Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-11

Investment in

Amber Corp.

Acquisition

Price

49,200

34,200

Basic

15,000

Excess Reclass.

0

E5-4 Computation of Consolidated Balances

a.

Inventory

$140,000

b.

Land

$ 60,000

c.

Buildings and Equipment

$550,000

d.

Fair value of consideration given by Ford

$470,000

Fair value of noncontrolling interest

117,500

Total fair value

$587,500

Book value of Slim’s net assets

$450,000

Fair value increment for:

Inventory

20,000

Land

(10,000)

Buildings and equipment (net)

70,000

Fair value of identifiable net assets

(530,000)

Goodwill

$ 57,500

e.

Investment in Slim Corporation: None would be reported;

the balance in the investment account is eliminated.

f.

Noncontrolling Interest = FV of the NCI

$117,500

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

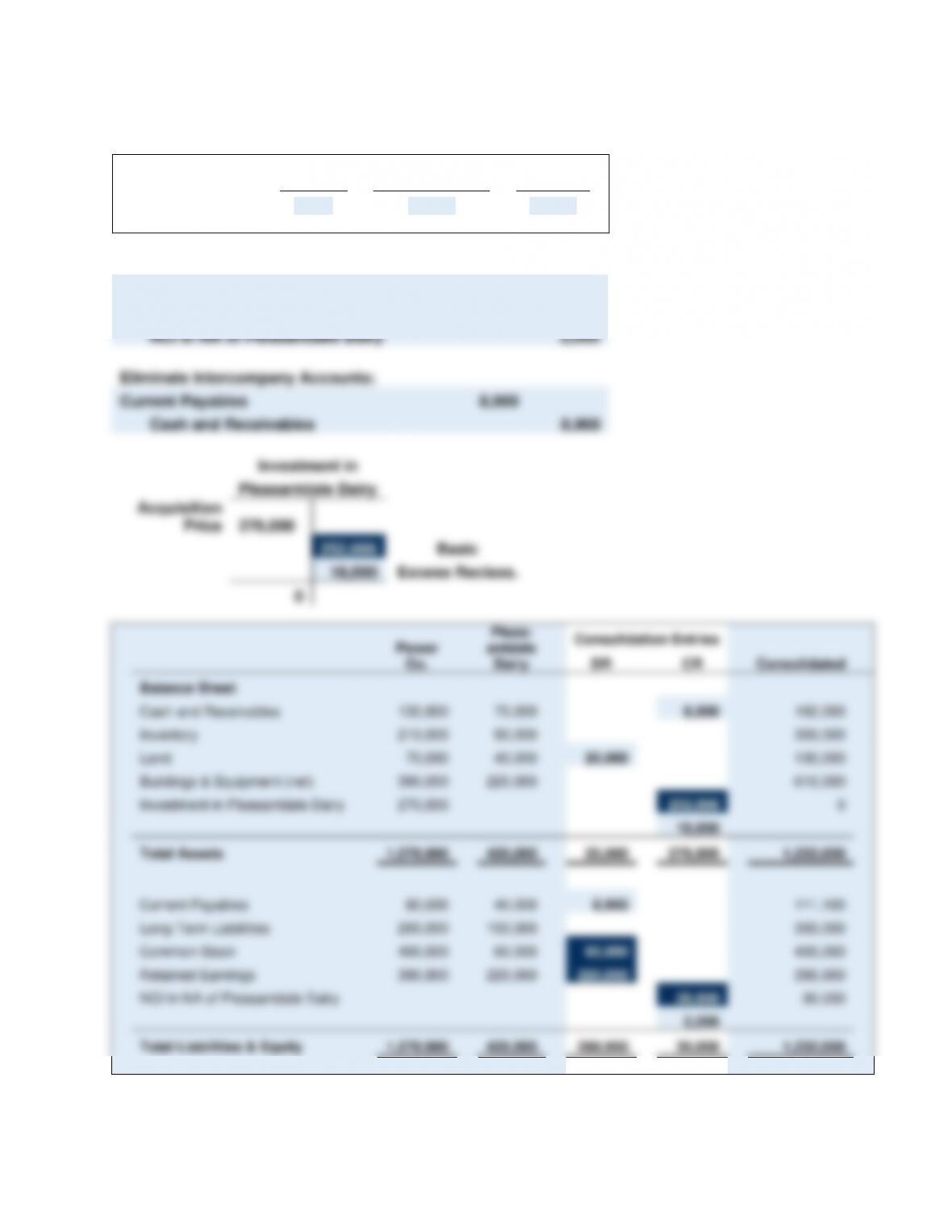

E5-5 Balance Sheet Worksheet

Cash and Receivables

900

Retained Earnings

900

Accrued interest earned by Power Co.

Equity Method Entries on Power Co.’s Books:

Investment in Pleasantdale Dairy

270,000

Cash

270,000

Record the initial investment in Pleasantdale Dairy

Book Value Calculations:

NCI

10%

+

Power Co.

90%

=

Common

Stock

+

Retained

Earnings

Book value at

acquisition

28,000

252,000

60,000

220,000

Goodwill = 0

Identifiable

Excess = 18,000

$270,000

Initial

investment in

Pleasantdale

Dairy

90%

Book value =

252,000

Basic consolidation entry

Common Stock

60,000

Retained Earnings

220,000

Investment in Pleasantdale Dairy

252,000

NCI in NA of Pleasantdale Dairy

28,000

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

E5-5 (continued)

Excess Value (Differential) Calculations:

NCI

10%

+

Power Co.

90%

=

Land

Beginning balances

2,000

18,000

20,000

Excess Value (Differential) Reclassification Entry:

Land

20,000

Investment in Pleasantdale Dairy

18,000

NCI in NA of Pleasantdale Dairy

2,000

Eliminate Intercompany Accounts:

Current Payables

8,900

Cash and Receivables

8,900

Investment in

Pleasantdale Dairy

Acquisition

Price

270,000

252,000

Basic

18,000

Excess Reclass.

