Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 05 - Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-51

P5-29 (continued)

Excess Value (Differential) Reclassification Entry:

Inventory

6,000

Buildings & Equipment

15,000

Investment in Darla Corp.

14,700

NCI in NA of Darla Corp.

6,300

Eliminate Intercompany Accounts:

Accounts Payable

12,500

Accounts Receivable

12,500

Optional Accumulated Depreciation Consolidation Entry

Accumulated Depreciation

80,000

Building & Equipment

80,000

Investment in

Darla Corp.

Acquisition Price

102,200

87,500

Basic

14,700

Excess Reclass.

0

Chapter 05 - Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-52

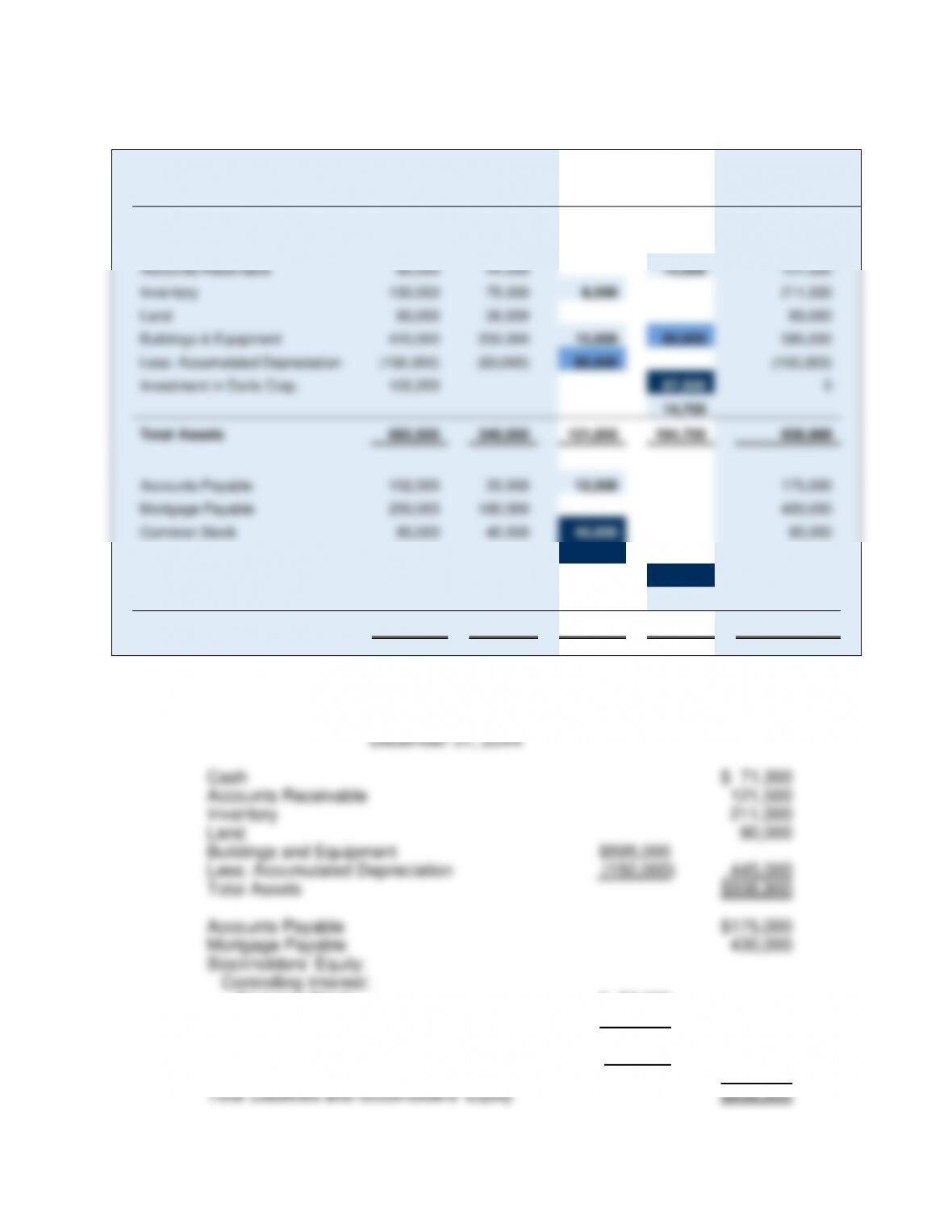

P5-29 (continued)

Porter

Corp.

