Archives

Accounting Chapter 1 Has Regulatory Mandate And Enforcement

4. Explain the need for high-quality standards. 5. Identify the objective of financial reporting. 6. Identify the major policy-setting bodies and their role in the standard-setting process. 7. Explain the meaning of IFRS. 8. Describe the challenges facing financial reporting. […]

Accounting Chapter 1 The Financial Statements Most Frequently Provided

CHAPTER 1 FINANCIAL REPORTING AND ACCOUNTING STANDARDS CHAPTER LEARNING OBJECTIVES 1. Describe the growing importance of global financial markets and their relation to financial reporting. 2. Explain the objective of financial reporting. 3. Identify the major policy-setting bodies and their […]

Accounting Chapter 1 The Foundation Selects The Members The

CHAPTER 1 Financial Reporting and Accounting Standards ASSIGNMENT CLASSIFICATION TABLE Topics Questions Concepts for Analysis 1. Global markets and financial reporting. 1, 2, 3, 4 4 2. Objective of financial reporting. 5, 6, 7, 8, 9, 10 2, 3 3. […]

Accounting Chapter 10 Capitalization Should Occur Only The Benefits Exceed

PROBLEM 10.8 (Continued) 3. Holyfield SA Machinery ……………………………………………………… 95,000 Accumulated Depreciation—Machinery …………… 60,000 Loss on Disposal of Machinery ……………………….. 8,000 Machinery ………………………………………………. 160,000 Cash ………………………………………………………. 3,000 Liston Company Machinery ……………………………………………………… 92,000 Accumulated Depreciation—Machinery …………… 75,000 Cash ……………………………………………………………… 3,000 Machinery ………………………………………………. […]

Accounting Chapter 10 Computation of Weighted-Average Accumulated

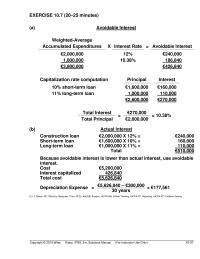

EXERCISE 10.7 (20–25 minutes) (a) Avoidable Interest Weighted-Average Accumulated Expenditures X Interest Rate = Avoidable Interest €2,000,000 12% €240,000 1,800,000 10.38% 186,840 €3,800,000 €426,840 Capitalization rate computation Principal Interest 10% short-term loan €1,600,000 €160,000 11% long-term loan 1,000,000 110,000 €2,600,000 […]

Accounting Chapter 10 Land 299250 Warehouse 192375 Office Building

CHAPTER 10 ACQUISITION AND DISPOSITION OF PROPERTY, PLANT, AND EQUIPMENT CHAPTER LEARNING OBJECTIVES 1. Identify property, plant, and equipment and its related costs. 2. Discuss the accounting problems associated with interest capitalization. 3. Explain accounting issues related to acquiring and […]

Accounting Chapter 10 Lobos Statement Financial Position Investment Land The

EXERCISE 10.24 (15–20 minutes) 1/30 Accumulated Depreciation—Buildings …………………….. 95,200* Loss on Disposal of Machinery ………………………….. 21,900** Buildings ………………………………………………………. 112,000 Cash ………………………………………………………. 5,100 *(5% X $112,000 = $5,600; $5,600 X 17 = $95,200) **($112,000 – $95,200) + $5,100 3/10 Cash ($2,900 […]

Accounting Chapter 10 Requires That Grants Used Acquire Property

1. Identify property, plant, equipment, and its related costs. 3. Explain accounting issues related to acquiring and valuing plant assets. Copyright © 2018 John Wiley &Sons, Inc. Kieso Intermediate: IFRS 3e, Instructor’s Manual 10-1 5. Describe the accounting treatment for […]

Accounting Chapter 10 Purchase of equipment with zero-interest-bearing

CHAPTER 10 Acquisition and Disposition of Property, Plant, and Equipment ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Valuation and classification of land, buildings, and equipment. 1, 2, 3, 5, 6, 11, 12, […]

Accounting Chapter 11 Comparative Analysis Case Continued 2 Profit Margin

COMPARATIVE ANALYSIS CASE (Continued) (2) Profit margin on sales: Puma adidas €61.7 = 1.82% €640 = 3.78% €3,387.4 €16,915 (3) Return on assets: Puma adidas €61.7 =2.39% €640 = 4.97% €2,549.9 + €2,620.3 €12,417 + €13,343 2 2 Each of […]

Accounting Chapter 11 Depreciation Not Taken Assets Intended Sold C

EXERCISE 11.6 (Continued) 2nd full year [25% X ($304,000 – $76,000)] = $57,000 2019 Depreciation 3/12 X $76,000 = $19,000 2020 Depreciation 9/12 X $76,000 = $57,000 3/12 X $57,000 = 14,250 $71,250 LO: 1,2, Bloom: AP, Difficulty: Moderate, Time: […]

Accounting Chapter 11 Normally Assets Not Used Productive Capacity Held

4. Discuss the accounting procedures for depletion of mineral resources. 5. Apply the accounting for revaluations. 5. Demonstrate how to report and analyze property, plant, equipment, and mineral resources. *7. Illustrate revaluation accounting procedures. *This material is covered in an […]

Accounting Chapter 11 The 2019 Income Statement Will Report Loss

CHAPTER 11 DEPRECIATION, IMPAIRMENTS, AND DEPLETION CHAPTER LEARNING OBJECTIVES 1. Describe depreciation concepts and methods of depreciation. 2. Identify other depreciation issues. 3. Explain the accounting issues related to asset impairment. 4. Discuss the accounting procedures for depletion of mineral […]

Accounting Chapter 11 The amounts to be recorded on the books

PROBLEM 11.2 Depreciation Expense 2019 2020 (a) Straight-line: (€89,000 – €5,000) ÷ 7 = €12,000/yr. 2019: €12,000 X 7/12 €7,000 2020: €12,000 €12,000 (b) Units-of-output: (€89,000 – €5,000) ÷ 525,000 units = €.16/unit 2019: €.16 X 55,000 8,800 2020: €.16 […]

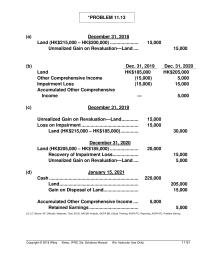

Accounting Chapter 11 Unrealized Gain on Revaluation—Equipment

*PROBLEM 11.13 (a) December 31, 2018 Land (HK$215,000 – HK$200,000) …………………. 15,000 Unrealized Gain on Revaluation—Land …. 15,000 (b) Dec. 31, 2019 Dec. 31, 2020 Land HK$185,000 HK$205,000 Other Comprehensive Income (15,000) 5,000 Impairment Loss (15,000) 15,000 Accumulated Other Comprehensive […]

Accounting Chapter 12 Cost Trademark Net Amortization Copyright 2018

EXERCISE 12.12 (20–25 minutes) Net assets of Terrell as reported ($575,000 – $350,000) …………………………………………. $225,000 Adjustments to fair value Increase in land value …………………………………… 50,000 Decrease in equipment value ………………………… (5,000) 45,000 Net assets of Terrell at fair value …………………………… […]

Accounting Chapter 12 Factors to be considered in determining useful

CHAPTER 12 Intangible Assets ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Intangible assets; concepts, definitions; items comprising intangible assets. 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, […]

Accounting Chapter 12 Goodwill Trademarks And Other Intangible Assets Puma

CA 12.2 (Continued) The amount of interest cost for the first nine months of 2019 is part of the 2018 loss resulting from the tornado. The extension of the construction period to October 2019 because of the tornado does not […]

