Chapter 01 – INTERCORPORATE ACQUISITIONS AND INVESTMENTS IN OTHER ENTITIES

DESCRIPTIONS OF CASES, EXERCISES, AND PROBLEMS

C1-1

35 min.

LO 1-2,

LO 1-5

M

Assignment of Acquisition Costs

Students must research the current authoritative accounting standards as well as

any FASB proposals regarding the treatment of acquisition costs and report their

findings.

C1-2

15 min.

LO 1-1,

LO 1-3

M

Evaluation of a Merger

Students are asked to explain the funding of an acquisition as well as the impact

on receivables and inventory.

C1-3

15 min.

LO 1-4

M

Business Combinations

Students must identify and evaluate tax incentives and other economic factors

associated with the frequency of business combinations since the 1960s.

C1-4

25 min.

LO 1-5

E

Determination of Goodwill Impairment

Students must research the authoritative literature regarding impairment testing

of goodwill. Students must report their findings and explain the type of tests

used to determine whether goodwill has been impaired and provide some

example that would indicate possible goodwill impairment.

C1-5

25 min.

LO 1-1

E

Risks Associated with Acquisitions

Students must discuss the risks that Google sees inherent in potential acquisitions

after researching the information provided by the company to investors about its

motivation for acquiring companies and the possible risks associated with such

acquisitions.

C1-6

20 min.

LO 1-1

E

Numbers Game

Students must read Arthur Levitt’s speech “The Numbers Game” and explain the

motivations and techniques for earnings management, as well as the significance

of the issue.

C1-7

20 min.

LO 1-1,

LO 1-4

M

MCI: A Succession of Mergers

Students are asked to look at the primary business activities and growth strategies

of MCI WorldCom, Inc. They should trace the major acquisitions leading to MCI

WorldCom and indicate the type of consideration used in the acquisitions. Some

specific information is required.

Chapter 01 – INTERCORPORATE ACQUISITIONS AND INVESTMENTS IN OTHER ENTITIES

C1-8

25 min.

LO 1-4

M

Leveraged Buyouts

Students must explain a leveraged buyout and contrast it with a management

buyout. They must identify authoritative pronouncements and the major issue

involved in determining proper basis for an interest in an LOB acquired company.

E1-1

20 min.

LO 1-1, LO

1-3, LO 1-5

M

Multiple-Choice Questions on Complex Organizations

A set of 5 multiple-choice questions testing students’ understanding of complex

business organizations.

E1-2

20 min.

LO1-2, LO

1-5

E

Multiple-Choice Questions on Recording Business Combinations

[AICPA Adapted] A set of five multiple-choice questions test students’ basic

understanding of recording business combinations.

E1-3

13 min.

LO 1-2,

LO 1-5

M

Multiple-Choice Questions on Reported Balances

[AICPA Adapted] Four multiple-choice questions cover the computation of

stockholders’ equity and asset balances for the combined entity following a

business combination.

E1-4

13 min.

LO 1-2,

LO 1-5

M

Multiple-Choice Questions Involving Account Balances

Five multiple-choice questions cover the computation of account balances and

related journal entries after a business combination.

E1-5

20 min.

LO 1-3

E

Asset Transfer to Subsidiary

Students are asked to show the journal entries made by the parent and subsidiary

for the transfer of assets to the subsidiary.

E1-6

15 min.

LO 1-3

E

Creation of New Subsidiary

Students are asked to show the journal entries made by the parent and the

subsidiary for the transfer of assets to the subsidiary.

Chapter 01 – INTERCORPORATE ACQUISITIONS AND INVESTMENTS IN OTHER ENTITIES

E1-7

15 min.

LO 1-2,

LO 1-3

E

Balance Sheet Totals of Parent Company

Journal entries are required for transfer of assets and accounts payable between a

parent company and its newly created subsidiary. Both the parent and subsidiary

journal entries must be made.

E1-8

12 min.

