In accordance with the Single Audit Act of 1984, external auditors issue the standard

audit report on the governmental unit’s financial statements and must also issue:

I. a special report on the effectiveness with which the governmental unit is achieving its

social objectives.

II. a special report on the governmental unit’s internal control system.

III. a special report on the governmental unit’s compliance with laws and regulations.

A. I only

B. I and II

C. II and III

D. I, II, and III

Nash Company acquired Seel Corporation through an exchange of common shares. All

of Seel’s assets and liabilities were immediately transferred to Nash. Nash’s common

stock was trading at $25 per share at the time of the exchange. The total par value of

Nash’s stock outstanding before and after the acquisition was $750,000 and $840,000,

respectively. Nash’s additional paid-in capital before and after the acquisition were

$200,000 and $560,000, respectively.

Based on the preceding information, what is the fair value of Seel’s net assets if

goodwill of $20,000 is recorded in the acquisition?

A. $430,000

B. $470,000

C. $540,000

D. $580,000

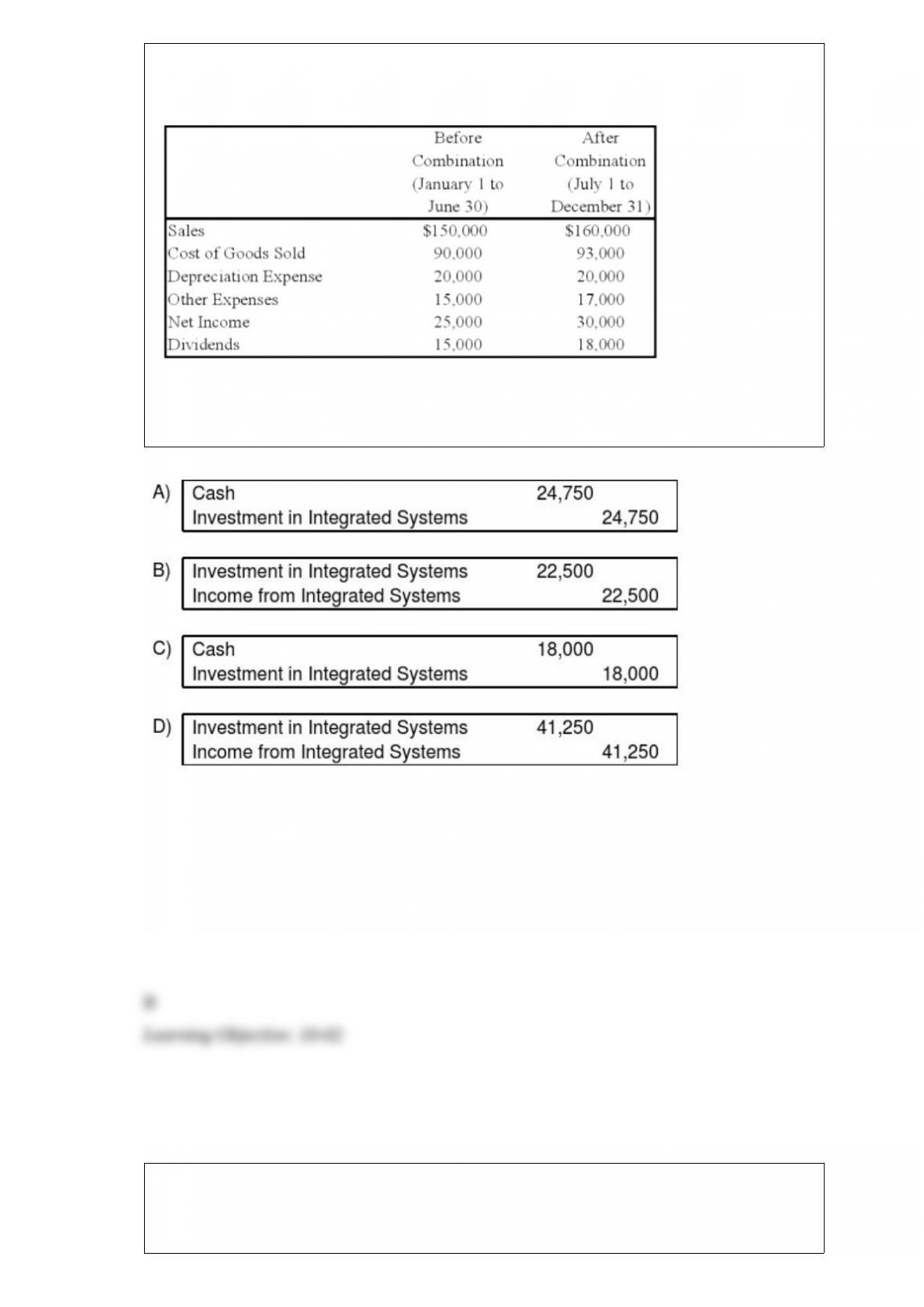

On July 1, 20X8, Fair Logic Corporation acquires 75 percent of Integrated Systems Inc.

common stock for its underlying book value. At the time of acquisition, the fair value of

the noncontrolling interest is equal to its proportionate share of book value of Integrated

Systems. On January 1, 20X8 Integrated reported common stock of $100,000 and

retained earnings of $130,000. For the year 20X8, Integrated reports the following

items:

Fair Logic uses the equity method in accounting for this investment.

Based on the preceding information, what journal entry would Fair Logic make to

record equity method income for the year?

A. Option A

B. Option B

C. Option C

D. Option D

On December 31, 20X1, Oak Corporation acquired 100 percent ownership of Cherry

Corporation. On that date, Cherry reported assets and liabilities with books values of

$450,000 and $200,000, respectively, common stock outstanding of $150,000, and

retained earnings of $100,000. The book values and fair values of Cherry’s assets and

liabilities were identical except for land which had increased in value by $15,000 and

inventories which had decreased by $5,000.

Based on the preceding information, what amount of goodwill will be reported in the

consolidated balance sheet on the acquisition date if the acquisition price was

$280,000?

A. $10,000

B. $20,000

C. $30,000

D. $35,000

Identify the regulation that created an entity which insures investors from possible

losses if an investment house enters bankruptcy.

A. Federal Deposit Insurance Protection Act

B. Securities Investor Protection Act

C. Investment Advisers Act

D. Federal Bankruptcy Acts

The capital projects fund of Hood River completed construction of an addition to its

city hall at a cost of $4,000,000. The city council approved payment of the amount due

the general contractor, less a 10 percent retainage. How should the capital projects fund

account for the 10 percent retainage?

I. As a credit of $400,000 to Deferred Revenue-Retained Percentage

II. As a credit for $400,000 to Contracts Payable-Retained Percentage.

A. I only

B. II only

C. Either I or II

D. Neither I nor II

On January 1, 20X7, Pisa Company acquired 80 percent of Siena Company by

purchasing 40,000 shares of Siena’s common stock. There was no differential related to

this transaction. The noncontrolling interest had a fair value equal to 20 percent of book

value. The book value of Siena on December 31, 20X7 was as follows:

On January 1, 20X8, Pisa purchased an additional 12,500 shares directly from Siena for

$25 per share.

Based on the preceding information, the elimination entry to prepare the consolidated

financial statements on December 31, 20X7 would include a:

A. credit to common stock for $625,000

B. debit to retained earnings for $37,500

C. credit to Investment in Siena Co. for $976,500

D. credit to NCI in the net assets of Siena Co. for $232,500

Pilfer Company acquired 90 percent ownership of Scrooge Corporation in 20X7, at

underlying book value. On that date, the fair value of noncontrolling interest was equal

to 10 percent of the book value of Scrooge Corporation. Pilfer purchased inventory

from Scrooge for $90,000 on August 20, 20X8, and resold 70 percent of the inventory

to unaffiliated companies on December 1, 20X8, for $100,000. Scrooge produced the

inventory sold to Pilfer for $67,000. The companies had no other transactions during

20X8.

Based on the information given above, what inventory balance will be reported by the

consolidated entity on December 31, 20X8?