Accounting Chapter 12 Identify impairment procedures and presentation requirements

CHAPTER 12 INTANGIBLE ASSETS CHAPTER LEARNING OBJECTIVES 1. Discuss the characteristics valuation, and amortization of intangible assets. 2. Describe the accounting for various types of intangible assets. 3. Explain the accounting issues for recording goodwill. 4. Identify impairment procedures and […]

Accounting Chapter 12 The Company Intends And Has The Ability

3. Explain the accounting issues for recording goodwill. 4. Identify impairment issues and presentation requirements for intangible assets. 5. Describe the accounting and presentation for research and development and similar costs. CHAPTER 12 Intangible Assets LEARNING OBJECTIVES 1. Discuss the […]

Accounting Chapter 13 Accounting Analysis And Principles Continued

COMPARATIVE ANALYSIS CASE (Continued) 20 Other provisions Other provisions consist of the following: Other provisions (€ in millions) Jan.1, 2015 Currency translation differences Usage Reversals Additions Transfers Dec.31, 2015 There of non-current Marketing 79 0 (77) (0) 20 — 21 […]

Accounting Chapter 13 Because the cause for litigation occurred before

PROBLEM 13.2 December 5 1. Cash ………………………………………………………. 500 Returnable Deposit (Liability) ………………………….. 500 December 1–31 2. Cash ………………………………………………………. 798,000 Sales Revenue (€798,000 ÷ 1.05) ……………………… 760,000 Value-Added Taxes Payable (€760,000 X .05) ………………………….. 38,000 December 10 3. Trucks (€120,000 X […]

Accounting Chapter 13 Depreciation Expense 100000 And Interest Expense

CHAPTER 13 CURRENT LIABILITIES, PROVISIONS, AND CONTINGENCIES CHAPTER LEARNING OBJECTIVES 1. Describe the nature, valuation, and reporting of current liabilities. 2. Explain the accounting for different types of provisions. 3. Explain the accounting for loss and gain contingencies. 4. Indicate […]

Accounting Chapter 13 For Company Record Restructuring Costs And Related

2. Explain the accounting for different types of provisions. 3. Explain the accounting for loss and gain contingencies. 4. Indicate how to present and analyze liability-related information. CHAPTER 13 Current Liabilities, Provisions, and Contingencies LEARNING OBJECTIVES 1. Describe the nature, […]

Accounting Chapter 13 Premium entries and financial statement presentation

CHAPTER 13 Current Liabilities, Provisions, and Contingencies ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Concept of liabilities; definition and classification of current liabilities. 1, 2, 3, 4, 6, 8 1, 5 1, […]

Accounting Chapter 13 Time And Purpose Concepts For Analysis 131

TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS CA 13.1 (Time 20–25 minutes) Purpose—to provide the student with the opportunity to define a liability, to distinguish between current and non-current liabilities, and to explain accrued liabilities. The student must also describe […]

Accounting Chapter 13 To accrue the expense and liability for vacations

EXERCISE 13.6 (Continued) (b) Accrued liability at year-end: 2018 2019 Vacation Payable Sick Pay Payable Vacation Payable Sick Pay Payable Jan. 1 balance € 0 € 0 € 8,640 €1,728 + accrued 8,640 5,184 9,360 5,616 – paid (0) (3,456) […]

Accounting Chapter 14 A bond indenture is a contractual agreement

CHAPTER 14 Non-Current Liabilities ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Non-current liability; classification; definitions. 1, 10, 11, 19, 20, 22, 23, 24 1, 2 10 1, 2, 3 2. Issuance of […]

Accounting Chapter 14 Carrying value of the note at January 1

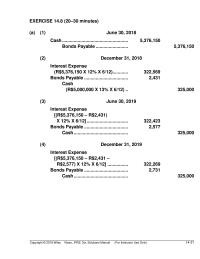

EXERCISE 14.8 (20–30 minutes) (a) (1) June 30, 2018 Cash ………………………………………………………. 5,376,150 Bonds Payable ………………………….. 5,376,150 (2) December 31, 2018 Interest Expense (R$5,376,150 X 12% X 6/12)………………………….. 322,569 Bonds Payable ………………………………………………………. 2,431 Cash (R$5,000,000 X 13% X 6/12) ………………………….. 325,000 […]

Accounting Chapter 14 For Example This Case Changes The Fair

COMPARATIVE ANALYSIS CASE (Continued) Using foreign debt to finance operations is subject to the risk of foreign currency exchange rate fluctuations. adidas enters into interest rate and foreign currency swaps to effectively change the interest rate and currency of specific […]

Accounting Chapter 14 Noncurrent Liabilities Learning Objectives Describe The

2. Explain the accounting for long-term notes payable. 3. Explain the accounting for the extinguishment of non-current liabilities. 4. Indicate how to present and analyze non-current liabilities. CHAPTER 14 Non-Current Liabilities LEARNING OBJECTIVES 1. Describe the nature of bonds and […]

Accounting Chapter 14 September 2019 Interest Expense Bonds Payable

PROBLEM 14.2 (Continued) Entry for accrued interest Interest Expense ($204,868 X 1/2 X 1/2) ……………………. 51,217 Bonds Payable ………………………………………………………. 1,283 Cash ($210,000 X 1/2 X 1/2) ………………………….. 52,500 Entry for reacquisition Bonds Payable ………………………………………………………. 1,023,055* Loss on Extinguishment of Debt […]

Accounting Chapter 14 The Amount Amortization The Difference Between Recognized

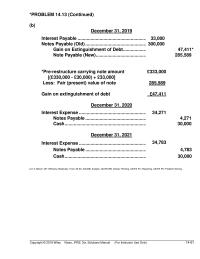

*PROBLEM 14.13 (Continued) (b) December 31, 2019 Interest Payable …………………………………………………….. 33,000 Notes Payable (Old) ……………………………………………….. 300,000 Gain on Extinguishment of Debt ……………………… 47,411* Note Payable (New) ………………………………………… 285,589 *Pre-restructure carrying note amount [(£330,000 – £30,000) + £33,000] Less: Fair (present) […]

Accounting Chapter 14 The Present Value The Note Was 1442000

CHAPTER 14 NON-CURRENT LIABILITIES CHAPTER LEARNING OBJECTIVES 1. Describe the Nature of bonds and indicate the accounting for bond issuances. 2. Explain the accounting for long-term notes payable. 3. Explain the accounting for the extinguishment of non-current liabilities. 4. Indicate […]

Accounting Chapter 15 December When The Market Price The Shares

CHAPTER 15 EQUITY CHAPTER LEARNING OBJECTIVES 1. Describe the corporate form and the issuance of shares. 2. Explain the accounting and reporting for treasury shares. 3. Explain the accounting and reporting issues related to dividends. 4. Indicate how to present […]

Accounting Chapter 15 fixed per share amount assigned to a share by

CHAPTER 15 Equity ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Shareholders’ rights; corporate form. 1, 2, 3 1 2. Equity. 4, 5, 6, 16, 17, 18 3 7, 10, 16, 17 1, […]

Accounting Chapter 15 Property Dividends 25 Property Dividends Kind

3. Explain the accounting and reporting issues related to dividends. 4. Indicate how to present and analyze equity. *5. Discuss the different type of preference share dividends and their effect on book value per share. *This material is covered in […]

