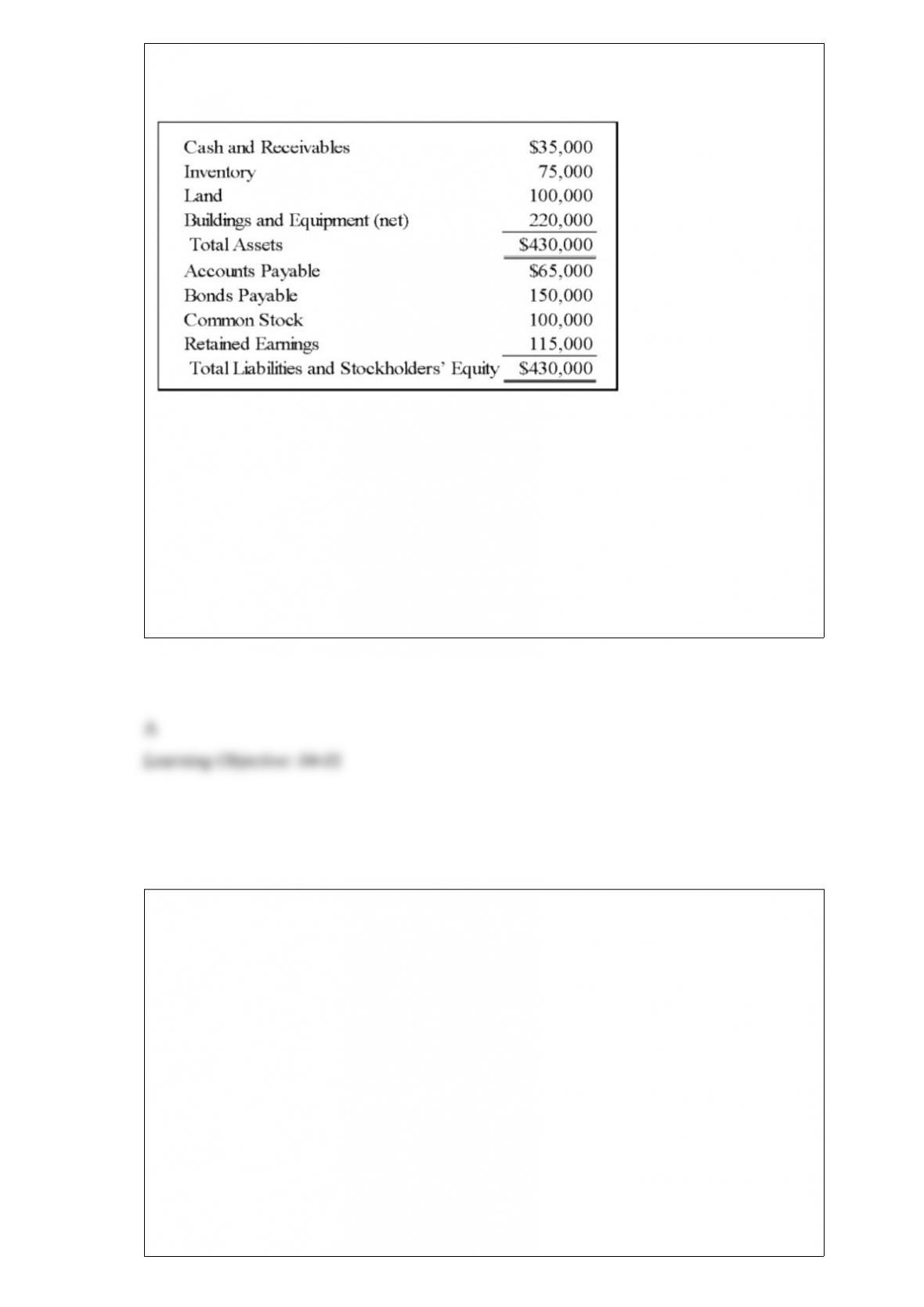

Wilbur Corporation is to be liquidated under Chapter 7 of the Bankruptcy Code. The

balance sheet on December 31, 20X8, is as follows:

The following additional information is available:

1) Marketable securities consist of 2,000 shares of Bristol Inc. common stock. The

market value per share of the stock is $8. The stock was pledged against a $20,000, 8

percent note payable that has accrued interest of $800.

2) Accounts receivable of $40,000 are collateral for a $35,000, 10 percent note payable

that has accrued interest of $3,500.

3) Inventory with a book value of $35,000 and a current value of $32,000 is pledged

against accounts payable of $60,000. The appraised value of the remainder of the

inventory is $50,000.

4) Only $1,000 will be recovered from prepaid insurance.

5) Land is appraised at $65,000 and plant and equipment at $160,000.

6) It is estimated that the franchises can be sold for $15,000.

7) All the wages payable qualify for priority.

8) The mortgages are on the land and on a building with a book value of $110,000 and

an appraised value of $100,000. The accrued interest on the mortgages is $7,500.

9) Estimated legal and accounting fees for the liquidation are $10,000.

Required

a. Prepare a statement of affairs as of December 31, 20X8.

b. Compute the estimated percentage settlement to unsecured creditors.

Which of the following items is not recognized as revenue by a governmental unit?

