Chapter 18 – Governmental Entities: Special Funds and Government–Wide Financial Statements

P18-13 (continued)

Fund

Journal Entries

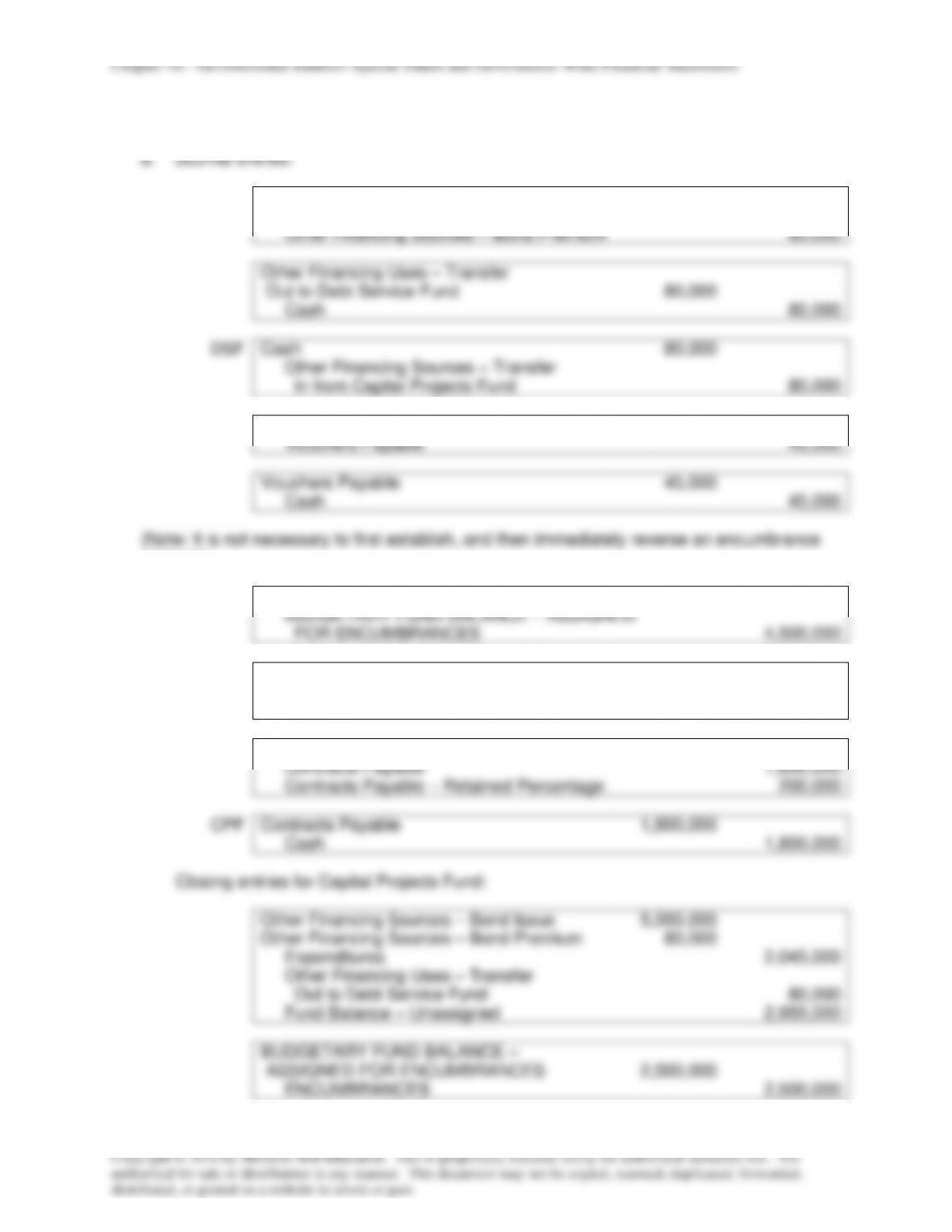

7.

Capital

ENCUMBRANCES

75,000

Projects

BUDGETARY FUND BALANCE – ASSIGNED

Fund

FOR ENCUMBRANCES

75,000

BUDGETARY FUND BALANCE – ASSIGNED

FOR ENCUMBRANCES

75,000

ENCUMBRANCES

75,000

Expenditures

75,000

Contracts Payable

75,000

Contracts Payable

75,000

Cash

75,000

8.

Internal

Inventory of Supplies

1,900

Service

Cash (or Vouchers Payable)

1,900

Fund

9.

General

Cash

393,000

Fund

Taxes Receivable – Current

386,000

Revenue – Licenses and Fees

7,000

Allowance for Uncollectibles – Current

3,800

Revenue – Taxes

3,800

Estimate

$7,800

Actual

(4,000)

Correction

$3,800

10.

Capital

Cash

500,000

Projects

Other Financing Sources – Bond Issue

500,000

Fund

11.

General

BUDGETARY FUND BALANCE – ASSIGNED

Fund

FOR ENCUMBRANCES

15,000

ENCUMBRANCES

15,000

Expenditures

15,000

Cash

15,000

Chapter 18 – Governmental Entities: Special Funds and Government–Wide Financial Statements

P18-18 Questions on Fund Transactions [AICPA Adapted]

1.

$104,500

(Stated in item #3.)

2.

$17,000

(Stated in item #4.)

3.

$125,000

(Item #5 states that $83,000 is assigned for encumbrances. To this

is added the $42,000 reserve for the ending inventory.)

4.

$236,000

(Item #1 states that $600,000 of bond proceeds were received in

the capital project fund, less $364,000 of construction expenditures

in the period.)

5.

$6,000

(Item #2 states that $109,000 tax revenues were received from

which $81,000 and $22,000 was expended.)

6.

$104,500

(Stated in item #3.)

7.

$386,000

(Item #1 states construction expenditures of $364,000 plus item #2

states a motor vehicle purchase of $22,000.)

8.

$100,000

(Item #3 states a reduction in long-term debt principal of

$100,000.)

9.

$181,000

(Item #6 states that $181,000 was used to purchase supplies

during the period.)

10.

$190,000

(Item #6 states encumbrances of $190,000.)