PROBLEM 21.8 (Continued)

End of the Year

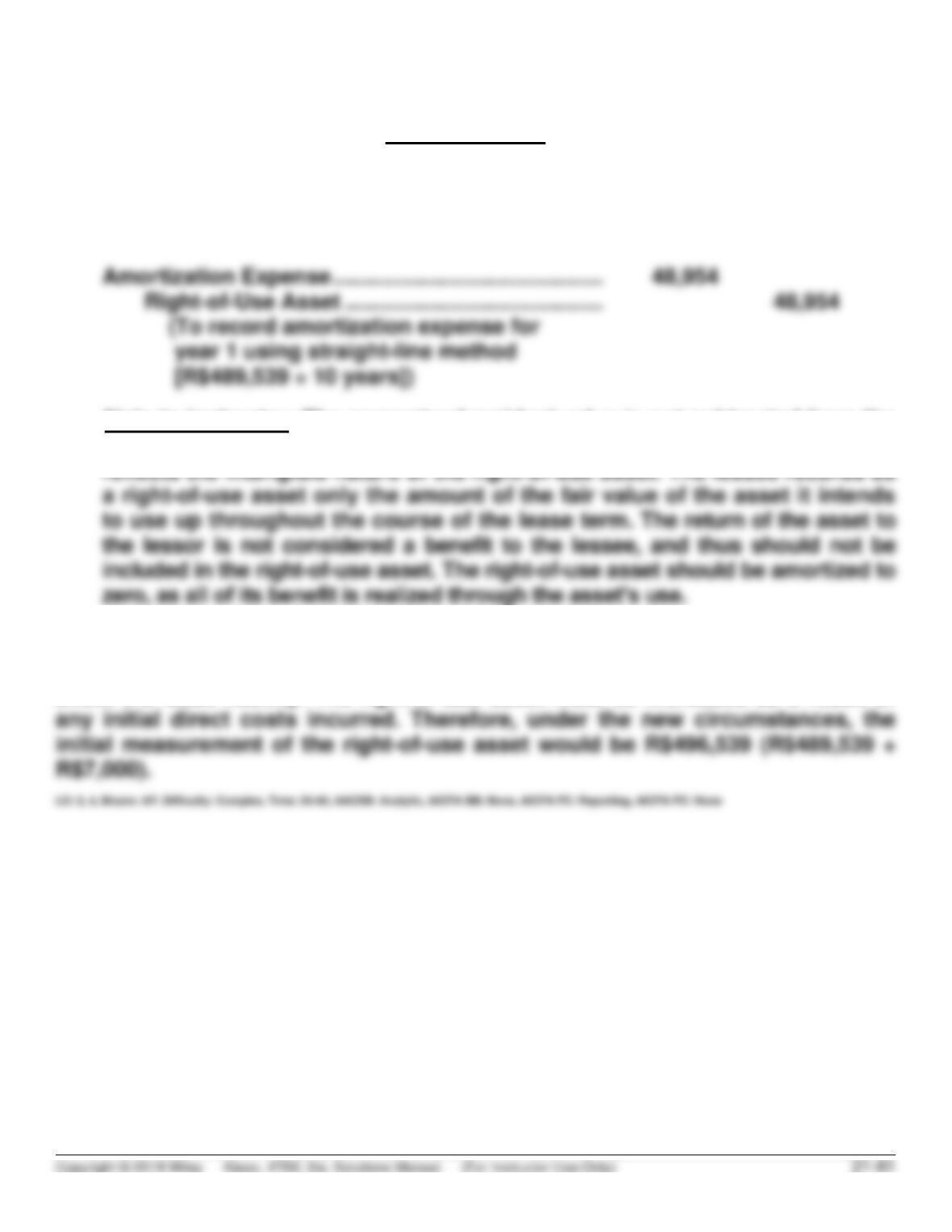

Interest Expense …………………………………………….. 21,477

Lease Liability ………………………………………….. 21,477

(To record accrual of annual interest on

lease obligation)

Note to instructor: The guaranteed residual value is not subtracted from the

right-of–use asset for purposes of determining the amortizable base. This

(d) The document preparation costs are considered initial direct costs. As such,

they will impact the initial measurement of the right-of-use asset, but will not

affect the lease liability. The right-of-use asset must be increased as a result of

PROBLEM 21.9

(a) The lease is a sales-type lease because: (1) the lease term exceeds 75% of

the asset’s estimated economic life (10/12 = 83%), and (2) the present value of

the lease payments is greater than 90% of the fair value of the asset, as

calculated below:

