Chapter 11 – Multinational Accounting: Foreign Currency Transactions And Financial Instruments

P-11–23A (continued)

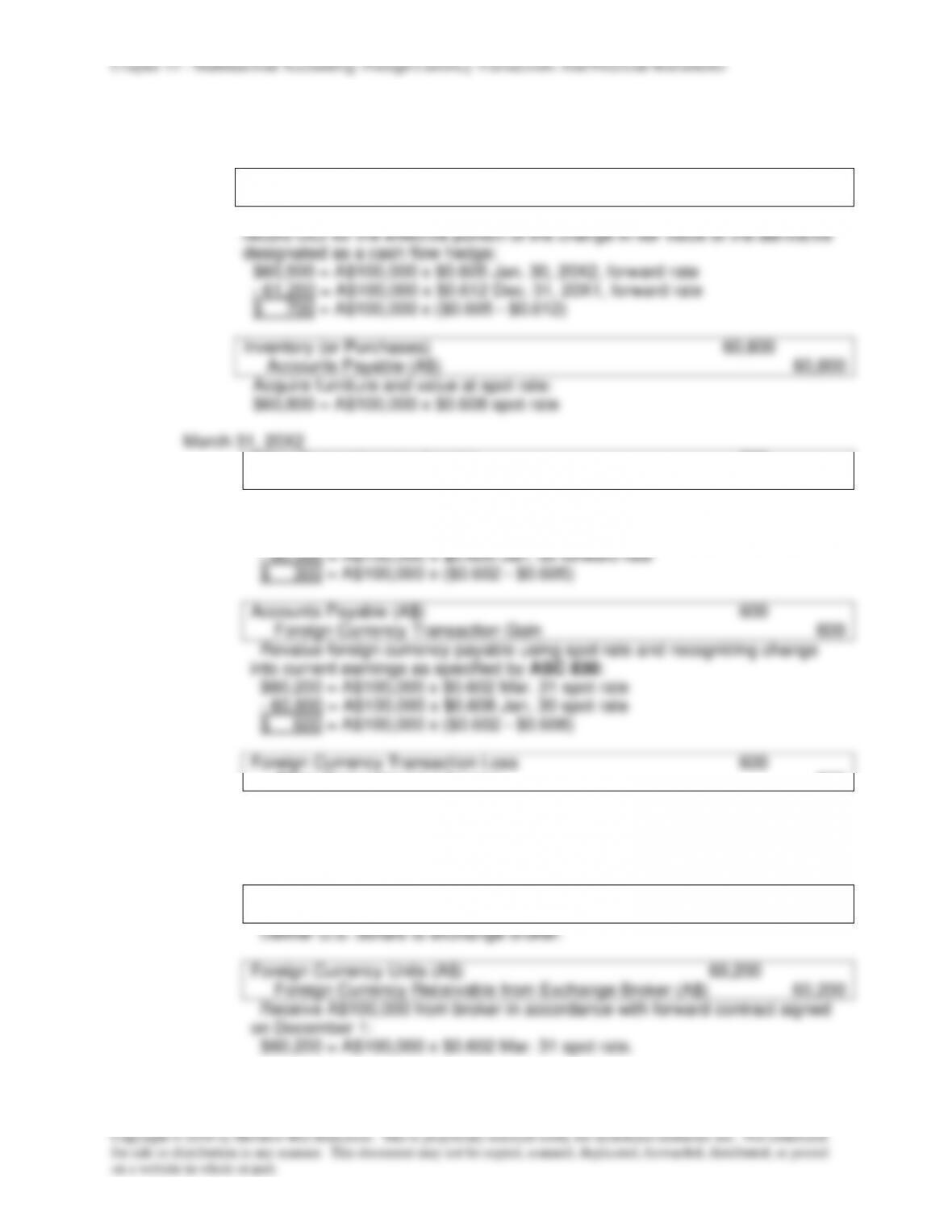

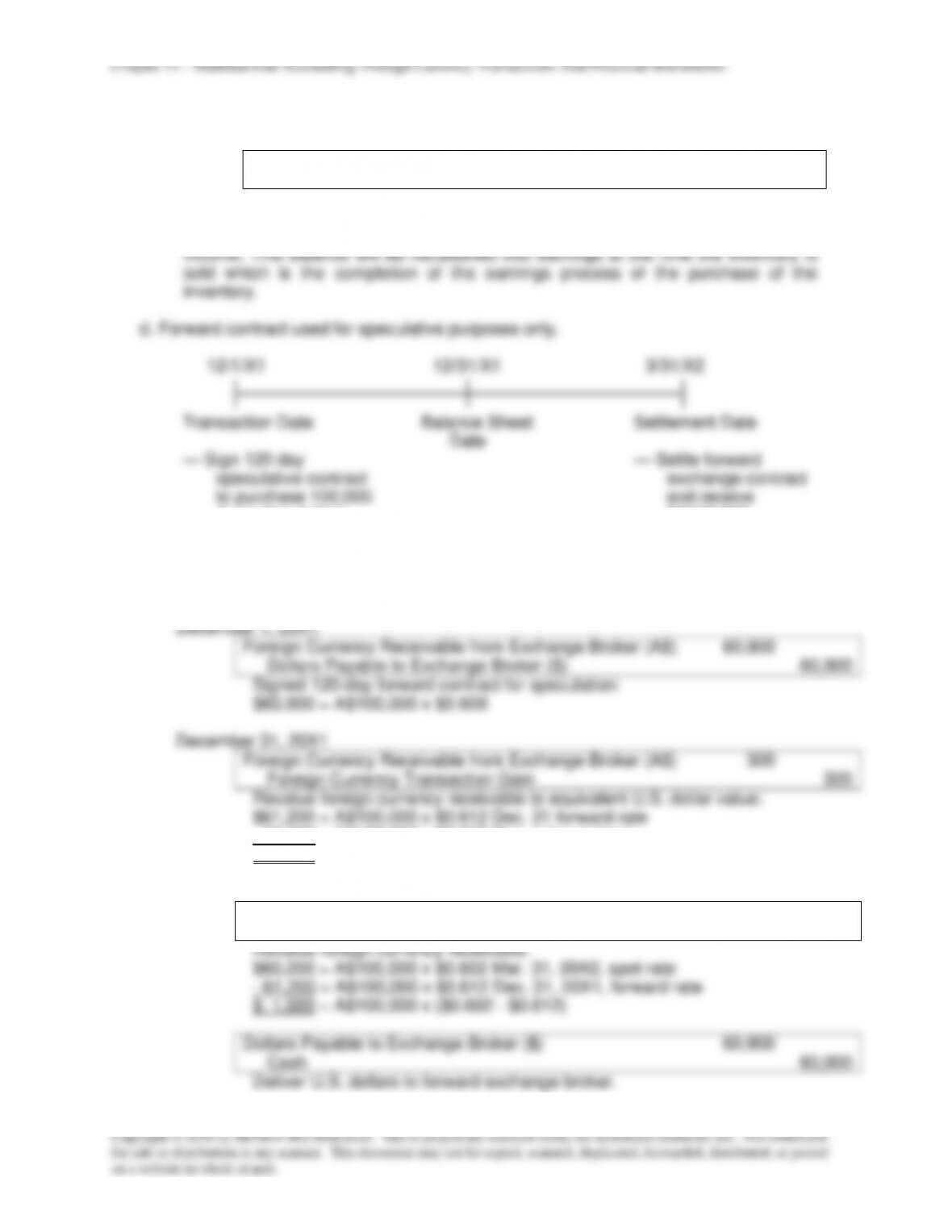

c. Use of forward contract as cash flow hedge of forecasted foreign currency transaction.

12/1/X1

12/31/X1

1/30/X2

3/31/X2

Commitment

Balance Sheet

Transaction

Settlement

Date

Date

Date

Date

— Sign foreign

— Purchase of

— Settle

exchange contract

furniture

foreign

to hedge forecasted

resulting

currency

foreign currency

in foreign

commitment

transaction.

currency

and receive

payable

A$100,000

— Pay foreign

currency

payable

Forward rate:

A$1 = $0.609

A$1 = $0.612

A$1 = $0.605

Spot rate:

A$1 = $0.600

A$1 = $0.610

A$1 = $0.608

A$1 = $0.602

December 1, 20X1

Foreign Currency Receivable from Exchange Broker (A$)

60,900

Dollars Payable to Exchange Broker ($)

60,900

Signed 120-day forward contract as a cash flow hedge of the forecasted

foreign currency transaction of the purchase of furniture on January 30 for

A$100,000:

$60,900 = A$100,000 x $0.609 forward rate

December 31, 20X1

Foreign Currency Receivable from Exchange Broker (A$)

300

Other Comprehensive Income

300

Revalue foreign currency receivable to fair value and record OCI for effective

portion of change in fair value of the derivative designated as a cash flow

hedge:

$61,200 = A$100,000 x $0.612 Dec. 31 forward rate

– 60,900 = A$100,000 x $0.609 Dec. 1 forward rate

$ 300 = A$100,000 x ($0.612 – $0.609)