Darla

Corp.

Consolidation

Entries

DR

CR

Consolidated

Balance Sheet

Cash

50,300

21,000

71,300

Accounts Receivable

90,000

44,000

12,500

121,500

Inventory

130,000

75,000

6,000

211,000

Land

60,000

30,000

90,000

Buildings & Equipment

410,000

250,000

15,000

80,000

595,000

Less: Accumulated Depreciation

(150,000)

(80,000)

80,000

(150,000)

Investment in Darla Corp.

102,200

87,500

0

14,700

Total Assets

692,500

340,000

101,000

194,700

938,800

Accounts Payable

152,500

35,000

12,500

175,000

Mortgage Payable

250,000

180,000

430,000

Common Stock

80,000

40,000

40,000

80,000

Retained Earnings

210,000

85,000

85,000

210,000

NCI in NA of Darla Corp.

37,500

43,800

6,300

Total Liabilities & Equity

692,500

340,000

137,500

43,800

938,800

c.

Porter Corporation and Subsidiary

Consolidated Balance Sheet

December 31, 20X4

Cash

$ 71,300

Accounts Receivable

121,500

Inventory

211,000

Land

90,000

Buildings and Equipment

$595,000

Less: Accumulated Depreciation

(150,000)

445,000

Total Assets

$938,800

Accounts Payable

$175,000

Mortgage Payable

430,000

Stockholders’ Equity:

Controlling Interest:

Common Stock

$ 80,000

Retained Earnings

210,000

Total Controlling Interest

$290,000

Noncontrolling Interest

43,800

Total Stockholders’ Equity

333,800

Total Liabilities and Stockholders' Equity

$938,800

Chapter 05 - Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

P5-30 Balance Sheet Consolidation of Majority-Owned Subsidiary

a.

Equity Method Entries on Total Corp.'s Books:

Investment in Ticken Tie Co.

510,000

Bonds Payable

500,000

Bond Premium

10,000

Record the initial investment in Ticken Tie Co.

Book Value Calculations:

NCI

25%

+

Total

Corp.

75%

=

Common

Stock

+

Add. Paid-

in Capital

+

Retained

Earnings

Book value at

acquisition

119,500

358,500

200,000

130,000

148,000

Chapter 05 - Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-54

P5-30 (continued)

Excess Value (Differential) Calculations:

NCI

25%

+

Total

Corp.

75%

=

Inven-

tory

+

Land

+

Building &

Equipment

+

Patent

+

Goodwill

Beg.

balances

50,500

151,500

4,000

20,000

50,000

40,000

88,000

Excess Value (Differential) Reclassification Entry:

Inventory

4,000

Land

20,000

Building & Equipment

50,000

Patent

40,000

Goodwill

88,000

Investment in Ticken Tie Co.

151,500

NCI in NA of Ticken Tie Co.

50,500

Eliminate Intercompany Accounts:

Current Payables

6,500

Receivables

6,500

Optional Accumulated Depreciation Consolidation Entry

Accumulated Depreciation

220,000

Building & Equipment

220,000

Investment in

Ticken Tie Co.

Acquisition Price

510,000

358,500

Basic

151,500

Excess Reclass.