¥ 40,000 Annual rental payment

1. Present value of an annuity-due of $1 for

10 periods discounted at 8% ………………………………. 7.24689

Annual lease payment ……………………………………………. X ¥ 40,000

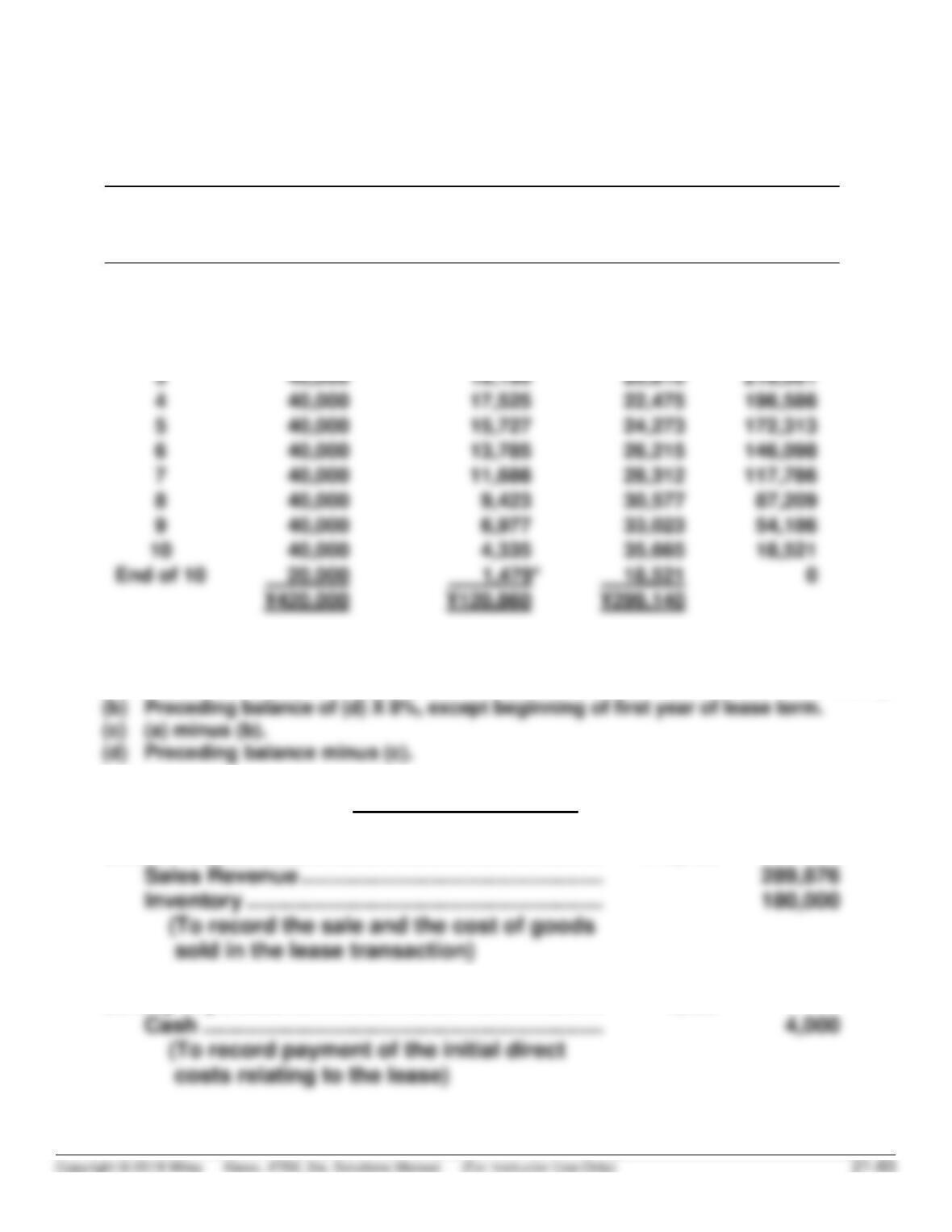

2. Sales revenue is ¥289,876 (the present value of the 10 annual lease

payments) or, the lease receivable of ¥299,140 minus the PV of the un-

guaranteed residual value of ¥9,264.