A. sales tax proceeds

B. property tax levies

C. bond proceeds

D. grants received from other governmental units

On December 31, 20X9, Add-On Company acquired 100 percent of Venus

Corporation’s common stock for $300,000. Balance sheet information Venus just prior

to the acquisition is given here:

At the date of the business combination, Venus’s net assets and liabilities approximated

fair value except for inventory, which had a fair value of $60,000, land which had a fair

value of $125,000, and buildings and equipment (net), which had a fair value of

$250,000.

Based on the information provided, what amount of inventory will be included in the

consolidated balance sheet immediately following the acquisition?

A. $60,000

B. $75,000

C. $15,000

D. $45,000

Tower Corporation’s controller has just finished preparing a consolidated balance sheet,

income statement, and statement of changes in retained earnings for the year ended

December 31, 20X9. Tower owns 80 percent of Network Corporation’s stock, which it

acquired at underlying book value on November 1, 20X6. At that date, the fair value of

the noncontrolling interest was equal to 20 percent of Network Corporation’s book

value. The following information is available:

Consolidated net income for 20X9 was $160,000.

Network reported net income of $50,000 for 20X9.

Tower paid dividends of $30,000 in 20X9.

Network paid dividends of $10,000 in 20X9.

Tower issued common stock on February, 18, 20X9, for a total of $100,000.

Consolidated wages payable decreased by $6,000 in 20X9.

Consolidated depreciation expense for the year was $15,000.

Consolidated accounts receivable decreased by $20,000 in 20X9.

Bonds payable of Tower with a book value of $102,000 were retired for $100,000 on

December 31, 20X9.

Consolidated amortization expense on patents was $10,000 for 20X9.

Tower sold land that it had purchased for $75,000 to a nonaffiliate for $80,000 on June

10, 20X9.

Consolidated accounts payable decreased by $7,000 during 20X9.

Total purchases of equipment by Tower and Network during 20X9 were $180,000.

Consolidated inventory increased by $36,000 during 20X9.

There were no intercompany transfers between Tower and Network in 20X9 or prior

years except for Network’s payment of dividends. Tower uses the indirect method in

preparing its cash flow statement.

Based on the preceding information, what amount will be reported in the consolidated

cash flow statement as net cash used in investing activities for 20X9?

A. $180,000

B. $100,000

C. $255,000

D. $110,000

Parent Corporation owns 90 percent of Subsidiary 1 Company’s stock and 75 percent of

Subsidiary 2 Company’s stock. During 20X8, Parent sold inventory purchased in 20X7

for $48,000 to Subsidiary 1 for $60,000. Subsidiary 1 then sold the inventory at its cost

of $60,000 to Subsidiary 2. Prior to December 31, 20X8, Subsidiary 2 sold $45,000 of

inventory to a nonaffiliate for $67,000 and held $15,000 in inventory at December 31,

20X8.

Based on the information given above, what amount should be reported in the

December 31, 20X8, consolidated balance sheet as inventory?

A. $36,000

B. $12,000

C. $15,000

D. $28,000

Each of the following questions names an item. Select the correct description of the

item from this list. Indicate your selection by entering the letter of the description.

Descriptions

a. Provides preliminary information to investors about an upcoming issue.

b. Informs investors of an upcoming offering.

c. Required annual filing to the SEC.

d. Discloses unscheduled material events.

e. Includes amendments to the Securities Act, additional disclosure requirements, and

other current issues regarding accounting and auditing principles and standards.

f. Results in a thorough examination by the SEC of a registration statement.

g. Issued by the staff of the SEC and contains differences that must be corrected in a

registration statement before the securities may be offered or sale.

h. Quarterly report to SEC.

i. Includes new or revised administrative practices and interpretations used in reviewing

financial statements.

j. Includes the results of actions taken against accountants or other participants because

false or misleading statements were filed.

k. Includes Regulations S-X and S-K.

Form 8-K

Consolidated financial statements tend to be most useful for:

A. Creditors of a consolidated subsidiary.

B. Investors and long-term creditors of the parent company.

C. Short-term creditors of the parent company.

D. Stockholders of a consolidated subsidiary.

The accounting statement of affairs is prepared:

A. at the end of the reorganization process.

B. at the end of the liquidation process.

C. at the beginning of the reorganization process.

D. at the beginning of the liquidation process.

Pine City’s year end is June 30. Pine levies property taxes in January of each year for

the calendar year. One-half of the levy is due in May and one-half is due in October.

Property tax revenue is budgeted for the period in which payment is due. The following

information pertains to Pine’s property taxes for the period from July 1, 20X4, to June

30, 20X5:

Calendar Year

20X4 20X5

Levy $2,000,000 $2,400,000

Collected in:

May 950,000 1,100,000

July 50,000 60,000

October 920,000 —

December 80,000 —

The $40,000 balance due for the May 20X5 installments was expected to be collected in

August 20X5. What amount should Pine recognize for property tax revenue for the year

ended June 30, 20X5?

