Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

E5-10 Differential Assigned to Amortizable Asset

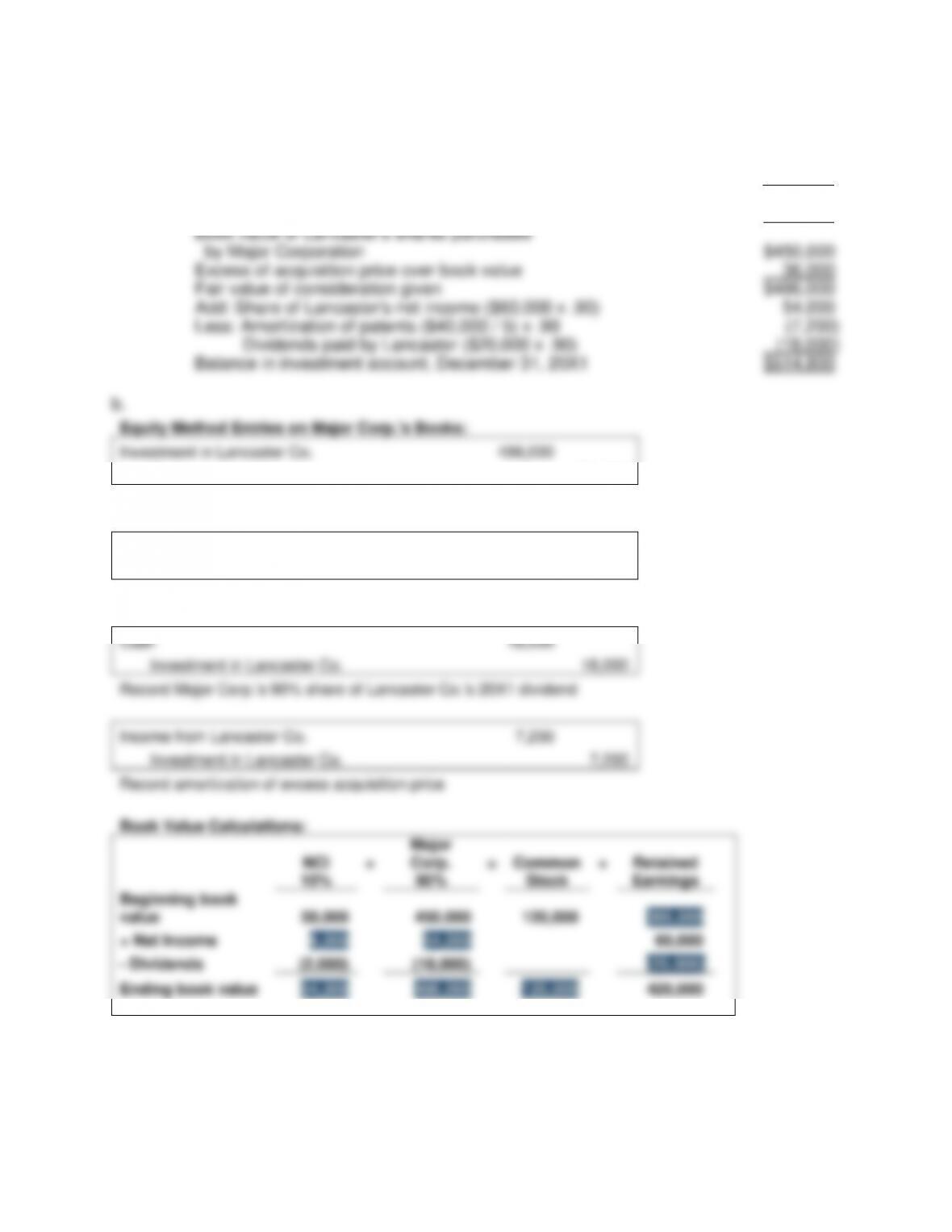

a.

