On the statement of functional expenses prepared for a voluntary health and welfare

organization, depreciation expense is allocated to

I. expenses for program services.

II. expenses for supporting services.

A. I only

B. II only

C. Both I and II

D. Neither I nor II

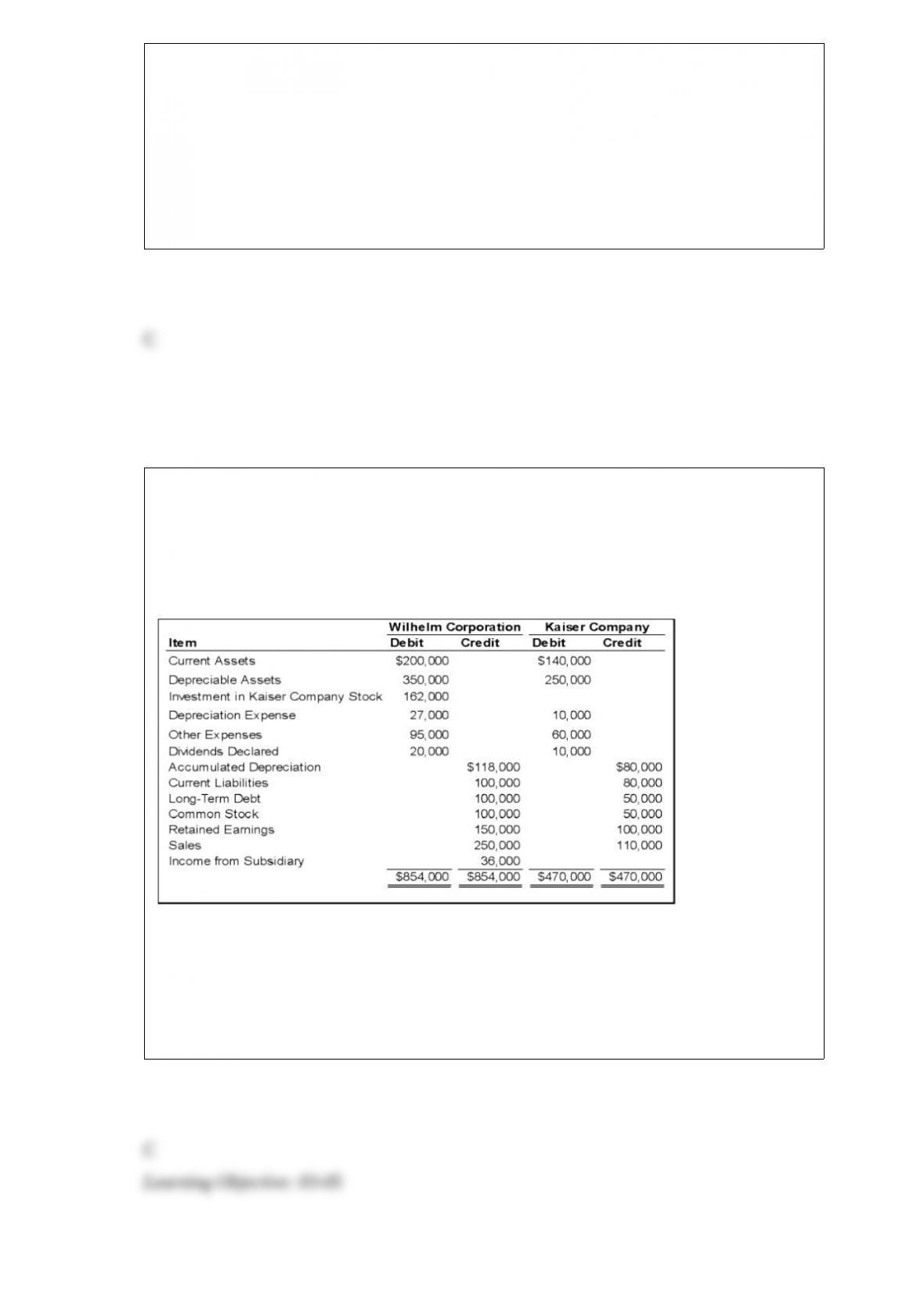

On January 1, 20X8, Wilhelm Corporation acquired 90 percent of Kaiser Company’s

voting stock, at underlying book value. The fair value of the noncontrolling interest was

equal to 10 percent of the book value of Kaiser at that date. Wilhelm uses the equity

method in accounting for its ownership of Kaiser. On December 31, 20X9, the trial

balances of the two companies are as follows:

Based on the preceding information, what amount would be reported as total assets in

the consolidated balance sheet at December 31, 20X9?

A. $805,000

B. $712,000

C. $742,000

D. $1,102,000

Paccu Corporation acquired 100 percent of Sallee Company’s common stock on

January 1, 20X7. Balance sheet data for the two companies immediately following the

acquisition follow:

Paccu Sallee

Cash $50,000 $30,000

Accounts Receivable 60,000 35,000

Inventory 130,000 45,000

Land 75,000 60,000

Buildings and Equipment 310,000 170,000

Less: Accumulated Depreciation (130,000) (30,000)

Investment in Sallee Company Stock 250,000

Total Assets $745,000 $310,000

Accounts Payable $40,000 $35,000

Taxes Payable 30,000 12,000

Bonds Payable 250,000 50,000

Common Stock 75,000 75,000

Retained Earnings 350,000 138,000

Total Liabilities and Stockholders’ Equity $745,000 $310,000

At the date of the business combination, the book values of Sallee’s assets and liabilities

approximated fair value except for inventory, which had a fair value of $55,000, and

land, which had a fair value of $65,000. The fair value of land for Paccu Corporation

was estimated at $90,000 immediately prior to the acquisition.

Based on the preceding information, what amount of total assets will appear in the

consolidated balance sheet prepared immediately after the business combination?

A. $745,000

B. $805,000

C. $830,000

D. $842,000

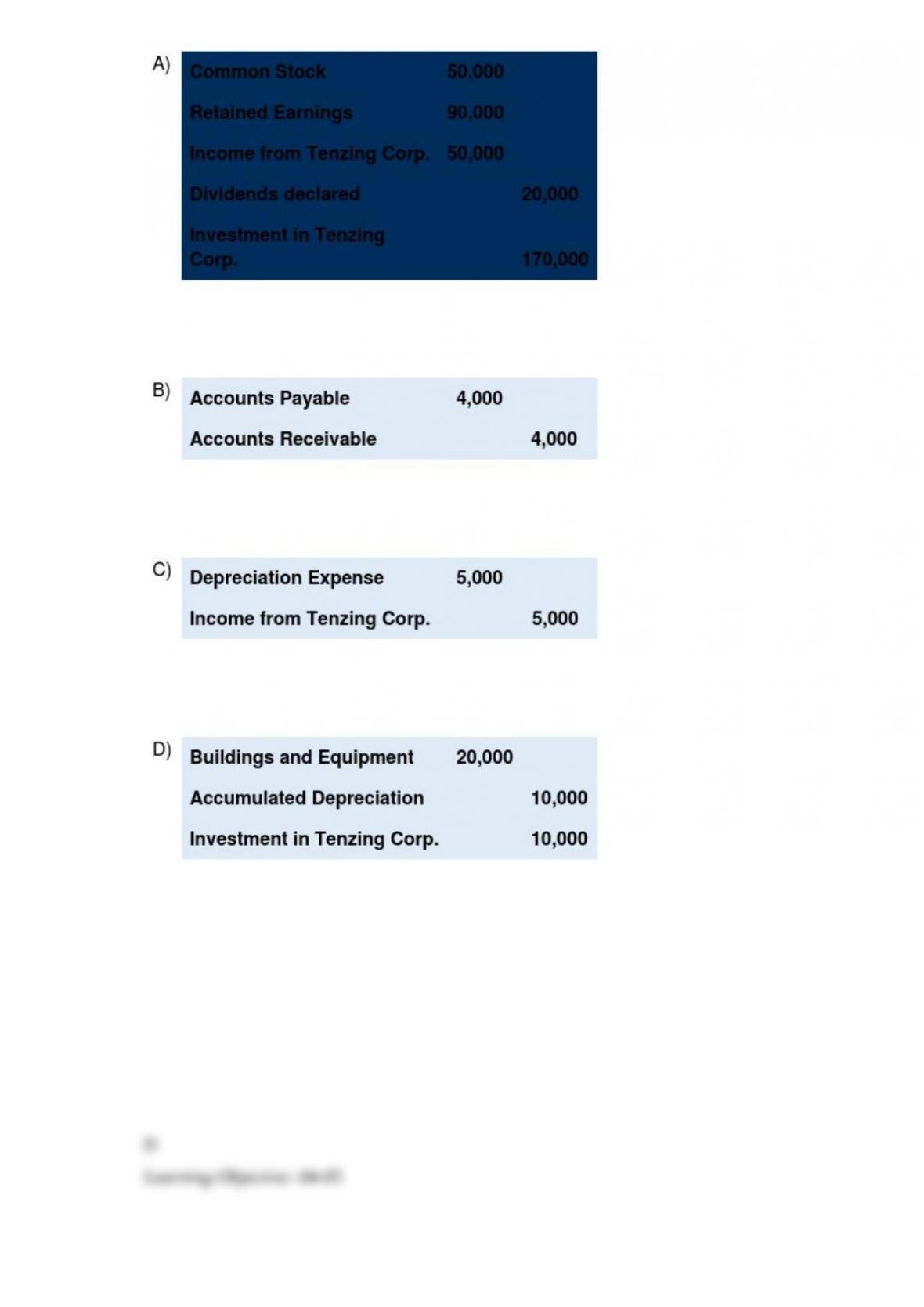

Lea Company acquired all of Tenzing Corporation’s stock on January 1, 20X6 for

$150,000 cash. On December 31, 20X8, the trial balances of the two companies were as

follows:

Tenzing Corporation reported retained earnings of $75,000 at the date of acquisition.