A. $2,160,000

B. $2,200,000

C. $2,360,000

D. $2,400,000

When a new partner is admitted into a partnership and the old partners’ goodwill is

recognized, the goodwill is allocated to:

I. all the partners in their profit-and-loss-sharing ratio.

II. the old partners in their profit and loss sharing ratio.

A. I only

B. II only

C. Either I or II

D. Neither I nor II

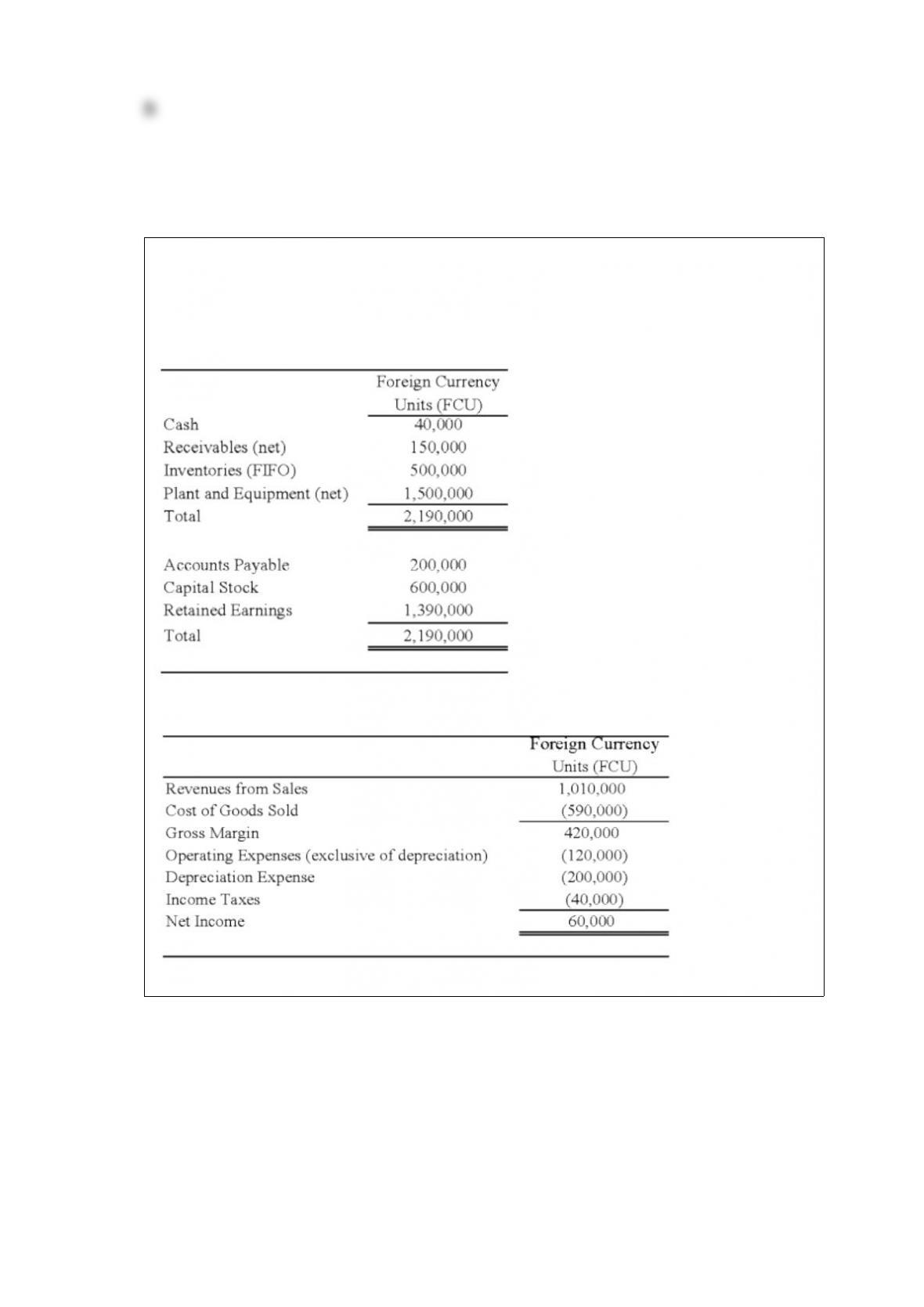

On January 2, 20X8, Johnson Company acquired a 100% interest in the capital stock of

Perth Company for $3,100,000. Any excess cost over book value is attributable to a

patent with a 10-year remaining life. At the date of acquisition, Perth’s balance sheet

contained the following information:

Perth’s income statement for 20X8 is as follows:

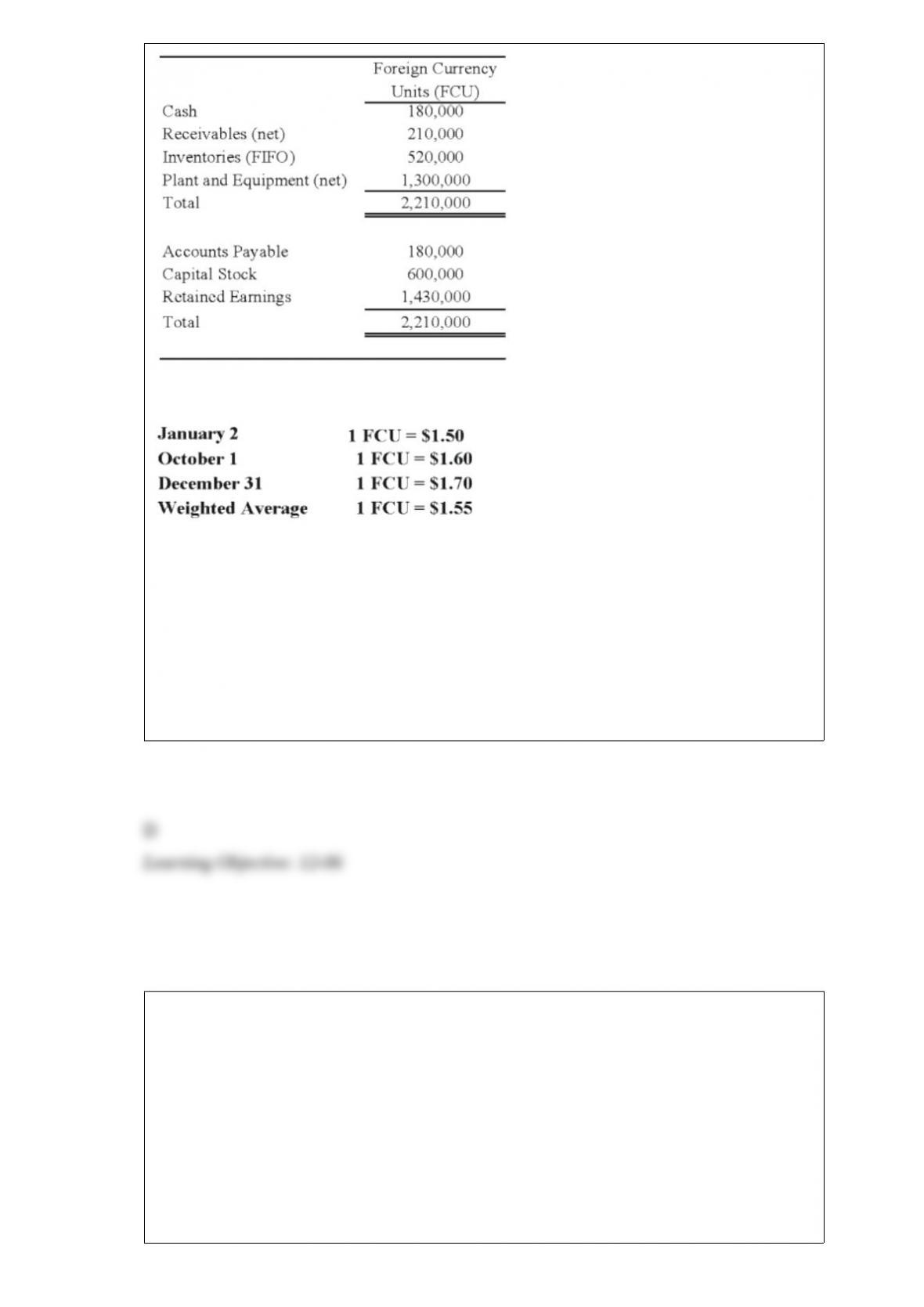

The balance sheet of Perth at December 31, 20X8, is as follows:

Perth declared and paid a dividend of 20,000 FCU on October 1, 20X8. Spot rates at

various dates for 20X8 follow:

Assume Perth’s revenues, purchases, operating expenses, depreciation expense, and

income taxes were incurred evenly throughout 20X8.

Refer to the above information. Assuming the U.S. dollar is the functional currency,

what is the amount of patent amortization for 20X8 that results from Johnson’s

acquisition of Perth’s stock on January 2, 20X8?

A. $11,884

B. $11,770

C. $12,550

D. $11,500

Cor-Eng Partnership was formed on January 2, 20X1. Under the partnership agreement,

each partner has an equal initial capital balance accounted for under the goodwill

method. Partnership net income or loss is allocated 60% to Cor and 40% to Eng. To

form the partnership, Cor originally contributed assets costing $30,000 with a fair value

of $60,000 on January 2, 20X1, while Eng contributed $20,000 in cash. Drawings by

the partners during 20X1 totaled

$3,000 by Cor and $9,000 by Eng. Cor-Eng’s 20X1 net income was $25,000. Eng’s

initial capital balance in Cor-Eng is

A. $25,000

B. $20,000

C. $60,000

D. $40,000

Which of the following observations is true of the discrete view of interim reporting?

A. An interim period is viewed as an installment of an annual period.

B. Recognition and adjustment of certain income or expense items may be affected by

judgments about the expected results of the entire year’s operations.

C. Each interim period is considered as a basic accounting period to be evaluated as if it

were an annual accounting period.

D. One interim period would not bear the entire expense that benefits more than one

interim period.

On January 1, 20X6, Interstate Corporation acquired 70 percent of Catapult Company’s

common stock for $210,000 cash. The fair value of the noncontrolling interest at that

date was determined to be $90,000. Data from the balance sheets of the two companies

included the following amounts as of the date of acquisition:

Interstate Catapult

Cash $50,000 $15,000

Accounts Receivable 70,000 25,000

Inventory 30,000 20,000

Land 150,000 80,000

Buildings and Equipment 250,000 200,000

Less: Accumulated Depreciation (70,000) (20,000)

Investment in Catapult Co. 210,000

Total Assets $690,000 $320,000

Accounts Payable $40,000 $10,000

Bonds Payable 150,000 40,000

Common Stock 300,000 90,000

Retained Earnings 200,000 180,000

Total Liabilities and Equity $690,000 $320,000

At the date of the business combination, the book values of Catapult’s assets and

liabilities approximated fair value except for inventory, which had a fair value of

$30,000, and land, which had a fair value of $95,000.

Based on the preceding information, what amount will be reported as noncontrolling

interest in the consolidated balance sheet prepared immediately after the business

combination?