0

Chapter 05 - Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

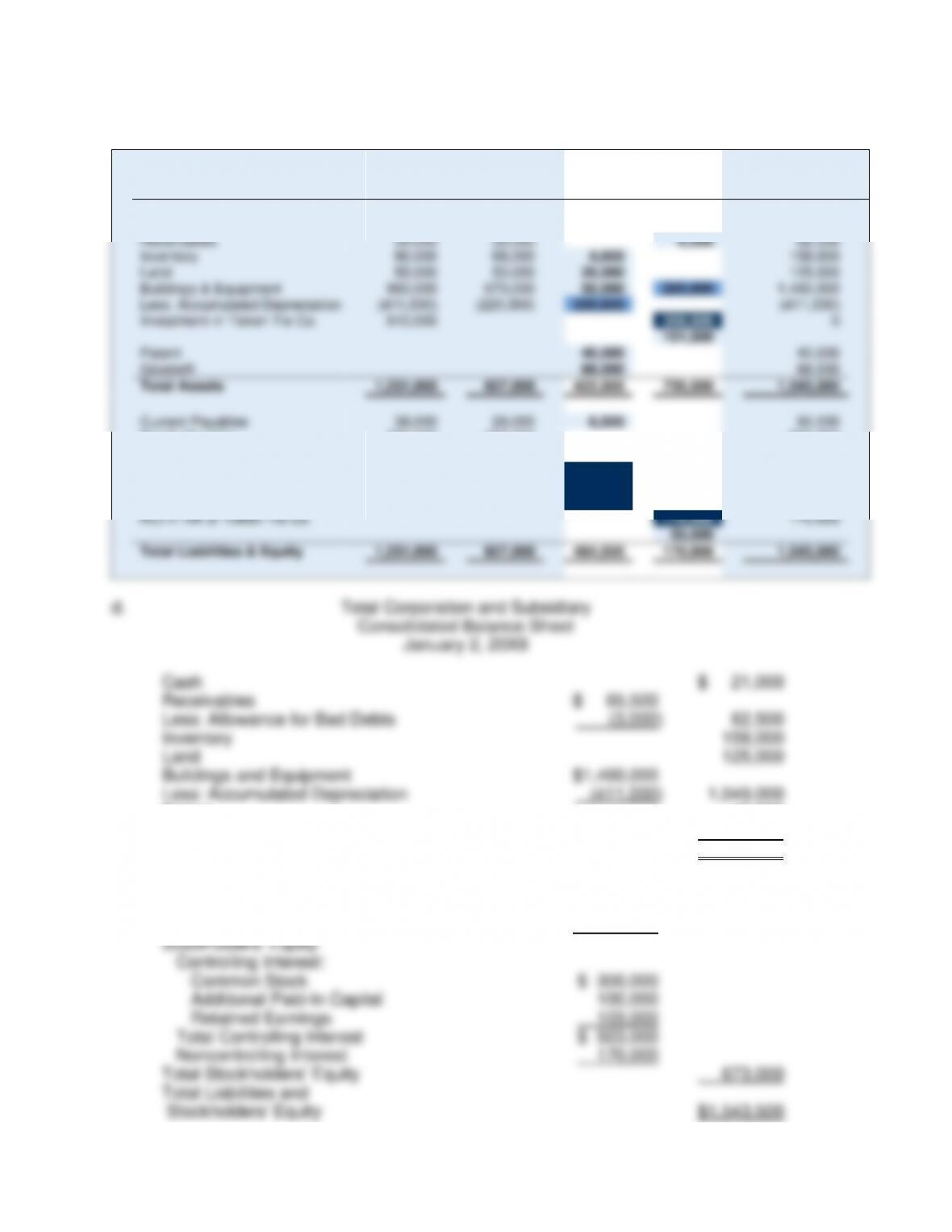

P5-30 (continued)

c.

Total

Corp.

Ticken

Tie Co.

Consolidation

Entries

DR

CR

Consolidated

Balance Sheet

Cash

12,000

9,000

21,000

Receivables

39,000

30,000

6,500

62,500

Inventory

86,000

68,000

4,000

158,000

Land

55,000

50,000

20,000

125,000

Buildings & Equipment

960,000

670,000

50,000

220,000

1,460,000

Less: Accumulated Depreciation

(411,000)

(220,000)

220,000

(411,000)

Investment in Ticken Tie Co.

510,000

358,500

0

151,500

Patent

40,000

40,000

Goodwill

88,000

88,000

Total Assets

1,251,000

607,000

422,000

736,500

1,543,500

Current Payables

38,000

29,000

6,500

60,500

Bonds Payable

700,000

100,000

800,000

Bond Premium

10,000

10,000

Common Stock

300,000

200,000

200,000

300,000

Additional Paid-in Capital

100,000

130,000

130,000

100,000

Retained Earnings

103,000

148,000

148,000

103,000

NCI in NA of Ticken Tie Co.

119,500

170,000

50,500

Total Liabilities & Equity

1,251,000

607,000

484,500

170,000

1,543,500

Chapter 05 - Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-56

P5-31 Incomplete Data

a.

$15,000

=

($115,000 + $46,000) - $146,000

b.

$65,000

=

($148,000 - $98,000) + $15,000

c.

Skyler: $24,000

=

$380,000 - ($46,000 + $110,000

+ $75,000 + $125,000)

Blue: $70,000

=

$94,000 - $24,000

d.

