Chapter 20 – Corporations in Financial Difficulty

Q20-1 The nonjudicial actions available to a financially distressed company are debt

Q20-2 The major difference between a Chapter 7 action and a Chapter 11 action is that

Q20-3 Under two circumstances an involuntary petition for relief may be filed. The first

circumstance is that the debtor is generally not paying debts as they become due. The

Q20-4 The following items are usually included in the Plan of Reorganization filed as

Q20-7 The financial statements that must be filed by a company during a Chapter 11

Q20-8 The rights of creditors with priority in a Chapter 7 liquidation are to receive any

Q20-9 The statement of affairs is the basic accounting report made at the beginning of

the liquidation process to present the expected realizable amounts from disposal of the

report.

Q20-10 A trustee who takes title to the debtor’s assets in a liquidation must make a

periodic financial report to the bankruptcy court reporting on the progress of the

assets.

Q20-11 Sales of assets are reported in the statement of realization and liquidation as

Copyright © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized

for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website in whole or part.

C20-1 Creditors’ Alternatives

The options to the creditors are (1) form a creditors‘ committee, (2) a Chapter 11

reorganization, and (3) a Chapter 7 liquidation. The eventual decision must rest upon the

creditors’ assessment of the viability of the rehabilitation of the debtor versus the

liquidation values of the debtor’s assets.

payments from the debtor.

The creditors’ committee is a nonjudicial action that provides for flexibility to both the

creditors and the debtor. The creditors’ committee typically works with the debtor

company to enact a plan of settlement of the debtor’s indebtedness. In some cases, the

creditors may assume management control of the company, but most creditors are

C20-2 Research Related to Bankruptcy

The website for the U.S. Bankruptcy Courts is:

http://www.uscourts.gov/FederalCourts/Bankruptcy.aspx

a. The Frequently Asked Questions (FAQs) for the U.S. Courts

(1) Total business filings are presented at the top of the form for business and

nonbusiness filings for the twelve month period ended for the most recent year.

Code.

(2) Students should find the Federal judicial district in which their educational institution

is located. The larger states typically have several districts and students may have

to make an assumption for which district they are located. It is instructive to see that

C20-3 Selection of Bankruptcy Trustee and Trustee’s Responsibilities

Title 11 of the United States Code may be obtained from several sources through using

a web search with the term, “Title 11 of the U.S. Code.” The case asks about trustees

for a Chapter 7 bankruptcy filing.

a. Subchapter 1 of Chapter 7 of Title 11 of the U.S. Code specifies the administration of

C20-4 The Bankruptcy of WorldCom

Overall, the 2002 bankruptcy of WorldCom resulted in a cumulative net reduction to their

shareholders’ equity of $70.8 billion as of December 31, 2001, and a reduction in

previously reported net income of $17.1 billion and $53.1 billion for the years ended

December 31, 2001, and 2000 respectively. Goodwill of $44.9 billion was reduced to

irregularities, and to protect the company from lawsuits from creditors and others.

For example, on June 26, 2002, the SEC filed a civil suit against the company for its

past financial reports. On April 29, 2002, Bernard Ebbers resigned as President and

Chief Executive Officer. The company undoubtedly felt it needed the protection of

bankruptcy to give it time to study the breadth of its financial and accounting

accounting irregularity that initiated the internal review.

d. (Source: Item 7, Management’s Discussion and Analysis) Item 7 of the company’s

2002 10-K presents a section titled “Restatements and Reclassifications of

Previously Issued Consolidated Financial Statements”. A table is presented that

summarizes the restatement items on revenue and pre-tax income or loss for the

C20-4 (continued)

Year Ended

December 31, 2001

Year Ended

December 31, 2000

Item:

Revenue

Pre-tax

income (loss)

Revenue

Pre-tax

income (loss)

Previously reported

35,121

2,375

39,020

7,581

Restatement adjustments:

1. Impairment

—

(12,592)

—

(47,180)

2. Improper reduction

of access costs

—

(2,933)

6

(1,827)

3. Purchase accounting

14

(2,273)

(193)

(3,567)