3. Cost of goods sold is ¥170,736 (the ¥180,000 cost of the asset less the

PROBLEM 21.9 (Continued)

(b) Kobayashi Group (Lessor)

Lease Amortization Schedule

Annuity-Due Basis, Unguaranteed Residual Value

Beginning

of Year

Annual Lease

Payment Plus

Residual Value

Interest (8%)

on Lease

Receivable

Lease

Receivable

Recovery

Lease

Receivable

(a)

(b)

(c)

(d)

Initial PV

¥299,140

1

¥ 40,000

¥ 0

¥ 40,000

259,140

2

40,000

20,731

19,269

239,871

3

40,000

4

5

172,313

6

40,000

7

8

40,000

9

40,000

33,023

*Rounding is ¥3.

(a) Annual lease payment (and return of expected residual value at end of the lease).

(c) Beginning of the Year

Lease Receivable …………………………………………… 299,140

Cost of Goods Sold ………………………………………… 170,736

Selling Expenses ……………………………………………. 4,000

PROBLEM 21.9 (Continued)

Cash ………………………………………………………………… 40,000

Lease Receivable ………………………………………… 40,000

(To record receipt of the first lease

payment)

End of the Year

Lease Receivable ……………………………………………… 20,731

PROBLEM 21.10

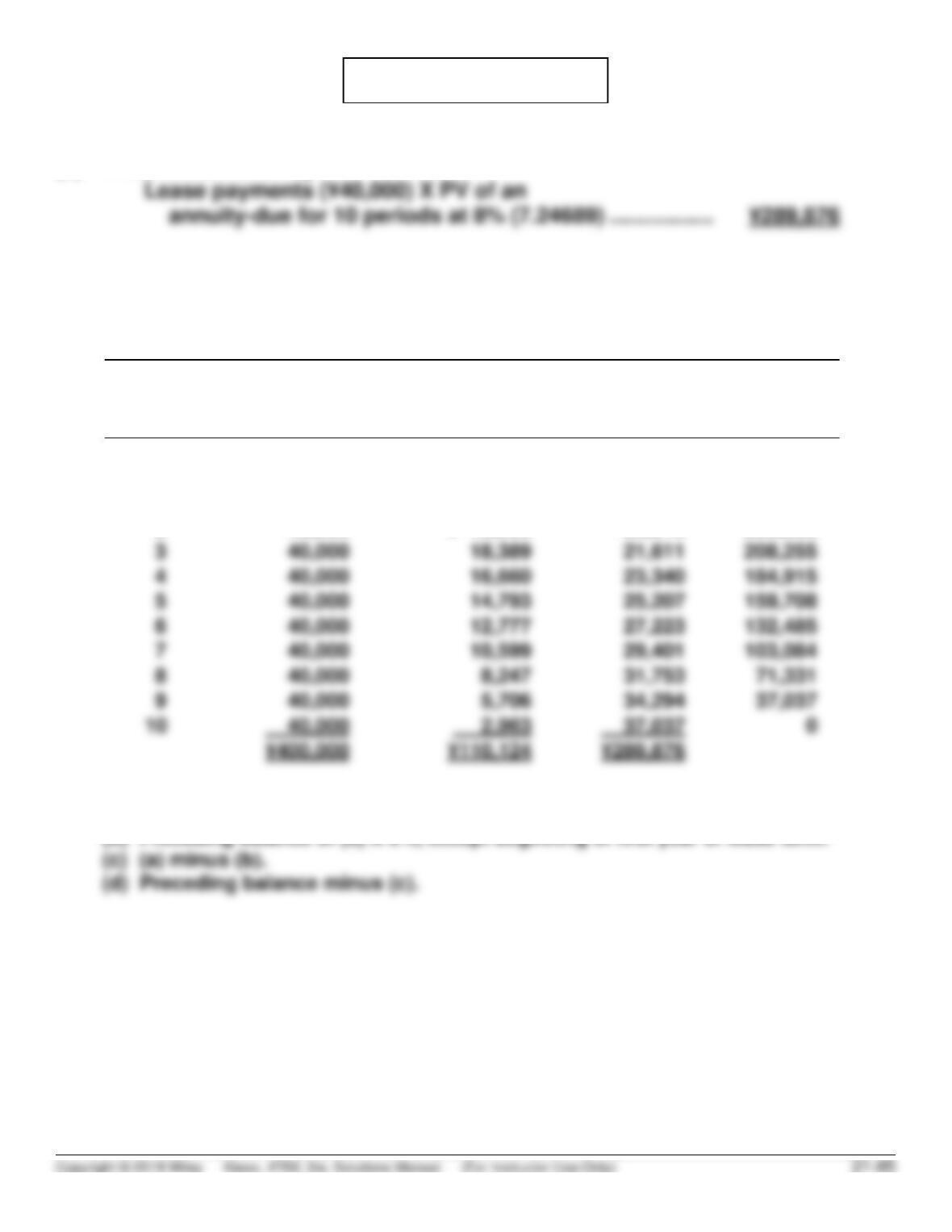

(a) Initial Lease Liability:

(b) JAL (Lessee)

Lease Amortization Schedule

(Annuity-due basis and URV)

Beginning

of Year

Annual Lease

Payment

Interest (8%)

on Lease

Liability

Reduction

of Lease

Liability

Lease

Liability

(a)

(b)

(c)

(d)

Initial PV

—

—

—

¥289,876

1

¥ 40,000

—

¥ 40,000

249,876

2

40,000

¥ 19,990

20,010

229,866

3

208,255

4

184,915

5

40,000

25,207

6

132,485

7

103,084

8

40,000

31,753

9

(a) Annual lease payment required by lease contract.

(b) Preceding balance of (d) X 8%, except beginning of first year of lease term.

PROBLEM 21.10 (Continued)

(c) Lessee’s journal entries:

Beginning of the Year

Right-of–Use Asset …………………………………………. 289,876

Lease Liability ………………………………………….. 289,876

End of the Year

Interest Expense …………………………………………….. 19,990

Lease Liability ………………………………………….. 19,990

PROBLEM 21.11

(a) The lease agreement satisfies the 90% of fair value requirement (calculation

below).

PV of Lease Payments:

PV of rental payments, $30,300 X 7.24689* …………………. $219,581

For the lessor, it is a sales-type lease.

Note to Instructor: For purposes of measuring the initial lease liability, only

PV of Lease Liability:

PV of rental payments, $30,300 X 7.24689* …………………. $219,581

PROBLEM 21.11 (Continued)

(b) January 1, 2019

Lessee:

Right-of–Use Asset …………………………………………. 221,897

Lease Liability ………………………………………….. 221,897

(see calculation in part a)

January 1, 2019

Lessor:

Lease Receivable …………………………………………… 242,741

December 31, 2019

Lessee:

Interest Expense …………………………………………….. 15,328

December 31, 2019

Lessor:

Lease Receivable ……………………………………………… 16,995

PROBLEM 21.11 (Continued)

(c) In both (1) and (2), the lessee is no longer obligated or expected to make any