Accounting Chapter 15 Some analysts use after-tax interest expense

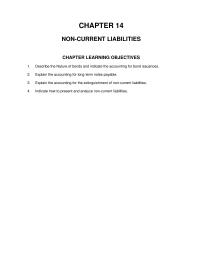

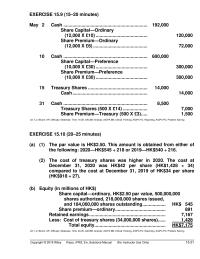

EXERCISE 15.9 (15–20 minutes) May 2 Cash ……………………………………………………….. 192,000 Share Capital—Ordinary (12,000 X £10) …………………………..…….. 120,000 Share Premium—Ordinary (12,000 X £6) …………………………………… 72,000 10 Cash ……………………………………………………….. 600,000 Share Capital—Preference (10,000 X £30) …………………………..…….. 300,000 Share Premium—Preference (10,000 X £30) …………………………..…….. […]

Accounting Chapter 15 The suggested cash dividend could be paid even

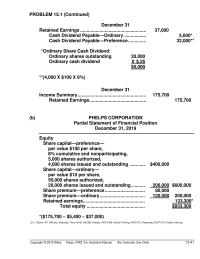

PROBLEM 15.1 (Continued) December 31 Retained Earnings …………………………………………… 37,000 Cash Dividend Payable—Ordinary …………….. 5,000* Cash Dividend Payable—Preference ………….. 32,000** *Ordinary Share Cash Dividend: Ordinary shares outstanding 20,000 Ordinary cash dividend X $.25 $5,000 **(4,000 X $100 X 8%) December 31 […]

Accounting Chapter 15 Unless There Are Specific Uses For The

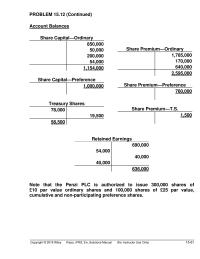

PROBLEM 15.12 (Continued) Account Balances Share Capital—Ordinary 850,000 50,000 200,000 54,000 1,154,000 Share Capital—Preference 1,000,000 1,785,000 170,000 640,000 2,595,000 Share Premium—Preference 760,000 Treasury Shares 78,000 19,500 58,500 1,500 Retained Earnings 690,000 54,000 40,000 40,000 636,000 Share Premium—Ordinary Share Premium—T.S. Note […]

Accounting Chapter 16 A corporation’s capital structure is regarded

PROBLEM 16.5 (a) Meng Group has a simple capital structure since it does not have any potentially dilutive securities. (b) The weighted-average number of shares that Ming Group would use in calculating earnings per share for the fiscal years ended […]

Accounting Chapter 16 Add Shares Assumed Issued 10000 Shares

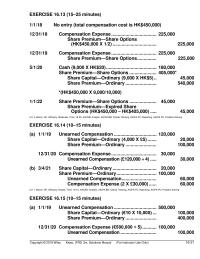

EXERCISE 16.13 (15–25 minutes) 1/1/18 No entry (total compensation cost is HK$450,000) 12/31/18 Compensation Expense …………………………….. 225,000 Share Premium—Share Options (HK$450,000 X 1/2) ……………………………. 225,000 12/31/19 Compensation Expense …………………………….. 225,000 Share Premium—Share Options …………… 225,000 5/1/20 Cash (9,000 X HK$20) […]

Accounting Chapter 16 Compute earnings per share in a complex situation.

CHAPTER 16 DILUTIVE SECURITIES AND EARNINGS PER SHARE CHAPTER LEARNING OBJECTIVES 1. Describe the accounting for the issuance, conversion, and retirement of convertible securities. 2. Describe the accounting for share warrants and for share warrants issued with other securities. 3. […]

Accounting Chapter 16 For Example Corporation Has 10000 Warrants Outstanding

CHAPTER 16 Dilutive Securities and Earnings Per Share ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Convertible debt and preference shares. 1, 2, 3, 4, 5, 6, 7 1, 2, 3 1, 2, […]

Accounting Chapter 16 Warrants 28 Share Options And Warrants Outstanding

3. Describe the accounting and reporting for share compensation plans. 4. Compute basic earnings per share. 5. Compute diluted earnings per share. *6. Explain the accounting for share-appreciation rights plans. *7. Compute earnings per share in a complex situation. *This […]

Accounting Chapter 16 which defeats the purpose of the assumed exercise

CA 16.7 Dear Mr. Dolan: I hope that the following brief explanation helps you understand why your warrants were not included in Rhode’s earnings per share calculations. Earnings per share (EPS) provides income statement users a quick assessment of the […]

Accounting Chapter 17 A cash flow hedge is used to hedge exposure

CHAPTER 17 Investments ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Debt investments. 1, 2, 3, 4, 11, 12 1, 9 4, 7 (a) Held-for-collection; Held-for-collection and selling 6, 7, 9 1, 2, […]

Accounting Chapter 17 Financial Position December 31 2018 Assets

CHAPTER 17 INVESTMENTS CHAPTER LEARNING OBJECTIVES 1. Describe the accounting for debt investments. 2. Describe the accounting for equity investments. 3. Explain the equity method of accounting. 4. Evaluate other major issues related to debt and equity investments. *5. Describe […]

Accounting Chapter 17 Interest Receivable Interest Revenue 312

PROBLEM 17.1 (Continued) Amortized Cost Fair Value Unrealized Gain (Loss) Spangler Company, 7% bonds $103,719 $105,650 $1,931 Previous fair value adjustment—Dr. 2,053* Fair value adjustment—Cr. $ (122) *($107,500 – $105,447) Unrealized Holding Gain or Loss—Income …………… 122 Fair Value Adjustment […]

Accounting Chapter 17 Since Komissarov will now receive the contractual

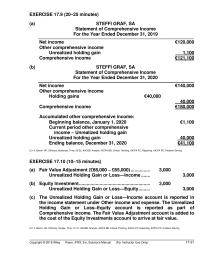

EXERCISE 17.9 (20–25 minutes) (a) STEFFI GRAF, SA Statement of Comprehensive Income For the Year Ended December 31, 2019 _____________________________________________________________ Net income €120,000 Other comprehensive income Unrealized holding gain 1,100 Comprehensive income €121,100 (b) STEFFI GRAF, SA Statement of Comprehensive […]

Accounting Chapter 17 The problems of accounting for investments

4. Evaluate other major issues related to debt and equity investments. *5. Describe the uses of and accounting for derivatives… *6. Explain the accounting for hedges. *7. Identify special reporting issues related to derivative financial instruments that cause unique accounting […]

Accounting Chapter 17 This Case Involves Three Independent Situations For

*PROBLEM 17.12 (a) July 7, 2019 Call Option …………………………………………………….. 240 Cash ………………………………………………………… 240 (b) September 30, 2019 Call Option …………………………………………………….. 1,400 Unrealized Holding Gain or Loss— Income (€7 X 200) …………………………………… 1,400 Unrealized Holding Gain or Loss—Income ……….. 60 Call […]

Accounting Chapter 17 Under The Fair Value Method For Nontrading

CA 17.5 Since Fontaine Company purchased 40% of Knoblett Company’s outstanding ordinary shares, Fontaine is considered to have significant influence over Knoblett Company. Therefore, Fontaine will account for this investment using the equity method. The investment is reported on the […]