Lancaster Company’s common stock, January 1, 20X1

$120,000

Lancaster Company’s retained earnings, January 1, 20X1

380,000

Book value of Lancaster’s net assets

$500,000

Proportion of stock acquired

x .90

Book value of Lancaster’s shares purchased

by Major Corporation

$450,000

Excess of acquisition price over book value

36,000

Fair value of consideration given

$486,000

Add: Share of Lancaster’s net income ($60,000 x .90)

54,000

Less: Amortization of patents ($40,000 / 5) x .90

(7,200)

Dividends paid by Lancaster ($20,000 x .90)

(18,000)

Balance in investment account, December 31, 20X1

$514,800

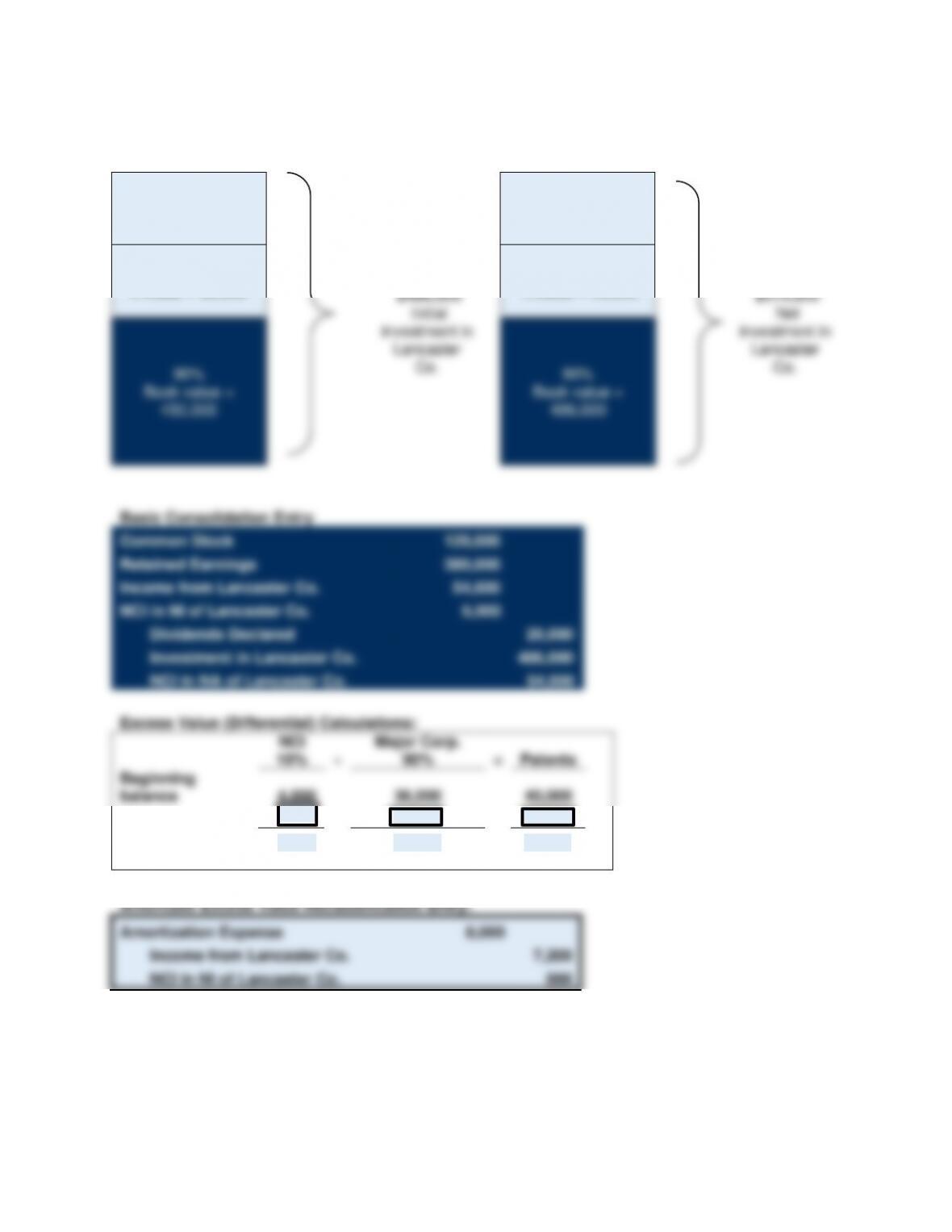

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

E5–10 (continued)

1/1/X1

Goodwill = 0

Identifiable

Excess = 36,000

$486,000

Initial

investment in

Lancaster

Co.

90%

Book value =

450,000

12/31/X1

Goodwill = 0

Identifiable

Excess = 28,800

$514,800

Net

investment in

Lancaster

Co.

90%

Book value =

486,000

Basic Consolidation Entry

Common Stock

120,000

Retained Earnings

380,000

Income from Lancaster Co.

54,000

NCI in NI of Lancaster Co.

6,000

Dividends Declared

20,000

Investment in Lancaster Co.

486,000

NCI in NA of Lancaster Co.

54,000

Excess Value (Differential) Calculations:

NCI

10%

+

Major Corp.