(d) While the lessor still includes even an unguaranteed residual value in the

calculation of a lease receivable under a finance (sales-type) lease, the lack

PROBLEM 21.12

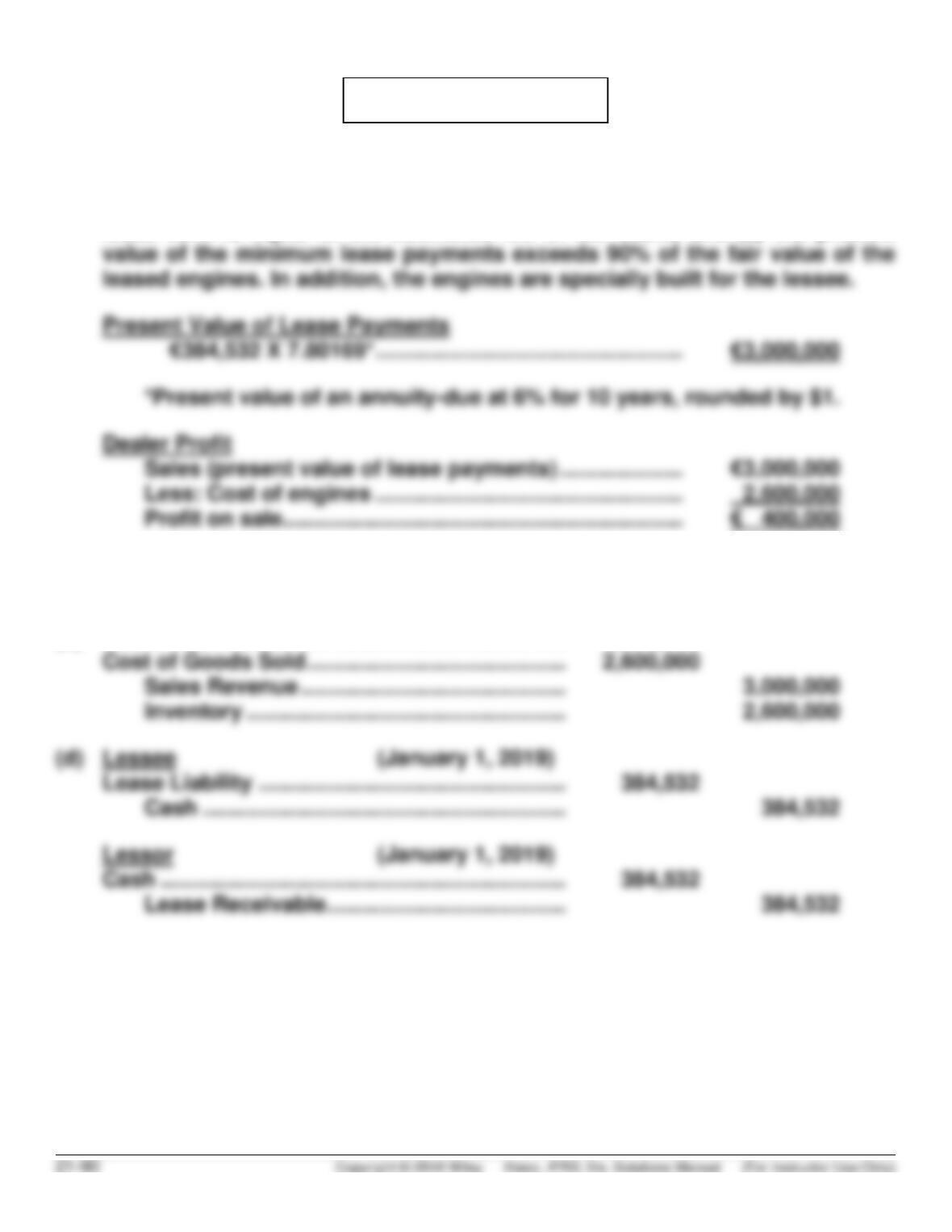

(a) The lease should be treated as a sales-type lease by Ewing. The lease

qualifies for because: (1) title to the engines transfers to the lessee, (2) the

lease term is equal to the estimated life of the asset, and (3) the present

(b) Right-of–Use Asset ……………………………………. 3,000,000

Lease Liability …………………………………….. 3,000,000

(c) Lease Receivable ……………………………………… 3,000,000

PROBLEM 21.12 (Continued)