The difference between the acquisition price and underlying book value is assigned to

buildings and equipment with a remaining economic life of five years from the date of

acquisition. At December 31, 20X8, Tenzing owed Lea $4,000 for services provided.

Based on the preceding information, all of the following are consolidating entries

required on December 31, 20X8, to prepare consolidated financial statements, except:

A. Option A

B. Option B

C. Option C

D. Option D

The gain or loss on the effective portion of a U.S. parent company’s hedge of a net

investment in a foreign entity should be treated as:

A. an adjustment to the retained earnings account in the stockholders’ equity section of

its balance sheet.

B. other comprehensive income.

C. a translation gain or loss in the computation of net income for the reporting period.

D. an adjustment to a valuation account in the asset section of its balance sheet.

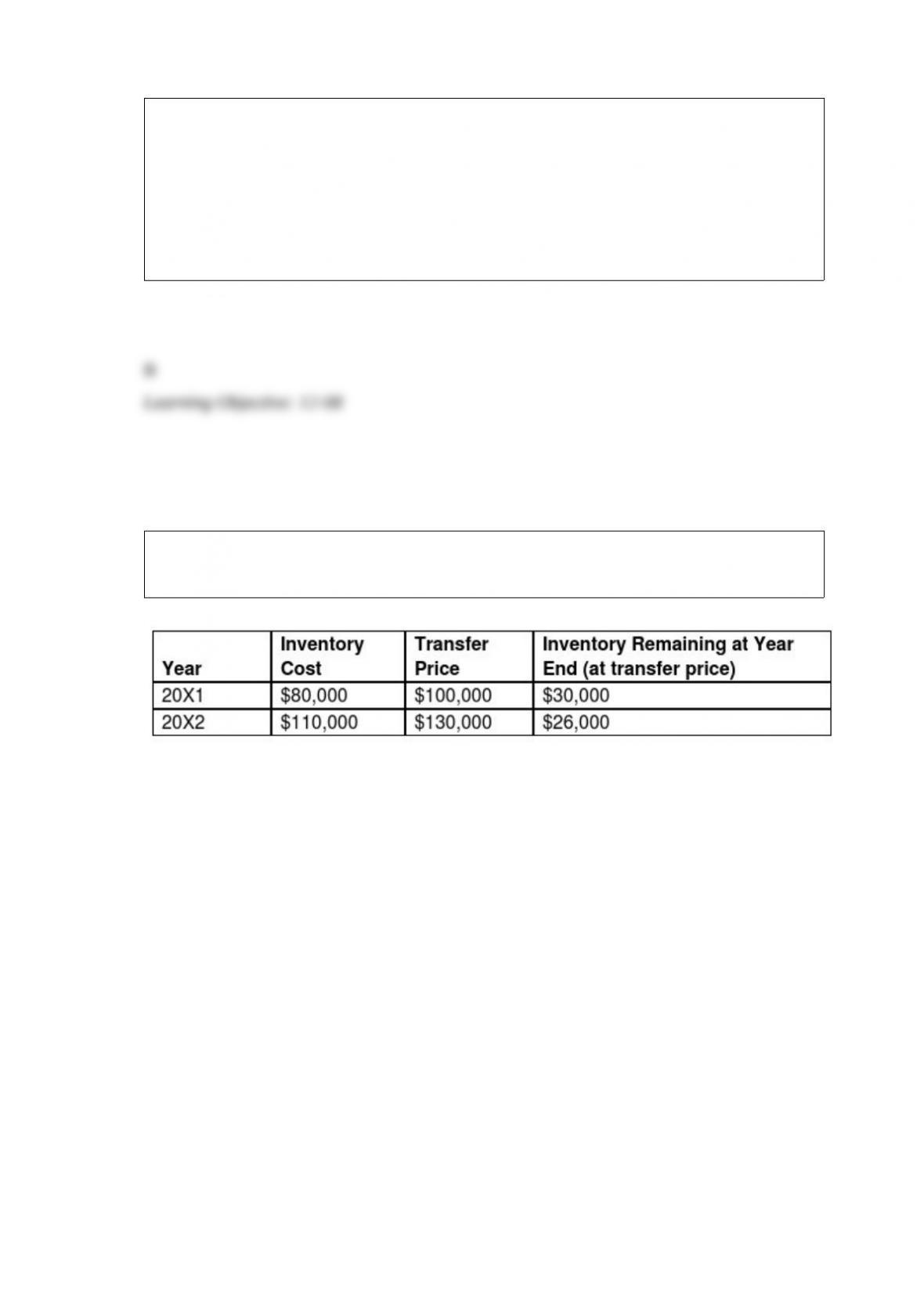

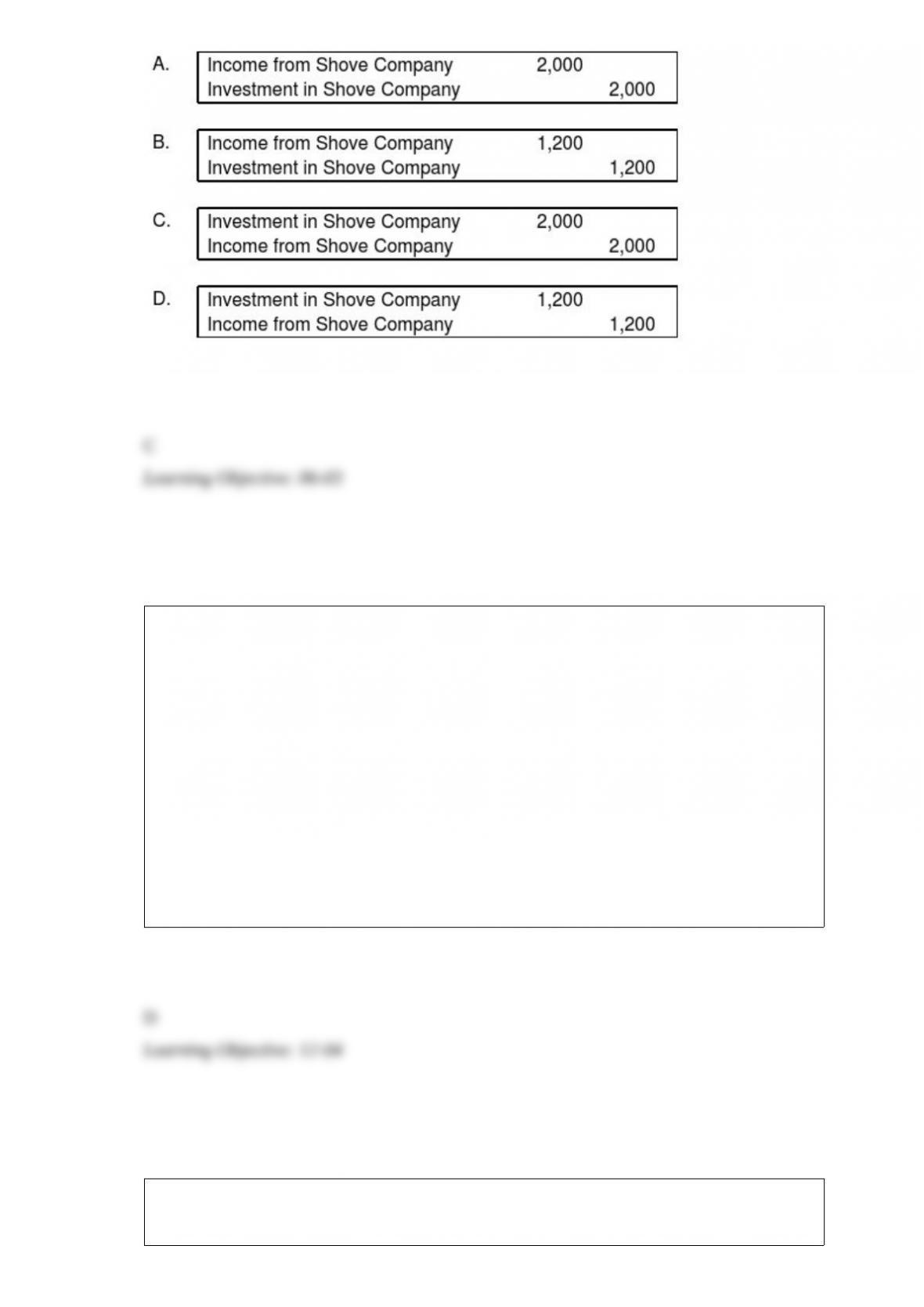

Push Company owns 60% of Shove Company’s outstanding common stock. Intra-entity

sales are as follows:

Assume Push sold the inventory to Shove. Using the fully adjusted equity method, what

journal entry would be recorded by Push to recognize the realization of the 20X1 deferred

intercompany profit and to defer the 20X2 unrealized gross profit on inventory sales to

Shove?

On October 15, 20X1, Jerry Company sold inventory to Garcia Corporation, its

Mexican subsidiary. The goods cost Jerry $2,700 and were sold to Garcia for $3,500,

payable in Mexican pesos. The goods are still on hand at the end of the year on

December 31. The Mexican peso is the functional currency of Garcia. The exchange

rates follow:

October 15 1 peso = $0.07

December 31 1 peso = $0.08

Based on the preceding information, at what dollar amount is the ending inventory

shown in the subsidiary’s trial balance column of the consolidation worksheet?