90%

=

Patents

Beginning

balance

4,000

36,000

40,000

Changes

(800)

(7,200)

(8,000)

Ending balance

3,200

28,800

32,000

Amortized Excess Value Reclassification Entry:

Amortization Expense

8,000

Income from Lancaster Co.

7,200

NCI in NI of Lancaster Co.

800

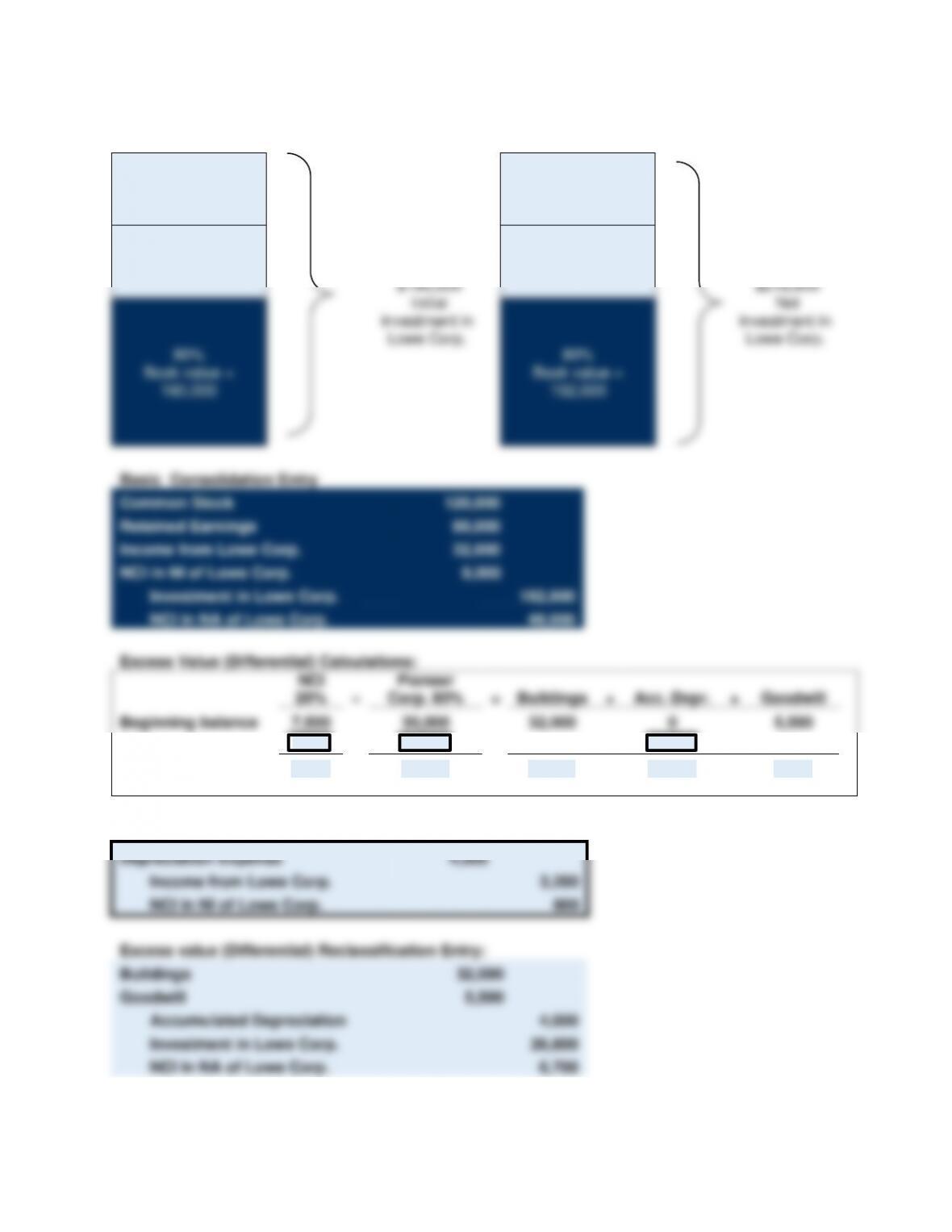

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-23

E5–10 (continued)

Excess Value (Differential) Reclassification Entry:

Patents

32,000

Investment in Lancaster Co.

28,800

NCI in NA of Lancaster Co.

3,200

Investment in

Income from

Lancaster Co.

Lancaster Co.

Acquisition

Price

486,000

90% Net Income

54,000

54,000

90% Net Income

18,000

90% Dividends

7,200

Excess Val. Amort.