A. $0

B. $81,000

C. $90,000

D. $96,000

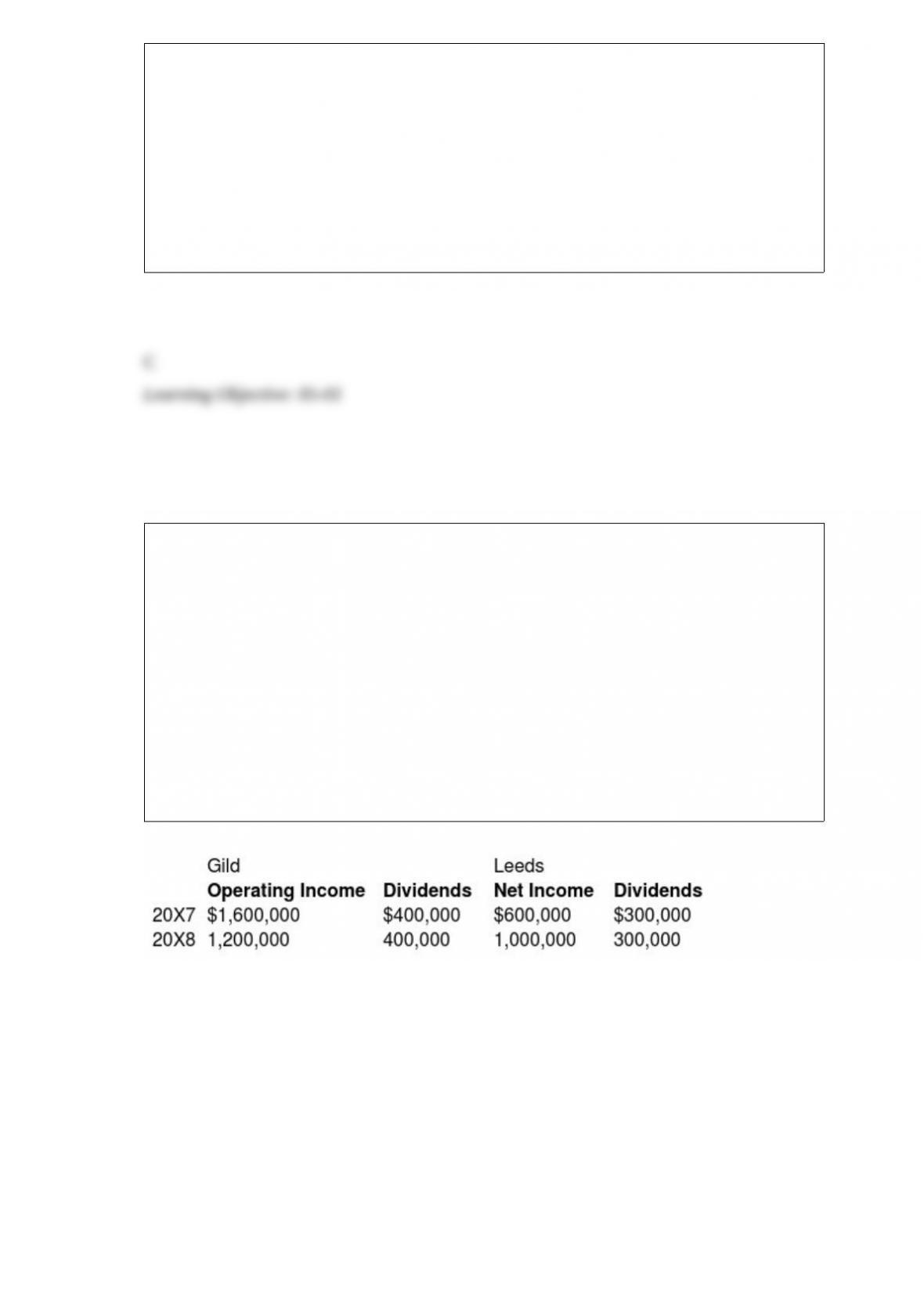

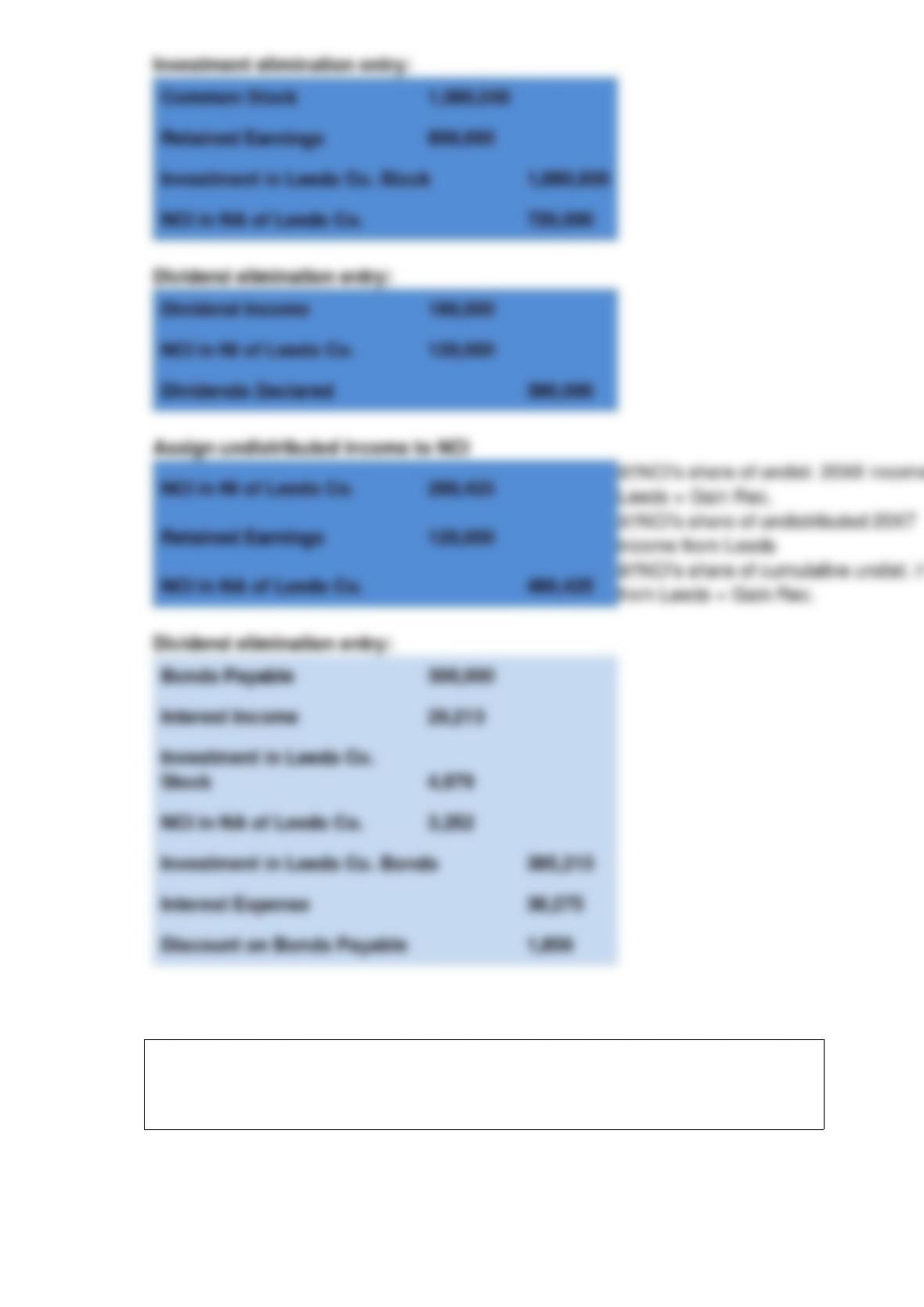

On January 1, 20X7, Gild Company acquired 60 percent of the outstanding common

stock of Leeds Company at the book value of the shares acquired. On that date, the fair

value of noncontrolling interest was equal to 40 percent of book value of Leeds. At the

time of purchase, Leeds had common stock of $1,000,000 outstanding and retained

earnings of $800,000.

On December 31, 20X7, Gild purchased 50 percent of Leeds’ bonds outstanding which

were originally issued on January 1, 20X4, at 99. The total bond issue has a face value

of $600,000, pays 10 percent interest annually, and has a 10-year maturity. Any

premium or discount is amortized using the effective interest method. Gild paid

$306,000 for its investment in Leeds’ bonds and intends to hold the bonds until

maturity.

Income and dividends for Gild and Leeds for 20X7 and 20X8 are as follows:

Assume Gild accounts for its investment in Leeds stock using the cost method.

Required:

A) Present the worksheet elimination entries necessary to prepare consolidated financial

statements for 20X7.

B) Present the worksheet elimination entries necessary to prepare consolidated financial

statements for 20X8.