A. $3,250

B. $3,500

C. $3,750

D. $4,000

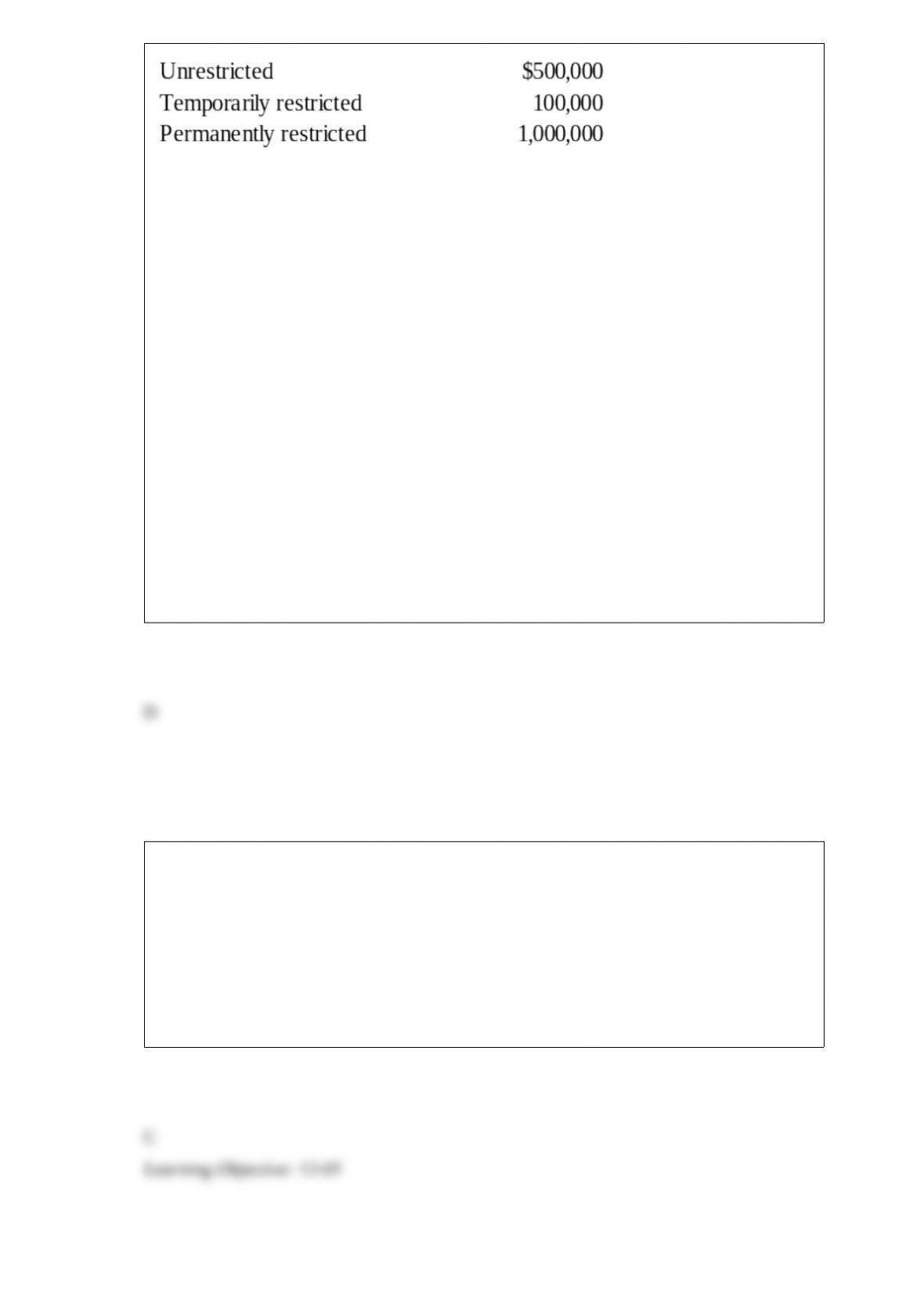

Local Services, a voluntary health and welfare organization had the following classes of

net assets on July 1, 20X8, the beginning of its fiscal year:

During the year ended June 30, 20X9, the following events occurred:

(1) It purchased equipment, costing $100,000, with contributions restricted for this

purpose. The contributions had been received from donors during June of 20X8.

(2) It received $130,000 of cash donations which were restricted for research activities.

During the year ended June 30, 20X9, $90,000 of the contributions were expended on

research.

(3) It sold investments classified in the permanently restricted class for a loss of

$40,000. Dividends and interest income earned on the investments amounted to

$70,000. There were no restrictions on how investment income was to be used.

(4) It received cash contributions of $200,000 from donors who did not place either

time or use restrictions upon their donations.

(5) Expenses, excluding depreciation expense, for program services and supporting

services incurred during the year ended June 30, 20X9, amounted to $260,000.

(6) Depreciation expense for the year ended June 30, 20X9, was $80,000.

Refer to the above information. At June 30, 20X9, the amount of permanently restricted

net assets reported on the statement of financial position would be:

A. $1,070,000.

B. $1,030,000.

C. $1,000,000.

D. $960,000.

All of the following describe the International Accounting Standard Board (IASB)

except for:

A. The IASB is a privately funded accounting standards-setting body based in London.

B. The mission of the IASB is to develop a single set of high-quality, understandable

and enforceable global accounting standards.

C. Board members of the IASB come from diverse geographical countries that have

adopted IFRS.

D. IASB members serve a five-year term subject to one reappointment.

Five of eight internally reported operating segments of Rollins Company qualify under

the standards set by ASC 280 for segment reporting. However, the five identified

segments do not meet the 75 percent revenue test. ASC 280 prescribes that

management:

A. subdivide segments until there are at least 10 reportable segments.

B. consolidate the remaining operating segments and include them under an “all other”

category.

C. select additional operating segments until the 75% threshold is met.

D. include the heading “corporate headquarters” as an operating segment.

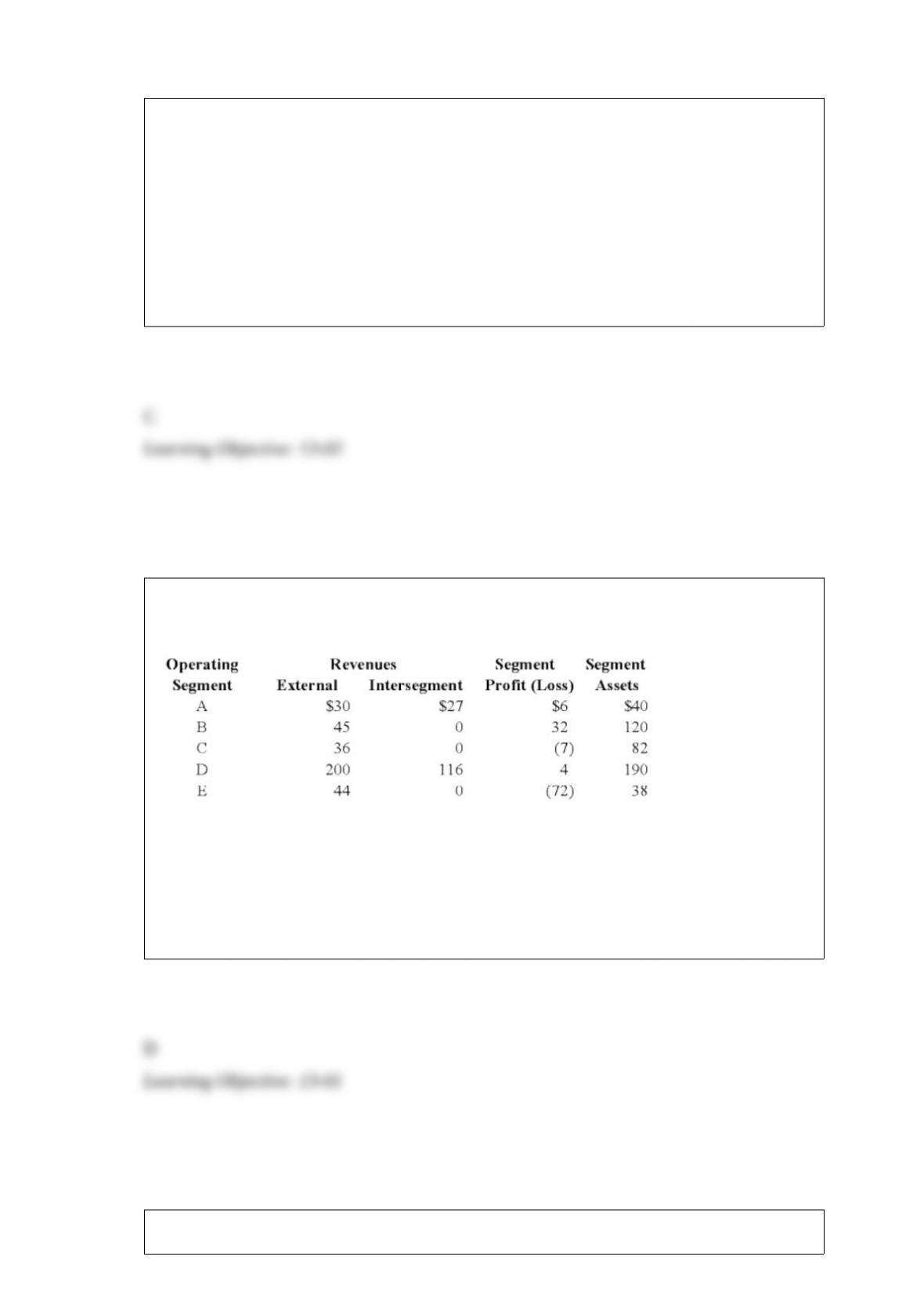

An analysis of Abbey Company’s operating segments provides the following

information:

Refer to the above information. Which of the operating segments above are reportable

segments?