4. Long lived asset

adjustments

—

2,750

—

(1,713)

5. International adjustments

(749)

(899)

18

(487)

6. Revenue related

adjustments

(1,204)

(575)

(36)

(995)

7. Adjustments to

accrued liabilities

—

(823)

—

(732)

8. Embratel and

Avantel acquisitions

5,268

(35)

1,127

(325)

9. Unclassified income/

(expense)

—

383

—

(426)

10. Other

(7)

(506)

4

(750)

Total adjustment items

3,322

(17,503)

926

(58,002)

Discontinued Operations

Adjustment

(775)

1,323

(602)

449

Revenue, as restated

37,668

39,344

Minority interest adjustment

(669)

52

Pre-tax loss, as restated

(14,474)

(49,920)

1. Impairment: The company discovered that impairment tests had not been

2. Improper reduction of access costs: The primary adjustments for this item were

3. Purchase accounting: The company made numerous acquisitions, including the

MCI acquisition, between 1993 and 2001 and a review of these acquisitions

C20-4 (continued)

4. Long lived asset accounting: This item includes adjustments to depreciation and

5. International: Adjustments were made for correcting the U.S. GAAP-based

6. Revenue related adjustments: A number of adjustments were made because of

101. In addition, the company had incorrectly accounted for some contracts as

costs.

7. Adjustments to accrued liabilities: Adjustments were made to eliminate improper

8. Embratel and Avantel acquisitions: A review of the Embratel acquisition showed

an incorrect interpretation with regard to not having control over Embratel and

9. Unclassified income/ (expense): A review of several accrued liability accounts

showed that there was inadequate documentation to support the accruals. Also,

10. Other: The company made a number of reclassifications, revaluations of

derivatives, intercompany balances, and certain capitalized costs such as

interest, labor and overhead for capital projects.

These adjustments were also carried through the restated balance sheet and

statement of cash flows for 2001 and 2000.

Copyright © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized

E20-1 Multiple-Choice Questions on Chapter 11 Reorganizations [AICPA

Adapted]

1.

c –

Correct

(a) incorrect. A trustee or receiver is not given stewardship over the company in

nonjudical actions.

(b) incorrect. If there are dissenting creditors, the other creditors can choose to

allow those in dissent to still be paid in full.

(d) incorrect. The payment is typically immediate as a result of the creditor not

collecting on the entire debt.

2.

d –

A trustee cannot be designated during a nonjudical action. A court must designate

a trustee.

(a) incorrect. The debtor is the party that submits the petition for temporary

protection from its creditors.

(b) incorrect. Her personal bankruptcy status will not be resolved by the

companies’ bankruptcy proceedings.

(c) incorrect. A plan of reorganization is filed by the debtor.

3.

c –

A reasonable investor or creditor must be able to make an informed judgment

about the worthiness of the plan.

(a) incorrect. This takes place in a Chapter 7 Liquidation

(b) incorrect. By instituting a composition agreement a creditor can accept an

impaired amount of money to satisfy the debt.

(d) incorrect. Not all claims are treated alike in a Chapter 11 reorganization.

4.

d –

The debtor must have 12 creditors, and the required number of creditors signing

the petition must be owed at least $5,000 in total.

5.

c –

The plan must be approved by at least half of all creditors who hold at least two-

thirds of the total debt.