Accounting Chapter 18 Because The Points Provide Material Right Customer

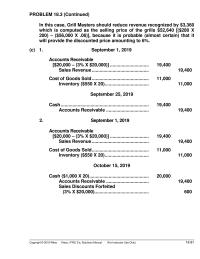

PROBLEM 18.3 (Continued) In this case, Grill Masters should reduce revenue recognized by $3,360 which is computed as the selling price of the grills $52,640 [($280 X 200) – ($56,000 X .06)], because it is probable (almost certain) that it […]

Accounting Chapter 18 Celic recognizes warranty expenses associated

EXERCISE 18.27 (15–20 minutes) (a) October 1, 2019 To record sales revenue, warranties, and related cost of goods sold Cash (or Accounts Receivable) ………………………….. 3,600 Sales Revenue ……………………………………………. 3,200 Unearned Warranty Revenue (Service-type) …. 400 Cost of Goods Sold …………………………………………… […]

Accounting Chapter 18 Change in control is the deciding factor

CHAPTER 18 Revenue Recognition ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Current Environment; 5-Step Model. 1, 2, 3, 4, 5, 6 1 8 1, 2, 3 2. Contracts. 7 1, 2 1, […]

Accounting Chapter 18 Cooper Uses The Percentage of completion Method Revenue Recognition

CHAPTER 18 REVENUE RECOGNITION CHAPTER LEARNING OBJECTIVES 1. Understand the fundamental concepts related to revenue recognition and measurement. 2. Understand and apply the five-step revenue recognition process. 3. Apply the five-step process to major revenue recognition issues. 4. Describe presentation […]

Accounting Chapter 18 Earnings per share in the second year of the four-year

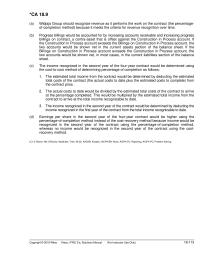

*CA 18.9 (a) Widjaja Group should recognize revenue as it performs the work on the contract (the percentage- of-completion method) because it meets the criteria for revenue recognition over time. (b) Progress billings would be accounted for by increasing accounts […]

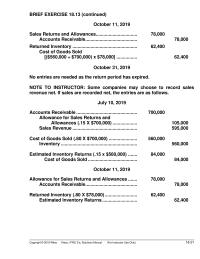

Accounting Chapter 18 No entries are needed as the return period

BRIEF EXERCISE 18.13 (continued) October 11, 2019 Sales Returns and Allowances………………………….. 78,000 Accounts Receivable …………………………………. 78,000 Returned Inventory ………………………………………….. 62,400 Cost of Goods Sold [($560,000 ÷ $700,000) x $78,000] ……………. 62,400 October 31, 2019 No entries are needed as the […]

Accounting Chapter 18 The Companys Performance Creates Enhances Asset

4. Describe presentation and disclosure regarding revenue. *5. Apply the percentage–of-completion method for long-term contracts. *6. Apply the cost-recovery method for long-term contracts. *7. Identify the proper accounting for losses on long-term contracts. *8. Explain revenue recognition for franchises. *This […]

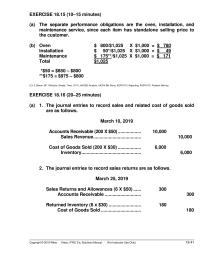

Accounting Chapter 18 The journal entries to record sales and related

EXERCISE 18.15 (10–15 minutes) (a) The separate performance obligations are the oven, installation, and maintenance service, since each item has standalone selling price to the customer. (b) Oven $ 800/$1,025 X $1,000 = $ 780 Installation $ 50*/$1,025 X $1,000 […]

Accounting Chapter 18 The student indicates the effect on earnings per

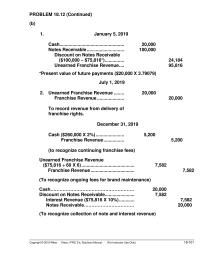

PROBLEM 18.12 (Continued) (b) 1. January 5, 2019 Cash………………………………………….. 20,000 Notes Receivable ……………………….. 100,000 Discount on Notes Receivable ($100,000 – $75,816*) …………… 24,184 Unearned Franchise Revenue …. 95,816 *Present value of future payments ($20,000 X 3.79079) July 1, 2019 2. […]

Accounting Chapter 19 Nol Expected The Year That Future Deductible

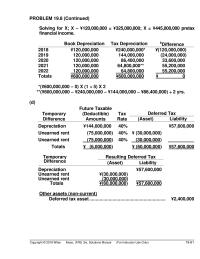

PROBLEM 19.8 (Continued) Solving for X; X – ¥120,000,000 = ¥325,000,000; X = ¥445,000,000 pretax financial income. Book Depreciation Tax Depreciation bDifferenceb 2018 ¥120,000,000 ¥240,000,000* (¥(120,000,000) 2019 120,000,000 144,000,000 (24,000,000) 2020 120,000,000 86,400,000 33,600,000 2021 120,000,000 64,800,000** 55,200,000 2022 120,000,000 […]

Accounting Chapter 19 Originating difference which will result in future

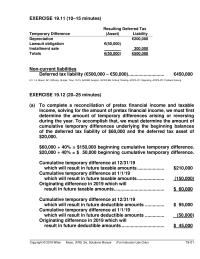

EXERCISE 19.11 (10–15 minutes) Resulting Deferred Tax Temporary Difference (Asset) Liability Depreciation €200,000 Lawsuit obligation €(50,000) Installment sale 300,000 Totals €(50,000) €500,000 Non-current liabilities Deferred tax liability (€500,000 – €50,000) ………………………. €450,000 LO: 1,4, Bloom: AP, Difficulty: Simple, Time: 10-15, […]

Accounting Chapter 19 Permanent Differences Bond Interest Revenue Pollution Fines

Time and Purpose of Problems (Continued) Problem 19.8 (Time 40–50 minutes) Purpose—to test a student’s understanding of the relationships that exist in the subject area of accounting for income taxes. The student is required to compute and classify deferred income […]

Accounting Chapter 19 taxable income and financial income frequently

3. Explain the accounting for loss carrybacks and loss carryforwards. 4. Describe the presentation of income taxes in financial statements. *5. Understand and apply the concepts and procedures of interperiod tax allocation. *This material is covered in an Appendix to […]

Accounting Chapter 19 The 12000 Deferred Tax Liability Should Classified

CHAPTER 19 Accounting for Income Taxes ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Reconcile pretax financial income with taxable income. 1, 12 1 1, 2, 4, 12, 18 1, 2, 3, 8 […]

Accounting Chapter 19 Use The Following Information For Questions And

CHAPTER 19 ACCOUNTING FOR INCOME TAXES CHAPTER LEARNING OBJECTIVES 1. Describe the fundamentals of accounting for income taxes. 2. Identify additional issues in accounting for income taxes. 3. Explain the accounting for loss carrybacks and loss carryforwards. 4. Describe the […]

Accounting Chapter 2 International Accounting Standards Board Makes Depreciation And

CHAPTER 2 CONCEPTUAL FRAMEWORK FOR FINANCIAL REPORTING CHAPTER LEARNING OBJECTIVES 1. Describe the usefulness of a conceptual framework and the objective of financial reporting. 2. Identify the qualitative characteristics of accounting information and the basic elements of financial statements. 3. […]

Accounting Chapter 2 Not Until This Obligation Fulfilled Should The

EXERCISE 2.9 (Continued) (d) At the present time, accountants generally do not recognize price- level adjustments in the accounts. Hence, it is misleading to deviate from the cost principle because conjecture or opinion can take place. It should also be […]