LO 1-2,

LO 1-5

M

Acquisition of Net Assets

Students are required to show the journal entries that the parent must make at time

of acquisition.

E1-9

20 min.

LO 1-5

M

Reporting Goodwill

Students must calculate goodwill to be reported under different acquisition prices.

E1-10

10 min.

LO 1-5

E

Stock Acquisition

Students must show the journal entry that the acquiring company must record

when it issues stock for acquiring a subsidiary.

E1-11

20 min.

LO 1-5

M

Balances Reported Following Combination

Students must calculate seven balances for balance sheet accounts immediately

following a business combination.

E1-12

15 min.

LO 1-5

E

Goodwill Recognition

Students must show the journal entry to be made by the acquiring company in

recording a business combination involving goodwill.

E1-13

15 min.

LO 1-5

M

Acquisition Using Debentures

Students must show the journal entry to be made by the acquiring company in

recording a business combination executed using debentures.

E1-14

15 min.

LO 1-5

M

Bargain Purchase

Students must show the journal entry to be made by the acquiring company in

recording a business combination involving gain on bargain purchase.

E1-15

20 min.

LO 1-5

M

Impairment of Goodwill

Students must calculate goodwill and potential impairment of goodwill given

three different fair value amounts.

Chapter 01 – INTERCORPORATE ACQUISITIONS AND INVESTMENTS IN OTHER ENTITIES

E1-16

15 min.

LO 1-5

M

Assignment of Goodwill

Students must calculate potential impairment of goodwill given three different

fair value amounts.

E1-17

20 min.

LO 1-5

M

Goodwill Assigned to Reporting Units

Students must calculate reported goodwill for a company, based on information

for four different reporting units.

E1-18

15 min.

LO 1-5

E

Goodwill Measurement

Students must calculate goodwill and potential impairment of goodwill given

four different fair value amounts.

E1-19

20 min.

LO 1-5

M

Computation of Fair Value

Students must calculate the fair value of buildings and equipment, given the cost

of acquisition, the fair value of other assets and liabilities, and the book value of

the building and equipment.

E1-20

20 min.

LO 1-5

M

Computation of Shares Issued and Goodwill

Students must determine the number of shares issued, the par value of the

acquiring company’s stock, and any goodwill arising from the business

combination.

E1-21

15 min.

LO 1-5

M, Ws

Combined Balance Sheet

Students must prepare a balance sheet of the combined company immediately

following the acquisition.

E1-22

20 min.

LO 1-5

M

Recording a Business Combination

Students must show the journal entries made by acquiring company given

financial statement information for both companies and market value of the

acquiring company’s common stock.

E1-23

15 min.

LO 1-5

M

Reporting Income

Students must compute net income and earnings-per-share reported in

comparative income statement for two years.

P1-24

10 min.

LO 1-3

E

Assets and Accounts Payable Transferred to Subsidiary

Students must show journal entries recorded for transfer of assets and liabilities

to the newly established subsidiary.

P1-25

10 min.

LO 1-3

E

Creation of New Subsidiary

Students must show journal entries made for the transfer of assets and liabilities

to a newly created entity.

Chapter 01 – INTERCORPORATE ACQUISITIONS AND INVESTMENTS IN OTHER ENTITIES

P1-26

25 min.

LO 1-3

M

Incomplete Data on Creation of Subsidiary

Students must calculate book value, reported amounts, reported shares, impact on

balance sheet amounts.

P1-27

20 min.

LO 1-5

M

Acquisition in Multiple Steps

Students must prepare journal entries for the completion of the acquisition of

additional shares of a previously owned company.

P1-28

15 min.

LO 1-5

M

Journal Entries to Record a Business Combination

Students must show the journal entries made to record a business combination in

which the acquiring company issues shares of common stock.

P1-29

15 min.

LO 1-5

M

Recording Business Combinations

Students must show the journal entries made to record a business combination in

which the acquiring company issues shares of common stock.

P1-30

30 min.

