In accounting for governmental funds, which of the following items could appear only

on government-wide financial statements?

A. I only

B. I and II

C. I and III

D. I, II, III

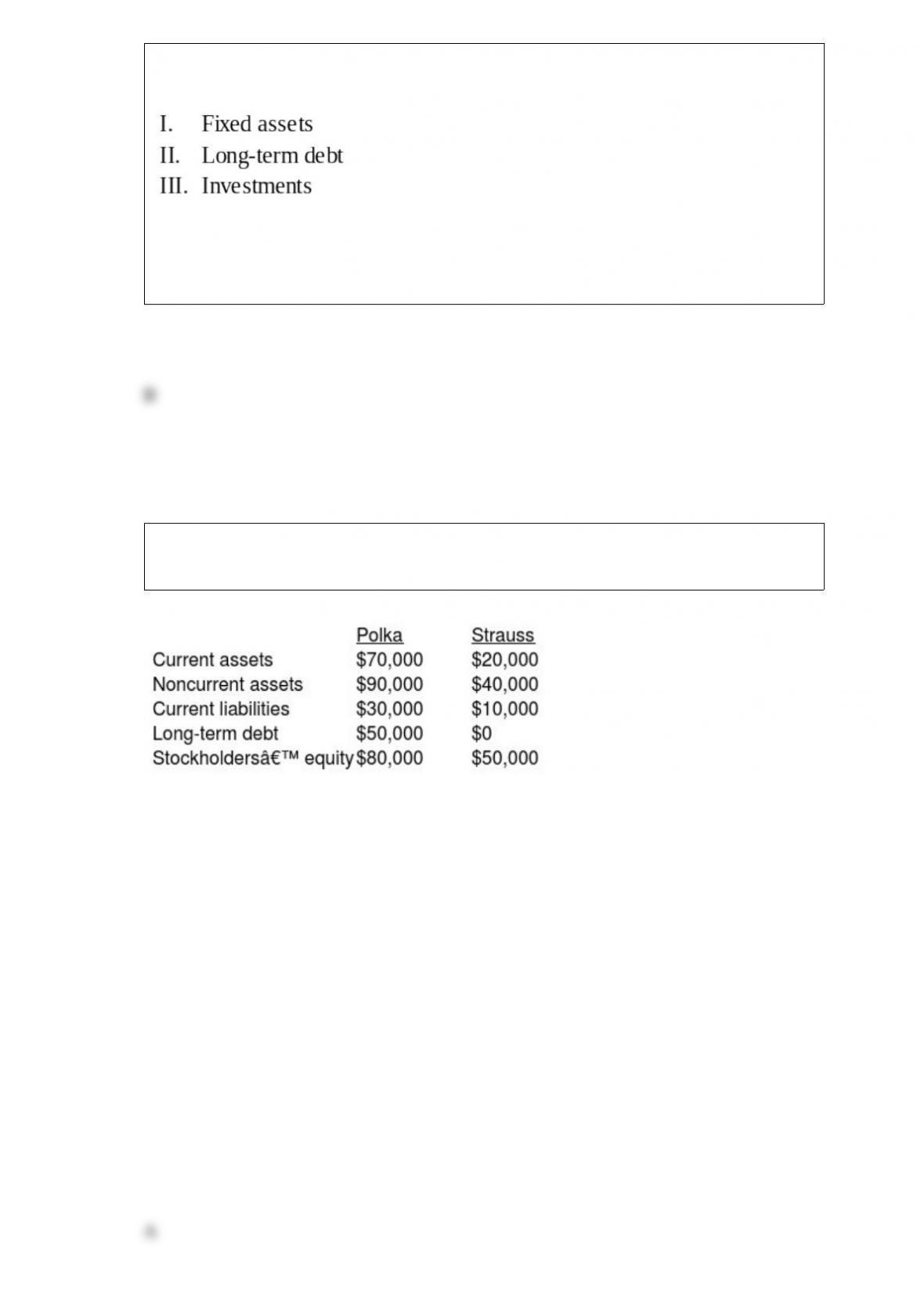

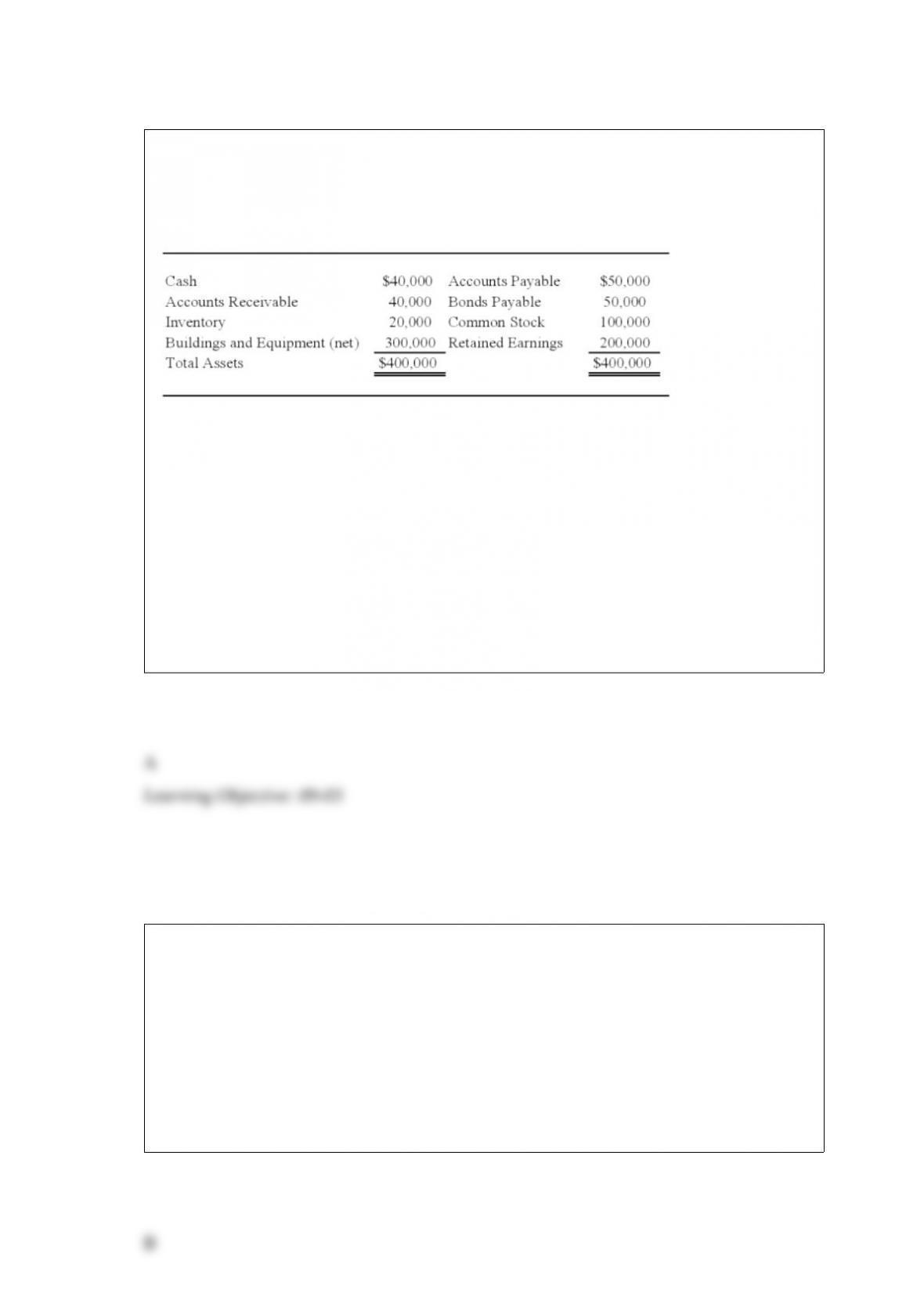

On January 1, 20X6, Polka Co. (Polka) and Strauss Co. (Strauss) had condensed

balance sheets as follows:

On January 2, 20X6, Polka borrowed $90,000 and used the proceeds to acquire 90% of the

outstanding common shares of Strauss. This debt is payable in ten equal annual principal

and accrued interest payments beginning December 30, 20X6. On the acquisition date, the

fair value of Strauss was $100,000, and the excess cost of the investment over Strauss’s

carrying amount of acquired net assets should be allocated 60% to inventory and 40% to

