CA 7.2 (Continued)

Kimmel should report interest revenue from the notes receivable on its income statement for the

CA 7.3

(1) Allowances and charge-offs. Method (a) is recommended. In the case of this company which

has a large number of relatively small sales transactions, it is practicable to give effect currently to

(2) Collection expenses. Method (a) or (b) is recommended. In the case of this company, one strong

argument for method (a) is that it is advisable to have the Bad Debt Expense account show the full

amount of expense relating to efforts to collect and failure to collect balances receivable. On the

(3) Recoveries. Method (c) is recommended. This method treats the recovery as a correction of a

previous write-off. It produces an allowance account that reflects the net experience with bad

CA 7.4

Part 1

Since Wallace Company is a calendar-year company, six months of interest should be accrued on

cash is received.

CA 7.4 (Continued)

Part 2

(a) The allowance method based on the balance in accounts receivable is consistent with the expense

recognition principle. It attempts to value accounts receivable at the amount expected to be

collected and records bad debt expense in periods when credit quality decreases. The method is

used.

(b) On Wallace’s statement of financial position, the allowance for doubtful accounts is presented as a

contra account to accounts receivable with the resulting difference representing the net accounts

LO: 2,4, Bloom: AP, Difficulty: Moderate, Time: 25-30, AACSB: Analytic, AICPA BB: None, AICPA FC: Reporting, AICPA PC: None

CA 7.5

(a) VALASQUEZ SA

Accounts Receivable Aging Schedule

May 31, 2019

Proportion

of Total

Amount in

Category

Probability of

Non-Collection

Estimated

Uncollectible

Amount

Not yet due

.680

R$1,088,000

.010

R$10,880

Less than 30 days past due

.150

.035

30 to 60 days past due

.080

.050

61 to 120 days past due

.050

.090

121 to 180 days past due

.025

.300

Over 180 days past due

.015

.800

CA 7.5 (Continued)

(b) VALASQUEZ SA

Analysis of Allowance for Doubtful Accounts

May 31, 2019

June 1, 2018 balance ………………………………………

R$ 43,300

Bad debt expense accrual (R$4,000,000 X .04) ….

160,000

Balance before write-offs of bad accounts ……….

Write-offs of bad accounts ………………………………

Balance before year-end adjustment ………………..

Estimated uncollectible amount ………………………

Bad Debt Expense …………………………………………..

5,780

Allowance for Doubtful Accounts ……………

(c)

(1) Steps to Improve

Accounts Receivable Situation

(2) Risks and Costs Involved

Establish more selective credit-

granting policies, such as more

restrictive credit requirements or

This policy could result in lost sales

and increased costs of credit

evaluation. The company may be all

CA 7.6

(a) The appropriate valuation basis of a note receivable at the date of sale is its discounted present

value of the future amounts receivable for principal and interest using the customer’s market rate

of interest, if known or determinable, at the date of the equipment’s sale.

(b) Corrs should increase the carrying amount of the note receivable by the effective-interest revenue

(c) 1. For notes receivable not sold, Corrs should recognize bad debt expense. The expense equals

the adjustment required to bring the balance of the allowance for doubtful accounts equal to

the estimated uncollectible amounts less the fair values of recoverable equipment.

CA 7.7

(a) 1. It was not possible to determine the machine’s fair value directly, so the sales price of the

2. Rolen reports 2019 interest revenue determined by multiplying the note’s carrying amount at

September 30, 2019, times the buyer’s market rate of interest at the date of issue, times three–

twelfths. Rolen should recognize that there is an interest factor implicit in the note, and this

interest is earned with the passage of time. Therefore, interest revenue for 2019 should include

three months’ revenue. The rate used should be the market rate established by the original

present value, and this is applied to the carrying amount of the note.