A. $51,490

B. $53,100

C. $37,000

D. $20,100

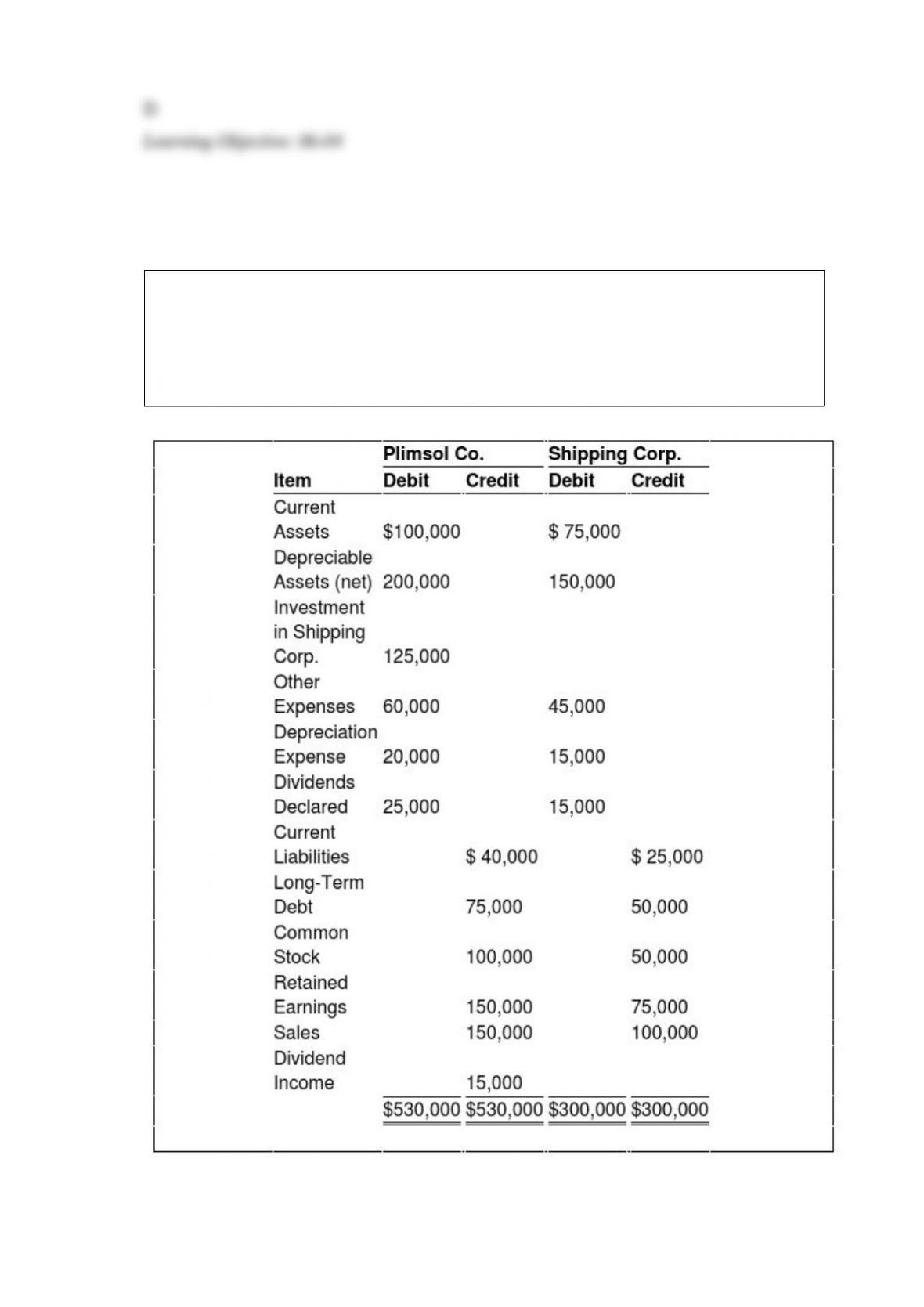

On January 1, 20X4, Plimsol Company acquired 100 percent of Shipping Corporation’s

voting shares, at underlying book value. Plimsol uses the cost method in accounting for

its investment in Shipping. Shipping’s retained earnings was $75,000 on the date of

acquisition. On December 31, 20X4, the trial balance data for the two companies are as

follows:

Based on the information provided, what amount of net income will be reported in the

consolidated financial statements prepared on December 31, 20X4?

A. $100,000

B. $85,000

C. $110,000

D. $125,000

The following information pertains to Auburn’s water and sewer fund, an enterprise

fund, for the year ended June 30, 20X9:

Based upon the information presented, what was the increase in the enterprise funds

unrestricted net assets for the fiscal year ended June 30, 20X9?

A. $200,000

B. $240,000

C. $300,000

D. $320,000

On January 1, 20X7, Pisa Company acquired 80 percent of Siena Company by

purchasing 40,000 shares of Siena’s common stock. There was no differential related to

this transaction. The noncontrolling interest had a fair value equal to 20 percent of book

value. The book value of Siena on December 31, 20X7 was as follows:

On January 1, 20X8, Siena sold an additional 12,500 shares to a nonaffiliate for $25 per

share.

Based on the preceding information, what is the ending balance in noncontrolling interest

in the net assets of Siena?

A. $186,000

B. $418,500

C. $523,125

D. $232,500

When an internal service fund (ISF) enters into a capital lease the transaction is

recorded in the:

I. fixed assets of the ISF.

II. long-term debt of the ISF.

A. I only

B. II only

C. Both I and II

D. Neither I nor II

On January 1, 20X9, Heathcliff Corporation acquired 80 percent of Garfield

Corporation’s voting common stock. Garfield’s buildings and equipment had a book

value of $300,000 and a fair value of $350,000 at the time of acquisition.

Based on the preceding information, what will be the amount at which Garfield’s

buildings and equipment will be reported in consolidated statements using the current

accounting practice?

A. $350,000

B. $340,000

C. $280,000

D. $300,000

Suppose the direct foreign exchange rates in U.S. dollars are as follows:

1 Swiss franc = $1.0371

1 Swedish krona = $0.1526

Based on the information given above, the indirect exchange rates for the Swiss franc

and the Swedish krona (from a U.S. perspective) are

A. 0.9642 Swiss francs and 6.5531 Swedish krona respectively.

B. 1.6893 Swiss francs and 5.2563 Swedish krona respectively.

C. 1.0371 Swiss francs and 0.1527 Swedish krona respectively.

D. 0.8372 Swiss francs and 4.2713 Swedish krona respectively.

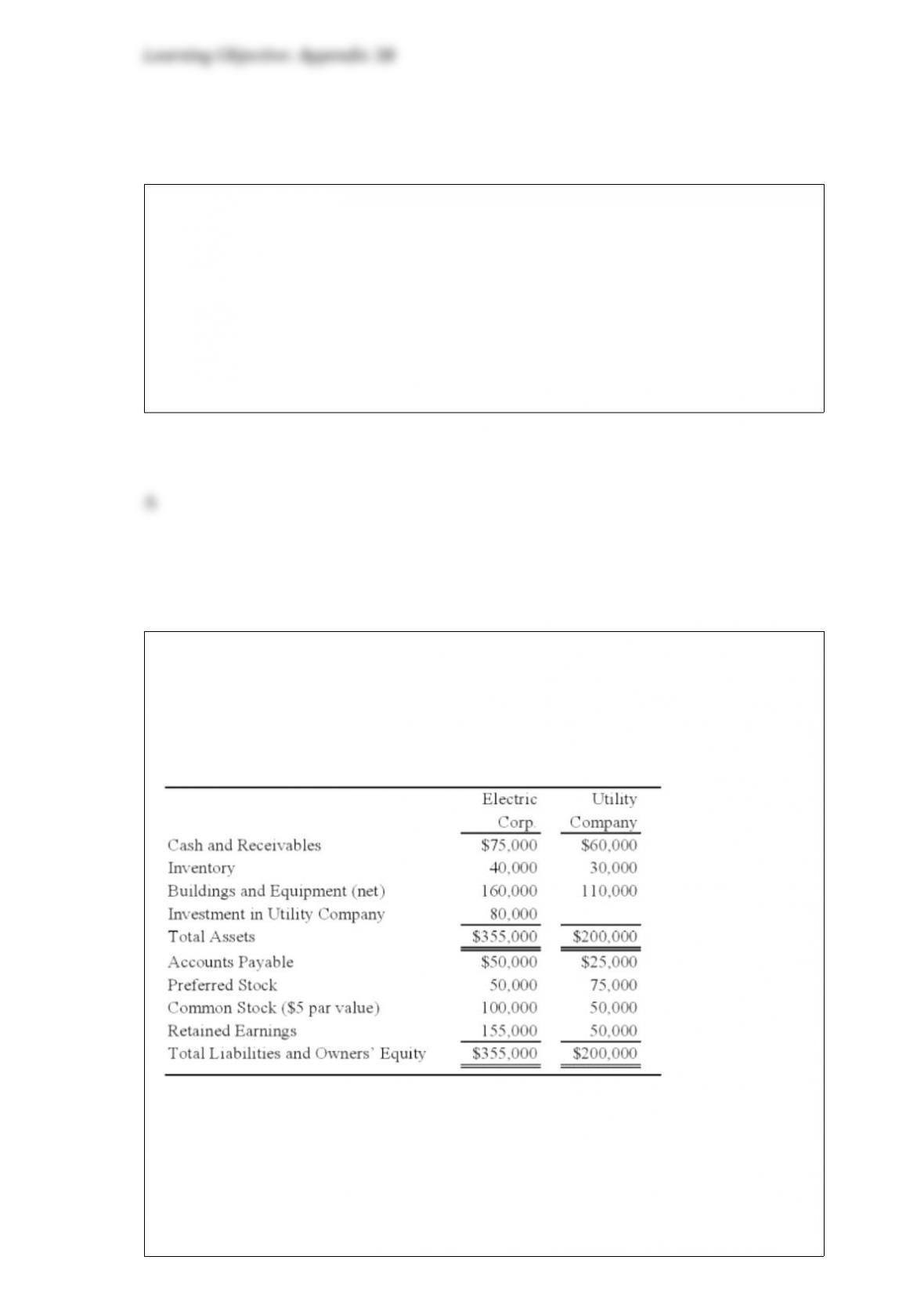

Electric Corporation holds 80 percent of Utility Company’s voting common shares,

acquired at book values, but none of its preferred shares. At the date of acquisition, the

fair value of the noncontrolling interest was equal to 20 percent of the book value of

Utility Company. Summary balance sheets for the companies on December 31, 20X8,

are as follows:

Neither of the preferred issues is convertible. Electric’s preferred pays a 8 percent

annual dividend, and Utility’s preferred pays a 12 percent dividend. Utility reported net

income of $30,000 and paid a total of $10,000 of dividends in 20X8. Electric reported

income from its separate operations of $70,000 and paid total dividends of $25,000 in

20X8.

Based on the preceding information, what is the consolidated earnings per share for

20X5?

A. $16.97

B. $17.42

C. $18.72

D. $19.17

ASC 280 requires certain disclosures about major customers. All of the following

statements about those disclosures are true with the exception of which statement?

A. The identity of the segment reporting the revenue from a significant customer must

be disclosed a footnote.

B. The amount of revenue from a significant customer must be disclosed in a footnote.

C. For applying the disclosure test a threshold of 10 percent of total revenues is

mandated.