Accounting Chapter 2 The Conclusion That His Business Lost 4900

FINANCIAL REPORTING PROBLEM (a) According to Note 1—Accounting Policies, “Revenue comprises sales of goods to customers outside the Group less an appropriate deduction for actual and expected returns, discounts and loyalty scheme vouchers, and is stated net of value added […]

Accounting Chapter 2 The Four Basic Principles Accounting Are Measurement

4. Identify the qualitative characteristics of accounting information. 5. Define the basic elements of financial statements. 6. Describe the basic assumptions of accounting. 7. Explain the application of the basic principles of accounting. 8. Describe the impact that the cost […]

Accounting Chapter 2 This Item Should Not Entered The Accounts

CHAPTER 2 Conceptual Framework for Financial Reporting ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Concepts for Analysis 1. Conceptual framework– general. 1 1, 2 2. Objective of financial reporting. 2, 7 13 1, 2 3 3. Qualitative […]

Accounting Chapter 20 A pension plan is an arrangement whereby an employer

3. Explain the accounting for past service costs. 4. Explain the accounting for remeasurements. 5. Describe the requirements for reporting pension plans in financial statements. 6. Explain the accounting for other postretirement benefits. CHAPTER 20 Accounting for Pensions and Postretirement […]

Accounting Chapter 20 A pension worksheet follows to provide supporting

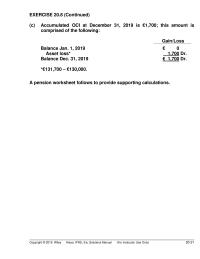

Copyright © 2018 Wiley Kieso, IFRS, 3/e, Solutions Manual (For Instructor Use Only) 20–21 EXERCISE 20.8 (Continued) (c) Accumulated OCI at December 31, 2019 is €1,700; this amount is comprised of the following: Gain/Loss Balance Jan. 1, 2019 € 0 […]

Accounting Chapter 20 Pension Asset liability The Cumulative Net Pension Expense

20-61 Copyright © 2018 Wiley Kieso, IFRS, 3/e, Solutions Manual (For Instructor Use Only) CHEN Group. Pension Worksheet—2019 General Journal Entries Memo Record PROBLEM 20.12 Annual Pension Expense Cash OCI— Gain/Loss Pension Asset/Liability Defined Benefit Obligation Plan Assets Balance, Jan. […]

Accounting Chapter 20 The Cost The Retroactive Benefits The Increase

CHAPTER 20 Accounting for Pensions and Postretirement Benefits ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Basic definitions and concepts related to pension plans. 1, 2, 3, 4, 5, 6, 7, 8, 9, […]

Accounting Chapter 20 Towson Amended Its Pension Plan January 2019

CHAPTER 20 ACCOUNTING FOR PENSIONS AND POSTRETIREMENT BENEFITS CHAPTER LEARNING OBJECTIVES 1. Discuss the fundamentals of pension plan accounting. 2. Use a worksheet for employer’s pension plan entries. 3. Explain the accounting for past service costs. 4. Explain the accounting […]

Accounting Chapter 20 While Selma May Correct Assuming That

CA 20.6 While Selma may be correct in assuming that the termination of non-vested employees would decrease its pension-related liabilities and associated expenses, she is callous to suggest that firing employees is a reasonable approach to correcting the underfunding of […]

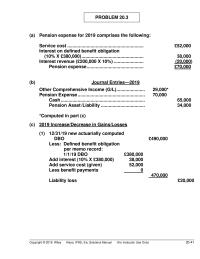

Accounting Chapter 20 Other comprehensive income gain

PROBLEM 20.3 (a) Pension expense for 2019 comprises the following: Service cost ………………………………………………….. £52,000 Interest on defined benefit obligation (10% X £380,000) ………………………………………… 38,000 Interest revenue (£200,000 X 10%) ………………….. (20,000) Pension expense …………………………………….. £70,000 (b) Journal Entries—2019 Other Comprehensive […]

Accounting Chapter 21 August Because The Agreement Began That Date

Copyright © 2018 Wiley Kieso, IFRS, 3/e, Solutions Manual (For Instructor Use Only) 21–61 Problem 21.9 (Time 30–40 minutes) Purpose—to develop an understanding of the accounting treatment accorded a sales-type lease involving an unguaranteed residual value. The student is required […]

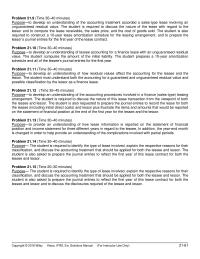

Accounting Chapter 21 Employee salaries are specifically excluded as initial

BRIEF EXERCISE 21.22 (Continued) Lease liability: $22,156 Legal fees: 1,000 Right-of–use asset: $23,156 Thus, the journal entry to record the initial lease liability and right–of-use asset is as follows: Right-of–Use Asset ………………………………………………… 23,156* Cash (Legal Fees) …………………………………………… 1,000 Lease Liability […]

Accounting Chapter 21 From The Perspective The Lessee There Unguaranteed

3. Explain the accountinf for leases by lessors. 4. Discuss the accounting and reporting for special features of lease arrangements. *5. Describe the lessee’s accounting for sale-leaseback transactions. *6. Apply lessee and lessor accounting to finance and operating leases. *This […]

Accounting Chapter 21 Lessee Entries with Bargain-Purchase Option

CHAPTER 21 Accounting for Leases ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Rationale for leasing. 1, 2, 3 2. Concepts, and measurement of leases by lessees. 4, 5, 6, 7, 8, 9, […]

Accounting Chapter 21 the appropriate accounting treatment which should

TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS CA 21.1 (Time 15–25 minutes) Purpose—to provide the student with an understanding of the theoretical reasons for requiring leases to be capitalized by the lessee and how a lease is recorded at its […]

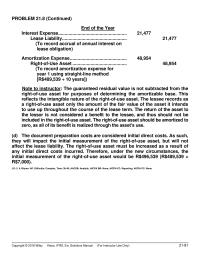

Accounting Chapter 21 The guaranteed residual value is not subtracted from

PROBLEM 21.8 (Continued) End of the Year Interest Expense …………………………………………….. 21,477 Lease Liability ………………………………………….. 21,477 (To record accrual of annual interest on lease obligation) Amortization Expense …………………………………….. 48,954 Right-of–Use Asset …………………………………… 48,954 (To record amortization expense for year 1 using […]

Accounting Chapter 21 The IASB agrees with the capitalization approach and requires

CHAPTER 21 ACCOUNTING FOR LEASES CHAPTER LEARNING OBJECTIVES 1. Understand the environment related to leasing transactions. 2. Explain the accounting for leases by lessees. 3. Explain the accounting for leases by lessors. 4. Discuss the accounting and reporting for special […]

Accounting Chapter 21 The Initial Measurement The Right of use Asset Will

EXERCISE 21.11 (20–30 minutes) (a) The lease agreement has a bargain-purchase option. The collectibility of the lease payments by Mooney is probable. The lease, therefore, qualifies as a sales- type lease from the viewpoint of the lessor. The lease payments […]

Accounting Chapter 22 Requirement by International Accounting Standards

Copyright © 2018 Wiley Kieso, IFRS, 3/e, Solutions Manual (For Instructor Use Only) 22-1 CHAPTER 22 Accounting for Changes and Error Analysis ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Differences between change […]

Accounting Chapter 22 The Books Have Been Closed The Error

2. Describe the accounting and reporting for changes in estimates. 3. Describe the accounting for correction of errors. 4. Analyze the effect of errors. CHAPTER 22 Accounting Changes and Error Analysis LEARNING OBJECTIVES 1. Discuss the types of accounting changes […]