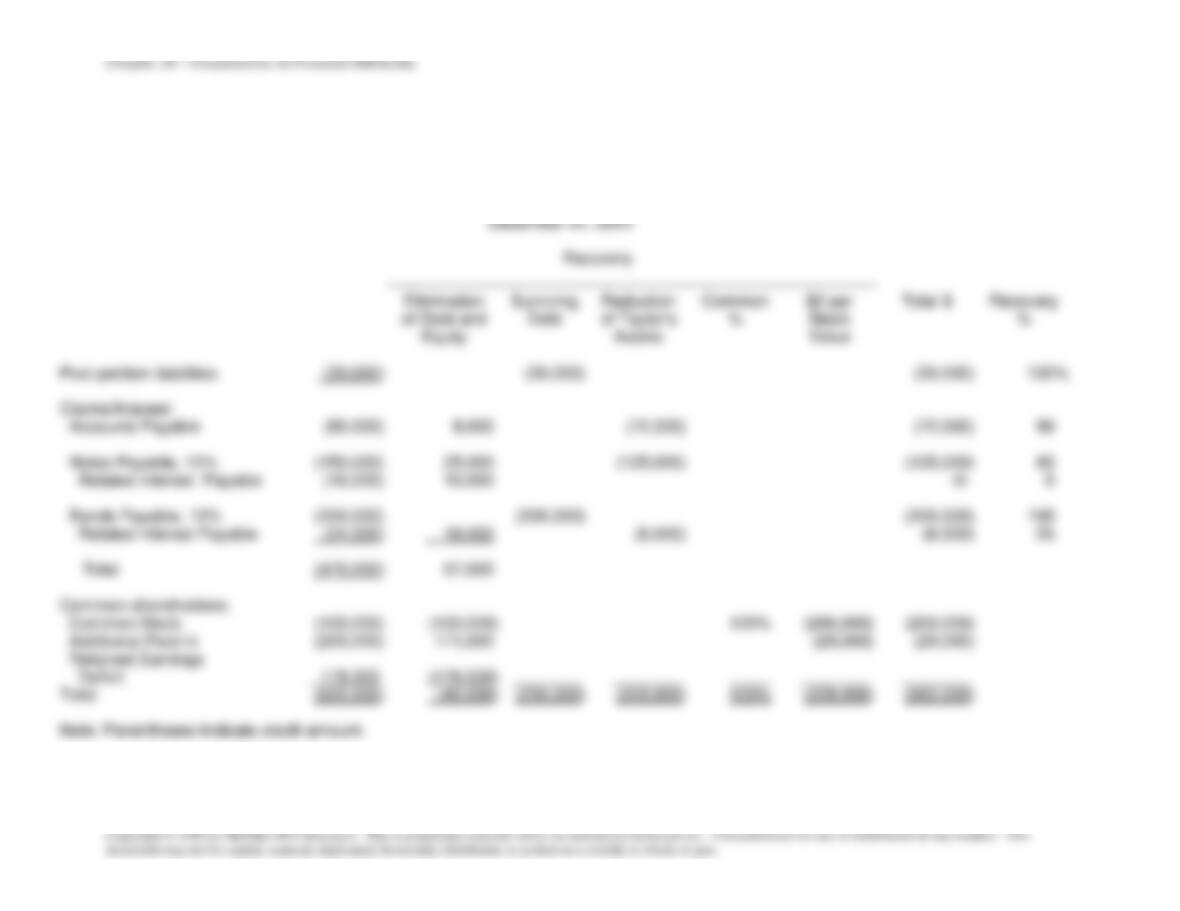

E20-2 Recovery Analysis for a Chapter 11 Reorganization

a.

Recovery analysis for plan of reorganization:

Taylor Companies, Inc.

Plan of Reorganization

Recovery Analysis

December 31, 20X1

Recovery

Elimination

of Debt and

Equity

Surviving

Debt

Reduction

of Taylor’s

Assets

Common

%

$2 par

Stock

Value

Total $

Recovery

%

Post-petition liabilities

(30,000)

(30,000)

(30,000)

100%

Claims/Interest:

Accounts Payable

(80,000)

8,000

(72,000)

(72,000)

90

Notes Payable, 10%

(150,000)

25,000

(125,000)

(125,000)

83

Related Interest Payable

(16,000)

16,000

-0-

0

Bonds Payable, 12%

(200,000)

(200,000)

(200,000)

100

Related Interest Payable

(24,000)

18,000

(6,000)

(6,000)

25

Total

(470,000)

67,000

Common shareholders:

Common Stock

(100,000)

(100,000)

100%

(200,000)

(200,000)

Additional Paid-In

(200,000)

171,000

(29,000)

(29,000)

Retained Earnings

Deficit

178,000

(178,000)

Total

(622,000)

(40,000)

(230,000)

(203,000)

100%

(229,000)

(662,000)

Note: Parentheses indicate credit amount.