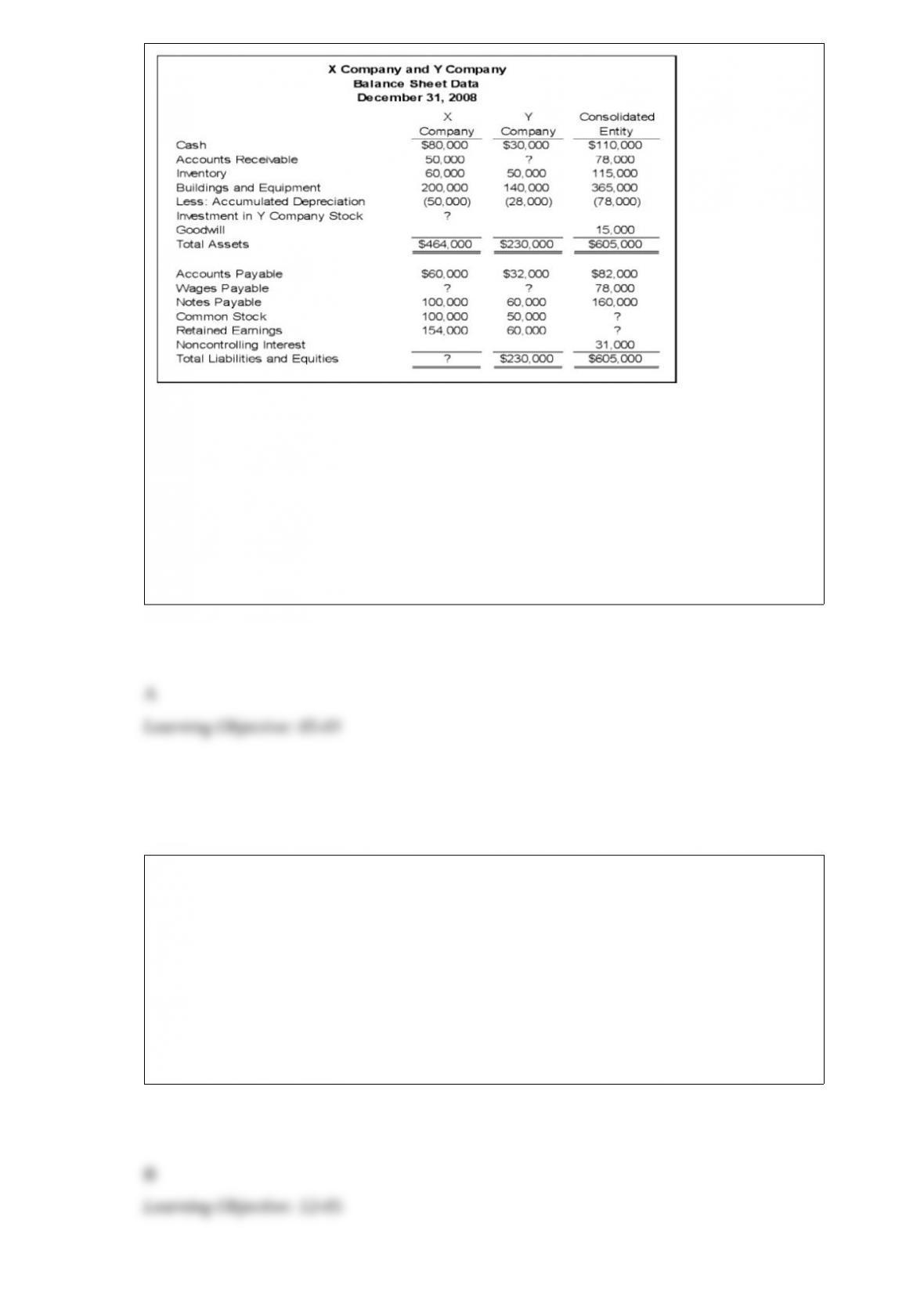

On December 31, 20X8, X Company acquired controlling ownership of Y Company. A

consolidated balance sheet was prepared immediately. Partial balance sheet data for the

two companies and the consolidated entity at that date follow:

During 20X8, X Company provided consulting services to Y Company and has not yet

paid for them. There were no other receivables or payables between the companies at

December 31, 20X8.

Based on the information given, what amount will be reported as total controlling

interest in the consolidated balance sheet?

A. $254,000

B. $285,000

C. $364,000

D. $395,000

Nichols Company owns 90% of the capital stock of a foreign subsidiary located in

Ireland. As a result of translating the subsidiary’s accounts, a debit of $160,000 was

needed in the translation adjustments account so that the foreign subsidiary’s debits and

credits were equal in U.S. dollars. How should Nichols report its translation

adjustments on its consolidated financial statements?

A. As a $144,000 increase in the stockholders’ equity section of the balance sheet.

B. As a $144,000 reduction in consolidated comprehensive net income.

C. As a $160,000 debit in stockholders’ equity section of the balance sheet.

D. As a $160,000 reduction in consolidated comprehensive net income.

Highland Company sold goods to an Egyptian company for 350,000 Egyptian pounds

on December 6, 20X3, with payment due on January 15, 20X4. The exchange rates

were as follows:

December 6, 20X3 1 Egyptian pound = $0.1593

December 31, 20X3 1 Egyptian pound = $0.1612

January 15, 20X4 1 Egyptian pound = $0.1604

Based on the preceding information, what is Highland’s overall net gain or net loss

from its foreign currency exposure related to this transaction?

A. $280 loss

B. $302 loss

C. $385 gain

D. $665 gain

A transfer of assets by a company in financial difficulty is considered a sale if:

I. the transfer includes a recourse provision allowing the buyer to return the asset.

II. the transferee obtains the right to pledge or exchange the transferred assets.

III. the transferred assets have been isolated from the transferor.

IV. the transferor does not maintain effective control over the transferred assets.

A. I, II, and IV

B. Both I and III

C. Both I and II

D. II, III, and IV

Which of the following fiduciary funds does not require a statement of changes in net

assets?

I. Private-purpose trust fund

II. Agency fund.

A. I only

B. II only

C. Both I and II

D. Neither I nor II

Which of the following observations is (are) consistent with the acquisition method of

accounting for business combinations?

