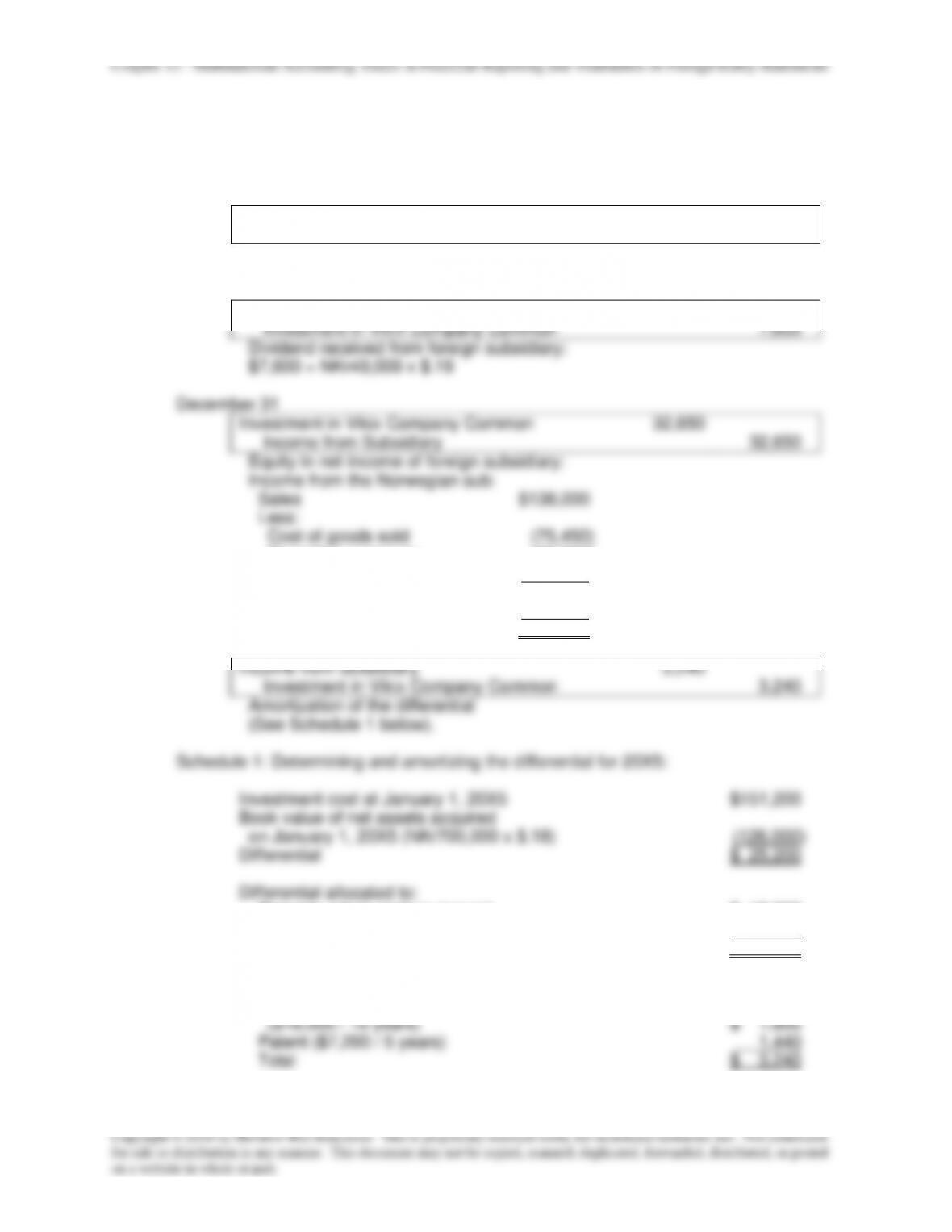

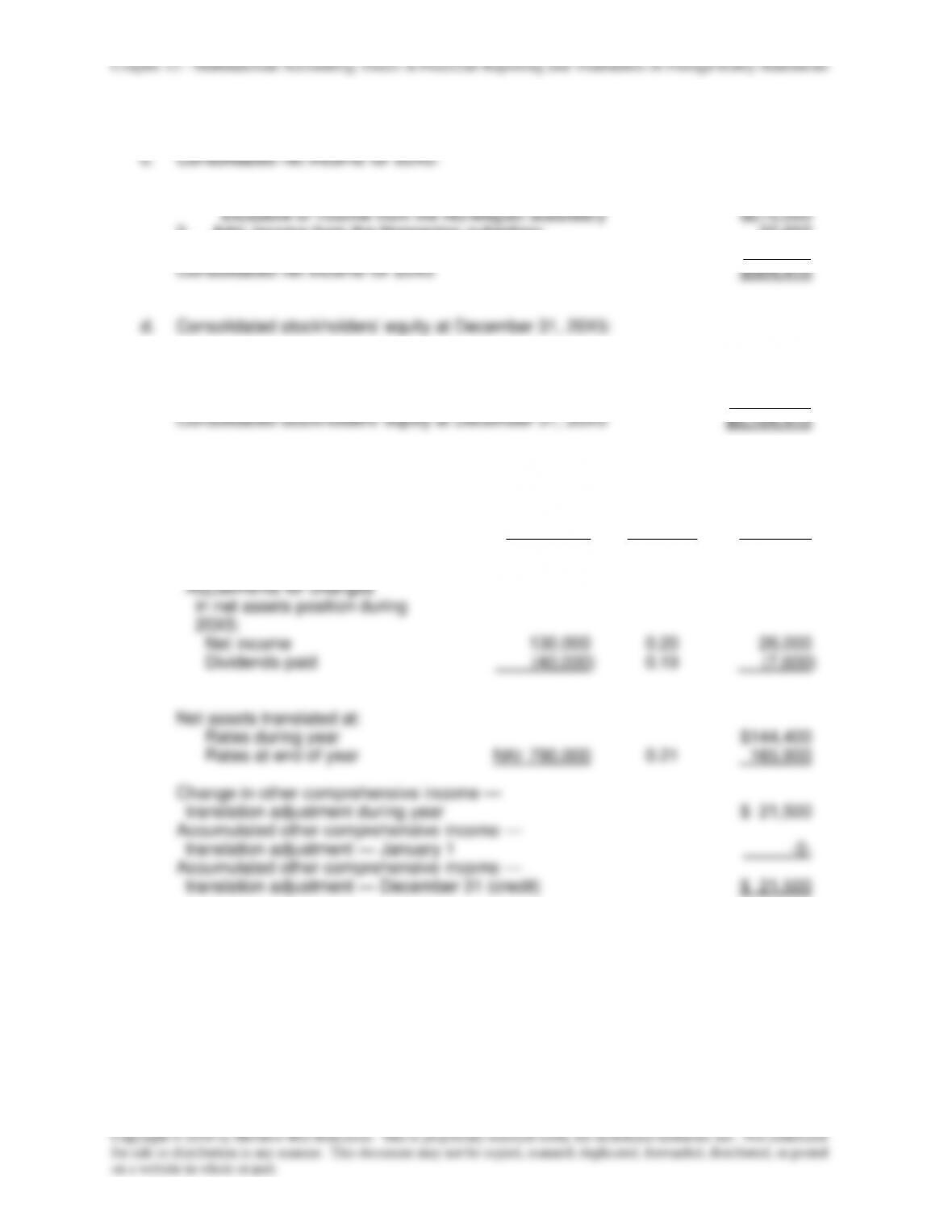

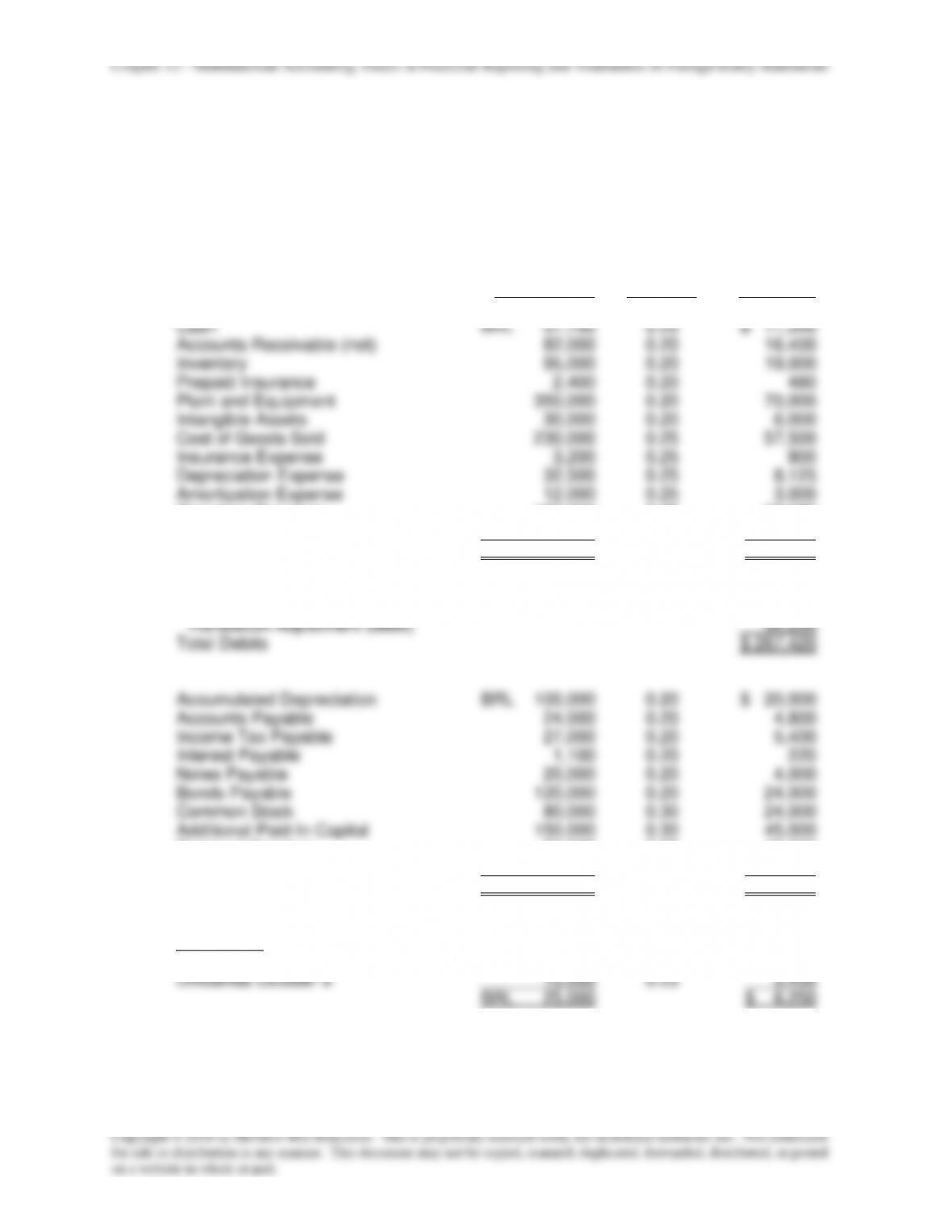

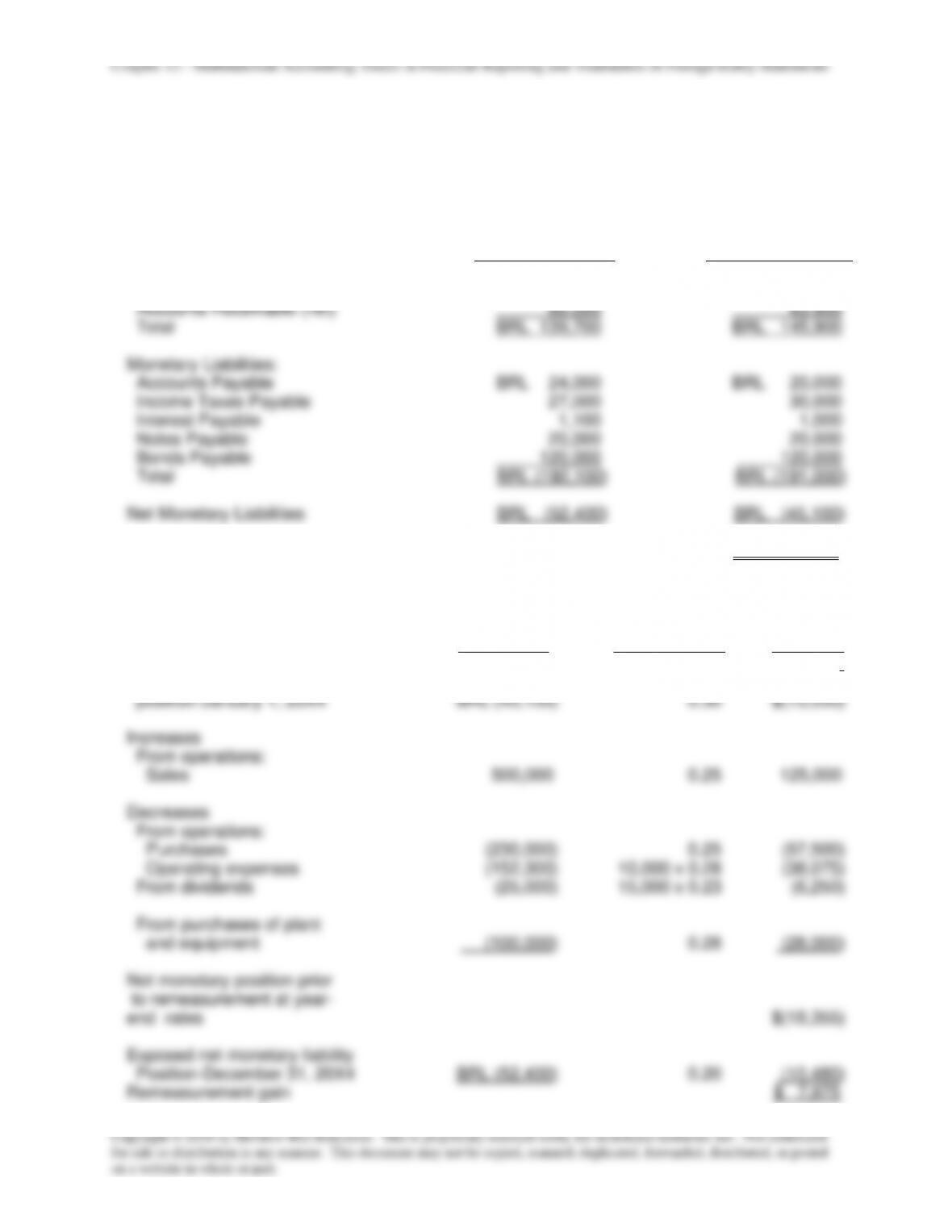

Chapter 12 – Multinational Accounting: Issues in Financial Reporting and Translation of Foreign Entity Statements

P12-17 (continued)

c.

Taft’s consolidated comprehensive income for 20X5:

1.

Income from Taft’s operations for 20X5, exclusive

of income from the Norwegian subsidiary

$ 275,000

2.

Add: Income from the Norwegian subsidiary for 20X5

26,000

3.

Deduct: Amortization of differential for 20X5

(3,600)

Taft’s Net Income

$ 297,400

4.

Add: Translation Adjustment ($21,500 + $4,020)

25,520

Taft’s Consolidated Comprehensive Income

$ 322,920

d.

Taft’s consolidated stockholders’ equity at December 31, 20X5:

1.

Taft’s stockholders’ equity at Jan. 1, 20X5

$3,500,000

2.

Add: Net income for 20X5

297,400

3.

Deduct: Dividends declared by Taft during 20X5

(100,000)

4.

Add: Accumulated other comprehensive income:

Foreign currency translation adjustment

25,520

Consolidated Stockholders’ Equity at Dec. 31, 20X5

$3,722,920