goodwill.

Current liabilities on the January 2, 20X6, consolidated balance sheet should be:

A. $49,000

B. $30,000

C. $40,000

D. $50,000

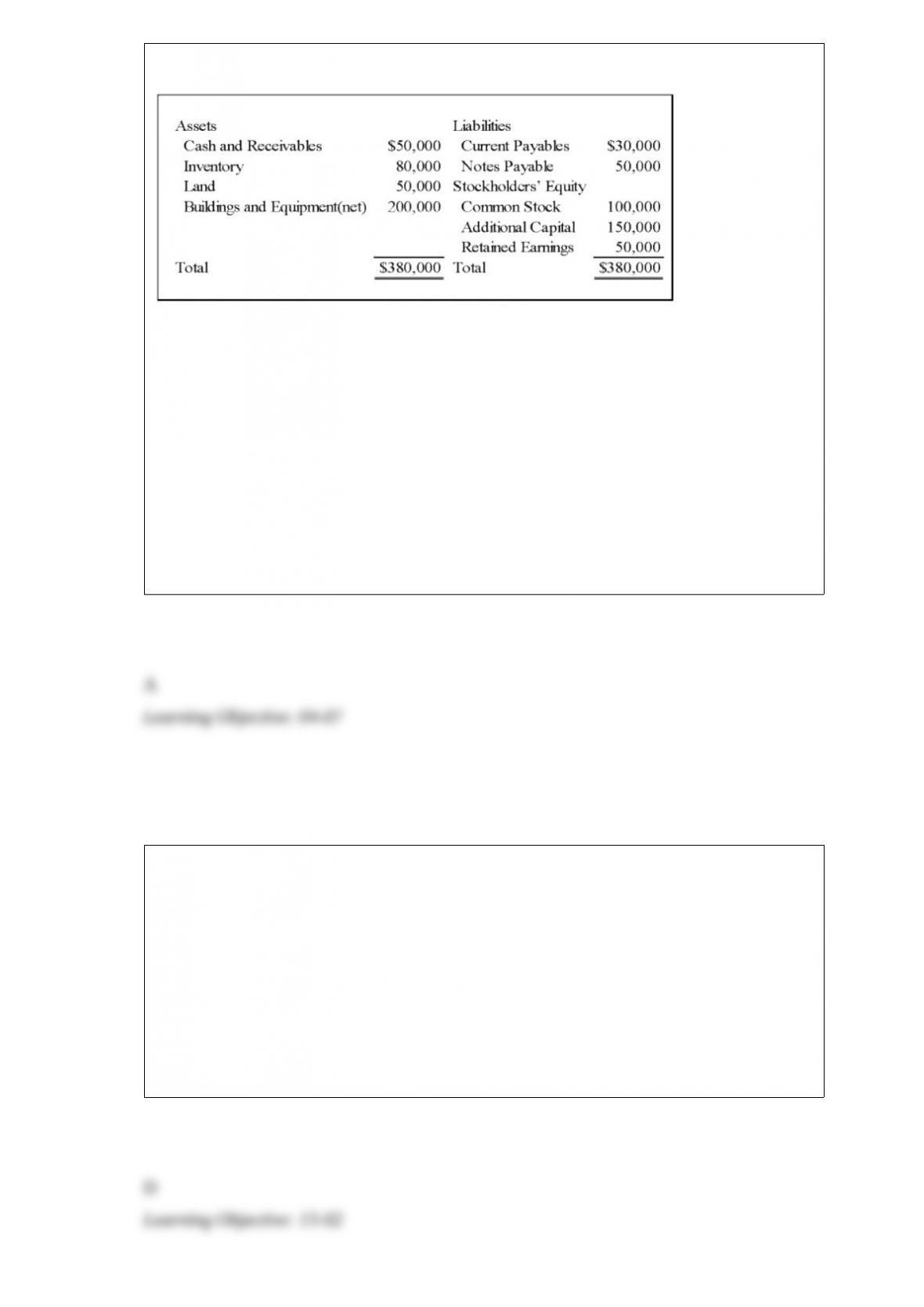

Bristle Corporation acquired 75 percent of Silver Corporation’s common stock on

December 31, 20X8, for $300,000. The fair value of the noncontrolling interest at that

date was determined to be $100,000. Silver’s balance sheet immediately before the

combination reflected the following balances:

A careful review of the fair value of Silver’s assets and liabilities indicated that

inventory, land, and buildings and equipment (net) had fair values of $65,000,

$100,000, and, $300,000 respectively. Goodwill is assigned proportionately to Bristle

and the noncontrolling shareholders.

