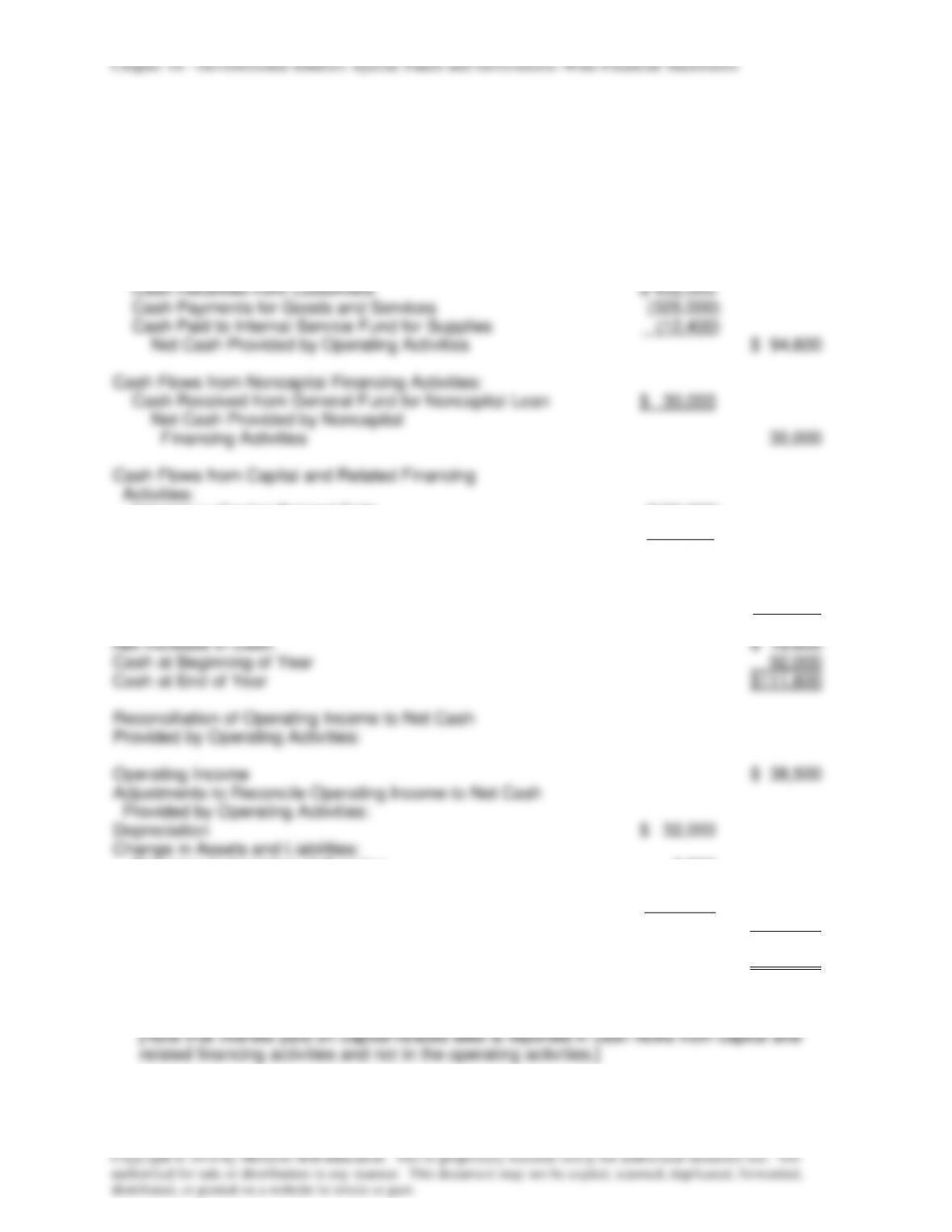

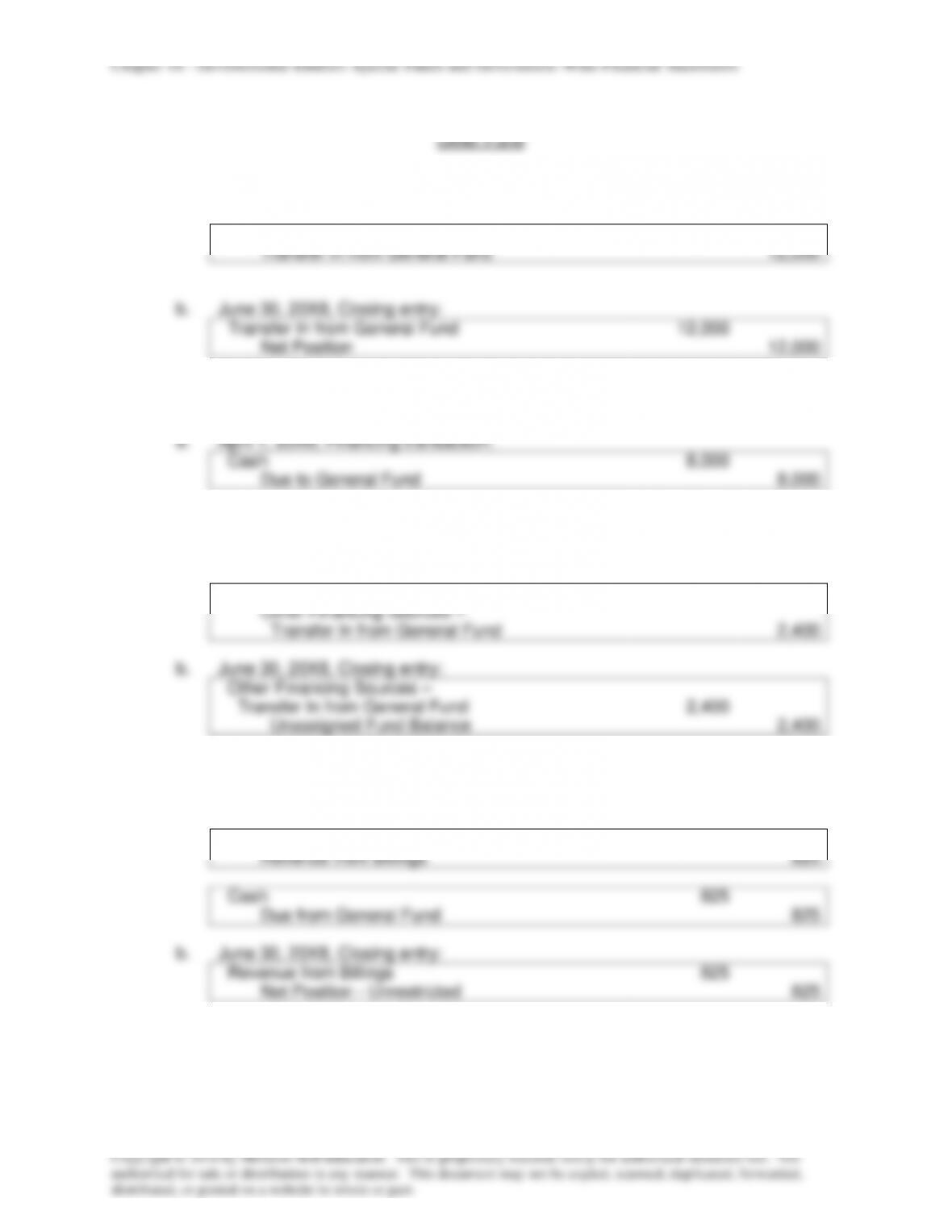

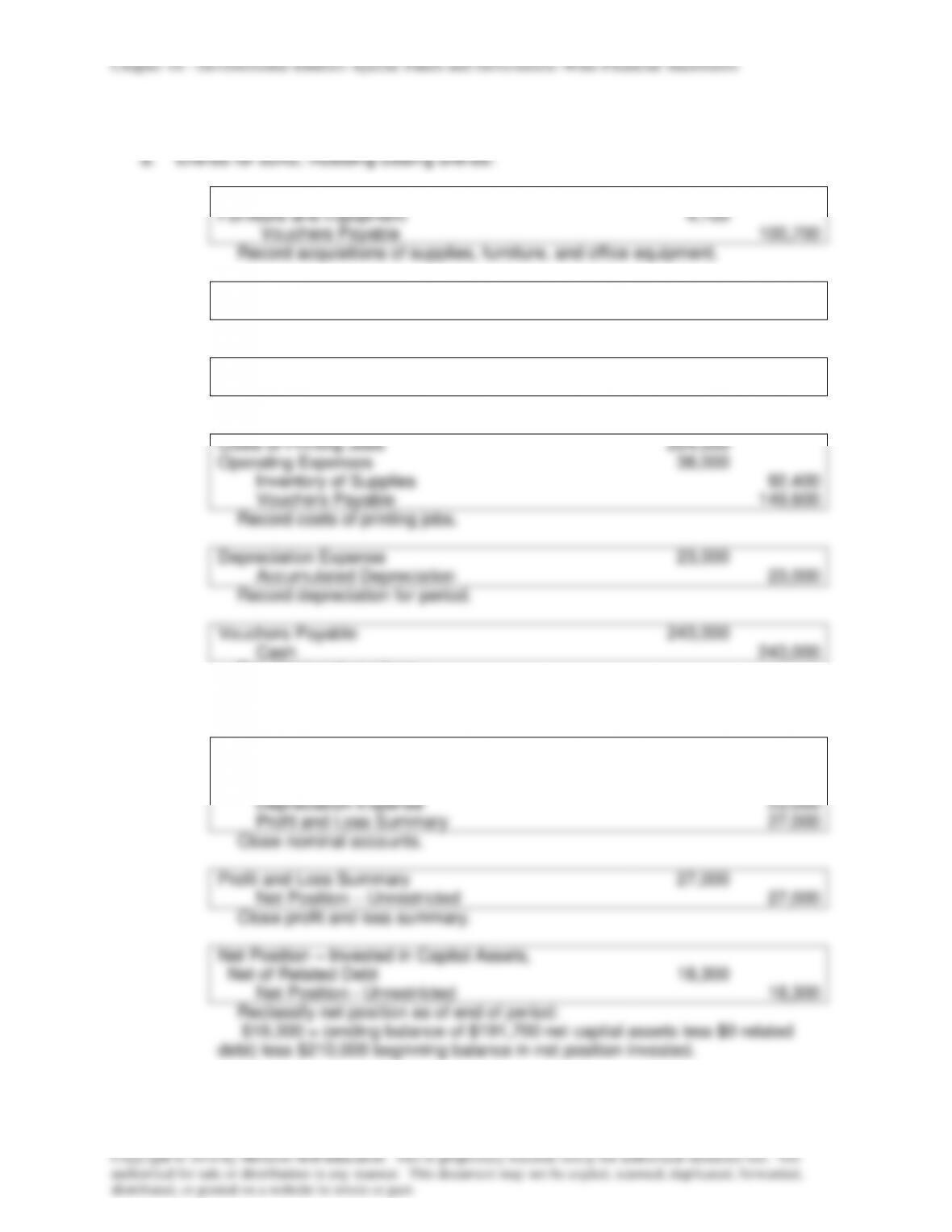

Chapter 18 – Governmental Entities: Special Funds and Government–Wide Financial Statements

E18-8 (continued)

c.