0

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

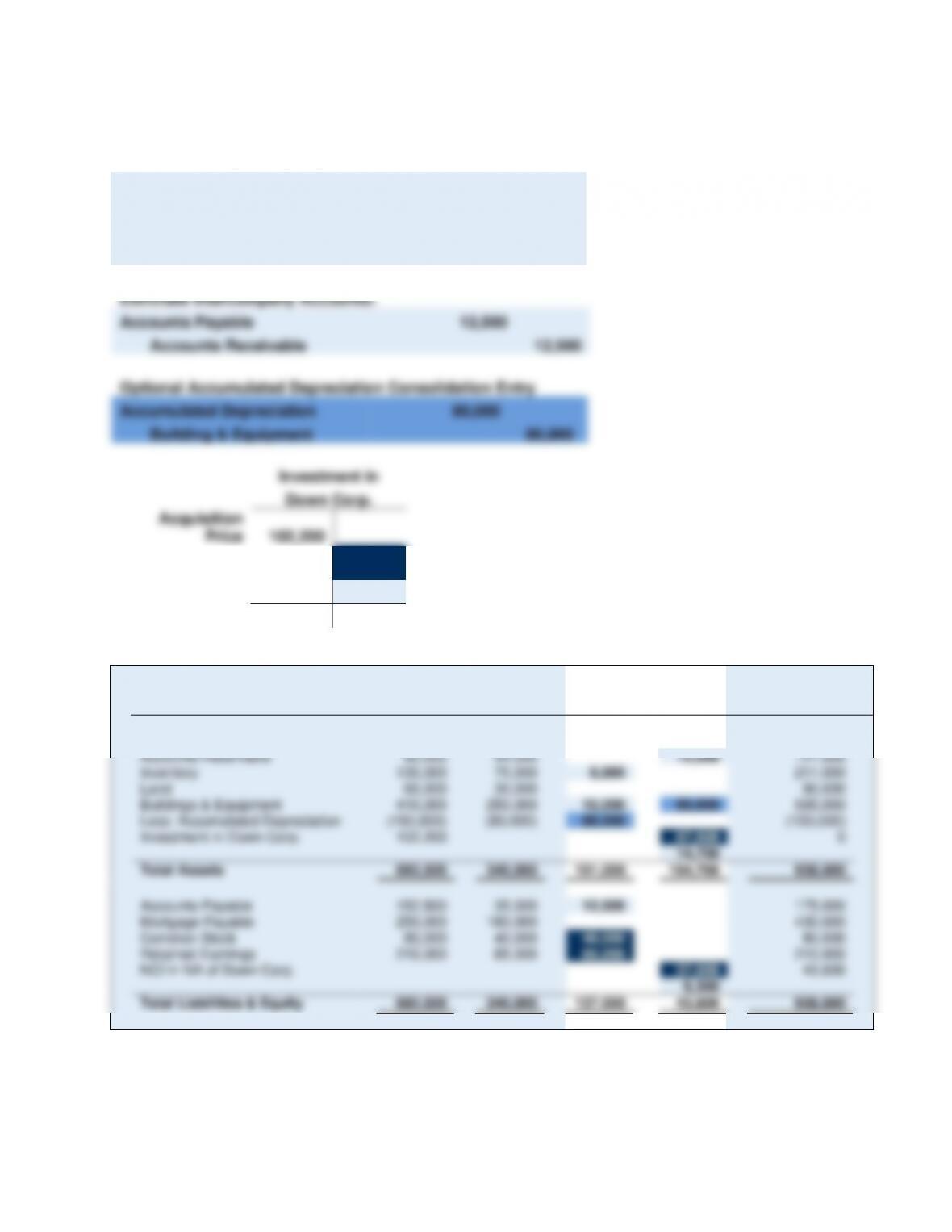

E5-6 Majority-Owned Subsidiary Acquired at Greater than Book Value

a.

Equity Method Entries on Zenith Corp.’s Books:

Investment in Down Corp.

102,200

Cash

102,200

Record the initial investment in Down Corp.

Book Value Calculations:

NCI

30%

+

Zenith

Corp.

70%

=

Common

Stock

+

Retained

Earnings

Book value at

acquisition

37,500

87,500

40,000

85,000

Basic Consolidation Entry

Common Stock

40,000

Retained Earnings

85,000

Investment in Down Corp.

NCI in NA of Down Corp.

Excess Value (Differential) Calculations:

+

=

Inventory

+

Beginning balances

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-15

E5-6 (continued)

Excess Value (Differential) Reclassification Entry:

Inventory

6,000

Buildings & Equipment

15,000

Investment in Down Corp.

14,700

NCI in NA of Down Corp.

6,300

Eliminate Intercompany Accounts:

Accounts Payable

12,500

Accounts Receivable

12,500

Optional Accumulated Depreciation Consolidation Entry

Accumulated Depreciation

80,000

Building & Equipment

80,000

Investment in

Down Corp.

Acquisition

Price

102,200

87,500

Basic

14,700

Excess Reclass.

0

b.

Zenith

Corp.

Down

Corp.

Consolidation

Entries

DR

CR

Consolidated

Balance Sheet

Cash

50,300

21,000

71,300

Accounts Receivable

90,000

44,000

12,500

121,500

Inventory

130,000

75,000

6,000

211,000

Land

60,000

30,000

90,000

Buildings & Equipment

410,000

250,000

15,000

80,000

595,000

Less: Accumulated Depreciation

(150,000)

(80,000)

80,000

(150,000)

Investment in Down Corp.

102,200

87,500

0

14,700

Total Assets

692,500

340,000

101,000

194,700

938,800

Accounts Payable

152,500

35,000

12,500

175,000

Mortgage Payable

250,000

180,000

430,000

Common Stock

80,000

40,000

40,000

80,000

Retained Earnings

210,000

85,000

85,000

210,000

NCI in NA of Down Corp.

37,500

43,800

6,300

Total Liabilities & Equity

692,500

340,000

137,500

43,800

938,800

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-16

E5-6 (continued)

c.