LO 1-5

E, Ws

Business Combination with Goodwill

Students must show the journal entry to be recorded by the acquiring company

and the balance sheet following the business combination.

P1-31

15 min.

LO 1-5

M

Bargain Purchase

Students must show the journal entry to be made by the acquiring company in

recording a business combination involving gain on bargain purchase.

P1-32

15 min.

LO 1-5

M

Computation of Account Balances

Calculation of liability balance and fair value is required with simultaneous

consideration of potential goodwill impairment.

P1-33

25 min.

LO 1-5

H

Goodwill Assigned to Multiple Reporting Units

Calculation of goodwill and potential goodwill impairment for multiple reporting

units in a company are required.

P1-34

15 min.

LO 1-5

M

Journal Entries

Students must show journal entries recorded by acquiring company for a business

combination. Costs of combination must be considered.

P1-35

30 min.

LO 1-5

M, Ws

Purchase at More than Book Value

Students must show journal entries to record a business combination and prepare

a balance sheet immediate after the business combination.

P1-36

25 min.

LO 1-5

Business Combination

Journal entries recorded by the acquiring company to record the business

combination. Several account balances must be adjusted.

Chapter 01 – INTERCORPORATE ACQUISITIONS AND INVESTMENTS IN OTHER ENTITIES

M

P1-37

30 min.

LO 1-5

H

Combined Balance Sheet

The balance sheet following the business combination is required. Stockholders’

equity balances are required assuming three different levels of stock are issued by

the acquiring company in completing the business combination.

P1-38

30 min.

LO 1-5

M

Incomplete Data

Balance sheet information for two separate entities and for the combined entity

immediate after a business combination is given. Students must calculate the

number of shares issued, market value of shares, fair value of inventory held by

the acquired company, acquired company’s net assets, goodwill arising from the

combination, retained earnings balance after combination, and depreciation

expense for the first year on the acquired company’s depreciable assets.

P1-39

30 min.

LO 1-5

M

Incomplete Data Following Purchase

Balance sheet information for two separate entities and for the combined entity

immediate after a business combination is given. Students must calculate the

number and price of shares issued, the amount of cash paid as stock issuance

costs, market value of shares issued on date of combination, cash paid for stock

issue costs, market value of shares issued, the fair value of inventory and net

assets, and the amount of goodwill to be reported.

P1-40

40 min.

LO 1-5

M

Comprehensive Business Combination

Students are given a comprehensive set of financial statements with book values

and fair values. They are required to prepare all journal entries on the acquiring

company’s books related to the business combination. Next they are asked to

present the entries that would have been entered on the acquired company’s

books.

