Chapter 06 – Intercompany Inventory Transactions

Q6-1 All inventory transfers between related companies must be eliminated to avoid an

Q6-2 An inventory transfer at cost results in an overstatement of sales and cost of goods sold.

Q6-3 An upstream sale occurs when the parent purchases items from one or more

subsidiaries. A downstream sale occurs when the sale is made by the parent to one or more

Q6-4 As in all cases, the total amount of the unrealized profit must be eliminated in preparing

Q6-5 Consolidated net income is reduced by the full amount of the unrealized profits. In the

upstream sale, the unrealized profits are apportioned between the parent company

Q6-6 The elimination of unrealized intercompany profits on an upstream sale will have a

greater effect on income assigned to the noncontrolling interest. Income assigned to the

Q6-7 The basic consolidation entry needed when the item is resold before the end of the

period is:

Sales

XXXXXX

Cost of Goods Sold

XXXXXX

Copyright © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized

for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website in whole or part.

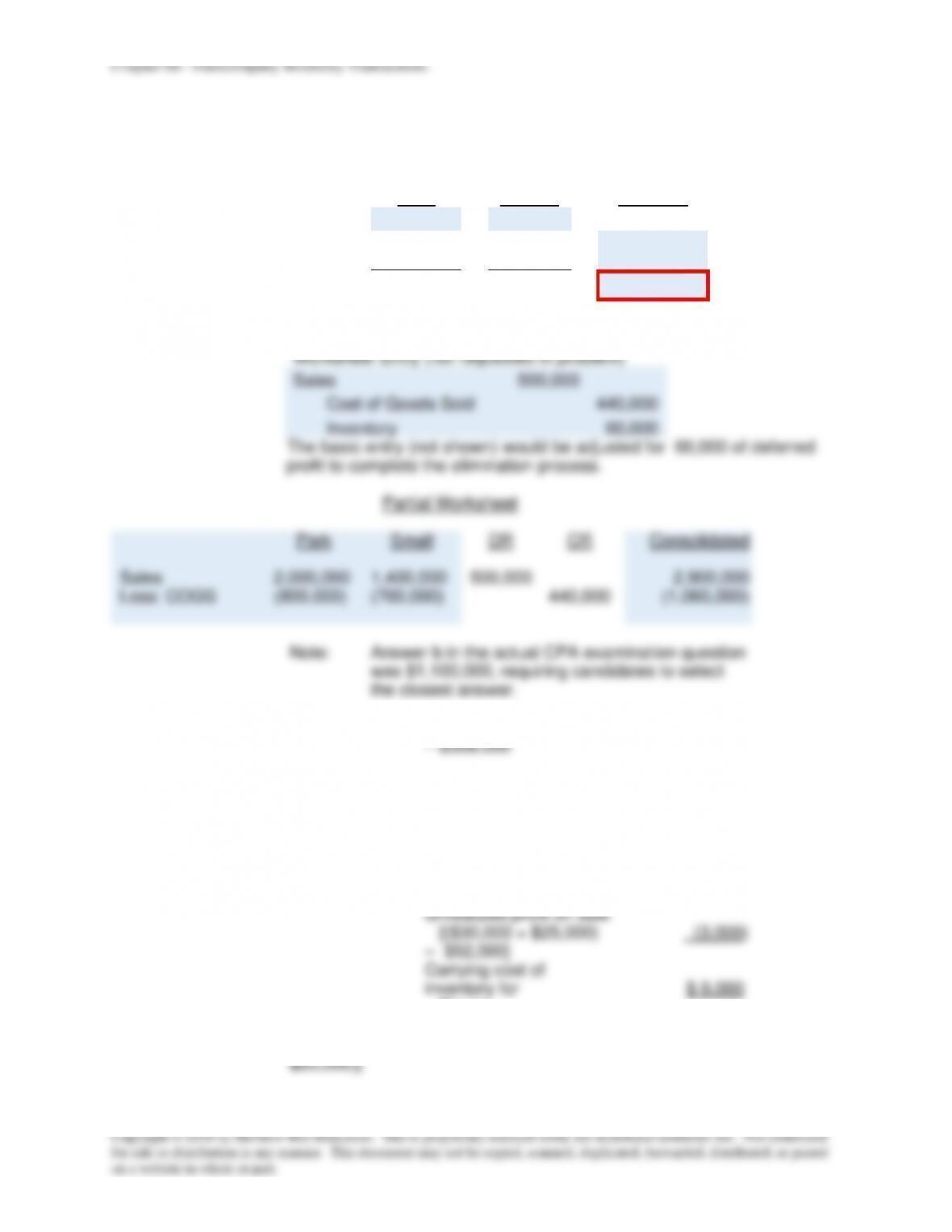

Q6-8 The consolidation entry needed when one or more of the items are not resold before the

end of the period is:

Sales

XXXXXX

Cost of Goods Sold

XXXXXX

Inventory

XXXXXX

The debit to sales is for the full amount of the transfer price. Inventory is credited for the

unrealized profit at the end of the period and cost of goods sold is credited for the amount

charged to cost of goods sold by the company making the intercompany sale. Additionally, the

basic consolidation entry would need to be adjusted to reflect the deferred gross profit.

Q6-9 Cost of goods sold is reported by the consolidated entity when inventory is sold to an

external party. The amount reported as cost of goods sold is based on the amount paid for the

Q6–10 No adjustment to retained earnings is needed if the intercorporate sales have been

made at cost or if all intercorporate sales have been resold to an external party in the same

accounting period. If all of the intercorporate sales have not been resold by the end of the

Q6–11 A proportionate share of the realized retained earnings of the subsidiary are assigned to

Q6–12 When inventory profits from a prior period intercompany transfer are realized in the

current period, the profit is added to consolidated net income and to the income assigned to the

shareholders of the company that made the intercompany sale. If the unrealized profits arise

Q6–13 Under the fully adjusted equity method, consolidated retained earnings is not affected

directly by unrealized profits. Unrealized profits are deferred in the investment in sub and

income from sub accounts on the parent’s books. Income from sub is closed out to retained

Copyright © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized

for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website in whole or part.

C6-1 Measuring Cost of Goods Sold

a. While the rule covers only a part of the elimination needed, Charlie is correct in that the cost

of goods sold recorded by the selling company must be eliminated to avoid overstating that

portion of the consolidated income statement.

profit.

Copyright © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized

for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website in whole or part.

E6-1 Multiple-Choice Questions on Intercompany Inventory Transfers

1. a – All intercompany sales and cost of goods sold must be eliminated in consolidation to

prevent double counting.

(b) Incorrect. The entire amount of sales and cost of goods gold must be eliminated.

(c) Incorrect. Net income is not directly reduced with a consolidation entry. Instead, sales

and cost of goods sold are adjusted.

(d) Incorrect. Adjustments to sales and cost of goods sold are required.

2. c – $500,000 = ($400,000 +$350,000 – $250,000)

3. a – $56,000 = ($40,000 *1.4)

4. c – $56,000. The revenue would be overstated by the amount of cost of goods sold that

should have been eliminated.

5

c –

Net assets reported

$320,000

Profit on intercompany sale

$48,000

Proportion of inventory unsold at year end

($60,000 / $240,000)

x 0.25

Unrealized profit at year end

(12,000)

Amount reported in consolidated statements

$308,000

6

c –

Inventory reported by Banks ($175,000 + $60,000)

$235,000

Inventory reported by Lamm

250,000

Total inventory reported

$485,000

Unrealized profit at year end

[$50,000 x ($60,000 / $200,000)]

(15,000)

Amount reported in consolidated statements

$470,000