Zenith Corporation and Subsidiary

Consolidated Balance Sheet

December 31, 20X4

Cash

$ 71,300

Accounts Receivable

121,500

Inventory

211,000

Land

90,000

Buildings and Equipment

$595,000

Less: Accumulated Depreciation

(150,000)

445,000

Total Assets

$938,800

Accounts Payable

$175,000

Mortgage Payable

430,000

Stockholders’ Equity:

Controlling Interest:

Common Stock

$ 80,000

Retained Earnings

210,000

Total Controlling Interest

$290,000

Noncontrolling Interest

43,800

Total Stockholders’ Equity

333,800

Total Liabilities and Stockholders’ Equity

$938,800

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

E5-7 Consolidation with Minority Interest

Equity Method Entries on Temple Corp.’s Books:

Investment in Dynamic Corp.

390,000

Cash

390,000

Record the initial investment in Dynamic Corp.

Book Value Calculations:

NCI

25%

+

Temple

Corp.

75%

=

Common

Stock

+

Retained

Earnings

Book value at

acquisition

90,000

270,000

120,000

240,000

Basic Consolidation Entry

Common stock

120,000

Retained earnings

240,000

Investment in Dynamic Corp.

NCI in NA of Dynamic Corp.

Excess Value (Differential) Calculations:

+

=

Buildings

+

Inventories

+

Goodwill

Beginning balances

40,000

Excess Value (Differential) Reclassification Entry:

Buildings

80,000

Inventories

36,000

Goodwill

44,000

120,000

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-18

E5-8 Multiple-Choice Questions on Balance Sheet Consolidation

1.

d –

$215,000

=

$130,000 + $70,000 + ($85,000 – $70,000)

2.

c –

$40,000

=

($150,500 + $64,500) – ($405,000 – $28,000 – $37,000

– $200,000) – $15,000 – $20,000

3.

b –

$1,121,000

=

Total Assets of Power Corp.

$ 791,500

Less: Investment in Silk Corp.

(150,500)

$ 641,000

Book value of assets of Silk Corp.

405,000

Book value reported by Power and

Silk

$1,046,000

Increase in inventory ($85,000 – $70,000)

15,000

Increase in land ($45,000 – $25,000)

20,000

Goodwill

40,000

Total assets reported

$1,121,000

4.

d –

$701,500

=

($61,500 + $95,000 + $280,000) + ($28,000 + $37,000

+ $200,000)

5.

d –

$64,500

6.

d –

$205,000

=

The amount reported by Power Corporation

7.