7,200

Ending Balance

514,800

46,800

Ending Balance

486,000

Basic

54,000

28,800

Excess Reclass.

7,200

Amort. Reclass

0

0

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

E5-11 Consolidation after One Year of Ownership

a.

Equity Method Entries on Pioneer Corp.’s Books:

Investment in Lowe Corp.

190,000

Cash

190,000

Record the initial investment in Lowe Corp.

Book Value Calculations:

NCI

20%

+

Pioneer Corp.

80%

=

Common

Stock

+

Retained

Earnings

Book value at

acquisition

40,000

160,000

120,000

80,000

Basic Consolidation Entry

120,000

80,000

Investment in Lowe Corp.

NCI in NA of Lowe Corp.

Excess Value (Differential) Calculations:

+

=

Buildings

+

Beginning balances

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-25

E5–11 (continued)

Excess Value (Differential) Reclassification Entry:

Buildings

32,000

Goodwill

5,500

Investment in Lowe Corp.

30,000

NCI in NA of Lowe Corp.

7,500

Investment in

Lowe Corp.

Acquisition Price

190,000

160,000

Basic

30,000

Excess Reclass.

0

Equity Method Entries on Pioneer Corp.’s Books:

Investment in Lowe Corp.

32,000

Income from Lowe Corp.

32,000

Record Pioneer Corp.’s 80% share of Lowe Corp.’s 20X2 income

Income from Lowe Corp.

3,200

Investment in Lowe Corp.

3,200

Record amortization of excess acquisition price

Book Value Calculations:

NCI

20%

+

Pioneer

Corp.

80%

=

Common

Stock

+

Retained

Earnings

Beginning book

value

40,000

160,000

120,000

80,000

+ Net Income

8,000

32,000

40,000

– Dividends

0

0

0

Ending book value

48,000

192,000

120,000

120,000

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

E5–11 (continued)

1/1/X2

Goodwill = 4,400

Identifiable

Excess = 25,600

$190,000

Initial

investment in

Lowe Corp.

80%

Book value =

160,000

12/31/X2

Goodwill = 4,400

Identifiable

Excess = 22,400

$218,800

Net

investment in

Lowe Corp.

80%

Book value =

192,000

Basic Consolidation Entry

Common Stock

120,000

Retained Earnings

80,000

Income from Lowe Corp.

32,000

NCI in NI of Lowe Corp.

8,000

Investment in Lowe Corp.

192,000

NCI in NA of Lowe Corp.

48,000

Excess Value (Differential) Calculations:

NCI

20%

+

Pioneer

Corp. 80%

=

Buildings

+

Acc. Depr.

+

Goodwill

Beginning balance

7,500

30,000

32,000

0

5,500

Changes

(800)

(3,200)

(4,000)

0

Ending balance

6,700

26,800

32,000

(4,000)

5,500

Amortized Excess Value Reclassification Entry:

Depreciation Expense

4,000

Income from Lowe Corp.

3,200

NCI in NI of Lowe Corp.

800

Excess value (Differential) Reclassification Entry:

Buildings

32,000

Goodwill

5,500

Accumulated Depreciation

4,000

Investment in Lowe Corp.

26,800

NCI in NA of Lowe Corp.

6,700

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

E5-11 (continued)

Investment in

Income from

Lowe Corp.

Lowe Corp.

Acquisition Price

190,000

80% Net Income

32,000

32,000

80% Net Income

3,200

Excess Val. Amort.

3,200

Ending Balance

218,800

28,800

Ending Balance

192,000

Basic

32,000

26,800

Excess Reclass.