Fair value of Skyler

as a whole:

$200,000

Book value of Skyler shares

10,000

Differential assigned to inventory

($195,000 - $105,000 - $80,000)

40,000

Differential assigned to buildings and equipment

($780,000 - $400,000 - $340,000)

9,000

Differential assigned to goodwill

$259,000

Fair value of Skyler

e.

65 percent = 1.00 – ($90,650 / $259,000)

f.

Capital Stock = $120,000

Retained Earnings = $115,000

.

Chapter 05 - Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-57

P5-32 Income and Retained Earnings

a.

Net income for 20X9:

Quill

North

Operating income

$ 90,000

$35,000

Income from subsidiary

24,500

Net income

$114,500

$35,000

Quill

North

Retained earnings, January 1, 20X9

$290,000

$40,000

Net income for 20X9

114,500

35,000

Dividends paid in 20X9

(30,000)

(10,000)

Retained earnings, December 31, 20X9

$374,500

$65,000

Chapter 05 - Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

P5-33 Consolidation Worksheet at End of First Year of Ownership

a.

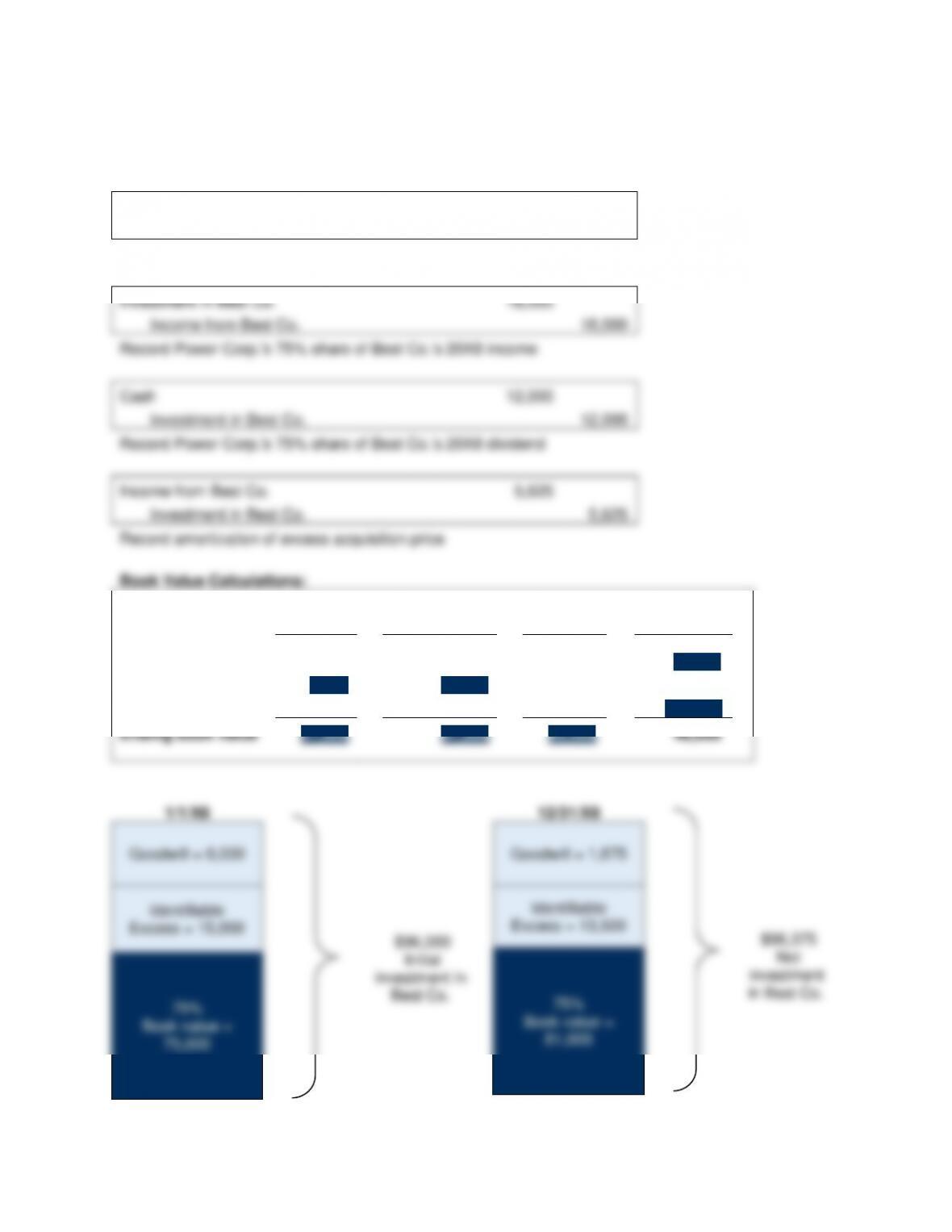

Equity Method Entries on Power Corp.'s Books:

Investment in Best Co.