Based on the preceding information, what amount of buildings and equipment (net) will

be included in the consolidated balance sheet immediately following the acquisition?

A. $0

B. $50,000

C. $250,000

D. $300,000

Gray College, a private not-for-profit institution, received a contribution of $100,000

for faculty research. The donation was received in 20X1 and $80,000 was spent in

20X1. As a result of these transactions, Gray College should report on its 20X1

statement of activities a:

A. $100,000 increase in temporarily restricted net assets.

B. $20,000 increase in temporarily restricted net assets.

C. $80,000 increase in temporarily restricted net assets.

D. $100,000 increase in unrestricted net assets.

Wally Corporation acquired 70 percent of the common shares and 60 percent of the

preferred shares of Safety Corporation at underlying book value on January 1, 20X6. At

that date, the fair value of the noncontrolling interest in Safety’s common stock was

equal to 30 percent of the book value of its common stock. Safety’s balance sheet at the

time of acquisition contained the following balances:

Assets $700,000 Liabilities $110,000

Preferred Stock 100,000

Common Stock 200,000

Retained Earnings 290,000

Total Assets $700,000 Total Liabilities and Equities $700,000

The preferred shares are cumulative and have an 8 percent annual dividend rate and are

three years in arrears on January 1, 20X6. All of the $10 par value preferred shares are

callable at $12 per share. During 20X6, Safety reported net income of $80,000 and paid

no dividends.

Based on the preceding information, the amount assigned to the noncontrolling

stockholders’ share of preferred stock interest in the preparation of a consolidated

balance sheet on January 1, 20X6 is

A. $57,600

B. $49,600

C. $48,000

D. $40,000

Catalyst Corporation acquired 90 percent of Trigger Corporation’s common stock on

September 30, 20X8 for $225,000. At that date, the fair value of the noncontrolling

interest was $25,000. On January 1, 20X8, Trigger reported the following stockholders’

equity balances:

Trigger reported net income of $80,000 in 20X8, earned uniformly throughout the year,

and declared and paid dividends of $10,000 on June 30 and $30,000 on December 31,

20X8. Catalyst reported retained earnings of $250,000 on January 1, 20X8, and had

20X8 income of $120,000 from its separate operations. Catalyst paid dividends of

$50,000 on December 31, 20X8. Catalyst accounts for its investment in Trigger

Corporation using the fully adjusted equity method.

Based on the information provided, what is the consolidated income to the controlling

interest reported for the year 20X8?

A. $192,000

B. $138,000

C. $140,000

D. $120,000

A partner’s tax basis in a partnership is comprised of which of the following items?

I. The partner’s tax basis of assets contributed to the partnership.

II. The amount of the partner’s liabilities assumed by the other partners.

III. The partner’s share of other partners’ liabilities assumed by the partnership.

A. I plus II minus III

B. I plus II plus III

C. I minus II plus III

D. I minus II minus III

Parent Company purchased 100 percent of Son Inc. on January 1, 20X2 for $420,000.

Son reported earnings of $82,000 and declared dividends of $4,000 during 20X2.

Based on the preceding information and assuming Parent uses the equity method to

account for its investment in Son, what is the balance in Parent’s Investment in Son

account on December 31, 20X2, prior to consolidation?