(e) WINSTON INDUSTRIES/EWING

Lease Amortization Schedule

Date

Annual

Lease

Receipt/

Payment

Interest on

Receivable/

Liability at 6%

Reduction in

Receivable/

Liability

Lease

Receivable/

Liability

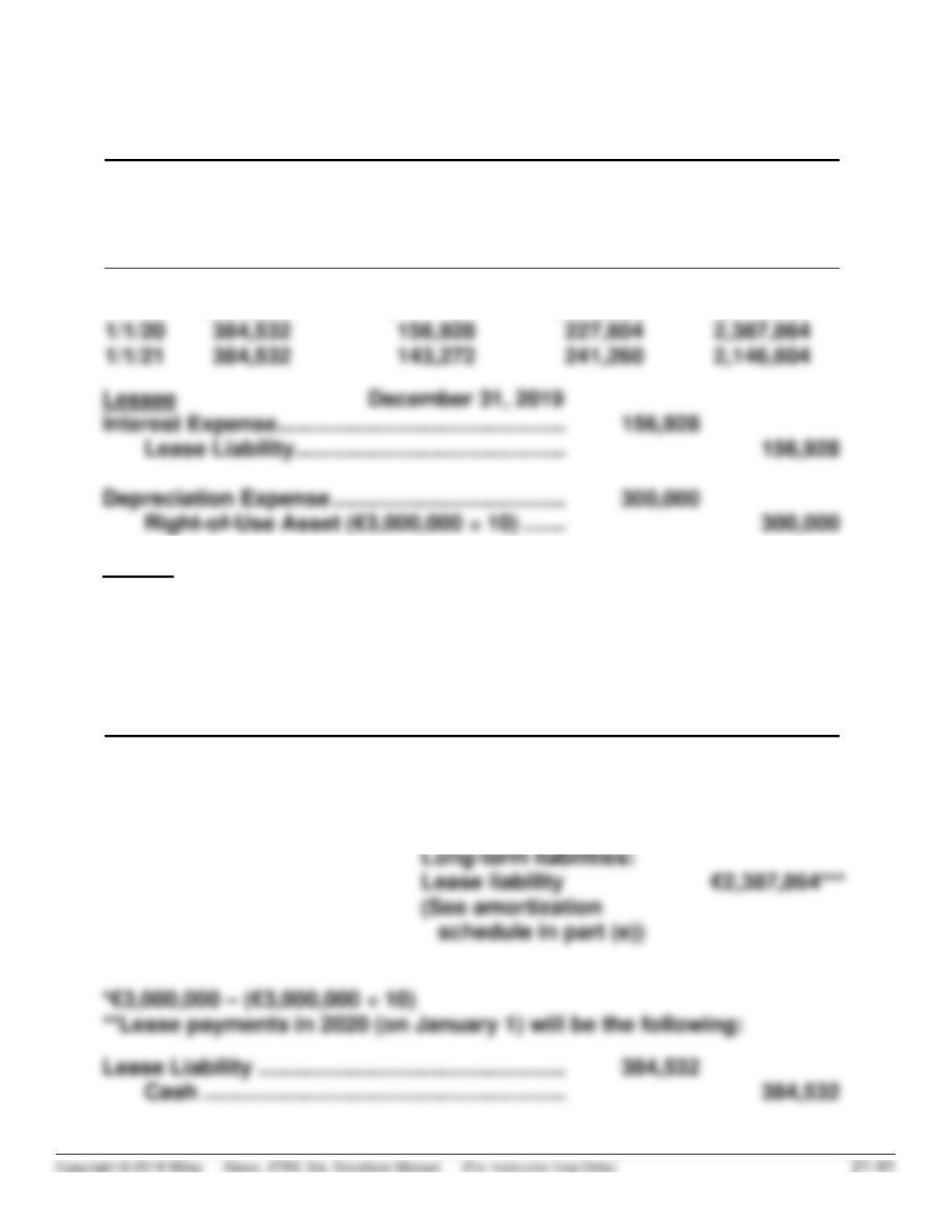

1/1/19

€3,000,000

1/1/19

€384,532

€ –0–

€384,532

2,615,468

2,146,604

Lessor December 31, 2017

Lease Receivable ……………………………………… 156,928

Interest Revenue …………………………………. 156,928

(f) WINSTON INDUSTRIES

Statement of Financial Position (Partial)

December 31, 2019

Non-current assets:

Current liabilities:

Right-of–Use

asset

€2,700,000*

Lease liability

€384,532**

PROBLEM 21.12 (Continued)