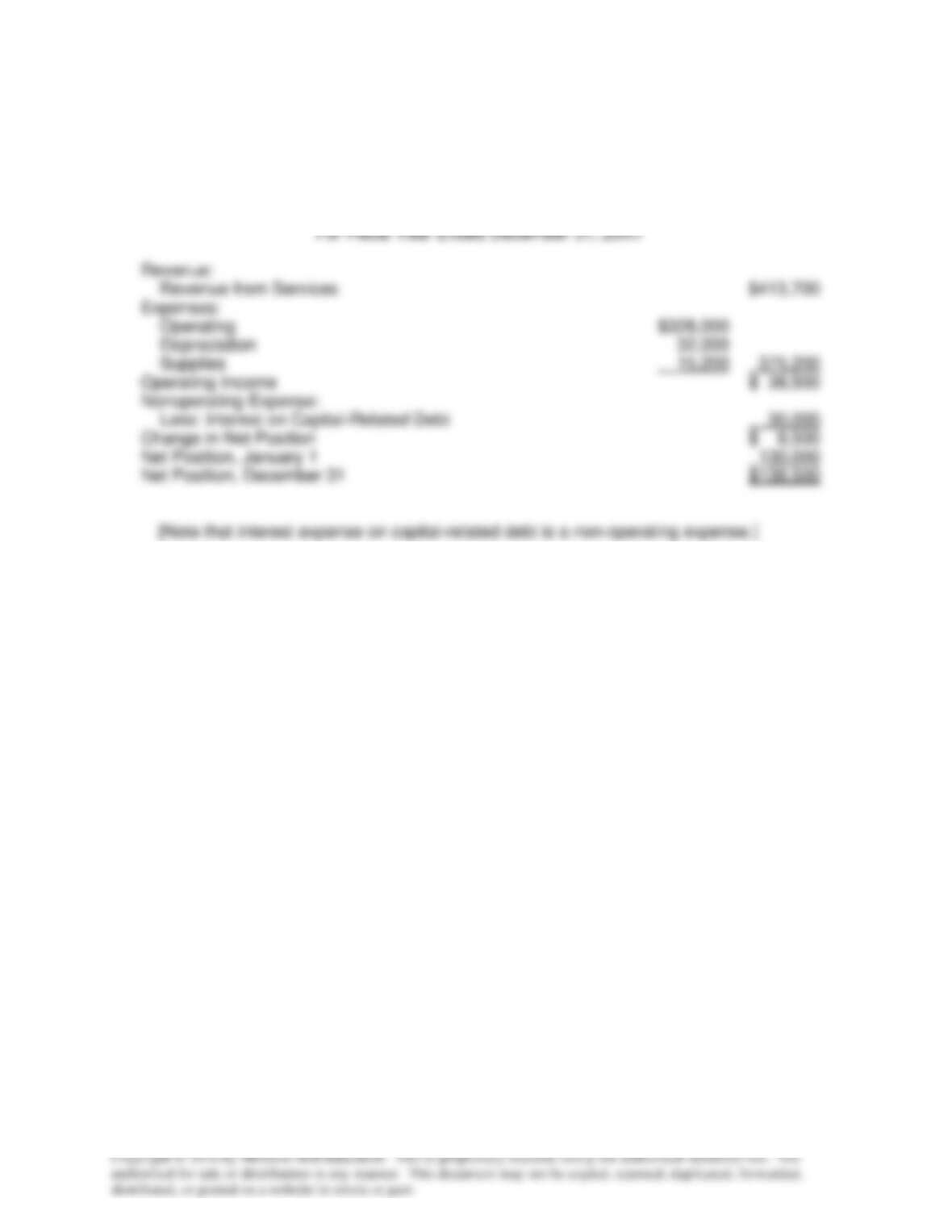

Augusta

MUD Enterprise Fund

Statement of Revenue, Expenses, and

Changes in Fund Net Position

For Fiscal Year Ended December 31, 20X1

Revenue:

Revenue from Services

$413,700

Expenses:

Operating

$328,000

Depreciation

32,000

Supplies

15,200

375,200

Operating Income

$ 38,500

Nonoperating Expense:

Less: Interest on Capital-Related Debt

30,000

Change in Net Position

$ 8,500

Net Position, January 1

130,000

Net Position, December 31

$138,500

[Note that interest expense on capital-related debt is a non-operating expense.]

Chapter 18 – Governmental Entities: Special Funds and Government–Wide Financial Statements

Copyright © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not

authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded,

distributed, or posted on a website in whole or part.

SOLUTIONS TO PROBLEMS

P18-12 Adjusting Entries for General Fund [AICPA Adapted]

Adjusting entries to correct the general fund:

1.

No entry required.

2.

Expenditures

300,000

Buildings

300,000

Correct for state grant expended for buildings.

Expenditures

22,000

Capital Outlays (equipment)

22,000

Correct for expenditures for playground equipment.

3.

Bonds Payable

1,000,000

Buildings

1,000,000

Correct for bonds used to construct buildings.

Other Financing Uses – Transfer

Out to Debt Service Fund

130,000

Debt Service from Current Funds

130,000

Correct for transfer to debt service fund.

4.

ENCUMBRANCES

2,800

BUDGETARY FUND BALANCE – ASSIGNED

FOR ENCUMBRANCES

2,800

Correct for unrecorded encumbrances.