96,000

Cash

96,000

Record the initial investment in Best Co.

Investment in Best Co.

18,000

Income from Best Co.

18,000

Record Power Corp.'s 75% share of Best Co.'s 20X8 income

Cash

12,000

Investment in Best Co.

12,000

Record Power Corp.'s 75% share of Best Co.'s 20X8 dividend

Income from Best Co.

5,625

Investment in Best Co.

5,625

Record amortization of excess acquisition price

Book Value Calculations:

NCI

25%

+

Power Corp.

75%

=

Common

Stock

+

Retained

Earnings

Beginning book

value

25,000

75,000

60,000

40,000

+ Net Income

6,000

18,000

24,000

- Dividends

(4,000)

(12,000)

(16,000)

Ending book value

27,000

81,000

60,000

48,000

Chapter 05 - Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-59

P5-33 (continued)

Basic Consolidation Entry

Common Stock

60,000

Retained Earnings

40,000

Income from Best Co.

18,000

NCI in NI of Best Co.

6,000

Dividends Declared

16,000

Investment in Best Co.

81,000

NCI in NA of Best Co.

27,000

Excess Value (Differential) Calculations:

NCI

25%

+

Power Corp.

75%

=

Buildings &

Equipment

+

Acc.

Depr.

+

Goodwill

Beginning balance

7,000

21,000

20,000

0

8,000

Changes

(1,875)

(5,625)

(2,000)

(5,500)

Ending balance

5,125

15,375

20,000

(2,000)

2,500

Amortized Excess Value Reclassification Entry:

Depreciation Expense

2,000

Goodwill Impairment Loss

5,500

Income from Best Co.

5,625

NCI in NI of Best Co.

1,875

Excess Value (Differential) Reclassification Entry:

Buildings & Equipment

20,000

Goodwill

2,500

Acc. Depr.

2,000

Investment in Best Co.

15,375

NCI in NA of Best Co.

5,125

Optional Accumulated Depreciation Consolidation Entry

Accumulated Depreciation

30,000

Building & Equipment

30,000

Investment in

Income from

Best Co.

Best Co.

Acquisition Price

96,000

75% Net Income

18,000

18,000

75% Net Income

12,000

75% Dividends

5,625

Excess Val. Amort.

5,625

Ending Balance

96,375

12,375

Ending Balance

81,000

Basic

18,000

15,375

Excess Reclass.

5,625

Amort. Reclass

0

0

Chapter 05 - Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-60

P5-33 (continued)