Accounting Chapter 22 Under This Approach The Cumulative Effect The

PROBLEM 22.7 (Continued) (9) Insurance Expense ($12,000 ÷ 3) ………………………………… 4,000 Prepaid Insurance …………………………………………………….. 6,000 Retained Earnings ……………………………………………… 10,000 (10) Amortization Expense ($50,000 ÷ 10) ………………………….. 5,000 Retained Earnings …………………………………………………….. 5,000 Trademarks ……………………………………………………….. 10,000 LO: 3,4, Bloom: AP, Difficulty: Moderate, […]

Accounting Chapter 22 Working Capital Overstated 1500 Working Capital Understated

CHAPTER 22 ACCOUNTING CHANGES AND ERROR ANALYSIS CHAPTER LEARNING OBJECTIVES 1. Discuss the types of accounting changes, and the accounting for changes in accounting policies. 2. Describe the accounting and reporting for changes in estimates. 3. Describe the accounting for […]

Accounting Chapter 22 Purpose—to develop an understanding of the correcting

EXERCISE 22.15 (Continued) 4. Amortization Expense—Copyright …………………… 2,500(c) Retained Earnings ………………………………………….. 5,000(d) Copyright ($2,500 + $5,000) ………………………. 7,500 ($50,000 ÷ 20 = $2,500(c); ($2,500 X 2 = $5,000(d)) 5. Loss on Write-down of Inventories (or Cost of Goods Sold) ……………………………….. […]

Accounting Chapter 23 Changes Deferred Income Taxes Affect Net Income

1. Describe the usefulness and format of the statement of cash flows. 3. Contrast the direct and indirect methods of calculating net cash flows from operating activities. Copyright © 2018 John Wiley & Sons, Inc. Kieso Intermediate: IFRS 3e, Instructor’s […]

Accounting Chapter 23 Depreciation Expense Gain Sale Investment

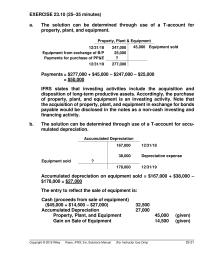

EXERCISE 23.10 (25–35 minutes) a. The solution can be determined through use of a T-account for property, plant, and equipment. Property, Plant & Equipment 12/31/18 247,000 45,000 Equipment sold Equipment from exchange of B/P 25,000 Payments for purchase of PP&E […]

Accounting Chapter 23 For The Year Ended December 31 2019

CHAPTER 23 STATEMENT OF CASH FLOWS CHAPTER LEARNING OBJECTIVES 1. Describe the usefulness and format of the statement of cash flows. 2. Prepare a statement of cash flows. 3. Contrast the direct and indirect methods of calculating net cash flow […]

Accounting Chapter 23 Net Cash Provided Financing Activities

CHAPTER 23 Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Format, objectives purpose, and source of statement. 1, 2, 5, 7, 8, 12 1, 2, 5, 6 2. Classifying […]

Accounting Chapter 23 Puma Concerning Trend That Should Monitored Investors

CA 23.1 (Continued) 6. The details of changes in long-term debt should be shown separately. Payments should not be netted against increases in long-term borrowings. The long-term borrowing of $620,000 should be shown as cash provided (cash inflow) and the […]

Accounting Chapter 23 Reduction in long-term notes payable

PROBLEM 23.3 MORTONSON PLC Statement of Cash Flows For the Year Ended December 31, 2019 (£ in thousands) Cash flows from operating activities Cash receipts from customers ……………….. £3,520 (a) Cash payments: Payments for merchandise ………………… £1,270 (b) Salaries and […]

Accounting Chapter 24 Income Tax Expense Benefit 8 Significant Noncash

Copyright © 2018 John Wiley & Sons, Inc. Kieso Intermediate: IFRS 3e, Instructor’s Manual 24–13 *51. (L.O. 13) When a company first adopts IFRS, it must present at least one year of comparative information, and its first set of financial […]

Accounting Chapter 24 Presented Below Information Related Tolbert Company Current

CHAPTER 24 PRESENTATION AND DISCLOSURE IN FINANCIAL REPORTING CHAPTER LEARNING OBJECTIVES 1. Describe the full disclosure principle and how it is implemented. 2. Discuss the disclosure requirements for related-party transactions, subsequent events, and major business segments, and interim reporting. 3. […]

Accounting Chapter 24 Ratio computations and additional analysis

CHAPTER 24 Presentation and Disclosure in Financial Reporting ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis * 1. The disclosure principle; type of disclosure. 2, 3, 22 1, 2, 3 * 2. Role of […]

Accounting Chapter 24 Strikes are considered general knowledge and therefore

CA 24.3 (Continued) Situation 3 The fact that a company chooses to self-insure the contingency of injury to others caused by its vehicles is not enough of a basis to accrue a loss contingency that has not occurred at the […]

Accounting Chapter 24 The Possible Effect The Market Price The

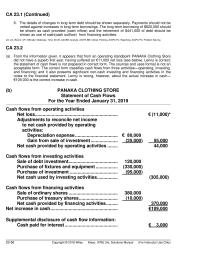

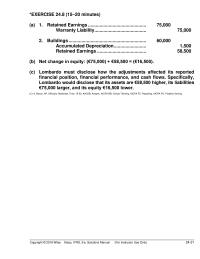

*EXERCISE 24.8 (15–20 minutes) (a) 1. Retained Earnings ……………………………………… 75,000 Warranty Liability …………………………………. 75,000 2. Buildings …………………………………………………… 60,000 Accumulated Depreciation ……………………. 1,500 Retained Earnings ……………………………….. 58,500 (b) Net change in equity: (€75,000) + €58,500 = (€16,500). (c) Lombardo must disclose […]

Accounting Chapter 24 Accountants and business executives are fully aware

Copyright © 2018 John Wiley & Sons, Inc. Kieso Intermediate: IFRS 3e, Instructor’s Manual 24-1 CHAPTER 24 Presentation and Disclosure in Financial Reporting LEARNING OBJECTIVES 1. Review the full disclosure principle and describe how it is implemented. 2. Discuss the […]

Accounting Chapter 3 Based on the balance in interest payable

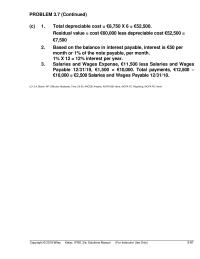

PROBLEM 3.7 (Continued) (c) 1. Total depreciable cost = €8,750 X 6 = €52,500. Residual value = cost €60,000 less depreciable cost €52,500 = €7,500 2. Based on the balance in interest payable, interest is €50 per month or 1% […]

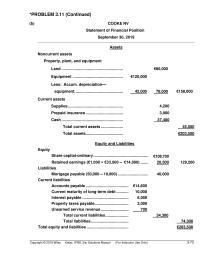

Accounting Chapter 3 Continued B Cooke Statement Financial

*PROBLEM 3.11 (Continued) (b) COOKE NV Statement of Financial Position September 30, 2019 Assets Noncurrent assets Property, plant, and equipment Land ………………………………………………………. €80,000 Equipment ………………………………………………………. €120,000 Less: Accum. depreciation— equipment. ………………………………………………………. 42,000 78,000 €158,000 Current assets Supplies ………………………………………………………. 4,200 Prepaid […]