(b) To report the sale of the note receivable with guarantee, Rolen should increase a liability to the

factor by the carrying amount of the note, increase cash by the amount received, record a

CA 7.8

(a) 1. For the interest-bearing note receivable, the interest revenue for 2019 should be determined by

2. For the zero-interest-bearing note receivable, the interest revenue for 2019 should be deter-

mined by multiplying the carrying value of the note by the prevailing rate of interest at the date

of the note by one third (September 1, 2019 to December 31, 2019). The carrying value of the

note at September 1, 2019 is the face amount discounted for two years at the prevailing interest

rate from the maturity date of August 31, 2021 back to the issuance date of September 1, 2019.

Interest, even if unstated, accrues with the passage of time, and it should be accounted for as an

element of revenue over the life of the note receivable.

(b) The interest-bearing note receivable should be reported at December 31, 2019 as a current asset

at its principal (face) amount.

CA 7.9

The controller of Engone Company cannot justify the manner in which the company has accounted for

the transaction in terms of sound financial accounting principles.

Several problems are inherent in the sale of Henderson Enterprises stock to Bimini Inc. First, the issue

of whether an arm’s-length transaction has occurred may be raised. The controller stated that the stock

has not been marketable for the past six years. Thus, the recognition of revenue is highly questionable

in view of the limited market for the stock; i.e., has an exchange occurred?

CA 7.9 (Continued)

For a gain to occur, the interest imputation must result in an interest rate of about 5% or less. To

illustrate:

Present value of an annuity of £1 at 5% for 10 years = 7.72173; thus the present value of ten

CA 7.10

To: Mark Price, Branch Manager

From: Accounting Major

Date: October 3, 2019

Subject: Shortage in the Accounts Receivable Account

While performing a routine test on accounts receivable balances today, I discovered a $58,000 shortage.

I believe that this matter deserves your immediate attention.

To compute the shortage, I determined that the accounts receivable balance should have been based

on the amount of inventory which has been sold. When we opened for business this year, we

purchased $360,000 worth of merchandise inventory, and this morning, the balance in this account was

$90,000.

CA 7.11

(a) No, the controller should not be concerned with Marvin Company’s growth rate in estimating the

allowance. The accountant’s proper task is to make a reasonable estimate of bad debt expense.

In making the estimate, the controller should consider the previous year’s write-offs and also an-

ticipate economic factors which might affect the company’s industry and influence Marvin’s current

FINANCIAL REPORTING PROBLEM

(a) M&S’s cash and cash equivalents include short-term deposits with

banks and other financial institutions, with an initial maturity of three

months or less and credit card debtor’s receivable within 48 hours.

The carrying amount of these assets approximates their fair value.

COMPARATIVE ANALYSIS CASE

Puma adidas

€ millions € millions

(a) 338.8

known amount of cash and

Cash and cash equivalents

12/31/15

Cash and cash equivalents

1,365

Cash and cash equivalents

12/31/15

Cash and cash equivalents

(b) 521.9

38.8

Trade receivables 12/31/15

Value adjustments

2,198

149

Accounts receivable, gross

12/31/15 accumulated

allowances for doubtful

receivables

FINANCIAL STATEMENT ANALYSIS CASE 1

(a) Cash may consist of funds on deposit at the bank, negotiable instru–

ments such as money orders, certified checks, cashier’s checks,

personal checks, bank drafts, and money market funds that provide

checking account privileges.

(b) Cash equivalents are short-term, highly liquid investments that are

(c) A compensating balance is that portion of any cash deposit main–

tained by an enterprise which constitutes support for existing borrow–

ing arrangements with a lending institution.

(d) Short-term investments are the investments held temporarily in place

of cash and can be readily converted to cash when current financing

FINANCIAL STATEMENT ANALYSIS CASE 1 (Continued)

The major differences between cash equivalents and short-term

investments are (1) cash equivalents typically have shorter maturity

(e) Petrochina would record a loss of RMB30,000,000 as revealed in the

following entry to record the transaction:

Cash ……………………………………………………….

345,000,000

Loss on Sale of Receivables …………………………..

30,000,000

Recourse Liability …………………………..