A. $416,000

B. $420,000

C. $424,000

D. $498,000

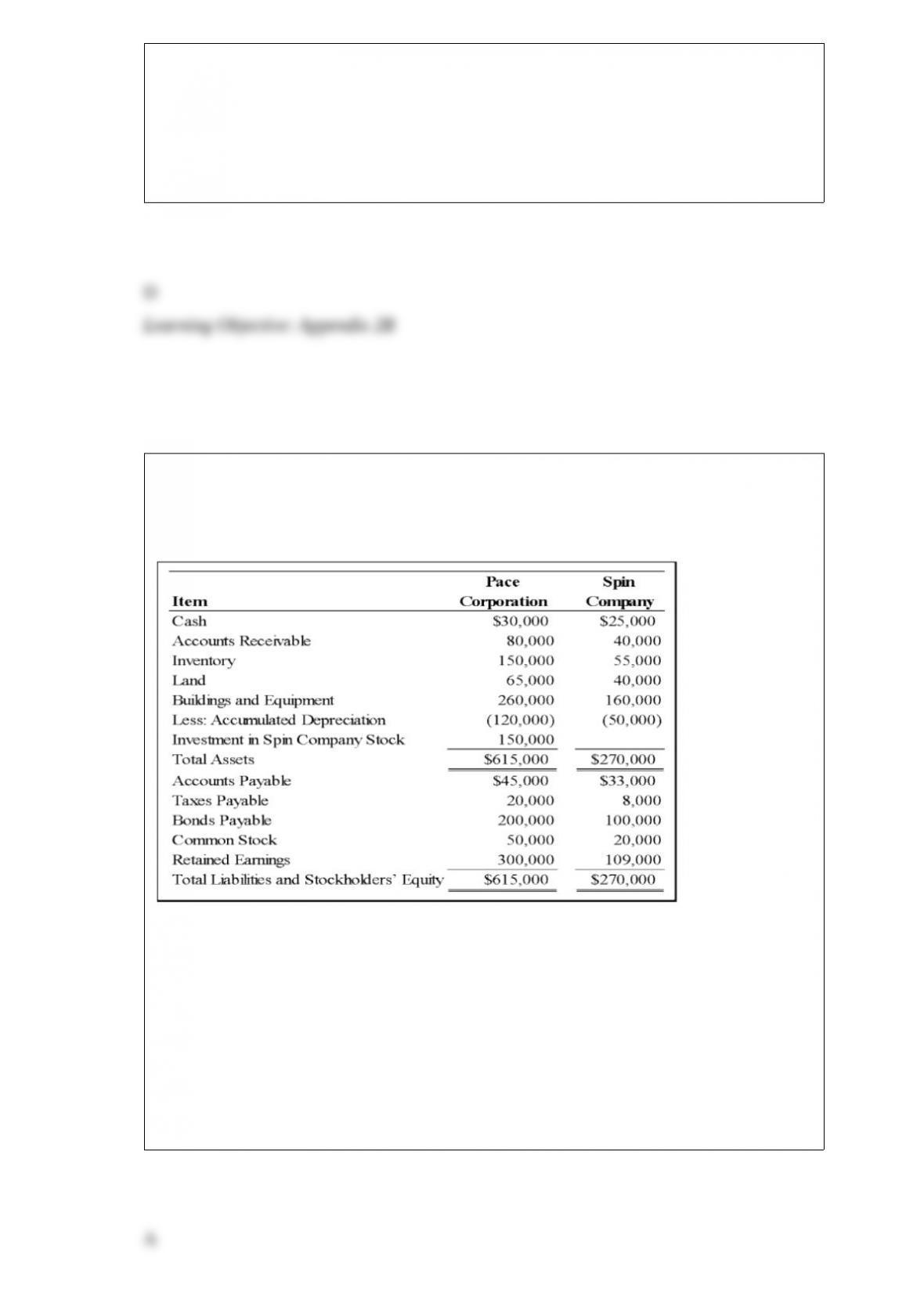

Pace Corporation acquired 100 percent of Spin Company’s common stock on January 1,

20X9. Balance sheet data for the two companies immediately following the acquisition

follow:

At the date of the business combination, the book values of Spin’s net assets and

liabilities approximated fair value except for inventory, which had a fair value of

$60,000, and land, which had a fair value of $50,000. The fair value of land for Pace

Corporation was estimated at $80,000 immediately prior to the acquisition.

Based on the preceding information, what amount of total assets will appear in the

consolidated balance sheet prepared immediately after the business combination?

A. $756,000

B. $735,000

C. $750,000

D. $642,000

The general fund of the City of Columbia transferred money to establish an internal

service fund for the city’s data processing needs. The general fund of Columbia should

account for this transaction as a(n):

A. expenditure.

B. interfund transfer.

C. interfund reimbursement.

D. loan.

When deficiencies are found in a registration statement that must be corrected before

the securities may be offered for sale, which of the following is issued by the SEC?