5.

Expenditures

4,950

Inventory of Supplies

4,950

Correct for supplies used in period.

Fund Balance – Unassigned

6,500

Fund Balance – Assigned for Inventory

6,500

Correct for reserve for ending inventory.

Copyright © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not

authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded,

distributed, or posted on a website in whole or part.

Fund

Journal Entries

1.

General

ESTIMATED REVENUES CONTROL

400,000

Fund

APPROPRIATIONS CONTROL

394,000

BUDGETARY FUND BALANCE – UNASSIGNED

6,000

2.

General

Taxes Receivable – Current

390,000

Fund

Revenue – Taxes

382,200

Allowance for Uncollectibles – Current

7,800

3.

Private-

Investments

50,000

Purpose

Contributions

50,000

Trust Fund

Cash

5,500

Additions – Interest

5,500

4.

General

Other Financing Uses – Transfer

Out to Internal Service Fund

5,000

Cash

5,000

Internal

Cash

5,000

Service

Transfer In from General Fund

5,000

Fund

5.

Capital

Cash

72,000

Projects

Other Financing Sources – Bond Issue

72,000

Due from General Fund

3,000

Other Financing Sources –

Transfer In from General Fund

3,000

Debt

Special Assessments Receivable

24,000

Service

Revenue – Special Assessments

24,000

Fund

General

Other Financing Uses – Transfer

Out to Capital Projects Fund

3,000

Due to Capital Projects Fund

3,000

6.

General

Due to Capital Projects Fund

3,000

Fund

Cash

3,000

Capital

Cash

3,000

Projects

Due from General Fund

3,000

Fund

Debt

Cash

24,000

Service

Special Assessments Receivable

24,000

Fund