D. A local, state, or foreign government can be considered a major customer.

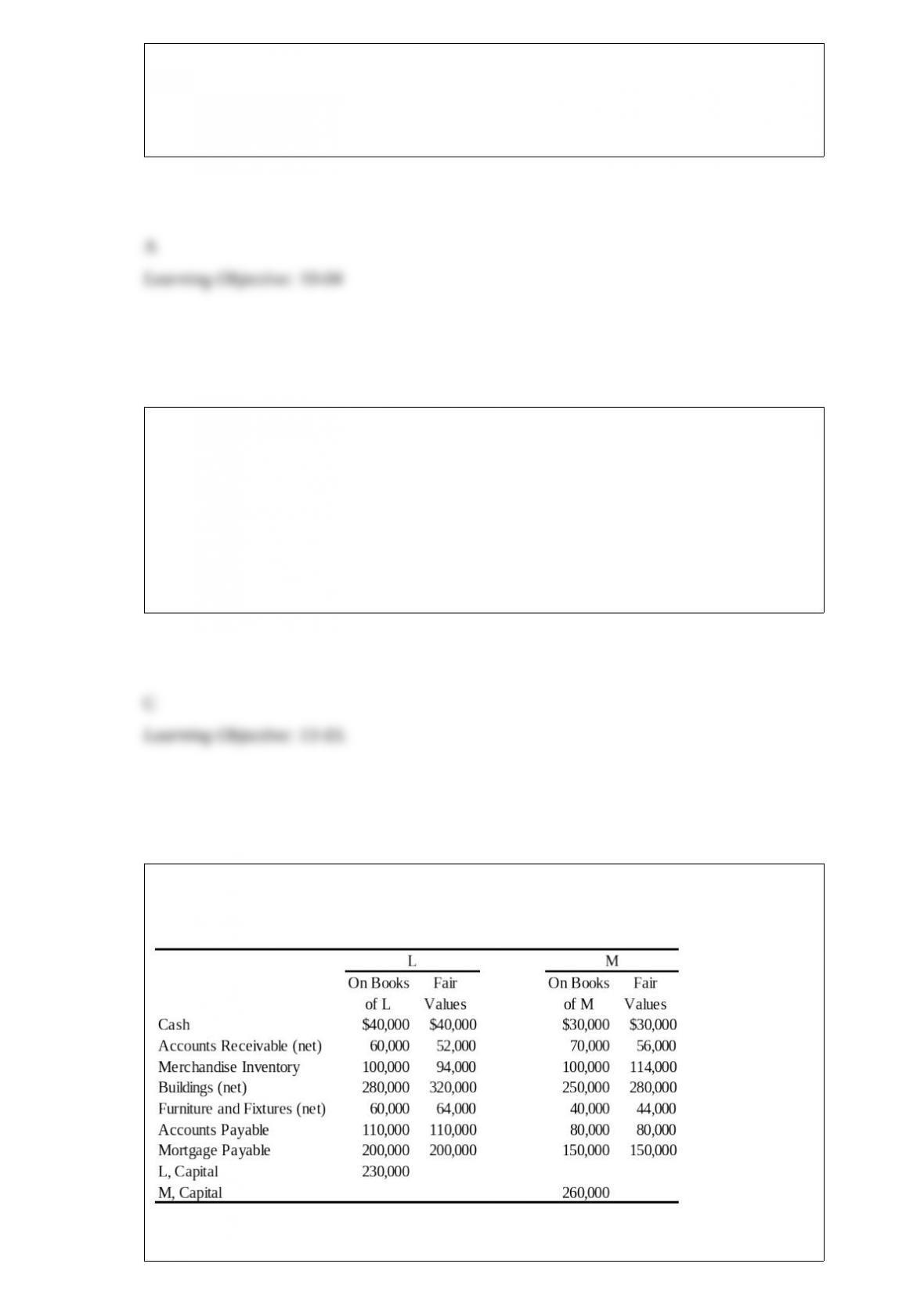

Two sole proprietors, L and M, agreed to form a partnership on January 1, 20X9. The

trial balance for each proprietorship is shown below as of January 1, 20X9.

The LM partnership will take over the assets and assume the liabilities of the

proprietors as of January 1, 20X9.

Required:

a) Prepare a balance sheet, for financial accounting purposes, for the LM partnership as

of January 1, 20X9.

b) In addition, assume that M agreed to recognize the goodwill generated by L’s

business. Accordingly, M agreed to recognize an amount for L’s goodwill such that L’s

capital equaled M’s capital on January 1, 20X9. Given this alternative, how does the

balance sheet prepared for requirement A change?

Senior Inc. owns 85 percent of Junior Inc. During 20X8, Senior sold goods with a 25

percent gross profit to Junior. Junior sold all of these goods in 20X8. How should 20X8

consolidated income statement items be adjusted?

A. No adjustment is necessary.

B. Sales and cost of goods sold should be reduced by 85 percent of the intercompany

sales.

C. Net income should be reduced by 85 percent of the gross profit on intercompany

sales.

D. Sales and cost of goods sold should be reduced by the intercompany sales.

Elvis Company purchases inventory for $70,000 on Mar 19, 20X8 and sells it to

Graceland Corporation for $95,000 on May 14, 20X8. Graceland still holds the

inventory on December 31, 20X8, and determines that its market value (replacement

cost) is $82,000 at that time. Graceland writes the inventory down from $95,000 to its

lower market value of $82,000 at the end of the year. Elvis owns 75 percent of

Graceland.

Based on the information given above, what amount of cost of goods sold should be

eliminated in the consolidation worksheet for 20X8?

A. $82,000

B. $70,000

C. $95,000

D. $60,000

On July 1, 20X4, Denver Corp. purchased 3,000 shares of Eagle Co.’s 10,000

outstanding shares of common stock for $20 per share. On December 15, 20X4, Eagle

paid $40,000 in dividends to its common stockholders. Eagle’s net income for the year

ended December 31, 20X4, was $120,000, earned evenly throughout the year. In its

20X4 income statement, what amount of income from this investment should Denver

report?

A. $12,000

B. $36,000

C. $18,000

D. $6,000

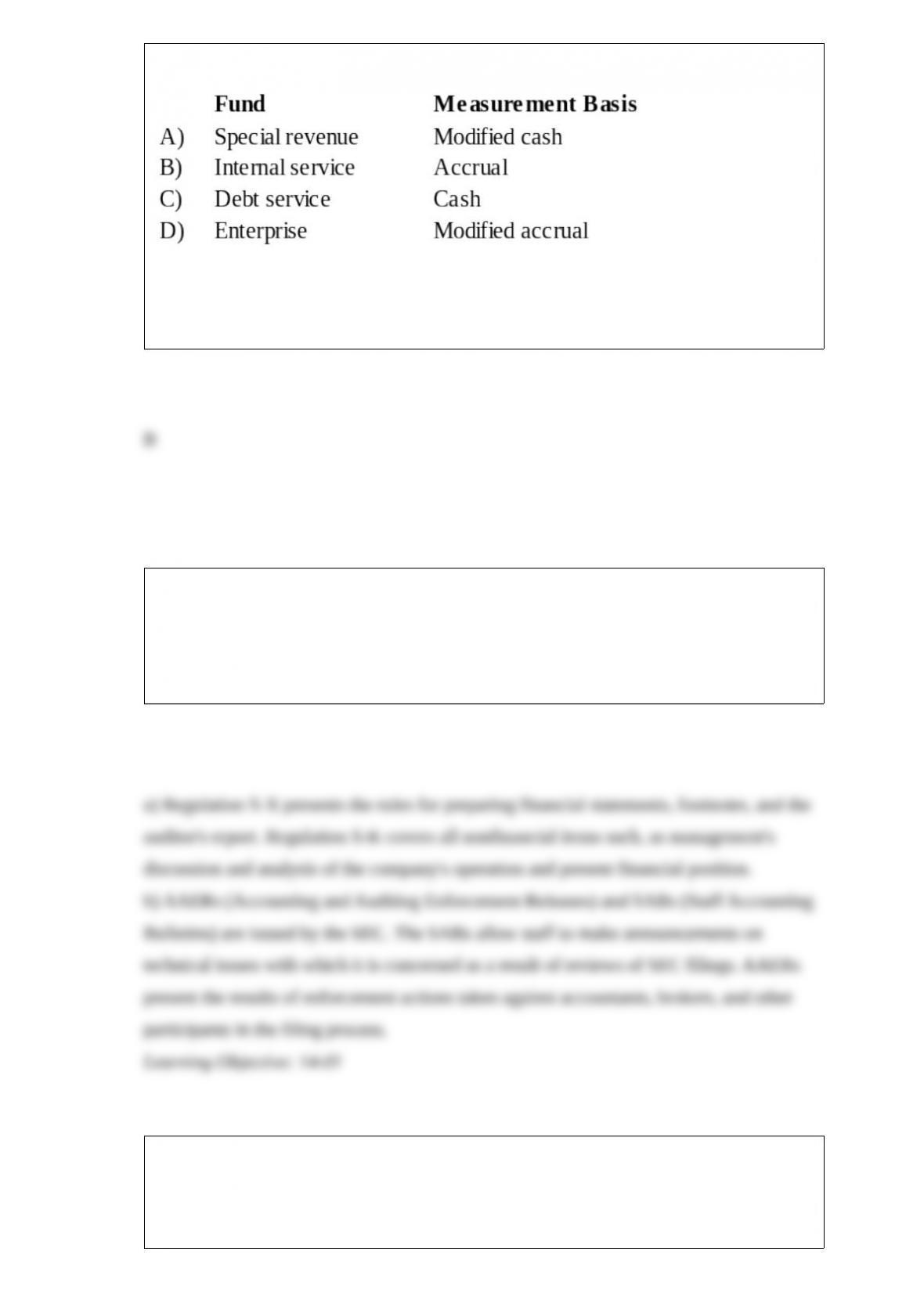

Which combination of fund and measurement basis is correct?

A. Option A

B. Option B

C. Option C

D. Option D

The SEC administers many laws and regulations governing the information made in

files reports.

Required:

a) What is the difference in issues covered by Regulation S-X and Regulation S-K?

b) How do the issues covered by these regulations differ from the AAERs and SABs?

On October 15, 20X1, Jerry Company sold inventory to Garcia Corporation, its

Mexican subsidiary. The goods cost Jerry $2,700 and were sold to Garcia for $3,500,

payable in Mexican pesos. The goods are still on hand at the end of the year on

December 31. The Mexican peso is the functional currency of Garcia. The exchange

rates follow:

October 15 1 peso = $0.07

December 31 1 peso = $0.08

Based on the preceding information, what amount of unrealized intercompany gross

profit is eliminated in preparing the consolidated financial statements for the year?

A. $0

B. $800

C. $1,000

D. $1,300

Mazeppa, Inc. is a multinational entity with its head office located in Toronto, Canada.

Its main foreign subsidiary is in Paris, France, but the primary economic environment in

which the foreign subsidiary generates and expends cash is in the United States. Based

on this information, which of the following statements is most likely true for Mazeppa,

Inc.?