3,200

Amort. Reclass

0

0

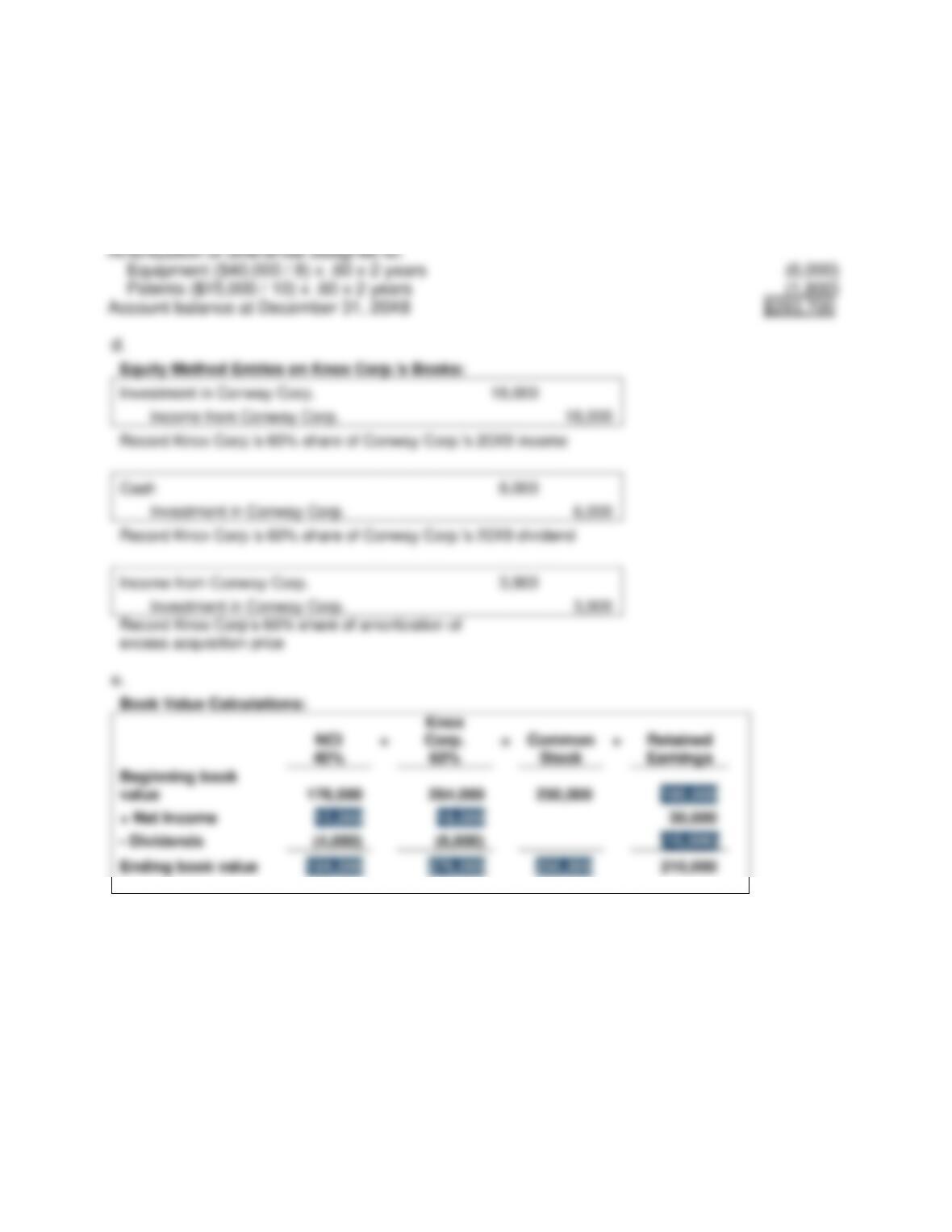

E5-12 Consolidation Following Three Years of Ownership

a.

Computation of increase in value of patents:

Fair value of consideration given by Knox

$277,500

Fair value of noncontrolling interest

185,000

Total fair value

$462,500

Book value of Conway stock

(400,000)

Excess of fair value over book value

$ 62,500

Increase in value of land ($30,000 – $22,500)

(7,500)

Increase in value of equipment ($360,000 – $320,000)

(40,000)

Increase In value of patents

$ 15,000

b.

Equity Method Entries on Knox Corp.’s Books:

Investment in Conway Corp.

277,500

Cash

277,500

Record the initial investment in Conway Corp.

Book Value Calculations:

acquisition

250,000

150,000

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

1/1/X7

Goodwill = 0

Identifiable

Excess = 37,500

$277,500

Net

investment in

Conway

Corp.

60%

Book value =

240,000

+

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

E5-12 (continued)

c. Computation of investment account balance at December 31, 20X8:

Fair value of consideration given

$277,500

Undistributed income since acquisition

($100,000 – $60,000) x .60

24,000

Amortization of differential assigned to:

Equipment ($40,000 / 8) x .60 x 2 years

(6,000)

Patents ($15,000 / 10) x .60 x 2 years

(1,800)

Account balance at December 31, 20X8

$293,700

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

E5-12 (continued)

1/1/X7

Goodwill = 0

Identifiable

Excess = 29,700

$293,700

Initial

investment in

Conway

Corp.

60%

Book value =

264,000

12/31/X7

Goodwill = 0

Identifiable

Excess = 25,800

$301,800

Net

investment in

Conway

Corp.

60%

Book value =

276,000

+