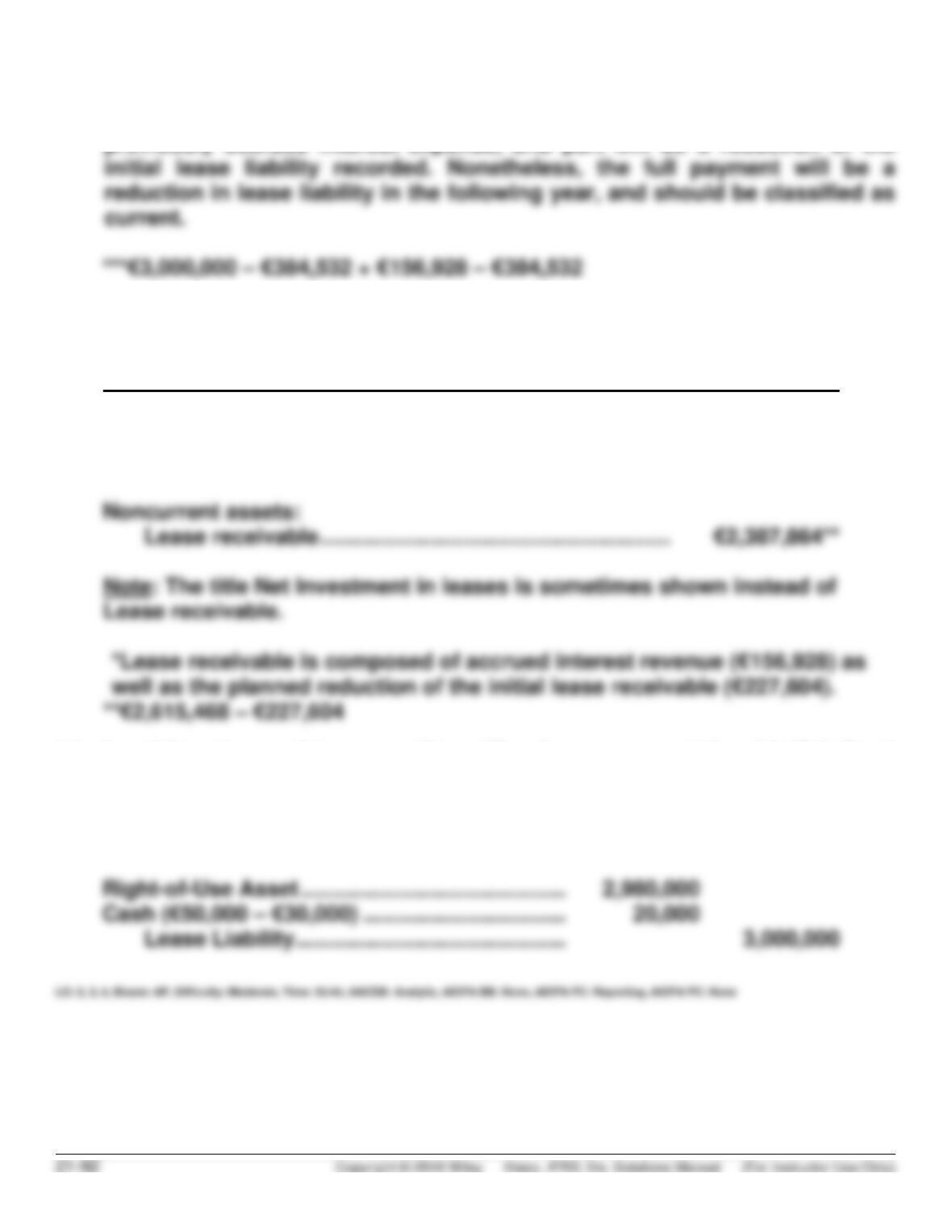

Part of the reduction in the lease liability will be attributable to the

previously accrued interest expense, and part will be a reduction of the

EWING SA

Statement of Financial Position (Partial)

December 31, 2019

Assets

Current assets:

Lease receivable …………………………..……………………. € 384,532*

(g) Legal fees incurred in connection with a lease are considered initial direct

costs of the lease, and should be capitalized as part of the right–of–use asset. In

contrast, lease incentives reduce the initial value of the right–of-use asset.

However, neither initial direct costs nor lease incentives affect the value of the

lease liability. Thus, the entry to initially record the lease is as follows:

PROBLEM 21.13

(a) 1. £ 20,027 Interest expense (See amortization schedule)

£ 52,174 Depreciation expense (£313,043 ÷ 6 = £52,174)

2. Current liabilities:

£ 62,700 Lease liability

4. Current liabilities:

£ 42,673 Lease liability

Long-term liabilities:

PROBLEM 21.13 (Continued)

2. Current liabilities:

£ 47,680 Lease liability (£42,673 + £5,007)

3. £ 19,174 Interest expense

[(£20,027 – £5,007) + (£16,614 X 3/12) =

[£15,020 + £4,154 = £19,174]

£ 52,174 Depreciation expense (£313,043 ÷ 6 = £52,174)

4. Current liabilities:

£ 50,240 Lease liability

PROBLEM 21.14

(a) The lease will be classified as an operating lease for the lessor. The lease

does not transfer ownership at the end of the lease term, does not have a

bargain purchase option, and the asset is not specialized. In addition,

neither the 75% test (3 ÷ 8 = 37.5%) nor the 90% test (calculation below) are

met.

PV of Lease Payments:

(b)