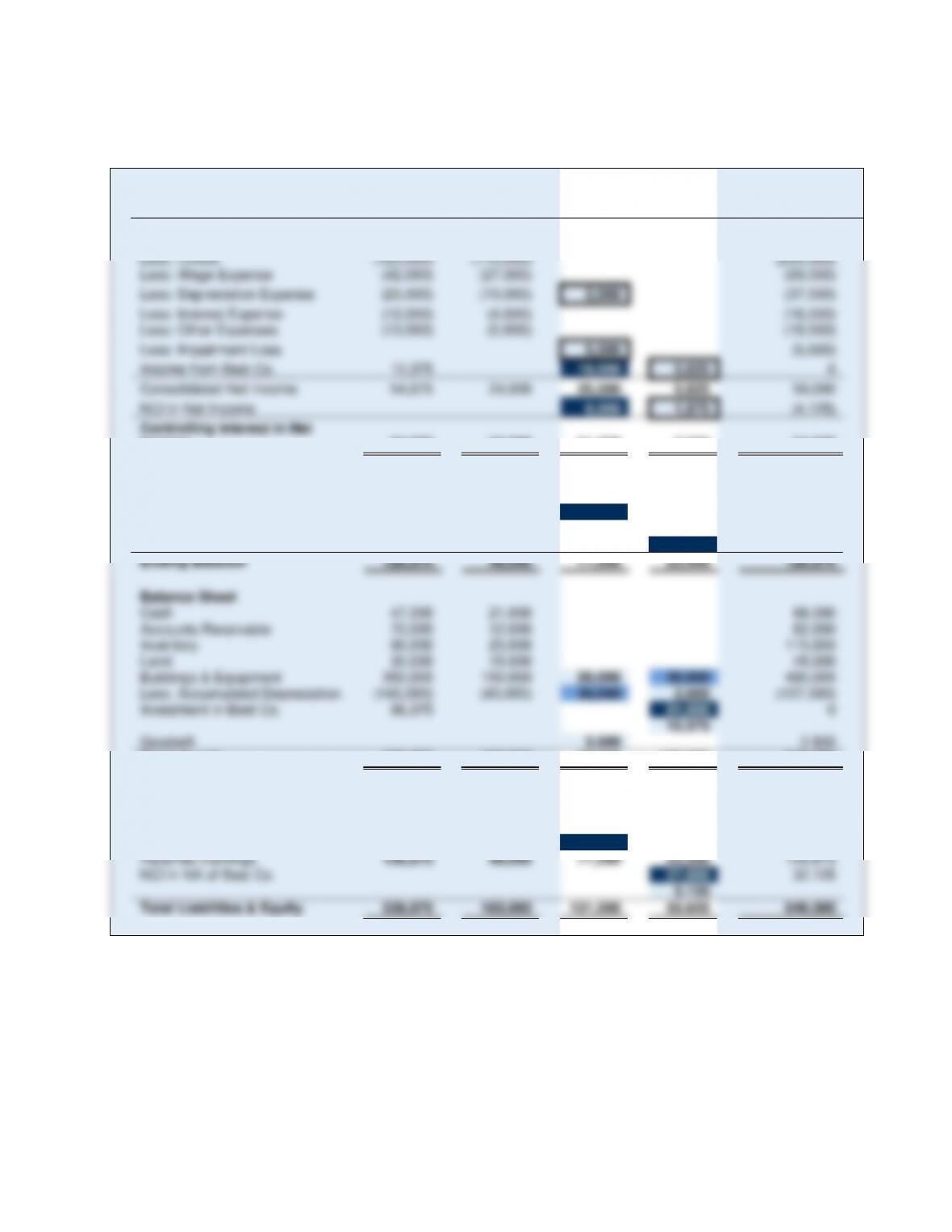

b.

Power

Corp.

Best Co.

Consolidation

Entries

DR

CR

Consolidated

Income Statement

Sales

260,000

180,000

440,000

Less: COGS

(125,000)

(110,000)

(235,000)

Less: Wage Expense

(42,000)

(27,000)

(69,000)

Less: Depreciation Expense

(25,000)

(10,000)

2,000

(37,000)

Less: Interest Expense

(12,000)

(4,000)

(16,000)

Less: Other Expenses

(13,500)

(5,000)

(18,500)

Less: Impairment Loss

5,500

(5,500)

Income from Best Co.

12,375

18,000

5,625

0

Consolidated Net Income

54,875

24,000

25,500

5,625

59,000

NCI in Net Income

6,000

1,875

(4,125)

Controlling Interest in Net

Income

54,875

24,000

31,500

7,500

54,875

Statement of Retained

Earnings

Beginning Balance

102,000

40,000

40,000

102,000

Net Income

54,875

24,000

31,500

7,500

54,875

Less: Dividends Declared

(30,000)

(16,000)

16,000

(30,000)

Ending Balance

126,875

48,000

71,500

23,500

126,875

Balance Sheet

Cash

47,500

21,000

68,500

Accounts Receivable

70,000

12,000

82,000

Inventory

90,000

25,000

115,000

Land

30,000

15,000

45,000

Buildings & Equipment

350,000

150,000

20,000

30,000

490,000

Less: Accumulated Depreciation

(145,000)

(40,000)

30,000

2,000

(157,000)

Investment in Best Co.

96,375

81,000

0

15,375

Goodwill

2,500

2,500

Total Assets

538,875

183,000

52,500

128,375

646,000

Accounts Payable

45,000

16,000

61,000

Wages Payable

17,000

9,000

26,000

Notes Payable

150,000

50,000

200,000

Common Stock

200,000

60,000

60,000

200,000

Retained Earnings

126,875

48,000

71,500

23,500

126,875

NCI in NA of Best Co.

27,000

32,125

5,125

Total Liabilities & Equity

538,875

183,000

131,500

55,625

646,000