I. Expenses related to the business combination are expensed.

II. Stock issue costs are treated as a reduction in the issue price.

III. All merger and stock issue costs are expensed.

IV. No goodwill is ever recorded.

A. III

B. IV

C. I and II

D. I, II, and IV

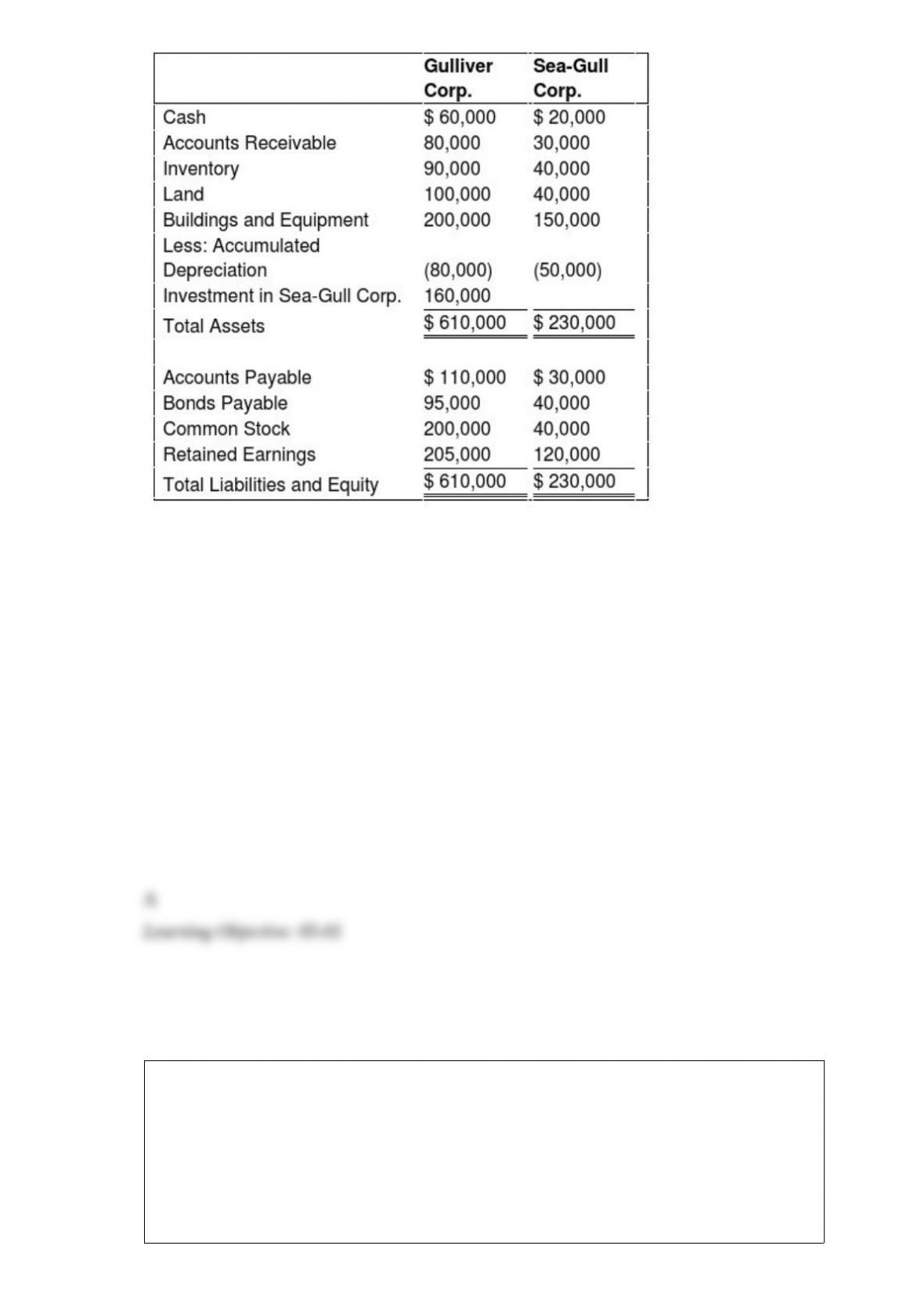

On January 1, 20X9, Gulliver Corporation acquired 80 percent of Sea-Gull Company’s

common stock for $160,000 cash. The fair value of the noncontrolling interest at that

date was determined to be $40,000. Data from the balance sheets of the two companies

included the following amounts as of the date of acquisition:

At the date of the business combination, the book values of Sea-Gull’s net assets and

liabilities approximated fair value except for inventory, which had a fair value of $45,000,

and land, which had a fair value of $60,000.

Based on the preceding information, what amount of total assets will be reported in the

consolidated balance sheet prepared immediately after the business combination?

A. $720,000

B. $840,000

C. $825,000

D. $865,000

When a parent owns less than 100% of a subsidiary, the noncontrolling interest

shareholders are allocated their ownership percentage of income or net assets in all of

the following consolidating entries except for:

A. The basic investment account consolidation entry

B. The excess value (differential) reclassification entry

C. The optional accumulated depreciation consolidation entry

D. The amortized excess value reclassification entry

Elvis Company purchases inventory for $70,000 on Mar 19, 20X8 and sells it to

Graceland Corporation for $95,000 on May 14, 20X8. Graceland still holds the

inventory on December 31, 20X8, and determines that its market value (replacement

cost) is $82,000 at that time. Graceland writes the inventory down from $95,000 to its

lower market value of $82,000 at the end of the year. Elvis owns 75 percent of

Graceland.

Based on the information given above, by what amount should Graceland write down

inventory in its books?

A. $14,000

B. $15,000

C. $13,000

D. $16,000

Suppose the direct foreign exchange rates in U.S. dollars are as follows:

1 Swiss franc = $1.0371

1 Swedish krona = $0.1526

Based on the information given above, how many U.S. dollars must be paid for a

purchase of goods costing 20,000 Swedish krona?

A. $131,062

B. $20,742

C. $19,285

D. $3.052

The general fund of Athens ordered computer equipment on December 1, 20X8, for

$32,000. The order was appropriately encumbered on this date. Athens received the

computer equipment on January 25, 20X9, and issued a voucher to pay the vendor

$32,400. Athens uses the calendar year for reporting, and all outstanding encumbrances

lapse at year-end. Athens’ governing board honors all outstanding encumbrances by

including them in the following year’s appropriations. On January 25, 20X9, the general

fund of Athens should debit:

A. Encumbrances for $32,000.

B. Fund Balance—assigned for Encumbrances for $32,400.

C. Expenditures-20X8 for $32,400.

D. Expenditures for $32,400.