c –

$419,500

=

($150,000 + $205,000) + $64,500

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

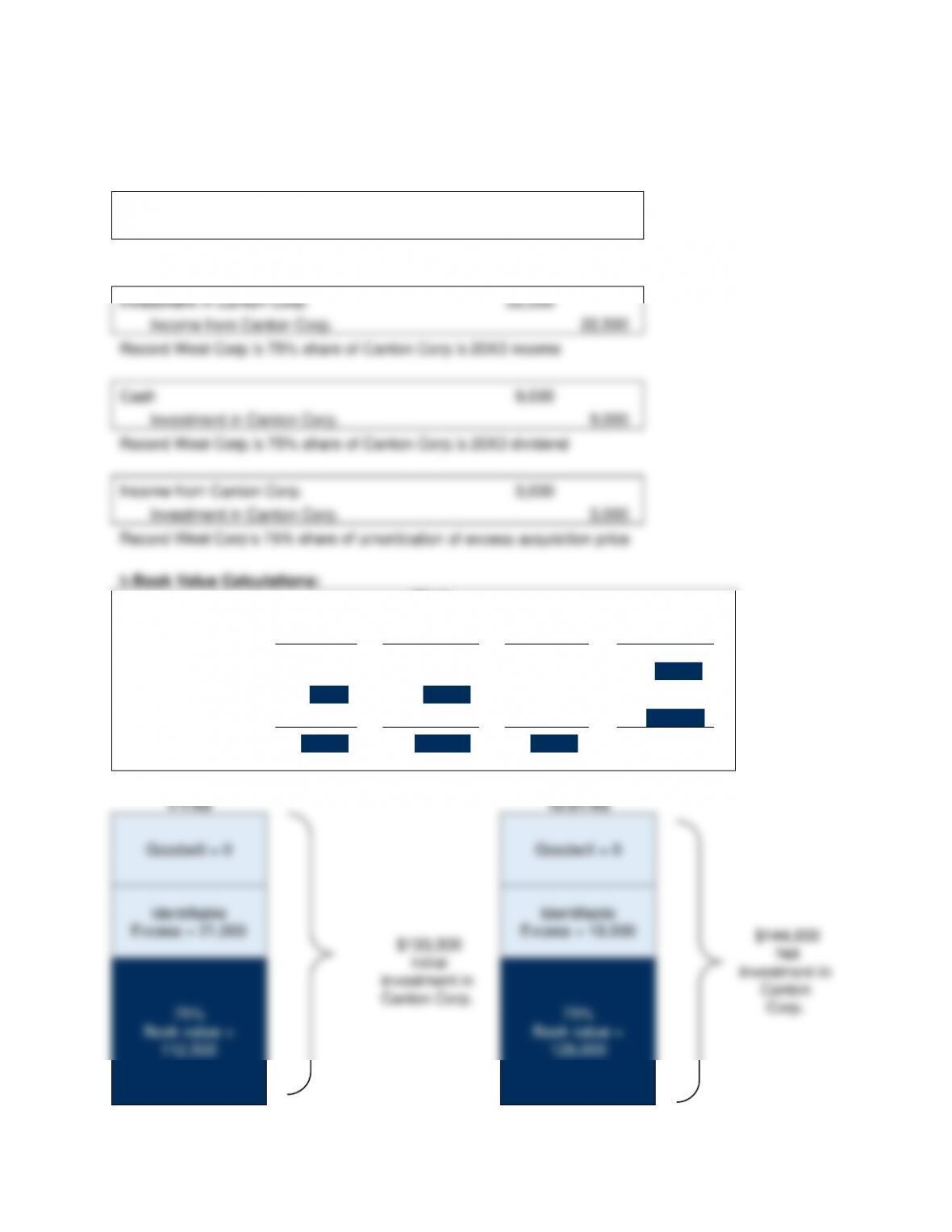

E5-9 Majority-Owned Subsidiary with Differential

a.

Equity Method Entries on West Corp.’s Books:

Investment in Canton Corp.

133,500

Cash

133,500

Record the initial investment in Canton Corp.

Investment in Canton Corp.

22,500

Income from Canton Corp.

22,500

Record West Corp.’s 75% share of Canton Corp.’s 20X3 income

Cash

9,000

Investment in Canton Corp.

9,000

Record West Corp.’s 75% share of Canton Corp.’s 20X3 dividend

Income from Canton Corp.

3,000

Investment in Canton Corp.

3,000

Record West Corp’s 75% share of amortization of excess acquisition price

+ Net Income

– Dividends

Ending book value

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-20

E5-9 (continued)

Basic Consolidation Entry

Common Stock

60,000

Retained Earnings

90,000

Income from Canton Corp.

22,500

NCI in NI of Canton Corp.

7,500

Dividends Declared

12,000

Investment in Canton Corp.

126,000

NCI in NA of Canton Corp.

42,000

Excess Value (Differential) Calculations:

NCI

25%

+

West Corp.

75%

=

Equipment

+

Acc. Depr.

Beginning balance

7,000

21,000

28,000

0

Changes

(1,000)

(3,000)

(4,000)

Ending balance

6,000

18,000

28,000

(4,000)

Amortized Excess Value Reclassification Entry:

Depreciation Expense

4,000

Income from Canton Corp.

3,000

NCI in NI of Canton Corp.

1,000

Excess Value (Differential) Reclassification Entry:

Equipment

28,000

Acc. Depr.

4,000

Investment in Canton Corp.

18,000

NCI in NA of Canton Corp.

6,000

Investment in

Income from

Canton Corp.

Canton Corp.

Acquisition Price

133,500

75% Net Income

22,500

22,500

75% Net Income

9,000

75% Dividends

3,000

Excess Val. Amort.

3,000

Ending Balance

144,000

19,500

Ending Balance

126,000

Basic

22,500

18,000

Excess Reclass.

3,000

Amort. Reclass

0

0