A. An audit opinion

B. A comment letter

C. A customary review

D. A comfort letter

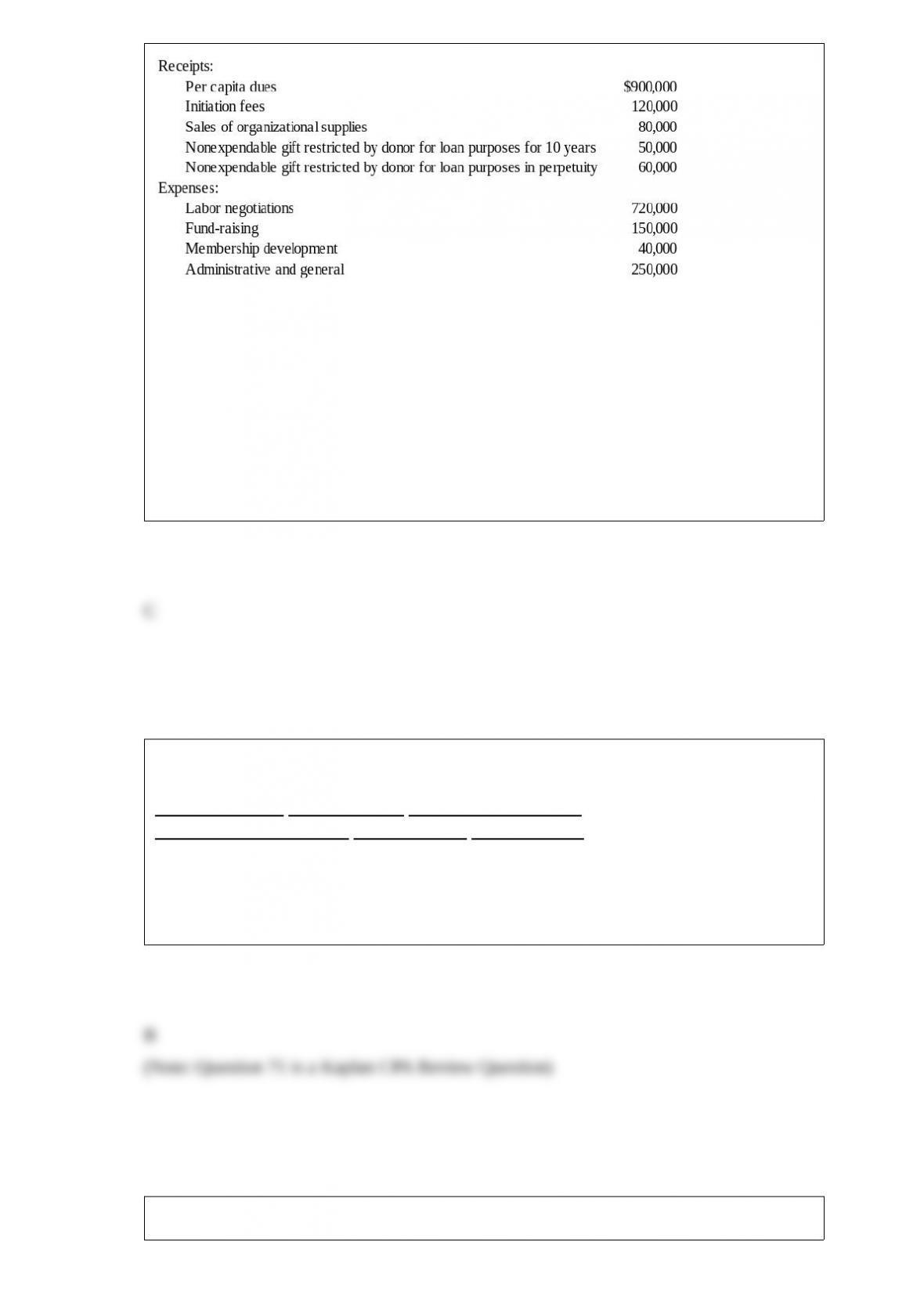

Golden Path, a labor union, had the following receipts and expenses for the year ended

December 31, 20X8:

The union’s constitution provides that 12 percent of the per capita dues be designated

for the strike insurance fund to be distributed for strike relief at the discretion of the

union’s executive board.

Based on the information provided, in Golden Path’s statement of activities for the year

ended December 31, 20X8, what amount should be reported under the classification of

supporting services?

A. $150,000

B. $720,000

C. $440,000

D. $290,000

Which of the following types of health care organizations follow FASB authoritative

literature?

Investor-Owned Not-For-Profit Governmental Health

Health Care Enterprises Organizations Organizations

A. Yes Yes Yes

B. Yes Yes No

C. No No Yes

D. Yes No Yes

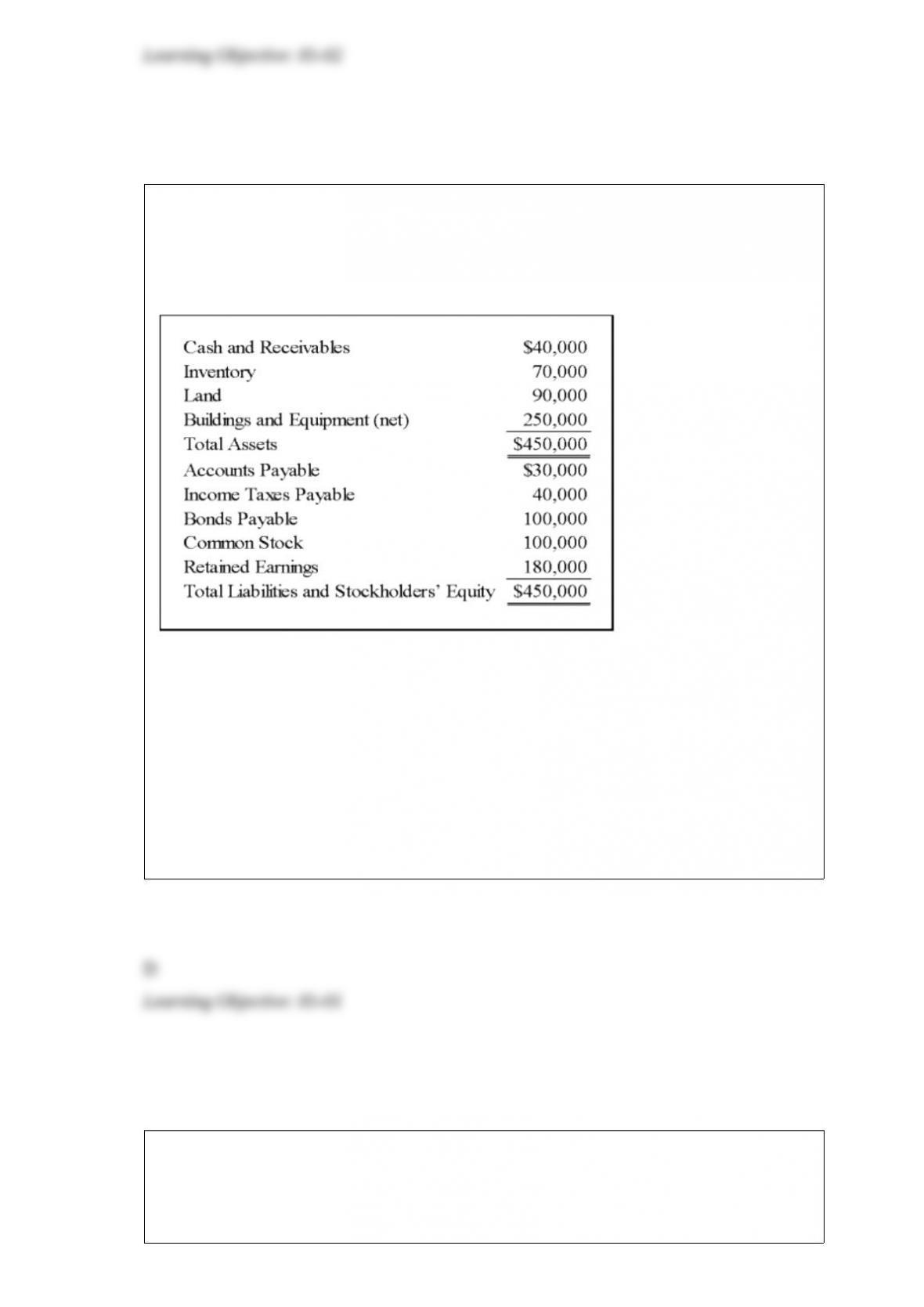

On January 1, 20X9, Wilton Company acquired all of Sirius Company’s common

shares, for $365,000 cash. On that date, Sirius’s balance sheet appeared as follows:

The fair values of all of Sirius’s assets and liabilities were equal to their book values

except for inventory that had a fair value of $85,000, land that had a fair value of

$60,000, and buildings and equipment that had a fair value of $250,000. Buildings and

equipment have a remaining useful life of 10 years with zero salvage value. Wilton

Company decided to employ push-down accounting for the acquisition. Subsequent to

the combination, Sirius continued to operate as a separate company.