A. B, C, and D

B. A, B, D, and E

C. B, D, and E

D. A, B, C, D, and E

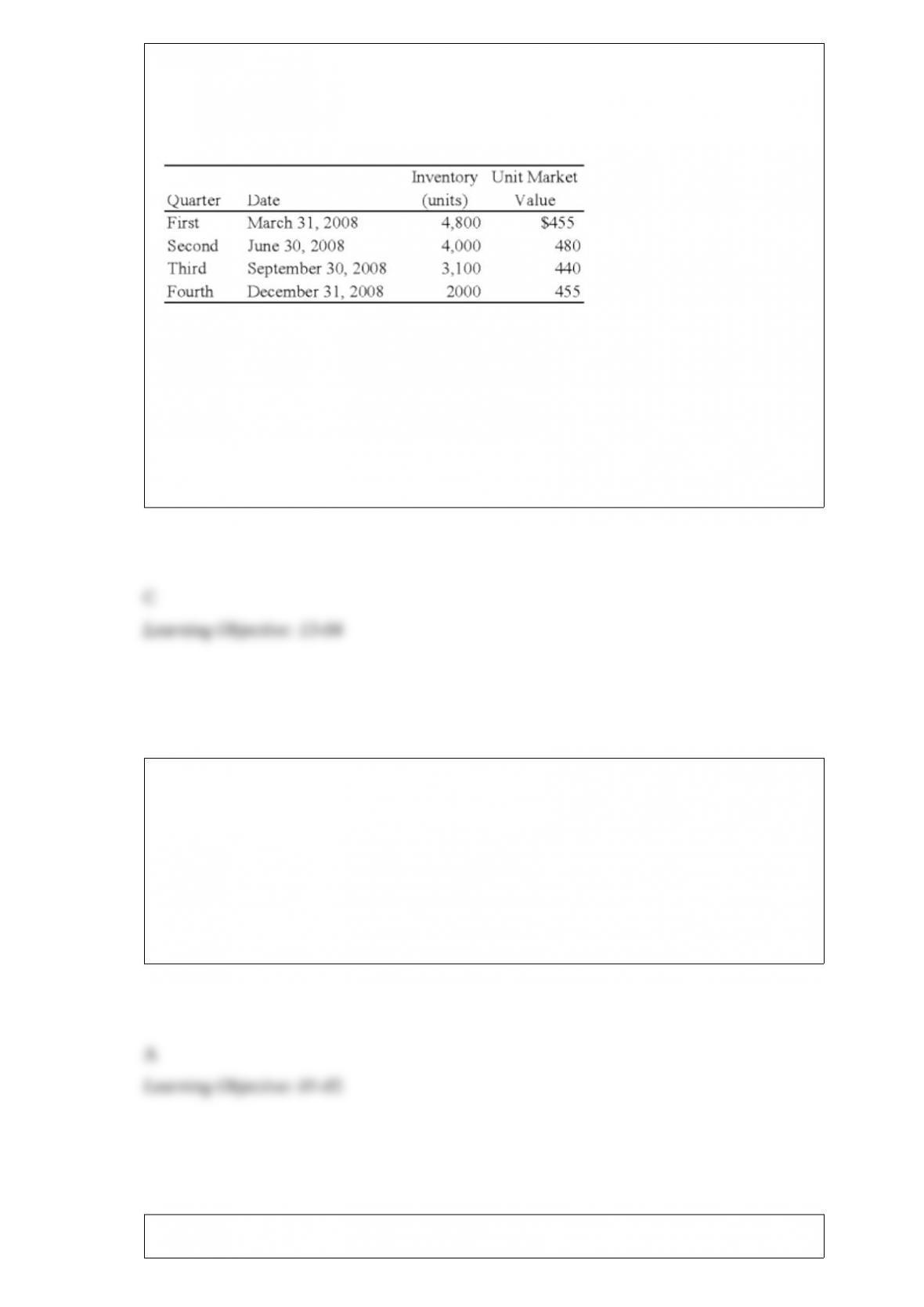

Forge Company, a calendar-year entity, had 6,000 units in its beginning inventory for

20X8. On December 31, 20X7, the units had been adjusted down to $470 per unit from

an actual cost of $510 per unit. It was the lower of cost or market. No additional units

were purchased during 20X8. The following additional information is provided for

20X8:

Forge does not have sufficient experience with the seasonal market for its inventory

units and assumes that any reductions in market value during the year will be

permanent.

Based on the preceding information, the cost of goods sold for the second quarter is:

A. $416,000

B. $364,000

C. $304,000

D. $424,000

Company X acquired for cash all of the outstanding common stock of Company Y. How

should Company X determine in general the amounts to be reported for the inventories

and long-term debt acquired from Company Y?

Inventories Long-term debt

A. Fair value Fair value

B. Fair value Recorded value

C. Recorded value Fair value

D. Recorded value Recorded value

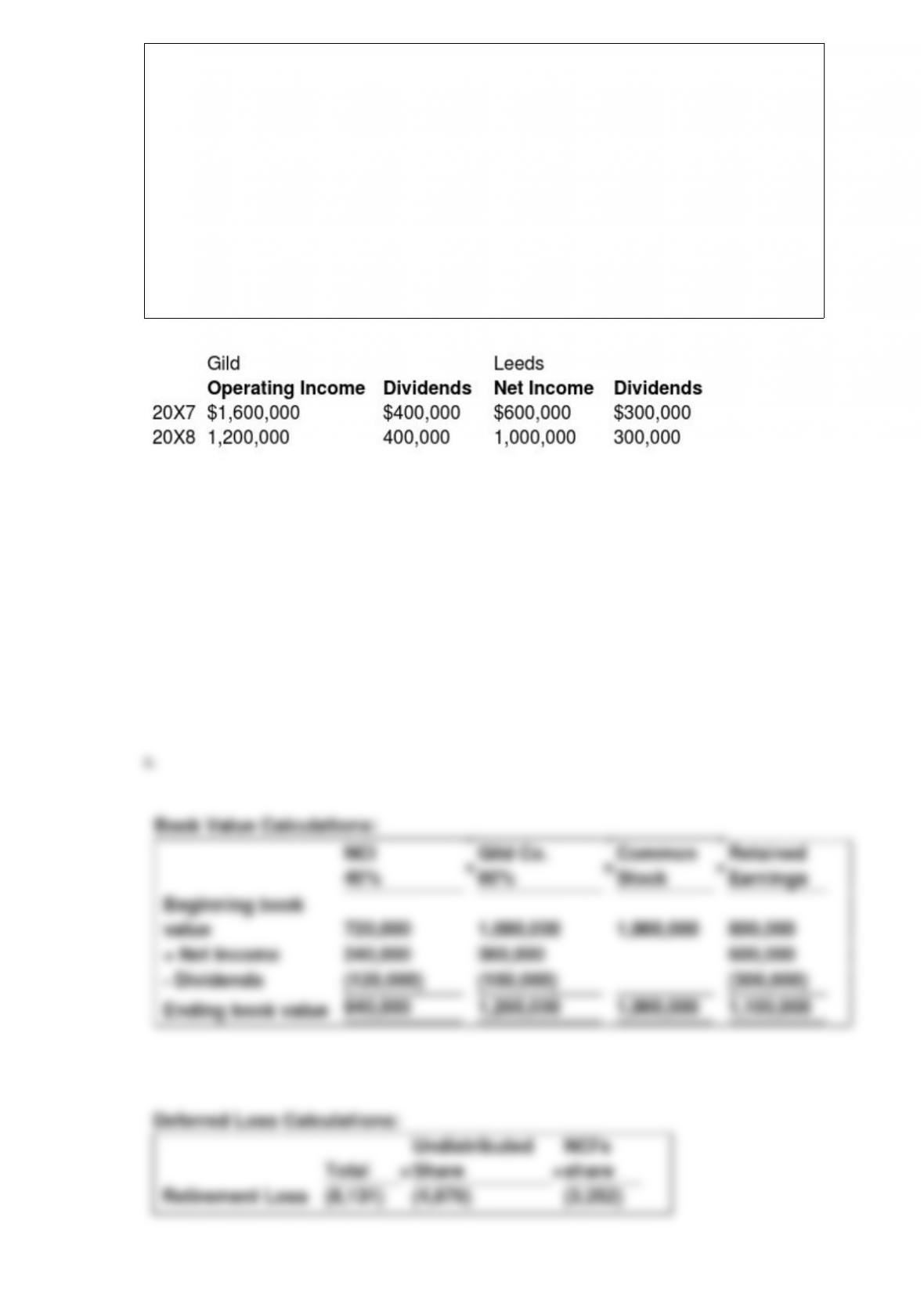

On January 1, 20X7, Gild Company acquired 60 percent of the outstanding common

stock of Leeds Company at the book value of the shares acquired. On that date, the fair

value of noncontrolling interest was equal to 40 percent of book value of Leeds. At the

time of purchase, Leeds had common stock of $1,000,000 outstanding and retained

earnings of $800,000.

On December 31, 20X7, Gild purchased 50 percent of Leeds’ bonds outstanding which

were originally issued on January 1, 20X4, at 99. The total bond issue has a face value

of $600,000, pays 10 percent interest annually, and has a 10-year maturity. Any

premium or discount is amortized using the effective interest method. Gild paid

$306,000 for its investment in Leeds’ bonds and intends to hold the bonds until

maturity.

Income and dividends for Gild and Leeds for 20X7 and 20X8 are as follows:

Assume Gild accounts for its investment in Leeds stock using the modified equity method.

Required:

A) Present the worksheet elimination entries necessary to prepare consolidated financial

statements for 20X7.

B) Present the worksheet elimination entries necessary to prepare consolidated financial

statements for 20X8.

Park Co. uses the equity method to account for its January 1, 20X5, purchase of Tun

Inc.’s common stock. On January 1, 20X5, the fair values of Tun’s depreciable assets

and land exceeded their carrying amounts. How do these excesses of fair values over

carrying amounts affect Park’s reported year-end Earnings from Investment in Tun for

20X5?