Accounting Chapter 3 Dec Prepaid Expenses Jan Prepaid Expenses Dec

EXERCISE 3.9 (15–20 minutes) (a) 10/15 Salaries and Wages Expense ………………………………………………….. 800 Cash ……………………………………………………………………………….. 800 (To record payment of October 15 payroll) 10/17 Accounts Receivable ………………………………………………………. 2,100 Service Revenue ………………………………………………………. 2,100 (To record revenue for services performed for which payment […]

Accounting Chapter 3 Enter The Transactions The Period Appropriate Journals

5. Explain the reasons for preparing adjusting entries. 6. Prepare financial statements from the adjusted trial balance. 7. Prepare closing entries. 8. Prepare financial statements for a merchandising company. *9. Differentiate the cash basis of accounting from the accrual basis […]

Accounting Chapter 3 Equity And Liabilities Equity Share Capital ordinary

PROBLEM 3.1 (Continued) (c) YASUNARI KAWABATA, D.D.S. Income Statement For the Month of September Service revenue ………………………………………………………. ¥9,620 Expenses: Salaries and wages expense ………………………… ¥1,800 Rent expense ……………………………………………… 680 Office expense ……………………………………………. Supplies expense 515 330 Depreciation expense ………………………….. 288 […]

Accounting Chapter 3 Increasing Equity 60000 Decreasing Liabilities 30000 Increasing

CHAPTER 3 THE ACCOUNTING INFORMATION SYSTEM CHAPTER LEARNING OBJECTIVES 1. Describe the basic accounting information system. 2. Record and summarize basic transactions. 3. Identify and prepare adjusting entries. 4. Prepare financial statements from the adjusted trial balance and prepare closing […]

Accounting Chapter 3 Worksheet and statement of financial position

CHAPTER 3 The Accounting Information System ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems 1. Transaction identification. 1, 2, 3, 5 1, 2 1, 3, 4, 17 1 2. Nominal accounts. 4, 7 3. Trial balance. 6, […]

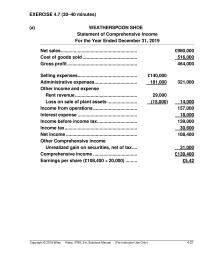

Accounting Chapter 4 Comprehensive Income Statement Net Income Unrealized

EXERCISE 4.7 (30–40 minutes) (a) WEATHERSPOON SHOE Statement of Comprehensive Income For the Year Ended December 31, 2019 Net sales ………………………………………………….. £980,000 Cost of goods sold …………………………………… 516,000 Gross profit ……………………………………………… 464,000 Selling expenses ………………………………………. £140,000 Administrative expenses …………………………… 181,000 […]

Accounting Chapter 4 Compute The Amount Net Income loss

CHAPTER 4 INCOME STATEMENT AND RELATED INFORMATION CHAPTER LEARNING OBJECTIVES 1. Identify the uses and limitations of an income statement. 2. Describe the content and format of the income statement. 3. Discuss how to report various income items. 4. Explain […]

Accounting Chapter 4 Earnings Per Share Income From Continuing Operations

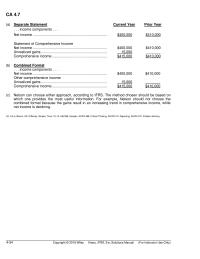

CA 4.7 (a) Separate Statement Current Year Prior Year . . . income components . . . Net income …………………………………………………………………. $400,000 $410,000 Statement of Comprehensive Income Net income …………………………………………………………………. $400,000 $410,000 Unrealized gains ………………………………………………………….. 15,000 _______ Comprehensive income ………………………………………………… $415,000 […]

Accounting Chapter 4 Loss Discontinued Operations Requires Separate Classification After

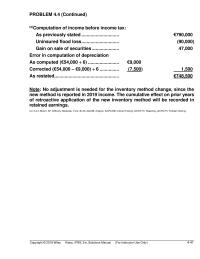

PROBLEM 4.4 (Continued) (a)Computation of income before income tax: As previously stated ……………………….. €790,000 Uninsured flood loss ……………………….. (90,000) Gain on sale of securities ………………… 47,000 Error in computation of depreciation As computed (€54,000 ÷ 6) …………………… €9,000 Corrected (€54,000 […]

Accounting Chapter 4 The Denominator Also Incorrect Neumann Had Any

CHAPTER 4 Income Statement and Related Information ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Income measurement concepts. 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 32 2, 3, 4, […]

Accounting Chapter 4 The income statement helps users of financial

3. Prepare an income statement. 4. Explain how to report items in the income statement. 5. Identify where to report earnings per share information. 6. Explain intraperiod tax allocation. 7. Understand the reporting of accounting changes and errors. 8. Prepare […]

Accounting Chapter 5 Generally The First Note The Financial Statements

5. Identify the content of the statement of cash flows. 6. Prepare a basic statement of cash flows. 7. Understand the usefulness of the statement of cash flows. 8. Determine additional information requiring note disclosure. 9. Describe the major disclosure […]

Accounting Chapter 5 Net Cash Provided Operating Activities Average Current

CHAPTER 5 STATEMENT OF FINANCIAL POSITION AND STATEMENT OF CASH FLOWS CHAPTER LEARNING OBJECTIVES 1. Explain the uses limitations and content of a statement of financial position. 2. Prepare a classified statement of financial position. 3. Identify the purpose content […]

Accounting Chapter 5 The Most Significant Difference Relates Intangible Assets

TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS CA 5.1 (Time 20–25 minutes) Purpose—to provide a varied number of financial transactions and then determine how each of these items should be reported in the financial statements. Accounting changes, additional assessments of […]

Accounting Chapter 5 Total Liabilities Total Equity And Liabilities

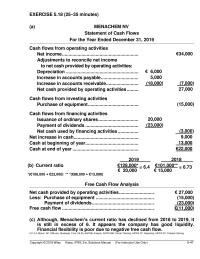

EXERCISE 5.18 (25–35 minutes) (a) MENACHEM NV Statement of Cash Flows For the Year Ended December 31, 2019 Cash flows from operating activities Net income ………………………………………………………. €34,000 Adjustments to reconcile net income to net cash provided by operating activities: Depreciation […]

Accounting Chapter 5 Total Noncurrent Liabilities Current Liabilities Short term

EXERCISE 5.5 (30–35 minutes) BRUNO SPA Statement of Financial Position December 31, 2019 Assets Non-current assets Long-term investments Land held for future use …………………… € 175,000 Property, plant, and equipment Buildings …………………………………………. €730,000 Less: Accum. depr.—buildings ………… 160,000 €570,000 Equipment […]

Accounting Chapter 5 and presentation of the statement of cash flows

CHAPTER 5 Statement of Financial Position and Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. of financial position, financial flexibility. 21, 29, 30 2. Classification of items in the […]

Accounting Chapter 6 Bid A should be accepted since its present

PROBLEM 6.3 Time diagram (Bid A): i = 9% W69,000 PV – OA = R = ? 3,000 3,000 3,000 3,000 69,000 3,000 3,000 3,000 3,000 0 0 1 2 3 4 5 6 7 8 9 10 n = […]

Accounting Chapter 6 Describe Accounting Applications Time Value Concepts Bonds

4. Identify variables fundamental to solving interest problems. 5. Solve future and present value of 1 problems. 6. Solve future value of ordinary and annuity due problems. 7. Solve present value of ordinary and annuity due problems. 8. Solve present […]

