EXERCISE 13.6 (Continued)

(b) Accrued liability at year-end:

2018

2019

Vacation

Payable

Sick Pay

Payable

Vacation

Payable

Sick Pay

Payable

Jan. 1 balance

€ 0

€ 0

€ 8,640

€1,728

€8,640

€1,728

(1)

9 employees X €12.00/hr. X 8 hrs./day X 10 days =

€ 8,640

(2)

9 employees X €12.00/hr. X 8 hrs./day X (6–4) days =

€ 1,728

€10,224

EXERCISE 13.7 (25–30 minutes)

(a)

2018

To accrue the expense and liability for vacations

Salaries and Wages Expense …………….

Salaries and Wages Payable ………

To record sick leave paid

Salaries and Wages Expense …………….

To record vacation time paid

EXERCISE 13.7 (Continued)

2019

To accrue the expense and liability for vacations

Salaries and Wages Expense…………….

9,864

(3)

Salaries and Wages Payable ……..

9,864

To record sick leave paid

Salaries and Wages Expense…………….

4,680

(4)

Cash ………………………………………..

4,680

To record vacation time paid

Salaries and Wages Expense…………….

Salaries and Wages Payable ……………..

8,359

(5)

Cash ………………………………………..

8,424

(6)

(1) 9 employees X €12.90/hr. X 8 hrs./day X 10 days = €9,288

(2) 9 employees X €12.00/hr. X 8 hrs./day X 4 days = €3,456

(b)

Accrued liability at year-end:

2018

2019

Jan. 1 balance

€ 0

€ 9,288

+ accrued

Dec. 31 balance

(1)

(2)

(1)

9 employees X €12.90/hr. X 8 hrs./day X 10 days …..

€ 9,288

(2)

9 employees X €12.90/hr. X 8 hrs./day X 1 day ………

€ 929

EXERCISE 13.8 (5–7 minutes)

(a)

June 30

Sales Revenue …………………………………………………

23,700

Sales Taxes Payable ………………………………

23,700

Computation:

+ R$153,700) …………………………………….

÷ 1.06) ……………………………………………..

(b) If the adjusting entry related to a VAT rather than sales tax, it would be

recorded as follows:

Sales Revenue ……………………………………………………….

Value Added Taxes Payable …………………………..

EXERCISE 13.9 (10 minutes)

(a)

Cash (€40,000 + €6,000) …………………………………………..

46,000

Sales Revenue ………………………………………………..

40,000

Value Added Taxes Payable (€40,000 X 15%) ……

6,000

(b)

Eastwood Ranchers does not have a net cash outlay related to the

EXERCISE 13.10 (10–15 minutes)

Salaries and Wages Expense …………………………………..

340,000

Withholding Taxes Payable ……………………………..

80,000

Social Security Taxes Payable* ………………………..

27,200

Union Dues Payable ………………………………………..

Cash ………………………………………………………………

223,800

Payroll Tax Expense ………………………………………………..

Social Security Taxes Payable …………………………

(See previous computation.)

EXERCISE 13.11 (15–20 minutes)

(a)

Computation of taxes

Factory

Wages …………………………..…….

€140,000

Social security taxes…………….

Total cost …………………………….

Wages …………………………..…….

Social security taxes…………….

Total cost …………………………….

Wages …………………………..…….

Social security taxes…………….

Total cost …………………………….

EXERCISE 13.11 (Continued)

Schedule

Total

Factory

Sales

Administrative

Wages

€208,000

€140,000

€32,000

€36,000

Social Security

(b)

Factory Payroll:

Salaries and Wages Expense …………………..

140,000

Withholding Taxes Payable………………

Social Security Taxes Payable ………….

Cash ……………………………………………….

Payroll Tax Expense ……………………………….

11,200

Social Security Taxes Payable ………….

Sales Payroll:

Salaries and Wages Expense …………………..

32,000

Withholding Taxes Payable………………

7,000

Social Security Taxes Payable ………….

2,560

Cash ……………………………………………….

Payroll Tax Expense ……………………………….