15,000,000

FINANCIAL STATEMENT ANALYSIS CASE 2

Part 1

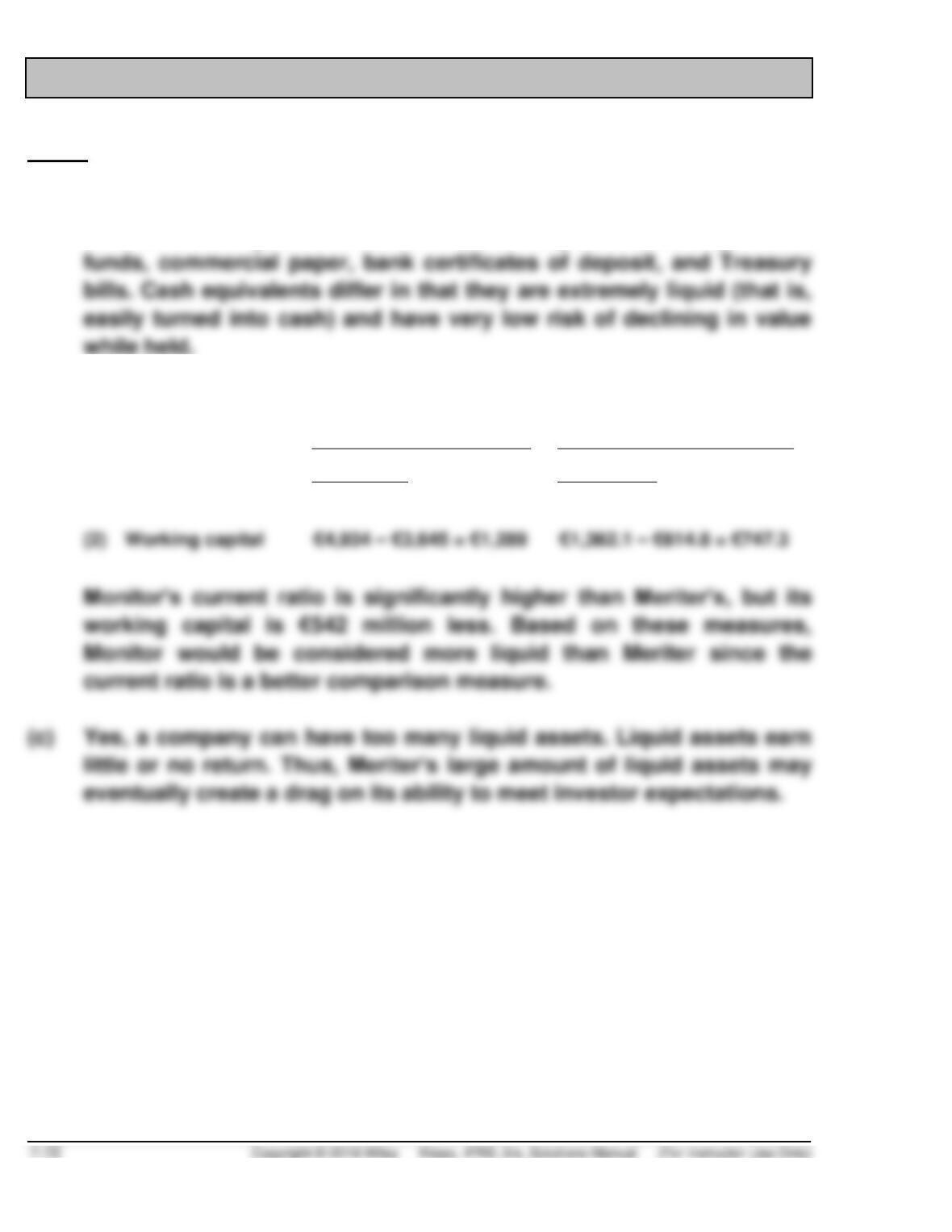

(a) Cash equivalents are short-term, highly liquid investments that can be

converted into specific amounts of cash. They include money market

(b)

(in millions)

Meriter

Monitor

(1) Current ratio

€4,934

= 1.4

€1,362.1

= 2.2

€3,645

€614.8

FINANCIAL STATEMENT ANALYSIS CASE 2 (Continued)

Part 2

(a)