A. The functional currency is the Euro.

B. The local currency is the U.S. dollar.

C. The reporting currency is the Canadian dollar.

D. The reporting currency is the U.S. dollar.

Blue Corporation holds 70 percent of Black Company’s voting common stock. On

January 1, 20X3, Black paid $500,000 to acquire a building with a 10-year expected

economic life. Black uses straight-line depreciation for all depreciable assets. On

December 31, 20X8, Blue purchased the building from Black for $180,000. Blue

reported income, excluding investment income from Black, of $140,000 and $162,000

for 20X8 and 20X9, respectively. Black reported net income of $30,000 and $45,000

for 20X8 and 20X9, respectively.

Based on the preceding information, the amount of income assigned to the controlling

shareholders in the consolidated income statement for 20X9 will be:

A. $207,000.

B. $202,000.

C. $212,000.

D. $190,000.

All of the following items are reported in a statement of realization and liquidation

except:

A. Cash

B. Prepaid assets

C. Depreciable assets (net)

D. Receiver’s expenses

Which of the following describes how a governmental fund (e.g. general fund) accounts

for a capital lease?

A. noncurrent liability

B. bond accounting

C. an asset and a lease liability

D. none of the above identifies the appropriate way to account for a capital lease.

Based on the preceding information, what is the overall effect on net income of

Robert’s use of the forward exchange contract?

A. No effect

B. Net loss of $150

C. Net loss of $200

D. Net gain of $350

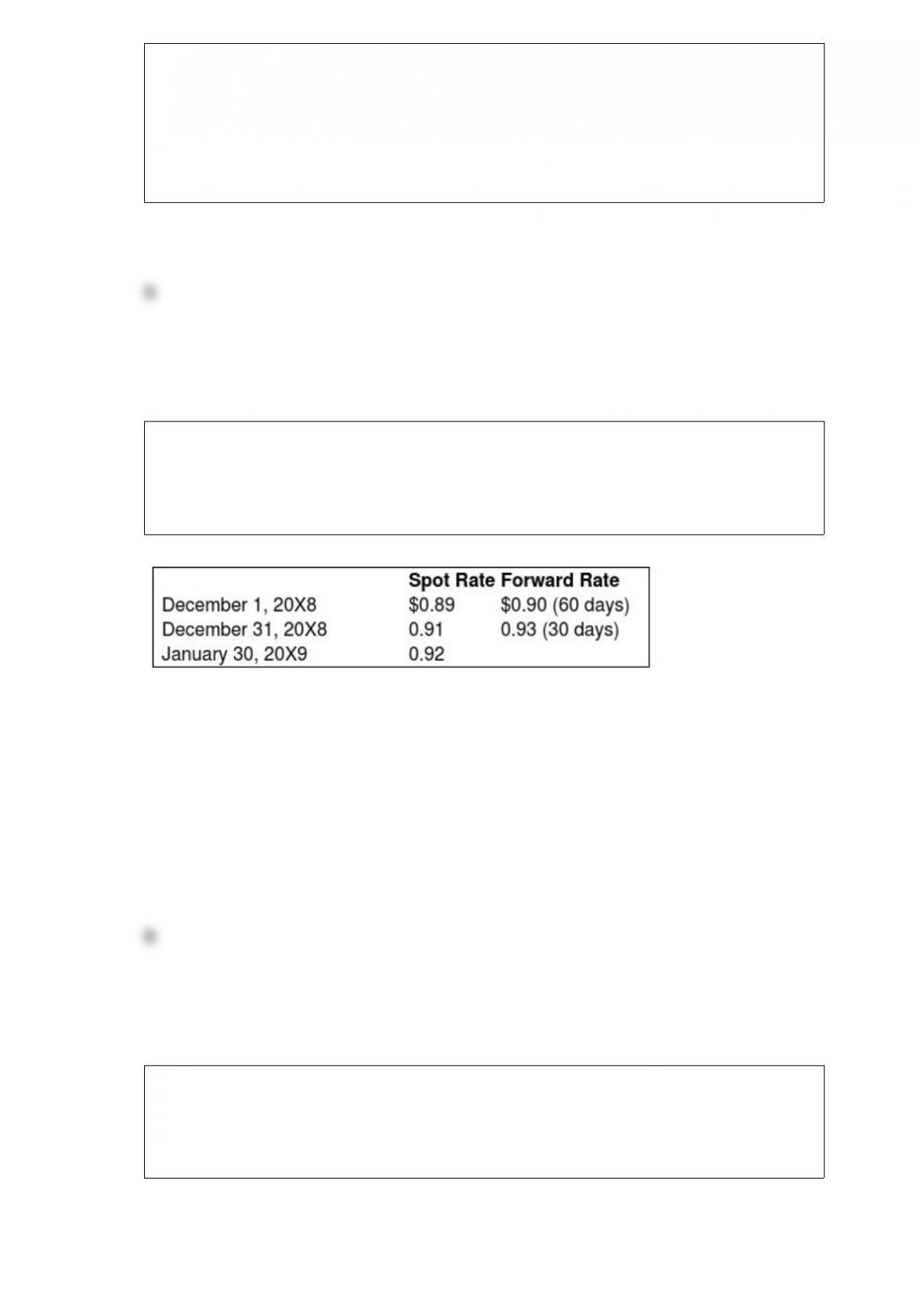

Taste Bits Inc. purchased chocolates from Switzerland for 200,000 Swiss francs (SFr)

on December 1, 20X8. Payment is due on January 30, 20X9. On December 1, 20X8, the

company also entered into a 60-day forward contract to purchase 100,000 Swiss francs.

The forward contract is not designated as a hedge. The rates were as follows:

Based on the preceding information, the entries on January 30, 20X9, include a:

A. Credit to Foreign Currency Units (SFr), $184,000.

B. Credit to Cash, $180,000.

C. Debit to Foreign Currency Transaction Loss, $4,000.

D. Debit to Dollars Payable to Exchange Broker, $184,000.

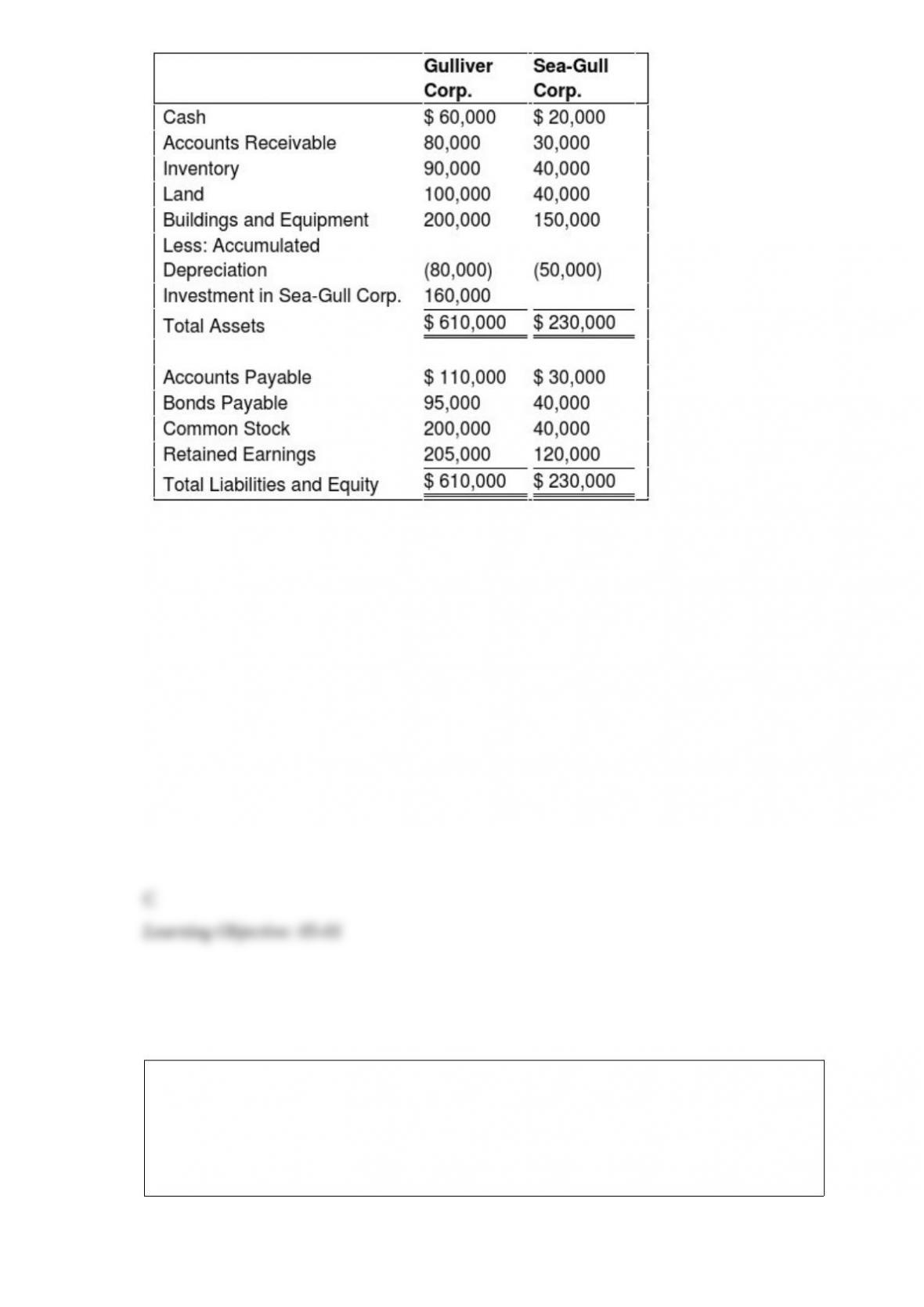

On January 1, 20X9, Gulliver Corporation acquired 80 percent of Sea-Gull Company’s

common stock for $160,000 cash. The fair value of the noncontrolling interest at that

date was determined to be $40,000. Data from the balance sheets of the two companies

included the following amounts as of the date of acquisition:

At the date of the business combination, the book values of Sea-Gull’s net assets and

liabilities approximated fair value except for inventory, which had a fair value of $45,000,

and land, which had a fair value of $60,000.