Based on the preceding information, what amount of differential will arise in the

consolidation process?

A. $0

B. $5,000

C. $15,000

D. $65,000

In 20X6 and 20X7, each of Putney Company’s four operating segments met one of the

three quantitative tests for segment reporting. In 20X8, Segment B failed to qualify

under the prescribed tests because of abnormal financial conditions. The other three

segments qualified for reporting. For 20X8, Segment B:

A. should be excluded from segment disclosure but referred to in the management letter

to shareholders.

B. should be distinctly separated from the other three segments and listed as a

“nonqualifying” segment.

C. should be combined with one of the other three segments and reported.

D. should be included in the segment disclosures at the discretion of management.

Mortar Corporation acquired 80 percent of Granite Corporation’s voting common stock

on January 1, 20X7. On January 1, 20X8, Mortar received $350,000 from Granite for

equipment Mortar had purchased on January 1, 20X5, for $400,000. The equipment is

expected to have a 10-year useful life and no salvage value. Both companies depreciate

equipment on a straight-line basis.

Based on the preceding information, in the preparation of consolidation entries related

to the equipment transfer for the 20X8 consolidated financial statements, net effect on

accumulated depreciation will be:

A. a decrease of $50,000.

B. an increase of $110,000.

C. an increase of $120,000.

D. a decrease of $160,000.

If the U.S. dollar is the currency in which the foreign affiliate’s books and records are

maintained, and the U.S. dollar is also the functional currency,

A. the translation method should be used for restatement.

B. the remeasurement method should be used for restatement.

C. either translation or remeasurement could be used for restatement.

D. no restatement is required.

In the issuer’s annual report, how many years of audited financial statements must be

presented?

I. Three years of audited income statements

II. Two years of audited balance sheets

III. Three years of audited statements of cash flows

A. I and II

B. II and III

C. I and III

D. I, II, and III

Reportable segments are not required to disclose which of the following:

A. Amortization expense

B. Intersegment sales

C. Capital expenditures

D. Long-term debt

On October 1, 20X3, Green Corporation paid $450,000 for all of Yellow Company’s

outstanding common stock. On that date, the book values and fair values of Yellow’s

recorded assets and liabilities were as follows:

Book Value Fair Value

Cash and Receivables $75,000 $75,000

Inventory 155,000 160,000

Buildings and Equipment (net) 260,000 320,000

Liabilities (150,000) (150,000)

Net Assets $340,000 $405,000

Based on the preceding information, the differential implicit in this acquisition is

A. $0

B. $45,000

C. $65,000

D. $110,000

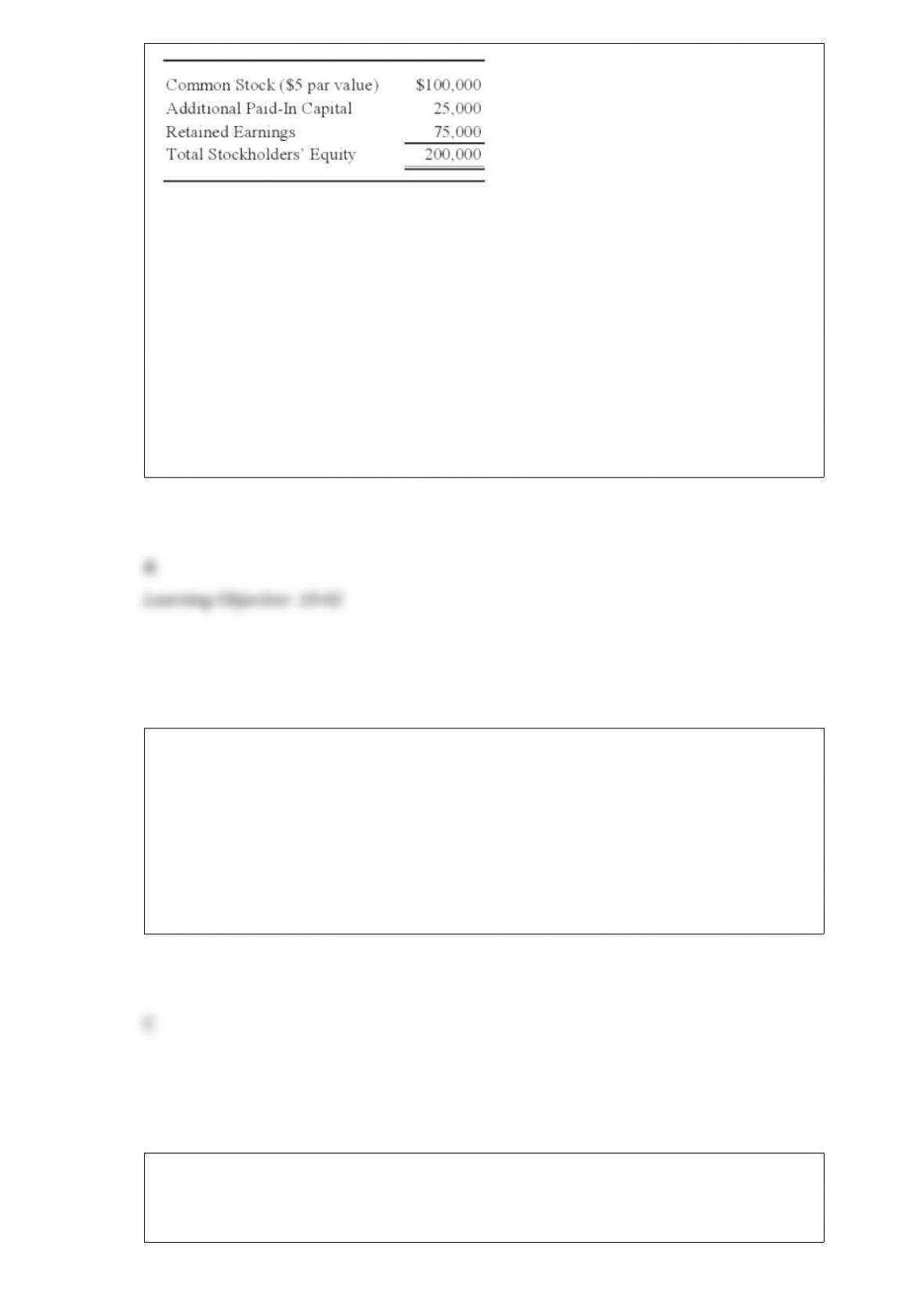

Vision Corporation acquired 75 percent of the stock of Meta Company on January 1,

20X7, for $225,000. At that date, the fair value of the noncontrolling interest was

$75,000. Meta’s balance sheet contained the following amounts at the time of the

combination:

During each of the next three years, Meta reported net income of $30,000 and paid

dividends of $10,000. On January 1, 20X9, Vision sold 1,500 shares of Meta’s $10 par

value shares for $60,000 in cash. Vision used the fully adjusted equity method in

accounting for its ownership of Meta Company.