GARCIA SA

Lease Amortization Schedule

Annuity-Due Basis

Date

Annual

Payment

Interest (6%) on

Liability

Reduction

of Lease

Liability

Lease Liability

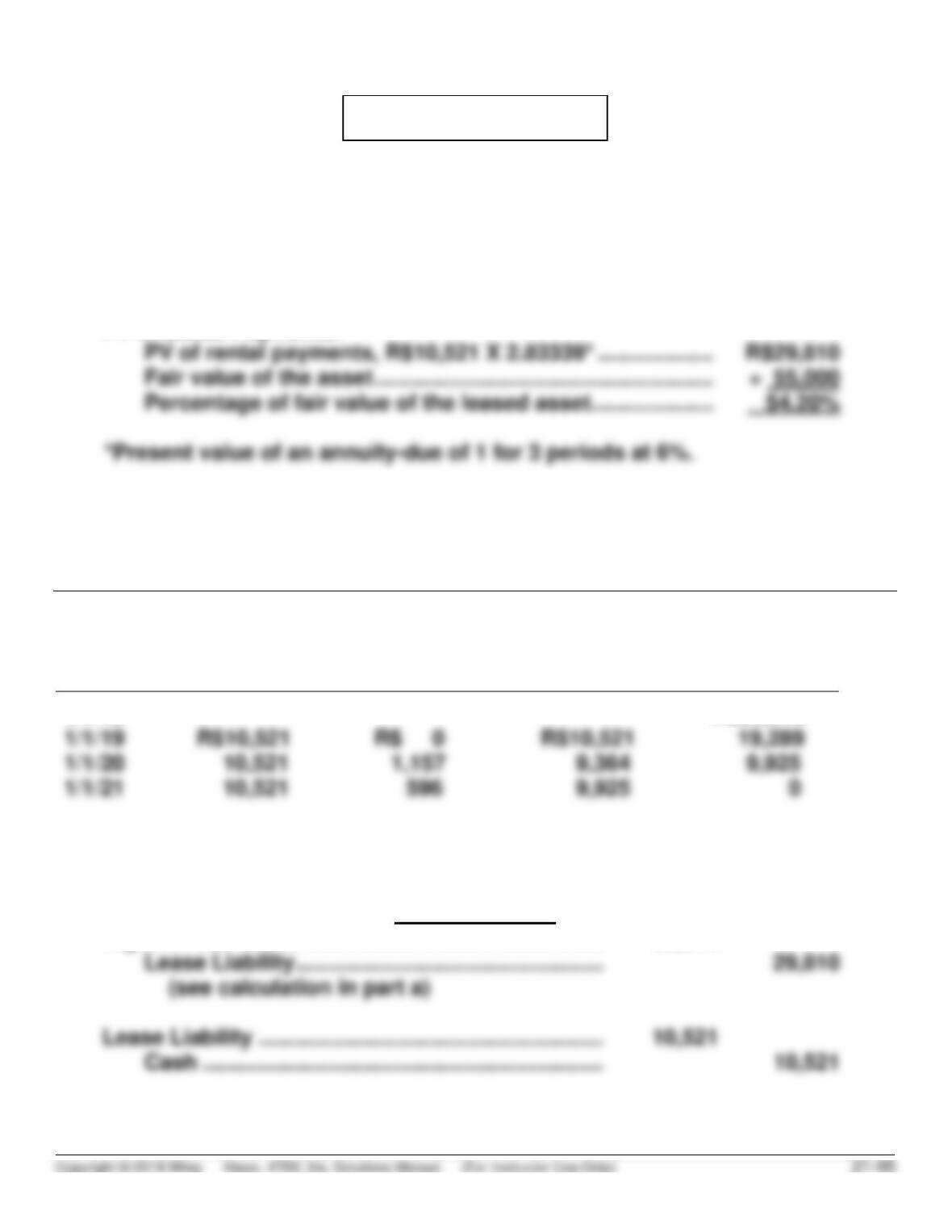

1/1/19

R$29,810

(c)

January 1, 2019

Right-of–Use Asset …………………………………………. 29,810

PROBLEM 21.14 (Continued)

December 31, 2019

Interest Expense …………………………………………….. 1,157

(d)

January 1, 2019

Cash ……………………………………………………………… 10,521

Unearned Lease Revenue …………………………. 10,521

(e) When a lessee elects to use the short-term lease option, the company need

not recognize a lease liability or right-of-use asset on its books. Instead, the lessee

expenses payments as they are made.

As a result, if the lease were only 1 year, Garcia’s only entry for the lease would be

the following:

January 1, 2019

PROBLEM 21.15

(a) The lease is an operating lease to the lessor because:

1. it does not transfer ownership,

2. it does not contain a bargain purchase option,

5. it does not meet the specialized asset test.

At least one of the five tests would have had to be satisfied for the lease to

be classified as other than an operating lease.

(b) Lessee’s Entries

1/1/19

PROBLEM 21.15 (Continued)

ABRIENDO CONSTRUCTION

Lease Amortization Schedule (partial)

Annuity-Due Basis

Date

Annual

Payment

Interest (8%) on

Liability

Reduction

of Lease

Liability

Lease Liability

1/1/19

R$209,375

1/1/19

R$48,555

R$ 0

R$48,555

160,820

12/31/19

Interest Expense ……………………………………………….. 12,866

Lease Liability …………………………………………….. 12,866

PROBLEM 21.15 (Continued)

12/31/19

Depreciation Expense ……………………………………….. 32,143

Accumulated Depreciation—Leased Equipment

(c) Abriendo as lessee must record both a lease liability, as well as a right-of-use

asset. The first cash payment is a total reduction of the lease liability (as no

time has passed, and thus no interest has accrued). At the end of the year,

Abriendo must make an accrual for the annual lease expense. In this case,

Cleveland as lessor must disclose in the statement of financial position or in

the notes the cost of the leased crane (R$240,000) and the accumulated

depreciation of R$32,143 separately from assets not leased. Additionally,

Cleveland must disclose in the notes the minimum future rentals as a total of