Based on the preceding information, what amount of total liabilities will be reported in the

consolidated balance sheet prepared immediately after the business combination?

A. $395,000

B. $280,000

C. $275,000

D. $195,000

On January 2, 20X1, Pencil Co. purchased 15 percent of Eraser, Inc.’s outstanding

common shares for $500,000. Pencil is the largest single shareholder in Eraser and is

able to exercise significant influence over Eraser. Eraser reported net income of

$400,000 for 20X1 and paid dividends of $100,000. In its December 31, 20X1, balance

sheet, what amount should Pencil report as investment in Eraser?

A. $485,000

B. $500,000

C. $545,000

D. $560,000

Based on the information given above, what amount of cost of goods sold must be

reported in the consolidated income statement for 20X4?

A. $1,612,000

B. $2,418,000

C. $2,790,000

D. $3,596,000

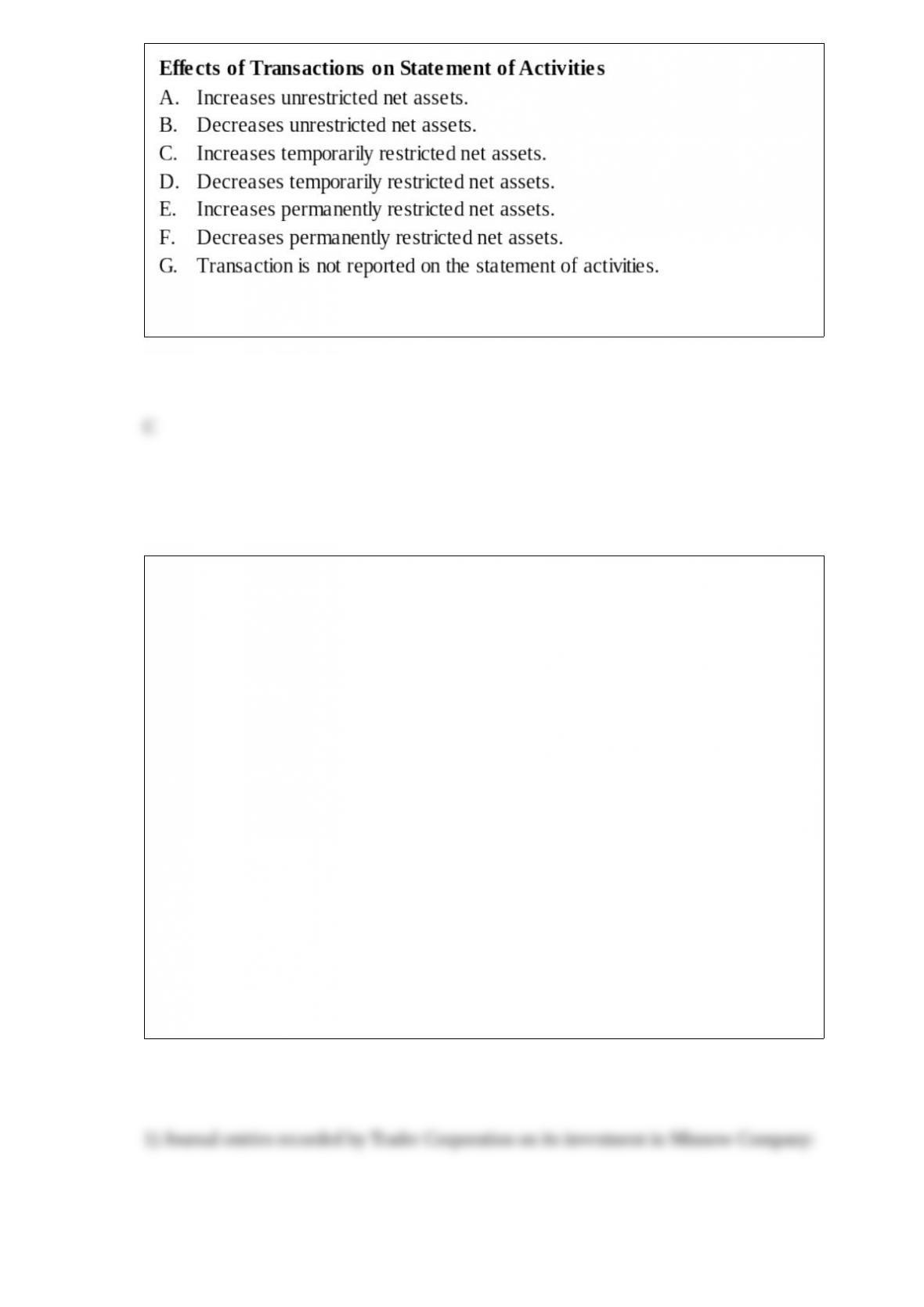

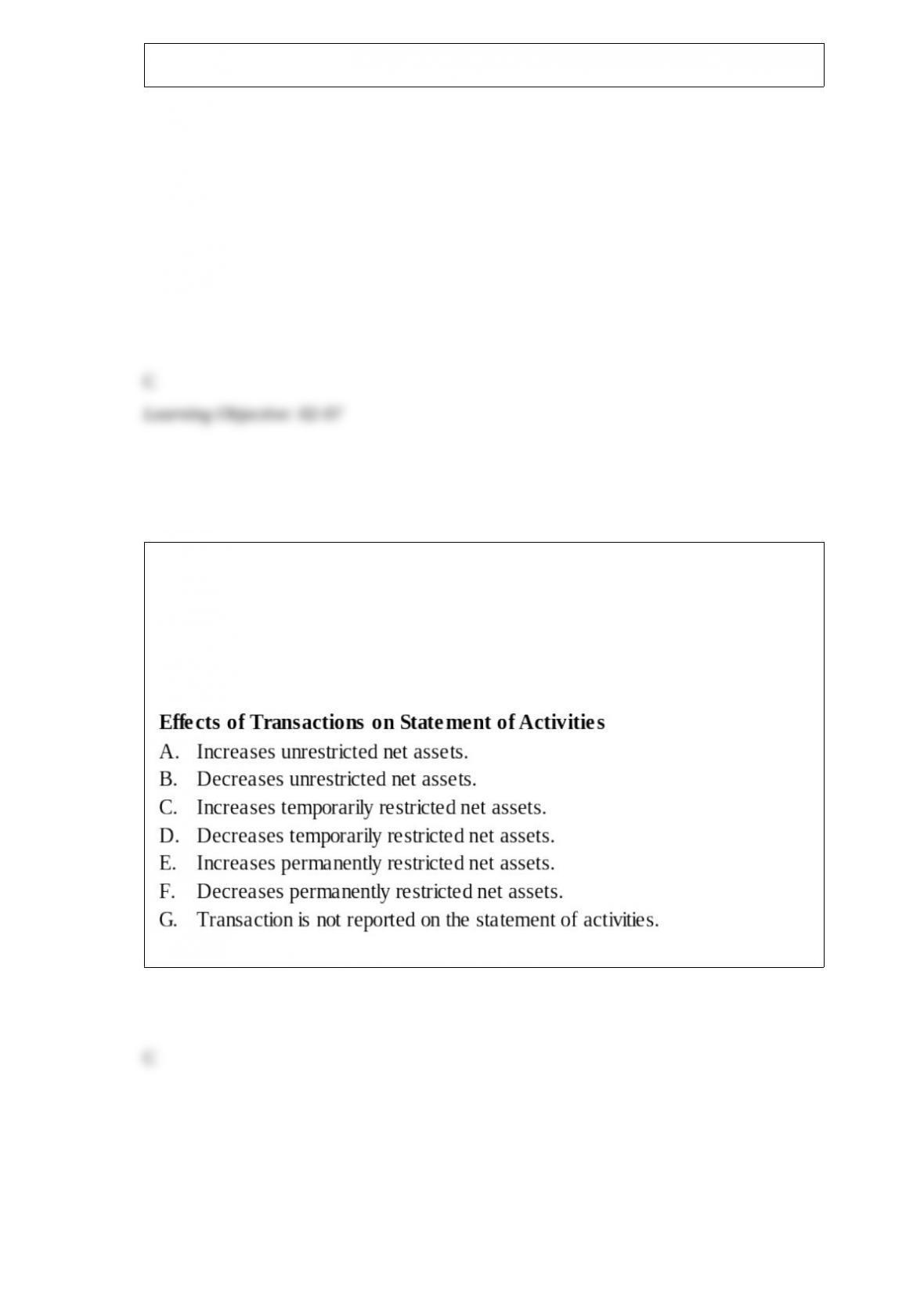

The transactions described in the following questions occurred in a voluntary health and

welfare organization during the year ended December 31, 20X8. For each transaction,

indicate its effect(s) on the organization’s statement of activities prepared for the year

ended December 31, 20X8. List all effects of transactions affecting more than one class

of net assets. Indicate your choice(s) by entering the letter corresponding to the effects

listed here:

Endowment income was earned. The donor specified that the income be used for

community service.

On January 1, 20X7, Infinity Corporation acquired 90 percent of Trader Corporation’s

common stock for $315,000. At the date of acquisition, the fair value of the

noncontrolling interest was $35,000, and Trader reported common stock outstanding of

$150,000 and retained earnings of $180,000. The differential is assigned to a patent

with a remaining life of eight years. Each year since acquisition, Trader has reported

income from operations of $50,000 and paid dividends of $30,000.

Trader acquired 75 percent ownership of Minnow Company on January 1, 20X9, for

$187,500. At that date, the fair value of the noncontrolling interest was $62,500, and

Minnow reported common stock outstanding of $100,000 and retained earnings of

$130,000. In 20X9, Minnow reported net income of $20,000 and paid dividends of

$8,000. The differential is assigned to buildings and equipment with an economic life of

10 years at the date of acquisition.

Required:

1) Prepare the journal entries recorded by Trader for its investment in Minnow during

20X9.

2) Prepare the journal entries recorded by Infinity for its investment in Trader during

20X9.

3) Prepare the consolidating entries related to Trader’s investment in Minnow and

Infinity’s investment in Trader needed to prepare consolidated financial statements for

Infinity and its subsidiaries at December 31, 20X9.