Based on the preceding information, in the elimination entries to complete a full

consolidation worksheet for 20X9, noncontrolling interest in the net income of Meta

Co. will be credited for:

A. $12,000.

B. $7,500.

C. $8,000.

D. $2,500.

Frahm Company incurred a first quarter operating loss before income tax effect of

$4,000,000. This is a normal occurrence for Frahm because of seasonal fluctuations.

Experience has demonstrated the income earned during the remaining quarters far

exceeds the first quarter losses each year. Frahm estimates its annual income tax rate

will be 30 percent. What net loss should Frahm report for the first quarter?

A. $4,000,000

B. $2,800,000

C. $700,000

D. $0

Which of the following is true? When companies employ push-down accounting:

A. the subsidiary revalues assets and liabilities to their fair values as of the acquisition

date.

B. a special account called Revaluation Capital will appear in the consolidated balance

sheet.

C. all consolidation entries are made on the books of the subsidiary rather than in

consolidated worksheets.

D. the subsidiary is not substantially wholly owned by the parent.

Based on the information provided, what is the consolidated net income reported for the

year 20X4?

A. $280,000

B. $275,000

C. $260,000

D. $200,000

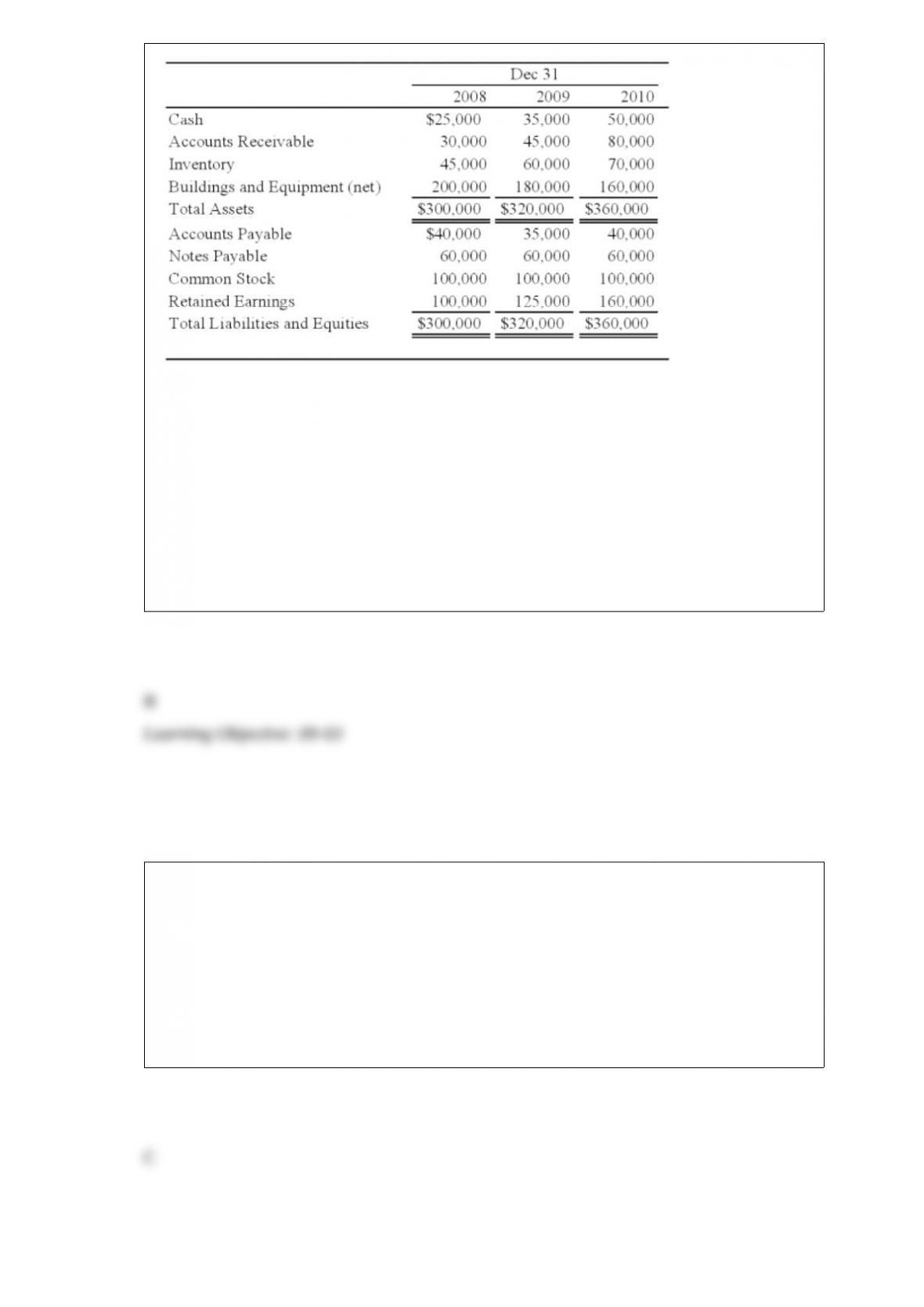

Perfect Corporation acquired 70 percent of Trevor Company’s shares on December 31,

2008, for $140,000. At that date, the fair value of the noncontrolling interest was

$60,000. On January 1, 2010, Perfect acquired an additional 10 percent of Trevor’s

common stock for $32,500. Summarized balance sheets for Trevor on the dates

indicated are as follows:

Trevor paid dividends of $10,000 in each of the three years. Perfect uses the fully

adjusted equity method in accounting for its investment in Trevor and amortizes all

differentials over 5 years against the related investment income. All differentials are

assigned to patents in the consolidated financial statements.