Accounting Chapter 6 Formula for property taxes and other costs

PROBLEM 6.10 1. Purchase. Time diagrams: Installments i = 10% PV – OA = ? R = $350,000 $350,000 $350,000 $350,000 $350,000 0 1 2 3 4 5 n = 5 Property taxes and other costs i = 10% PV […]

Accounting Chapter 6 Location And Location 103

CHAPTER 6 ACCOUNTING AND THE TIME VALUE OF MONEY CHAPTER LEARNING OBJECTIVES 1. Describe the fundamental concepts related to the time value of money. 2. Solve future and present value of 1 problems. 3. Solve future value of ordinary and […]

Accounting Chapter 6 The rate of interest is determined by dividing

EXERCISE 6.8 (10–15 minutes) (a) Present value of an ordinary annuity of 1 for 4 periods @ 8% 3.31213 Annual withdrawal X $25,000 Required fund balance on June 30, 2022 $82,803 (b) Fund balance at June 30, 2022 $82,803 = […]

Accounting Chapter 6 Solve present value of ordinary and annuity

CHAPTER 6 Accounting and the Time Value of Money ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems 1. Present value concepts. 1, 2, 3, 4, 5, 9, 17, 19 2. Use of tables. 13, 14 8 1 […]

Accounting Chapter 7 Allowance For Doubtful Accounts 10000 During

CHAPTER 7 CASH AND RECEIVABLES CHAPTER LEARNING OBJECTIVES 1. Indicate how to report cash and related items. 2. Define receivables and explain the accounting issues related to their recognition. 3. Explain accounting issues related to valuation of accounts receivable. 4. […]

Accounting Chapter 7 Cash And Receivables Assignment Classification Table

CHAPTER 7 Cash and Receivables ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Accounting for cash. 1, 2, 3, 4, 23 1 1, 2 1 2. Accounting for accounts receivable, bad debts, other […]

Accounting Chapter 7 Homework While Grants Collections Have Slowed Factoring The

EXERCISE 7.5 (Continued) (b) July 29 Cash ………………………………………………………. 2,000 Accounts Receivable—Arquette ………………………… 1,960 Sales Discounts Forfeited ………………………….. 40 (Note to instructor: Sales discounts forfeited could have been recog- nized at the time the discount period lapsed. The company, however, would […]

Accounting Chapter 7 Loss Resulting From Accounts Receivable Sold

Copyright © 2018 Wiley Kieso, IFRS, 3/e, Solutions Manual (For Instructor Use Only) 7-41 PROBLEM 7.4 (a) FORTNER PLC Analysis of Changes in the Allowance for Doubtful Accounts For the Year Ended December 31, 2019 Balance at January 1, 2019 […]

Accounting Chapter 7 The Carrying Amount These Assets Approximates Their

CA 7.2 (Continued) Kimmel should report interest revenue from the notes receivable on its income statement for the year ended December 31, 2019. Interest revenue is equal to the amount accrued on the notes receivable at the appropriate rate for […]

Accounting Chapter 7 This Process Designed Promote Control Over Small

4. Explain accounting issues related to recognition and valuation of notes receivable. 5. Explain accounting issues related to derecognition of accounts and notes receivable. 6. Describe how to report and analyze receivables. *7. Explain common techniques employed to control cash. […]

Accounting Chapter 8 FIFO and average cost—income statement presentation

CHAPTER 8 Valuation of Inventories: A Cost-Basis Approach ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. costs, and items to be included in inventory; the inventory equation; statement of financial position disclosure. 10, […]

Accounting Chapter 8 Four decimal places are used to minimize rounding

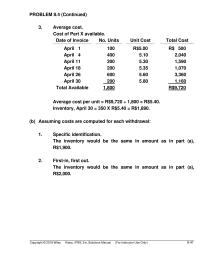

PROBLEM 8.4 (Continued) 3. Average cost. Cost of Part X available. Date of Invoice No. Units Unit Cost Total Cost April 1 100 R$5.00 R$ 500 April 4 400 5.10 2,040 April 11 300 5.30 1,590 April 18 200 5.35 […]

Accounting Chapter 8 The Ending Inventory Cost Determined Determining The

3. Compare the cost flow assumptions used to account for inventories. 4. Determine the effects of inventory errors on the financial statements. *5. Describe the LIFO cost flow assumption. *This material is covered in an Appendix to the chapter. CHAPTER […]

Accounting Chapter 8 The Moving average Cost Method The Other Hand

*PROBLEM 8.10 The accounts in the 2020 financial statements which would be affected by a change to LIFO and the new amount for each of the accounts are as follows: Account New amount for 2020 (1) Cash $176,400 (2) Inventory […]

Accounting Chapter 8 Unit Cost 977 Total Cost 29310

CHAPTER 8 VALUATION OF INVENTORIES: A COST-BASIS APPROACH CHAPTER LEARNING OBJECTIVES 1. Describe inventory classifications and different inventory systems. 2. Identify the goods and costs included in inventory. 3. Compare the cost flow assumptions used to account for inventories. 4. […]

Accounting Chapter 8 FIFO will yield the highest ending inventory

EXERCISE 8.11 (15–20 minutes) (a) 1. 2,100 units available for sale – 1,400 units sold = 700 units in the ending inventory. 500 @ $4.58 = $2,290 200 @ 4.60 = 920 700 $3,210 Ending inventory at FIFO cost. 2. […]

Accounting Chapter 9 Debit Unrealized Holding Loss For And

CHAPTER 9 INVENTORIES: ADDITIONAL VALUATION ISSUES CHAPTER LEARNING OBJECTIVES 1. Describe and apply the lower-of-cost-or– net realizable value rule. 2. Identify other inventory valuation issues. 3. Determine ending inventory by applying the gross profit method. 4. Determine ending inventory by […]

Accounting Chapter 9 Emphasize That The Inventory Techniques Not

3. Determine ending inventory by applying the gross profit method. 4. Determine ending inventory by applying the retail inventory method. 5. Explain how to report and analyze inventory. CHAPTER 9 Inventories: Additional Valuation Issues LEARNING OBJECTIVES 1. Describe and apply […]

Accounting Chapter 9 If the commitment is material in amount

Copyright © 2018 Wiley Kieso, IFRS, 3/e, Solutions Manual (For Instructor Use Only) 9-21 EXERCISE 9.10 (12–17 minutes) Cost per Chair £54 48 30 Cost Allocated to Chairs £21,600 14,400 24,000 £60,000 Total Cost £60,000 60,000 60,000 Gross Profit £ […]

Accounting Chapter 9 Inventory Turnover Its Gross Profit Percentages For

CA 9.2 (Continued) (c) Conan should use the loss method to disclose the decline in market value and avoid distorting cost of goods sold. However, he faces an ethical dilemma if Ortiz will not accept the method Conan wants to […]

Accounting Chapter 9 Relative standalone sales value method

CHAPTER 9 Inventories: Additional Valuation Issues ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Lower-of-cost-or–NRV. 1, 2, 3, 4, 5 1, 2, 3 1, 2, 3, 4, 5, 6 1, 2, 3, 10, […]

Accounting Chapter 9 The Term Cost Relatively Simple Refers The

PROBLEM 9.6 (Continued) *Computation of Gross Profit Ratio Net sales, 2017 ………………………………………… €390,000 Net sales, 2018 ………………………………………… 530,000 Total net sales ………………………………… 920,000 Beginning inventory …………………………………. € 66,000 Net purchases, 2017 …………………………………. 235,000 Net purchases, 2018 …………………………………. 280,000 Total ………………………………………………. […]