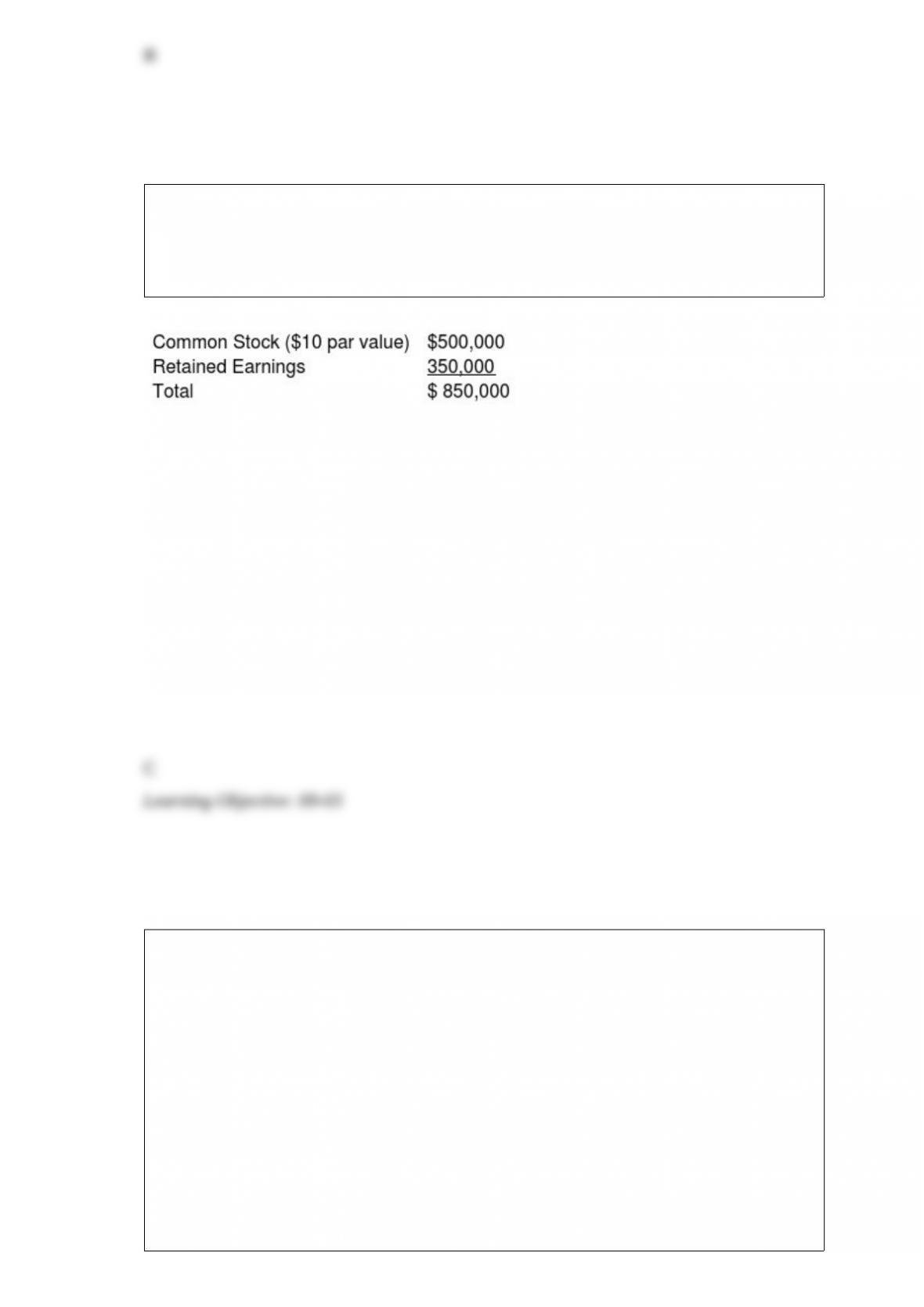

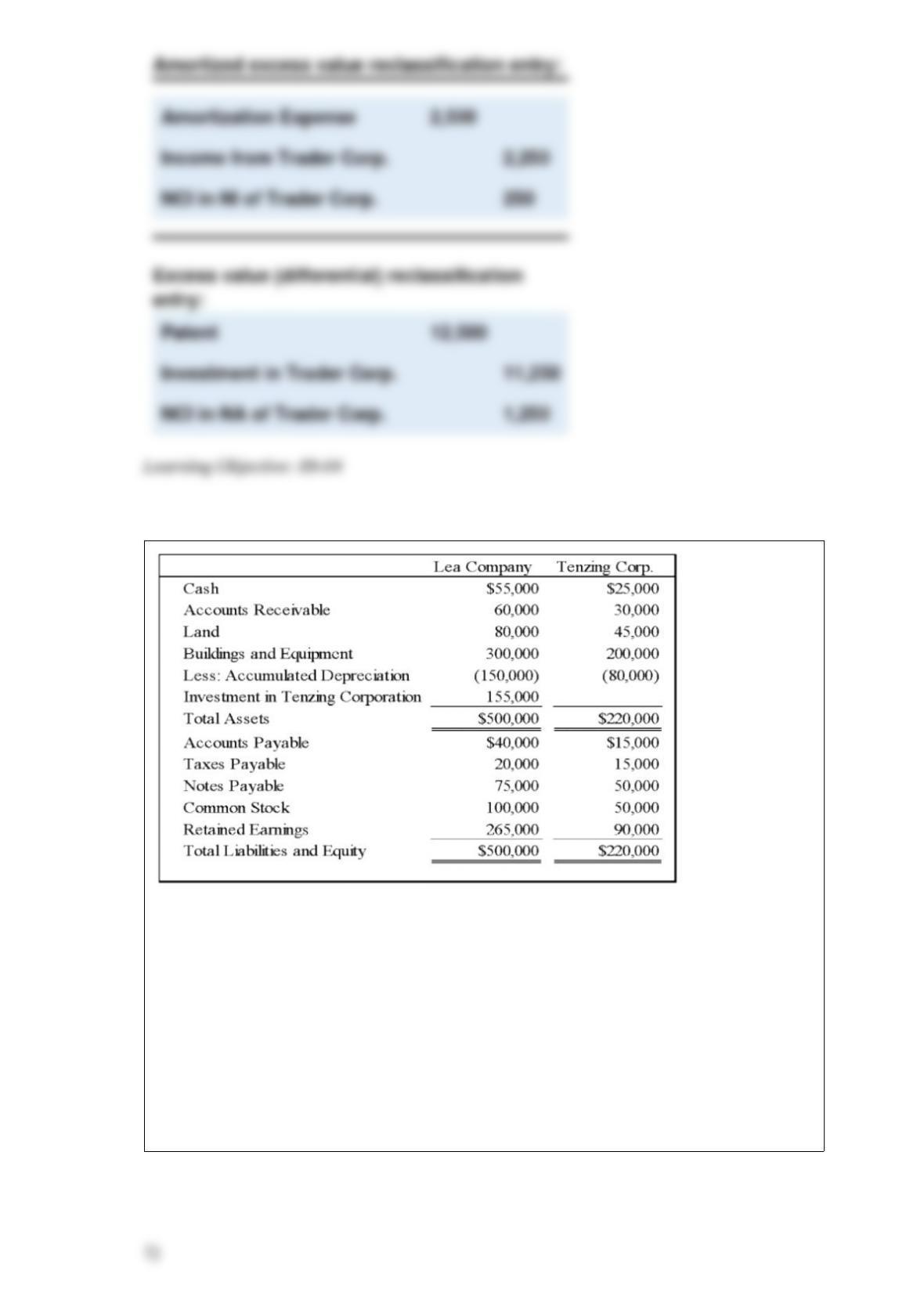

Lea Company acquired all of Tenzing Corporation’s stock on January 1, 20X6 for

$150,000 cash. On December 31, 20X7, the balance sheets of the two companies

showed the following amounts:

Tenzing Corporation reported retained earnings of $75,000 at the date of acquisition.

The difference between the acquisition price and underlying book value is assigned to

buildings and equipment with a remaining economic life of five years from the date of

acquisition.

Required:

1) Give the appropriate consolidating entry or entries needed to prepare a consolidated

balance sheet as of December 31, 20X7.

2) Prepare a consolidated balance sheet worksheet as of December 31, 20X7.