Based on the preceding information, what was the balance in Perfect’s Investment in

Trevor Company Stock account on December 31, 2009?

A. $164,500

B. $157,500

C. $165,000

D. $168,000

A debt service fund for the City of Madison received $50,000 from a capital projects

fund. The amount received represented the premium received from the issuance of

general obligation bonds. What account should the debt service fund credit to record

this receipt?

A. Revenue-General Obligation Bond Premium.

B. Matured Bonds Payable.

C. Other Financing Sources—Transfer In from Capital Projects Fund.

D. Due to Capital Projects Fund.

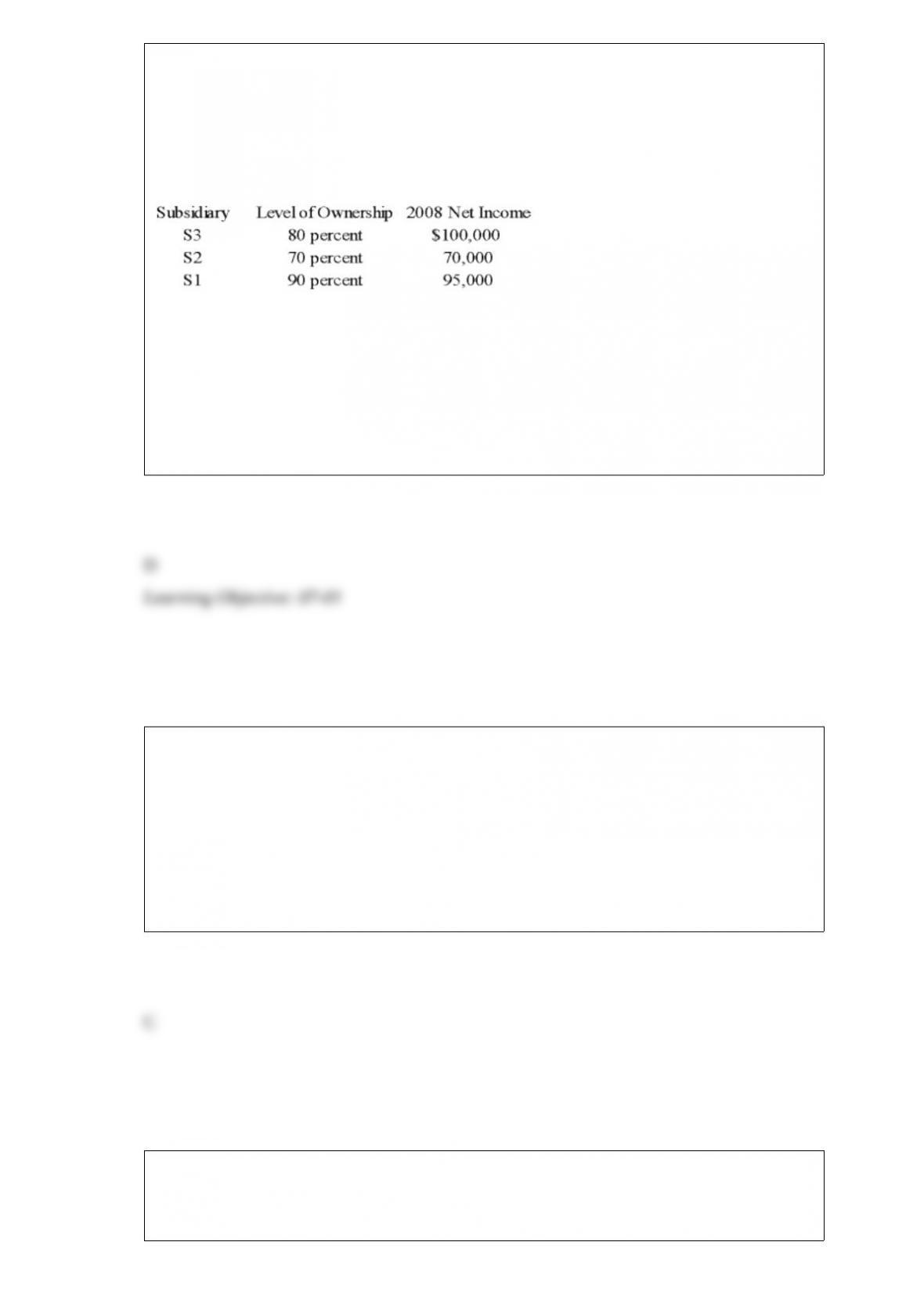

Parent Corporation purchased land from S1 Corporation for $220,000 on December 26,

20X8. This purchase followed a series of transactions between P-controlled

subsidiaries. On February 15, 20X8, S3 Corporation purchased the land from a

nonaffiliate for $160,000. It sold the land to S2 Company for $145,000 on October 19,

20X8, and S2 sold the land to S1 for $197,000 on November 27, 20X8. Parent has

control of the following companies:

Parent reported income from its separate operations of $200,000 for 20X8.

Based on the preceding information, at what amount should the land be reported in the

consolidated balance sheet as of December 31, 20X8?

A. $145,000

B. $220,000

C. $197,000

D. $160,000

Which of the following items are important in the determination of safe installment

payments to partners?

I. Deficits created in capital accounts are distributed to the remaining partners.

II. All unsold noncash assets are assumed to be worthless.

A. I only

B. II only

C. Both I and II

D. Neither I nor II

A city’s museum is supported by a special tax levy and by user charges. The user

charges constitute only 10 percent of the resources needed to support the operations of

the museum. In which fund should the city account for its museum?

A. An enterprise fund

B. An agency fund

C. An expendable trust fund

D. A special revenue fund