Accounts Receivable

Turnover

€10,799

=

€10,799

= 7.01 times

(€1,624 + €1,459)/2

€1,541.5

(c) Accounts receivable is reduced by the amount of bad debts in the

allowance account. This makes the denominator of the turnover ratio

ACCOUNTING, ANALYSIS, AND PRINCIPLES

ACCOUNTING

(a) Accounts Receivable:

Beginning balance ………………………… € 46,000

Allowance for Doubtful Accounts:

Beginning balance ………………………… € 550

Write-offs ……………………………………… (1,600)

(b) Current assets section of December 31, 2019 Flatiron Pub statement of

financial position

Accounts receivable (net of €1,575

allowance for uncollectibles ……….. €61,425

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

ANALYSIS

(a) 2018 current ratio = (€2,000 + €46,000 – €550 + €8,500) ÷ €37,000 = 1.51

2019 current ratio = €76,285 ÷ €44,660 = 1.71

the current ratio and accounts receivable turnover.

PRINCIPLES

The expense recognition principle requires that bad debt expense be

recorded in the period of the sale. Otherwise, income will be overstated by

RESEARCH CASE

(a) IFRS 9, paragraph 3.2 addresses derecognition of financial assets.

(b) According to 3.2.3 An entity shall derecognise a financial asset when,

and only when:

3.2.4 An entity transfers a financial asset if, and only if, it either:

(a) transfers the contractual rights to receive the cash flows of the

3.2.5 When an entity retains the contractual rights to receive the cash flows

of a financial asset (the ‘original asset’), but assumes a contractual

obligation to pay those cash flows to one or more entities (the

‘eventual recipients’), the entity treats the transaction as a transfer of

RESEARCH CASE (Continued)

(c) The entity has an obligation to remit any cash flows it collects

on behalf of the eventual recipients without material delay. In

(c) Transfers that qualify for derecognition – According to paragraph

3.2.10 If an entity transfers a financial asset in a transfer that qualifies

for derecognition in its entirety and retains the right to service the

(d) Paragraph 3.2.16 addresses continuing involvement…

If an entity neither transfers nor retains substantially all the risks and

rewards of ownership of a transferred asset, and retains control of the

transferred asset, the entity continues to recognise the transferred

asset to the extent of its continuing involvement. The extent of the

entity’s continuing involvement in the transferred asset is the extent to

which it is exposed to changes in the value of the transferred asset.

For example:

(a) When the entity’s continuing involvement takes the form of

guaranteeing the transferred asset, the extent of the entity’s

RESEARCH CASE (Continued)

(b) When the entity’s continuing involvement takes the form of a

written or purchased option (or both) on the transferred asset,

(c) When the entity’s continuing involvement takes the form of a

3.2.17 When an entity continues to recognise an asset to the extent of its

continuing involvement, the entity also recognises an associated

liability. Despite the other measurement requirements in this

Standard, the transferred asset and the associated liability are

3.2.18 The entity shall continue to recognise any income arising on the

transferred asset to the extent of its continuing involvement and

shall recognise any expense incurred on the associated liability.

3.2.19 For the purpose of subsequent measurement, recognised changes

RESEARCH CASE (Continued)

3.2.20 If an entity’s continuing involvement is in only a part of a

financial asset (eg when an entity retains an option to repurchase part

of a transferred asset, or retains a residual interest that does not result

3.2.14 apply. The difference between:

(a) the carrying amount (measured at the date of derecognition)

allocated to the part that is no longer recognised and

(b) the consideration received for the part no longer recognised

shall be recognised in profit or loss.

3.2.21 If the transferred asset is measured at amortised cost, the option in

GAAP CONCEPTS and APPLICATION

7.1 Both the IASB and the FASB have indicated that they believe that

financial statements would be more transparent and understandable if

7.2 Key similarities relate to (1) the definition used for cash equivalents,

(2) accounting and reporting issues related to recognition and

measurement of receivables, such as the use of allowance accounts,

how to record trade and sales discounts, use of percentage of sales

and receivables methods, pledging, and factoring, and (3) both