Depreciable assets excess Land excess

A. Decrease No effect

B. Decrease Decrease

C. Increase No effect

D. Increase Increase

The key to reporting accounting information by segments is determining what

constitutes a segment. Of the following, which is not a method of determining a

reportable segment?

A. Operating profit

B. Revenues

C. Number of employees

D. Combined identifiable assets

The general fund of the City of Atlanta received a check for $10,000 from an Atlanta

resident on July 1, 20X8. Of the amount received, $4,800 represented full payment of

property taxes for 20X8, and the remaining $5,200 represented an advance payment for

property taxes of 20X9. On July 1, 20X8, the general fund should record the receipt by

debiting Cash for $10,000 and by crediting

A. Revenue-Property Tax for $10,000.

B. Property Taxes Receivable-Current for $4,800 and Deferred Revenue for $5,200.

C. Revenue-Property Tax for $4,800 and Deferred Revenue for $5,200.

D. Property Taxes Receivable-Current for $4,800 and Revenue- Property Tax for

$5,200.

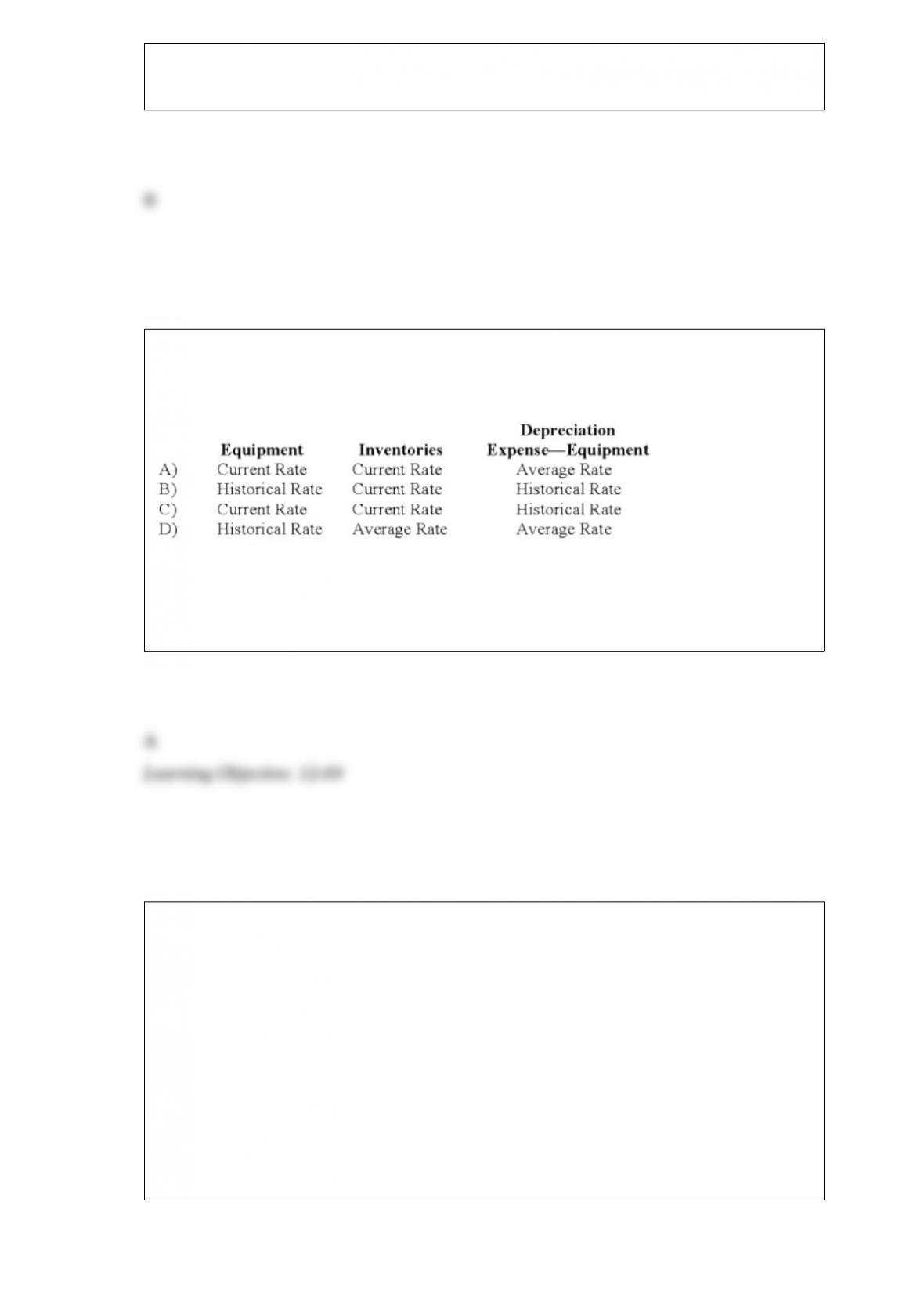

If the functional currency is the local currency of a foreign subsidiary, what exchange

rates should be used to translate the items below, assuming the foreign subsidiary is in a

country which has not experienced hyperinflation over three years?

A. Option A

B. Option B

C. Option C

D. Option D

The functional currency of Nash, Inc.’s subsidiary is the French franc. Nash borrowed

French francs as a partial hedge of its investment in the subsidiary. In preparing

consolidated financial statements, Nash’s translation loss on its investment in the

subsidiary exceeded its exchange gain on the borrowing. How should the effects of the

loss and gain be reported in Nash’s consolidated financial statements?

A. The translation loss less the exchange gain is reported separately as other

comprehensive income.

B. The translation loss less the exchange gain is reported in the income statement.

C. The translation loss is reported separately in the stockholders’ equity section of the

balance sheet and the exchange gain is reported in the income statement.

D. The translation loss is reported in the income statement and the exchange gain is

reported separately in the stockholders’ equity section of the balance sheet.

ASC 280 uses a(n) ______ approach to the definition of segments.

A. line of business

B. entity approach

C. portfolio

D. management

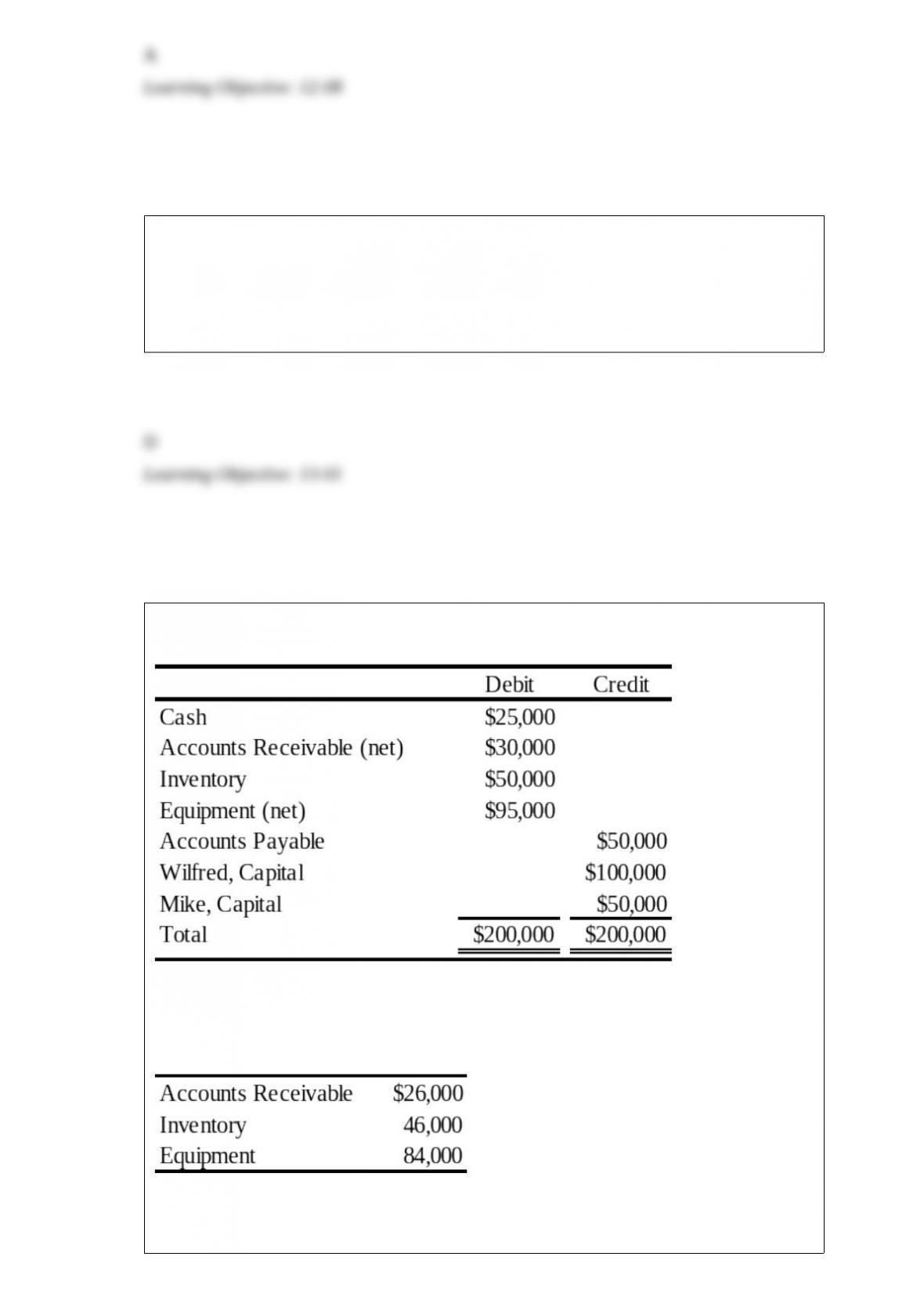

The trial balance of WM Partnership is as follows:

Wilfred and Mike decide to incorporate their partnership. The partnership’s books will

be closed, and new books will be used for W & M Corporation. The following

additional information is available:

1) The estimated fair values of the assets follow:

2)All assets and liabilities are transferred to the corporation.