Chapter 01 – INTERCORPORATE ACQUISITIONS AND INVESTMENTS IN OTHER ENTITIES

OTHER RESOURCES

Chapter 1

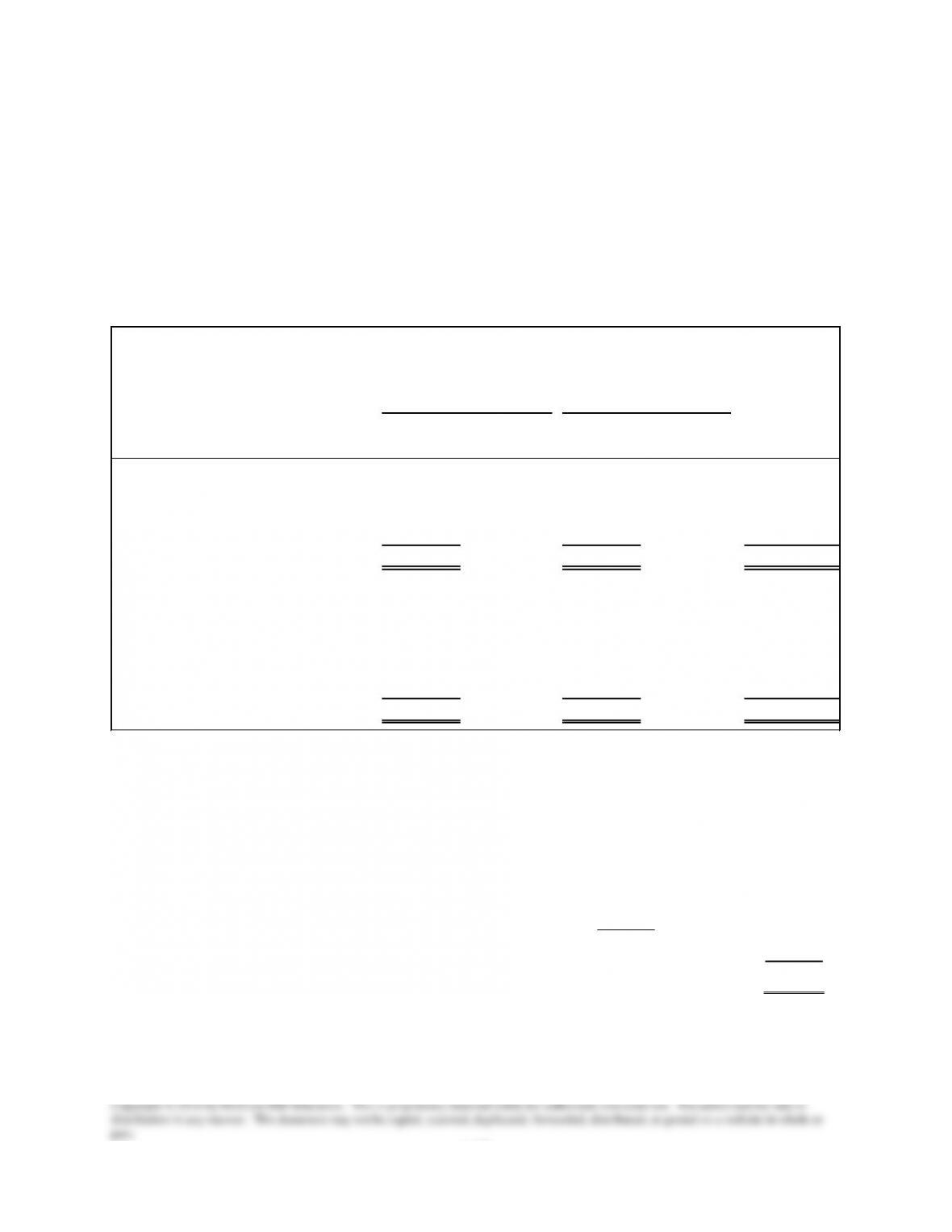

Business Combination Illustration

On January 1, 20X9, Aggressive Co. acquired all the common shares of Docile Corp. by issuing

common shares. Aggressive Co. issued shares with a par value of $15,000 and a market value of

$90,000 in completing the acquisition.

COMPUTATION OF GOODWILL

Fair Value of Shares issued by Aggressive Co.

$90,000

Fair Value of Docile Corp. Assets

$150,000

Fair Value of Docile Corp. Liabilities

(72,000)

Fair Value of Docile Corp. Net Assets

(78,000)

Goodwill

$12,000

Combined

Book Fair Book Fair Combined

Value Value Value Value Value

Cash $50,000 $50,000 $20,000 $20,000 $70,000

Inventory 50,000 70,000 40,000 50,000 100,000

Building & Equipment(net) 300,000 350,000 60,000 80,000 380,000

Goodwill 12,000

TOTAL ASSETS $400,000 $120,000 $562,000

Current Liabilities $25,000 $25,000 $40,000 $40,000 $65,000

Bonds Payable 75,000 76,500 30,000 32,000 107,000

Capital Stock 200,000 20,000 215,000

Additional Paid-In Capital 30,000 10,000 105,000

Retained Earnings 70,000 20,000 70,000

TOTAL LIABILITIES AND S.E $400,000 $120,000 $562,000

Balance Sheet Data

of Individual Companies

Aggressive Co.

Docile Corp.