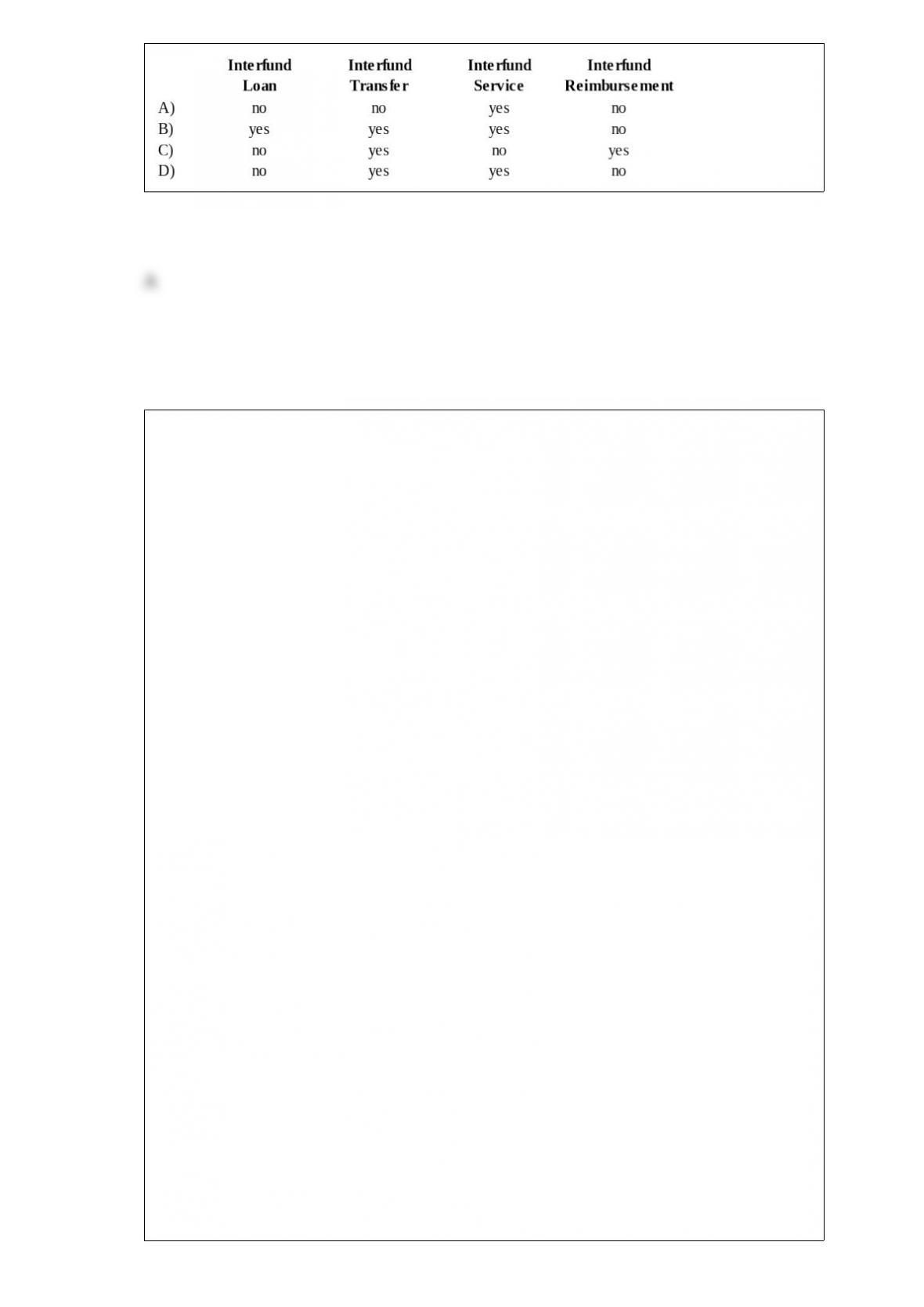

GASB 34 established four types of interfund activities. Interfund activities are

recognized as revenue in a governmental fund for an:

Newport Village was recently incorporated and began financial operations on January 1,

20X8, the beginning of its fiscal year. The following transactions occurred during this

first fiscal year, January 1, 20X8, to December 31, 20X8:

1) The village council adopted a budget for general operations for the fiscal year ending

December 31, 20X8. Revenue was estimated at $650,000. Legal authorizations for

budgeted expenditures totaled $620,000.

2) Property taxes were levied in the amount of $630,000; 3 percent of this amount was

estimated to prove uncollectible. These taxes are available as of the date of levy to

finance current expenditures.

3) During the year, a village resident donated marketable securities valued at $75,000 to

the village under the terms of a trust agreement which stipulates that the principal

amount be kept intact. The revenue generated by the securities is restricted to providing

support to the village library. Revenue earned and received on these amounted to

$3,000 through December 31, 20X8.

4) A general fund transfer of $8,000 was made to establish an internal service fund to

provide for a permanent investment in inventory.

5) The village decided to construct a small recreation facility through a special

assessment project authorized to do so at a cost of $100,000. The city is obligated if the

property owners default on their special assessments. Special assessment bonds were

issued in the amount of $90,000, and the first year’s special assessment of $22,500 was

levied against the village’s property owners. The remaining $10,000 for the project will

be contributed from the village’s general fund.

6) The special assessments for the lighting project are due over a four-year period, and

the first year’s assessments of $22,500 were collected. The $10,000 transfer from the

village’s general fund was received by the lighting capital projects fund.

7) A contract for $100,000 was let for the installation of the lighting. The capital

projects fund was encumbered for the contract. On December, 20X8, the contract was

completed and the contractor was paid.

8) During the year, the internal service fund purchased various supplies at a cost of

$3,000.

9) Current property taxes collected during the year was $615,000. Licenses and permit

fees collected amounted to $15,000. The allowance for estimated uncollectible taxes is

adjusted to $15,000.

Required:

Prepare journal entries to record each of these transactions in the appropriate fund or

funds of Newport Village for the fiscal year ended December 31, 20X8. Use the

following funds: general fund, capital projects fund, internal service fund, and

private-purpose trust fund. Closing entries are not required. Organize your answer using

the following format:

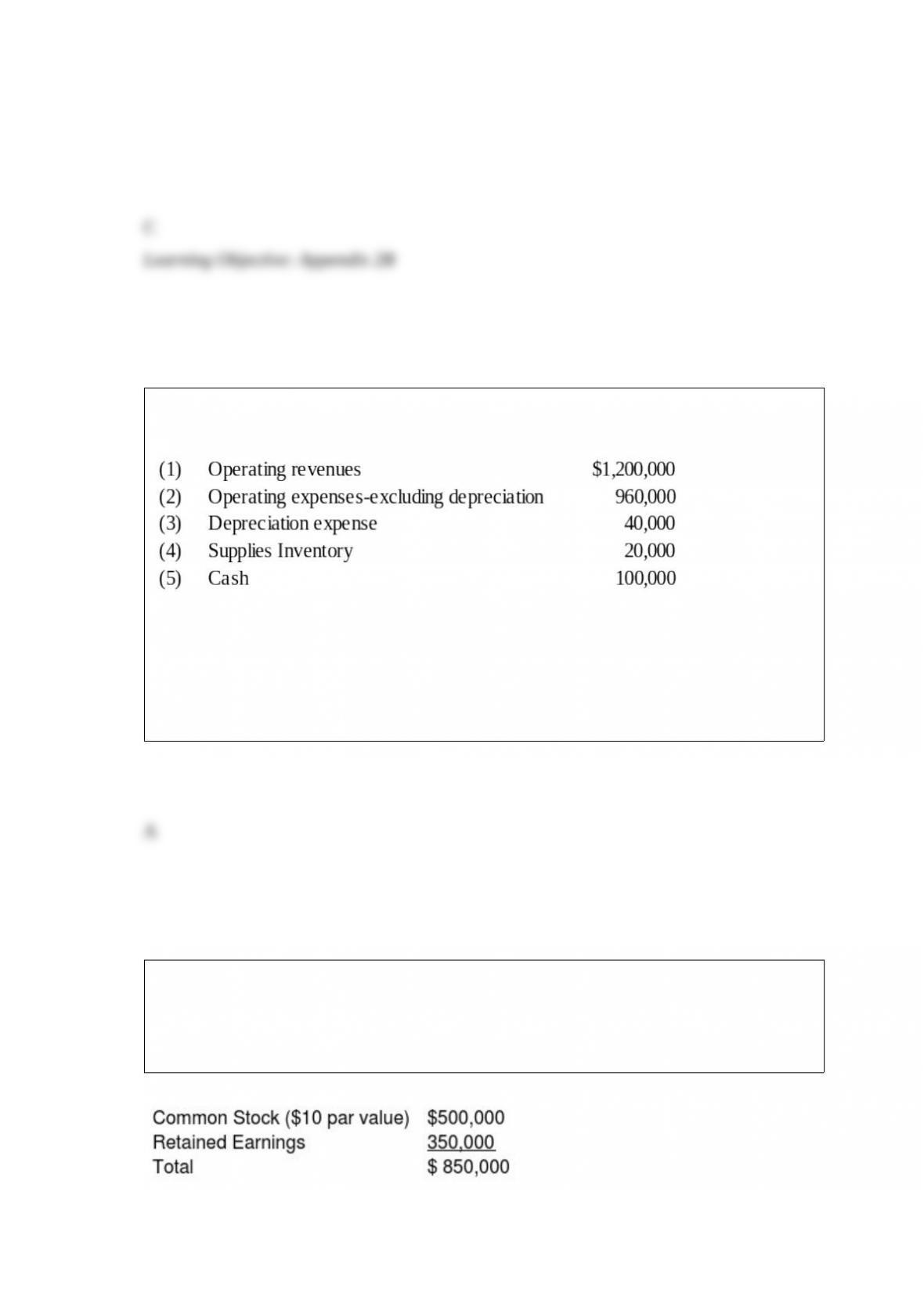

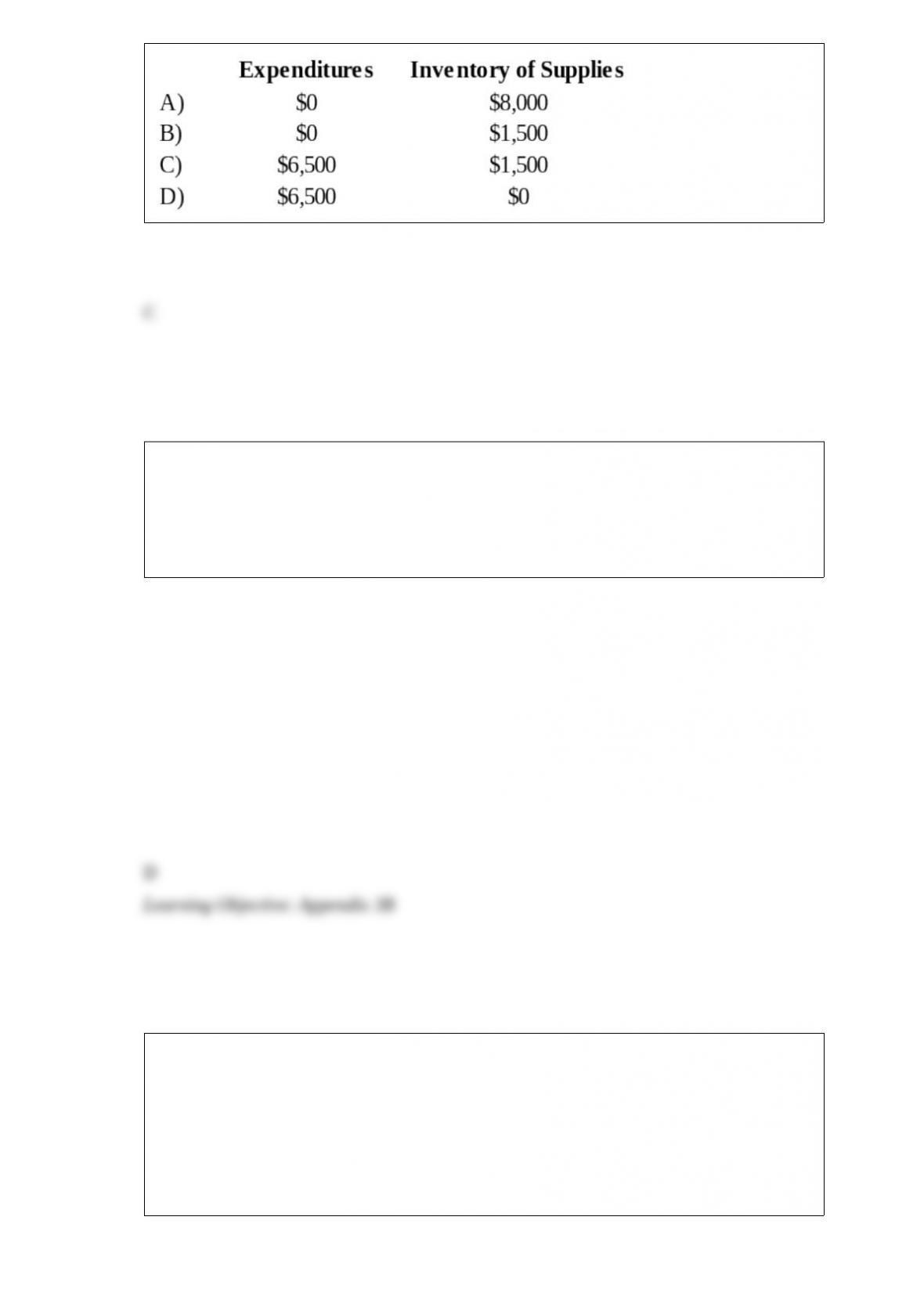

Gotham City acquires $25,000 of inventory on November 1, 20X7, having held no

inventory previously. On December 31, 20X7, the end of Gotham City’s fiscal year, a

physical count shows $8,000 still in stock. During 20X8, $6,500 of this inventory is

used, resulting in a $1,500 remaining balance of supplies on December 31, 20X8.

Based on the preceding information, which of the following would be the correct

account balances for 20X8 if Gotham City used the consumption method of accounting

for inventories?

Cosby Corporation acquired 60 percent of Huxtable Corporation’s voting common

stock. Huxtable’s buildings and equipment had a book value of $200,000 and a fair

value of $250,000 at the time of the acquisition. What will be the amount at which

Huxtable’s buildings and equipment will be reported in consolidated statements on the

acquisition date?

A. $150,000

B. $200,000

C. $230,000

D. $250,000

On January 1, 20X4, Timber Company acquired 25% of Johnson Company’s common

stock at underlying book value of $200,000. Johnson has 80,000 shares of $10 par

value, 6 percent cumulative preferred stock outstanding. No dividends are in arrears.

Johnson reported net income of $270,000 for 20X4 and paid total dividends of

$140,000. Timber uses the equity method to account for this investment.

Based on the preceding information, what amount would Timber Company receive as

dividends from Johnson for the year?

A. $23,000

B. $35,000

C. $37,500

D. $92,000

Alpha Company acquired 100 percent of the voting common shares of Gamma

Corporation by issuing bonds with a par value and fair value of $200,000. Immediately

prior to the acquisition, Alpha reported total assets of $600,000, liabilities of $370,000,

and stockholders’ equity of $230,000. At that date, Gamma reported total assets of

$500,000, liabilities of $300,000, and stockholders’ equity of $200,000. Included in

Gamma’s liabilities was an account payable to Alpha in the amount of $50,000, which

Alpha included in its accounts receivable.

Based on the preceding information, what amount of total assets did Alpha report in its

balance sheet immediately after the acquisition?

A. $1,100,000

B. $1,000,000

C. $800,000

D. $1600,000

Partners David and Goliath have decided to liquidate their business. The following

information is available:

Cash $100,000

Inventory $200,000

$300,000

Accounts Payable $80,000

David, Capital $140,000

Goliath, Capital $80,000

$300,000

David and Goliath share profits and losses in a 3:1 ratio, respectively. During the first

month of liquidation, half the inventory is sold for $70,000, and $50,000 of the

accounts payable are paid. During the second month, the rest of the inventory is sold for

$55,000, and the remaining accounts payable are paid. Cash is distributed at the end of

each month, and the liquidation is completed at the end of the second month.

Refer to the information provided above. Assume instead that the remaining inventory

was sold for $20,000 in the second month. What payments will be made to David and

Goliath at the end of the second month?

David Goliath

A. $0 $0

B. $10,000 $10,000

C. $15,000 $5,000

D. $20,000 $0

Tuttle Company discloses supplementary operating segment information for its three

reportable segments. Data for 20X3 are available as follows:

Segment A Segment B Segment C

Sales $500,000 $300,000 $200,000

Traceable operating expenses 250,000 120,000 90,000

Additional 20X3 expenses include indirect operating expenses of $100,000.

Appropriately selected common indirect operating expenses are allocated to segments

based on the ratio of each segment’s sales to total sales. The 20X3 operating profit for

Segment A was

A. $150,000

B. $180,000

C. $200,000

D. $250,000

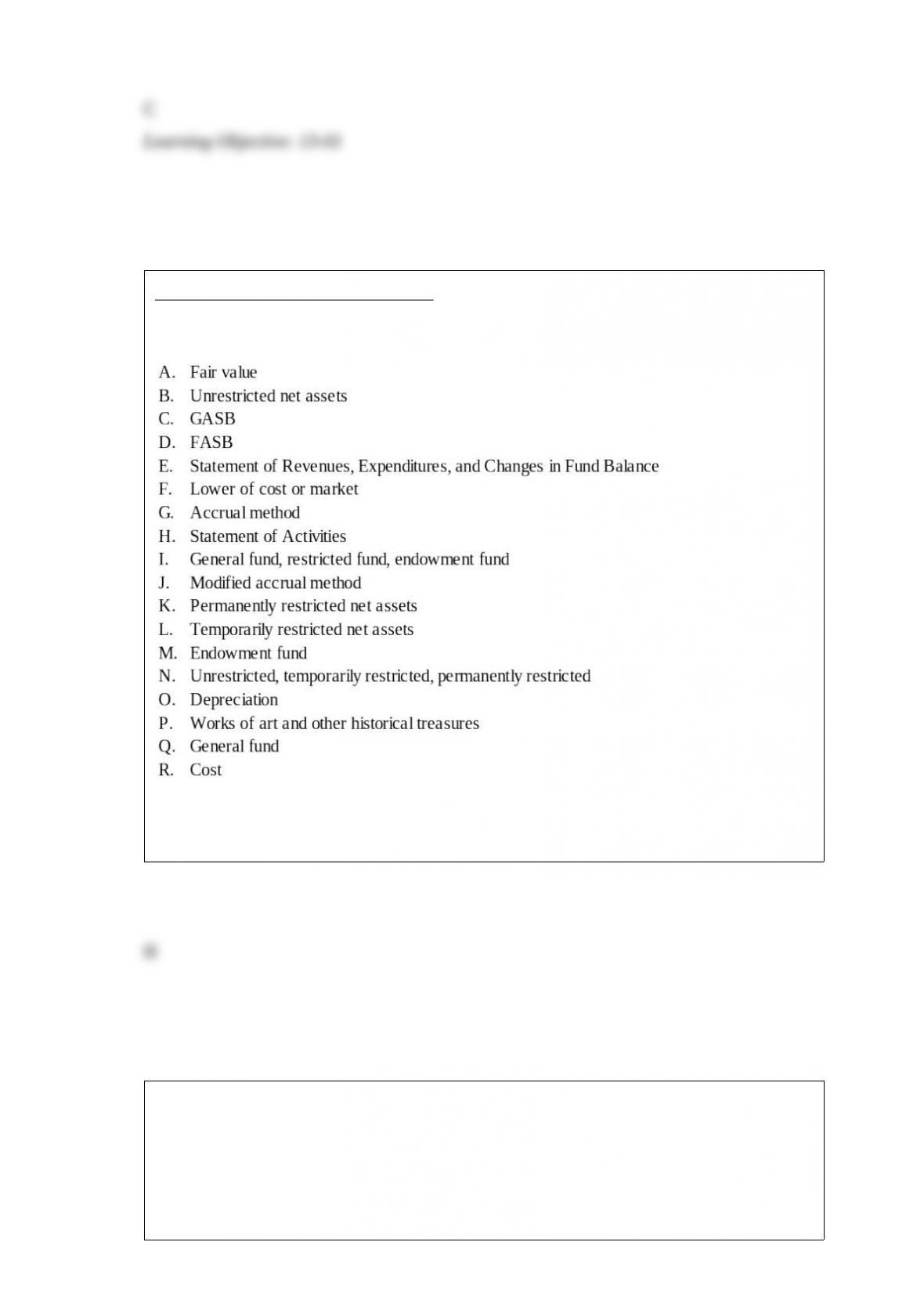

Private Not-For-Profit (NFP) Entities.

Select from this list of terms to answer the following questions.

Indicate your choice by entering the letter corresponding to the correct term. A term

may be used more than once or not at all.

”Financial statement of a private NFP entity” describes which term listed above?

Phips Co. purchases 100 percent of Sips Company on January 1, 20X2, when Phips’

retained earnings balance is $320,000 and Sips’ is $120,000. During 20X2, Sips reports

$20,000 of net income and declares $8,000 of dividends. Phips reports $125,000 of

separate operating earnings plus $20,000 of equity-method income from its 100 percent

interest in Sips; Phips declares dividends of $35,000.

Based on the preceding information, what is Sips’ post-closing retained earnings

balance on December 31, 20X2?

A. $108,000

B. $120,000

C. $132,000

D. $140,000

The transactions described in the following questions occurred in a voluntary health and

welfare organization during the year ended December 31, 20X8. For each transaction,

indicate its effect(s) on the organization’s statement of activities prepared for the year

ended December 31, 20X8. List all effects of transactions affecting more than one class

of net assets. Indicate your choice(s) by entering the letter corresponding to the effects

listed here:

Received cash contributions restricted by donors for research.