3) The common stock is $10 par. Wilfred and Mike receive a total of 10,000 shares.

4) The partners share profits and losses in the ratio 7:3.

Based on the preceding information, the journal entry on W & M Corporation’s books

to record the assets and the issuance of the common stock will include a credit to

Additional Paid-In Capital for:

A. $0.

B. $81,000.

C. $31,000.

D. $50,000.

On December 31, 20X9, Rudd Company acquired 80 percent of the common stock of

Wilton Company. At the time, Rudd held land with a book value of $100,000 and a fair

value of $260,000; Wilton held land with a book value of $50,000 and fair value of

$600,000. Using the parent company theory, at what amount would land be reported in

a consolidated balance sheet prepared immediately after the combination?

A. $550,000

B. $590,000

C. $700,000

D. $860,000

The transactions listed in the following questions occurred in a private, not-for-profit

hospital during 20X8. For each transaction, indicate its effect on the hospital’s statement

of operations for the year ended December 31, 20X8.

Transaction: Depreciation expense was recorded for the year.

Effect on Statement of Operations:

A. Increases operating income.

B. Decreases operating income.

C. The transaction is reported on the statement of operations, but there is no effect on

operating income.

D. The transaction is not reported on the statement of operations.

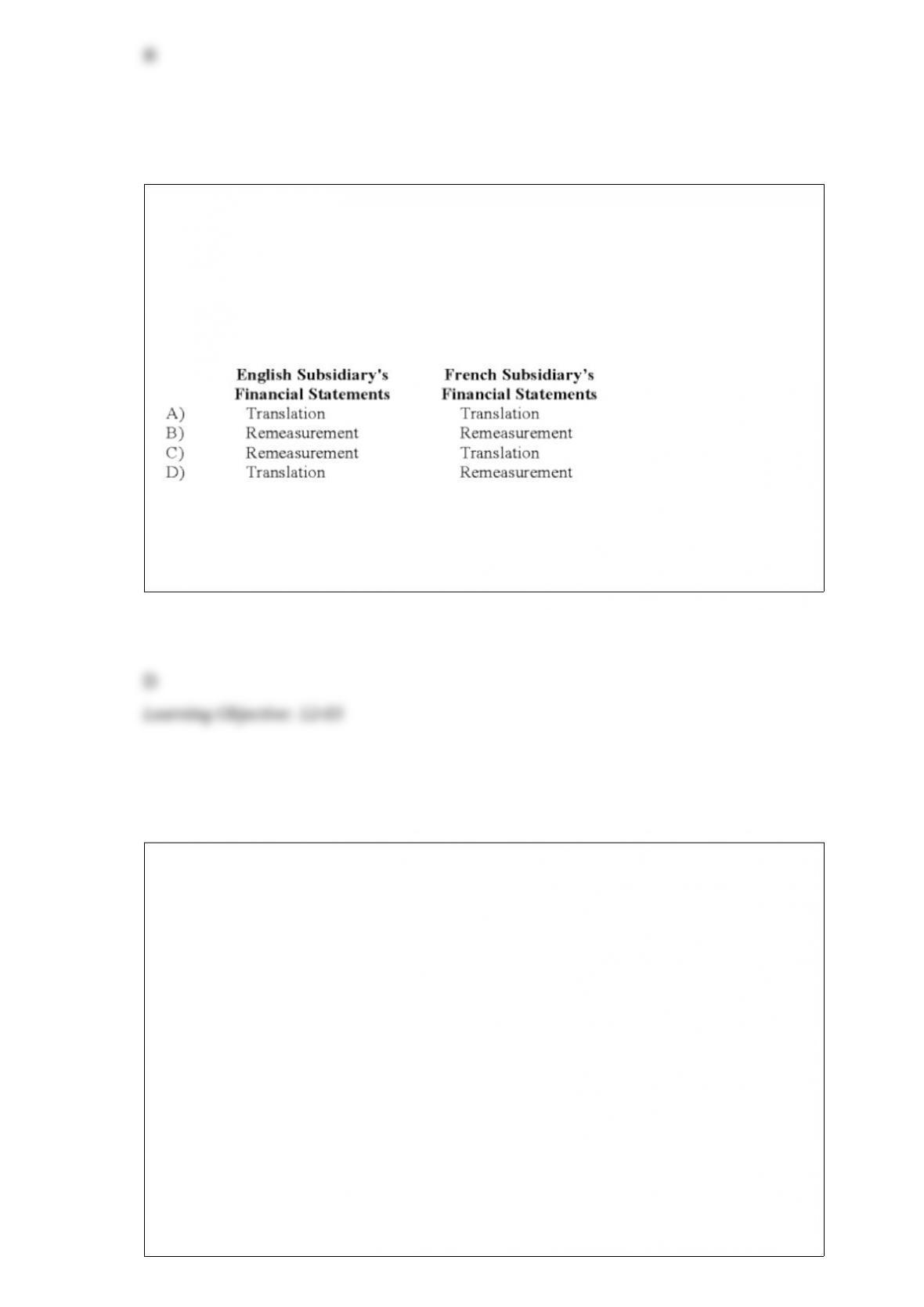

Simon Company has two foreign subsidiaries. One is located in France, the other in

England. Simon has determined the U.S. dollar is the functional currency for the French

subsidiary, while the British pound is the functional currency for the English subsidiary.

Both subsidiaries maintain their books and records in their respective local currencies.

What methods will Simon use to convert each of the subsidiary’s financial statements

into U.S. dollars?

A. Option A

B. Option B

C. Option C

D. Option D

Mom Corporation acquired 75 percent of Daughter Company’s voting shares on

January 1, 20X7, at underlying book value. On December 31, 20X7, it also purchased

$300,000 par value 9 percent Daughter bonds, which had been issued on January 1,

20X3 to Parry Corporation (unaffiliated with either Mom or Daughter) at a $20,000

premium. The bonds were originally issued with a 10-year maturity and pay interest

annually on December 31. During preparation of the consolidated financial statements

for December 31, 20X7, the following consolidation entry was included in the

consolidation worksheet:

Bonds Payable 300,000

Bond Premium 11,902

Loss on Bond Retirement 12,098

Investment in Daughter Company Bonds 324,000

Based on the information given above, what price did Mom pay to purchase the

Daughter bonds?

A. $324,000

B. $312,098

C. $311,902

D. $300,000

On October 15, 20X1, Jerry Company sold inventory to Garcia Corporation, its

Mexican subsidiary. The goods cost Jerry $2,700 and were sold to Garcia for $3,500,

payable in Mexican pesos. The goods are still on hand at the end of the year on

December 31. The Mexican peso is the functional currency of Garcia. The exchange

rates follow:

October 15 1 peso = $0.07

December 31 1 peso = $0.08

Based on the preceding information, at what amount is the inventory shown on the

consolidated balance sheet for the year?

A. $2,700

B. $3,200

C. $3,500

D. $4,000

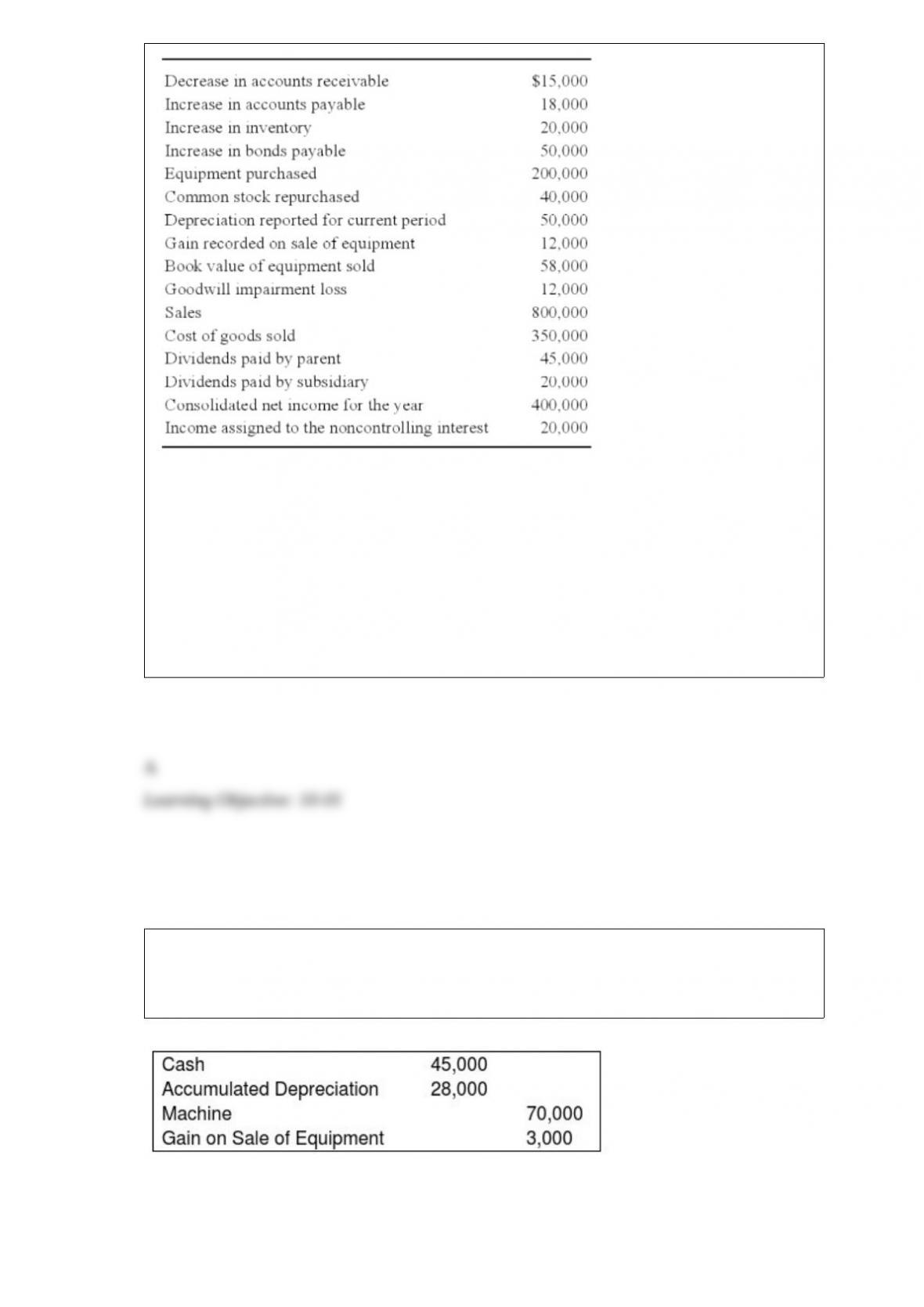

New Life Corporation has just finished preparing a consolidated balance sheet, income

statement, and statement of changes in retained earnings for 20X9. The following items

are proposed for inclusion in the consolidated cash flow statement:

New Life holds 75 percent of the voting stock of Shane Pharmaceuticals, acquired at

book value on June 21, 20X6. On the date of the acquisition, the fair value of the

noncontrolling interest was equal to 25 percent of the book value of Shane.

Based on the preceding information, what amount will be reported in the consolidated

cash flow statement as net cash used in financing activities for 20X9?

A. $40,000

B. $55,000

C. $90,000

D. $10,000

On January 1, 20X7, Servant Company purchased a machine with an expected

economic life of five years. On January 1, 20X9, Servant sold the machine to Master

Corporation and recorded the following entry:

Master Corporation holds 75 percent of Servant’s voting shares. Servant reported net

income of $50,000, and Master reported income from its own operations of $100,000 for

20X9. There is no change in the estimated economic life of the equipment as a result of the

intercorporate transfer.

Based on the preceding information, income assigned to the noncontrolling interest in the

20X9 consolidated income statement will be:

A. $12,000.

B. $14,000.

C. $12,500.

D. $48,000.

Which of the following usually does not represent a variable interest?

A. Common stock, with no special features or provisions

B. Senior debt

C. Subordinated debt

D. Loan or asset guarantees

A private, not-for-profit hospital uses a fund structure which includes a general fund

and donor restricted funds. Contributions received from donors for research to be

conducted by the hospital should be accounted for in the:

A. specific purpose fund.

B. time-restricted fund.

C. general fund.

D. restricted current fund.

Goshen City acquires $36,000 of inventory on November 1, 20X5, having held no

inventory previously. On December 31, 20X5, the end of Goshen City’s fiscal year, a

physical count shows $7,000 still in stock. During 20X6, $5,000 of this inventory is

used, resulting in a $2,000 remaining balance of supplies on December 31, 20X6.

Based on the preceding information, which of the following would be the correct

account balances for 20X6 if Goshen City used the purchase method of accounting for

inventories?

Expenditures Inventory of Supplies

A. $0 $2,000

B. $0 $7,000

C. $5,000 $2,000

D. $7,000 $2,000

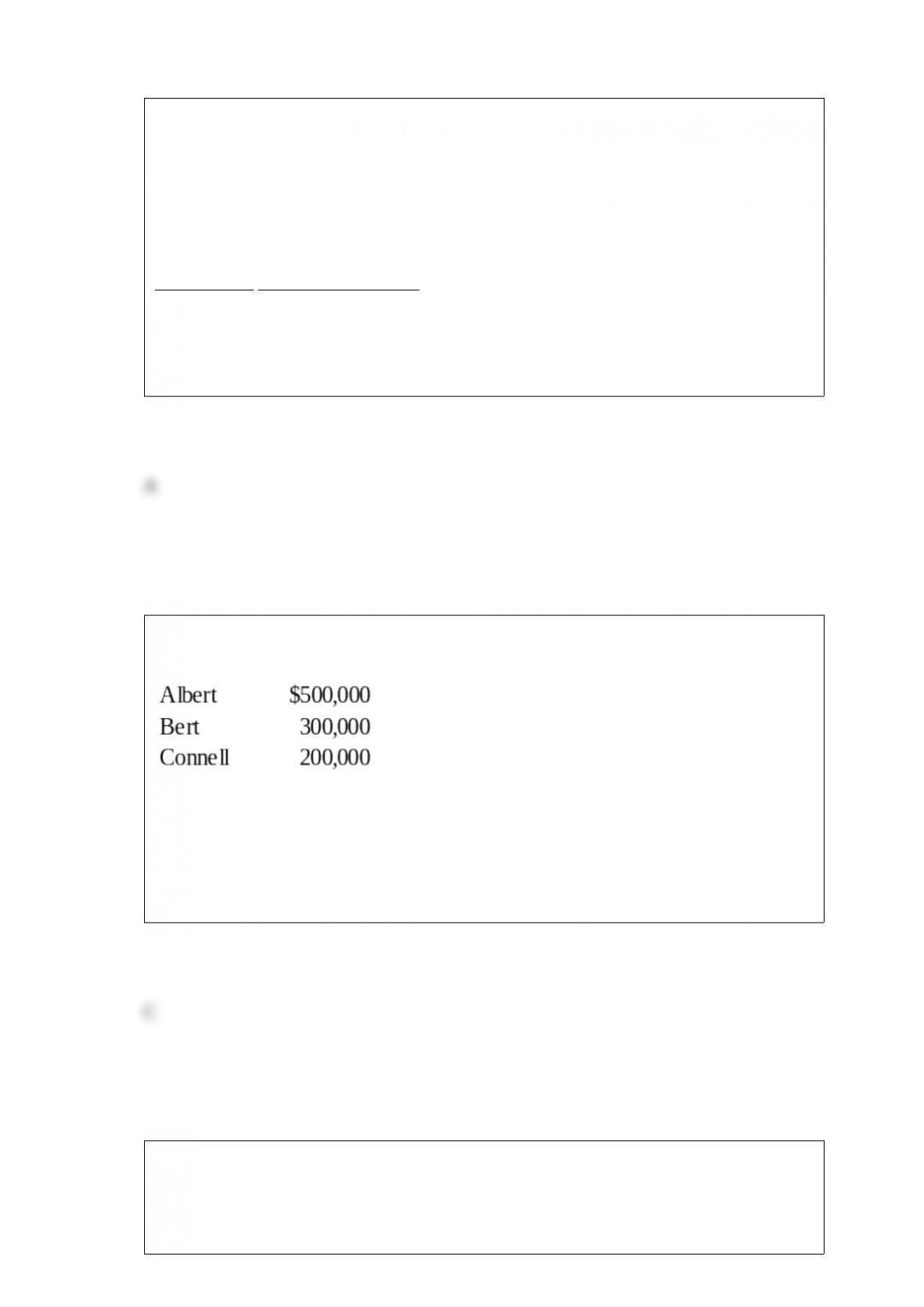

In the ABC partnership (to which Daniel seeks admittance), the capital balances of

Albert, Bert, and Connell, who share income in the ratio of 5:3:2 are:

Based on the preceding information, what amount of goodwill will be recorded if

Daniel invests $450,000 for a one-third interest?

A. $0

B. $10,000

C. $50,000

D. $100,000

Autumn Corporation acquired 90 percent of the stock of Spring Company on January 1,

20X2, for $360,000. At that date, the fair value of the noncontrolling interest was

$40,000. Spring’s balance sheet contained the following amounts at the time of the

combination:

Cash $20,000 Accounts Payable $25,000

Accounts Receivable 60,000 Bonds Payable 75,000

Inventory 70,000 Common Stock 100,000

Buildings and Equipment (net) 350,000 Retained Earnings 300,000

Total Assets $500,000 Total Liabilities & Equity $500,000

During each of the next three years, Spring reported net income of $70,000 and paid

dividends of $20,000. On January 1, 20X4, Autumn sold 3,000 shares of Spring’s $5

par value shares for $90,000 in cash. Autumn used the fully adjusted equity method in

accounting for its ownership of Spring Company.

Based on the preceding information, in the journal entry recorded by Autumn for the

sale of shares

A. Cash will be credited for $90,000.

B. Investment in Spring Stock will be credited for $90,000.

C. Investment in Spring Stock will be credited for $75,000.

D. Additional Paid-in Capital will be credited for $9,000.

In the LMN partnership, Lynn’s capital is $60,000, Marty’s is $80,000, and Nancy’s is

$70,000. They share income in a 4:3:3 ratio, respectively. Nancy is retiring from the

partnership. Each of the following questions is independent of the others.

Refer to the information above. Nancy is paid $84,000, and no goodwill is recorded. In

the journal entry to record Nancy’s withdrawal

A. Lynn, Capital will be debited for $7,000

B. Marty, Capital will be debited for $6,000

C. Nancy, Capital will be credited for $70,000

D. Cash will be debited for $84,000

Which rule-making body is currently setting standards of financial reporting for private

not-for-profit universities and for public (governmental) universities?

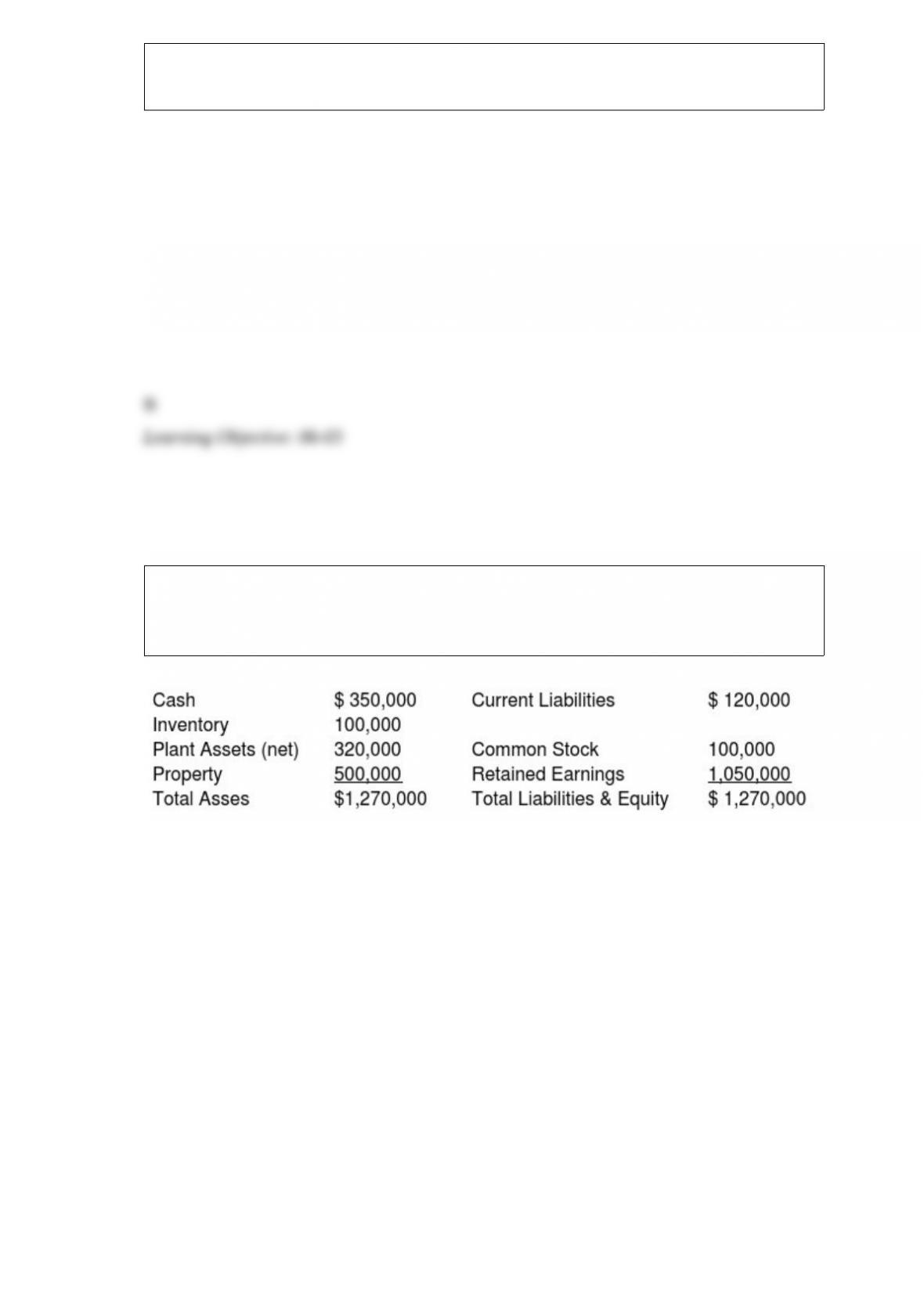

Partners David and Goliath have decided to liquidate their business. The following

information is available:

Cash $100,000

Inventory $200,000

$300,000

Accounts Payable $80,000

David, Capital $140,000

Goliath, Capital $80,000

$300,000

David and Goliath share profits and losses in a 3:1 ratio, respectively. During the first

month of liquidation, half the inventory is sold for $70,000, and $50,000 of the

accounts payable are paid. During the second month, the rest of the inventory is sold for

$55,000, and the remaining accounts payable are paid. Cash is distributed at the end of

each month, and the liquidation is completed at the end of the second month.

Refer to the information provided above. How much cash will be distributed to Goliath

at the end of the second month?

A. $11,250

B. $13,750

C. $20,000

D. $25,000

Based on the information given above, what amount of cost of goods sold did Sink

record in 20X4?

A. $1,612,000

B. $2,418,000

C. $2,790,000

D. $3,596,000

Parent Company acquired 90% of Son Inc. on January 31, 20X2 in exchange for cash.

The book value of Son’s individual assets and liabilities approximated their

acquisition-date fair values. On the date of acquisition, Son reported the following:

During the year Son Inc. reported $310,000 in net income and declared $15,000 in

dividends. Parent Company reported $520,000 in net income and declared $25,000 in

dividends. Parent accounts for their investment using the equity method.

Required:

1. What journal entry will Parent make on the date of acquisition to record the

investment in Son Inc.?

2. If Parent were to prepare a consolidated balance sheet on the acquisition date

(January 31, 20X2), what is the basic consolidation entry Parent would use in the

consolidation worksheet?

3. What is Parent’s balance in “Investment in Son Inc.” prior to consolidation on

December 31, 20X2?

4. What is the basic consolidation entry Parent would use in the consolidation

worksheet on December 31, 20X2?

Problem 47 (continued):

Pone Company purchased 100 percent of Sone Inc. on January 1, 20X9 for $625,000.

Sone reported earnings of $76,000 and declared dividends of $8,000 during 20X9.

Based on the preceding information and assuming Pone uses the cost method to account

for its investment in Sone, what is the balance in Pone’s Investment in Sone account on

December 31, 20X9, prior to consolidation?

A. $617,000

B. $625,000

C. $633,000

D. $693,000

The SRT partnership agreement specifies that partnership net income be allocated as

follows:

Partner S Partner R Partner T

Salary allowance $20,000 $25,000 $15,000

Interest on average capital balance 10% 10% 10%

Remainder 30% 30% 40%

Average capital balances for the current year were $60,000 for S, $50,000 for R, and

$40,000 for T.

Refer to the information given. Assuming a current year net income of $125,000, what

amount should be allocated to each partner?

Partner S Partner R Partner T

A. $15,000 $15,000 $20,000

B. $37,500 $37,500 $50,000

C. $41,000 $45,000 $39,000

D. $42,000 $48,000 $35,000

Private Not-For-Profit (NFP) Entities.

Select from this list of terms to answer the following questions.

Indicate your choice by entering the letter corresponding to the correct term. A term

may be used more than once or not at all.

”Classification of an endowment contribution” describes which term listed above?

On January 1, 20X8, Line Corporation acquired all of the common stock of Staff

Company for $300,000. On that date, Staff’s identifiable net assets had a fair value of

$250,000. The assets acquired in the purchase of Staff are considered to be a separate

reporting unit of Line Corporation. The carrying value of Staff’s investment at

December 31, 20X8, is $310,000. The fair value of the net assets (excluding goodwill)

at that date is $220,000 and the fair value of the reporting unit is determined to be

260,000.

Required:

1) Explain how goodwill is tested for impairment for a reporting unit.

2) Determine the amount, if any, of impairment loss to be recognized at December 31,

20X8.

Based on the information given above, what amount of sales will be reported in the

consolidated income statement for 20X3?

A. $725,000

B. $750,000

C. $875,000

D. $950,000

In the JK partnership, Jacob’s capital is $140,000, and Katy’s is $40,000. They share

income in a 3:2 ratio, respectively. They decide to admit Erin to the partnership. Each of

the following questions is independent of the others.

Refer to the information provided above. Erin invests $52,000 for a one-fifth interest.

What amount of goodwill will be recorded?

A. $7,000

B. $28,000

C. $50,000

D. $80,000

To obtain cash quickly, DebCo. sold $750,000 of its receivables to Finco., with

recourse. As the accountant for DebCo., what issues do you need to resolve in order to

determine the appropriate accounting treatment?

Based on the information given above, what amount of cost of goods sold did Pink

record in 20X4?

A. $1,612,000

B. $2,418,000

C. $2,790,000

D. $3,596,000

On January 1, 20X4, Timber Company acquired 25% of Johnson Company’s common

stock at underlying book value of $200,000. Johnson has 80,000 shares of $10 par

value, 6 percent cumulative preferred stock outstanding. No dividends are in arrears.

Johnson reported net income of $270,000 for 20X4 and paid total dividends of

$140,000. Timber uses the equity method to account for this investment.

Based on the preceding information, what amount of investment income will Timber

Company report from its investment in Johnson for the year?

A. $140,000

B. $67,500

C. $55,500

D. $35,000

Peanut Company acquired 75 percent of Snoopy Company’s stock at underlying book

value on January 1, 20X8. At that date, the fair value of the noncontrolling interest was

equal to 25 percent of the book value of Snoopy Company. Snoopy Company reported

shares outstanding of $350,000 and retained earnings of $100,000. During 20X8,

Snoopy Company reported net income of $60,000 and paid dividends of $3,000. In

20X9, Snoopy Company reported net income of $90,000 and paid dividends of

$15,000. The following transactions occurred between Peanut Company and Snoopy

Company in 20X8 and 20X9:

Snoopy Co. sold equipment to Peanut Co. for a $42,000 gain on December 31, 20X8.

Snoopy Co. had originally purchased the equipment for $140,000 and it had a carrying

value of $28,000 on December 31, 20X8. At the time of the purchase, Peanut Co.

estimated that the equipment still had a seven-year remaining useful life.

Peanut sold land costing $90,000 to Snoopy Company on June 28, 20X9, for $110,000.

Required:

Give all consolidating entries needed to prepare a consolidation worksheet for 20X9

assuming that Peanut Co. uses the cost method to account for its investment in Snoopy

Company.