Social Security Taxes Payable ………….

Administrative Payroll:

Salaries and Wages Expense …………………..

36,000

Withholding Taxes Payable………………

6,000

Social Security Taxes Payable ………….

2,880

Cash ……………………………………………….

Payroll Tax Expense ……………………………….

Social Security Taxes Payable ………….

2,880

EXERCISE 13.12 (10–15 minutes)

July 10, 2019

Cash (200 X £4,000) …………………………………………………

800,000

Sales Revenue ………………………………………………..

800,000

Warranty Expense …………………………………………………..

Inventory …………………………..…………………………..

Warranty Expense …………………………………………………..

Warranty Liability (£66,000-£17,000) …………………

EXERCISE 13.13 (15–20 minutes)

At Sale

(a)

Cash ………………………………………………………………………

3,000,000

Sales Revenue ………………………………………………..

3,000,000

Warranty Expense …………………………………………………..

Cash, Supplies, Wages Payable ……………………….

At Sale

(b)

Cash ………………………………………………………………………

3,000,000

Sales Revenue ………………………………………………..

2,944,000

Unearned Warranty Revenue …………………………..

Warranty Expense …………………………………………………..

Cash, Supplies, Wages Payable ……………………….

EXERCISE 13.13 (Continued)

December 31, 2019

Unearned Warranty Revenue …………………………..

Warranty Revenue ………………………………………….

(€56,000 ÷ 2)

EXERCISE 13-14 (15–20 minutes)

Inventory of Premiums (8,800 X $.80) ……………………….

7,040

Cash ………………………………………………………………

7,040

During 2019

Cash (110,000 X $3.30) …………………………………………….

Sales Revenue ………………………………………………..

Premium Expense …………………………………………………..

Inventory of Premiums [(44,000 ÷ 10) X $.80] …….

Premium Liability ……………………………………………

*[(110,000 X 60%) – 44,000] ÷ 10 X $.80 = 1,760

EXERCISE 13.15 (15–20 minutes)

(1) Lease termination penalties are included. The ¥400,000 penalty to break

the lease should therefore be included.

(3) Costs of training staff are excluded.

(4) Use of an outplacement firm to assist with the terminations are

EXERCISE 13.16 (15–20 minutes)

(a) A restructuring is a program that is planned and controlled by

management and materially changes either (1) the scope of a business

(b) The two provisions are described that the company (1) has a detailed

formal plan for the restructuring; and (2) raises a valid expectation to

those affected by implementation or announcement of the plan.

EXERCISE 13.17 (20–30 minutes)

1. The IASB requires that, when some amount within the range of ex–

pected loss appears at the time to be a better estimate than any other

2. The loss should be accrued for €6,000,000. The potential insurance

3. This is a contingent asset because the amount to be received will be in

excess of the book value of the plant. Contingent assets are not

EXERCISE 13.18 (25–30 minutes)

(a)

January 1, 2019

Depot …………………………..…………………………………………

600,000

Cash ……………………………………………………….

600,000

Depot …………………………..…………………………………………

Environmental Liability …………………………..

(b)

December 31, 2019

Depreciation Expense ……………………………………………..

60,000

Accumulated Depreciation—Depot …………………..

60,000

Depreciation Expense ……………………………………………..

Accumulated Depreciation—Depot …………………..

Interest Expense …………………………………………………….

(c)

December 31, 2028

Environmental Liability ……………………………………………

70,000

Loss on Settlement of Environmental Liability ………….

10,000

EXERCISE 13.19 (25–35 minutes)

1.

Liability for stamp redemptions, 12/31/18

$13,000,000

Cost of redemptions redeemed in 2019

(6,000,000)

2.

Total coupons issued

$800,000

Redemption rate

60%

To be redeemed

480,000

Handling charges ($480,000 X 10%)

48,000

Total cost

Total payments to retailers

3.

Boxes

700,000

Redemption rate

70%

Coupons to be redeemed (490,000 – 250,000)

240,000

Cost ($6.50 – $4.00)

$2.50

EXERCISE 13.20 (20–30 minutes)

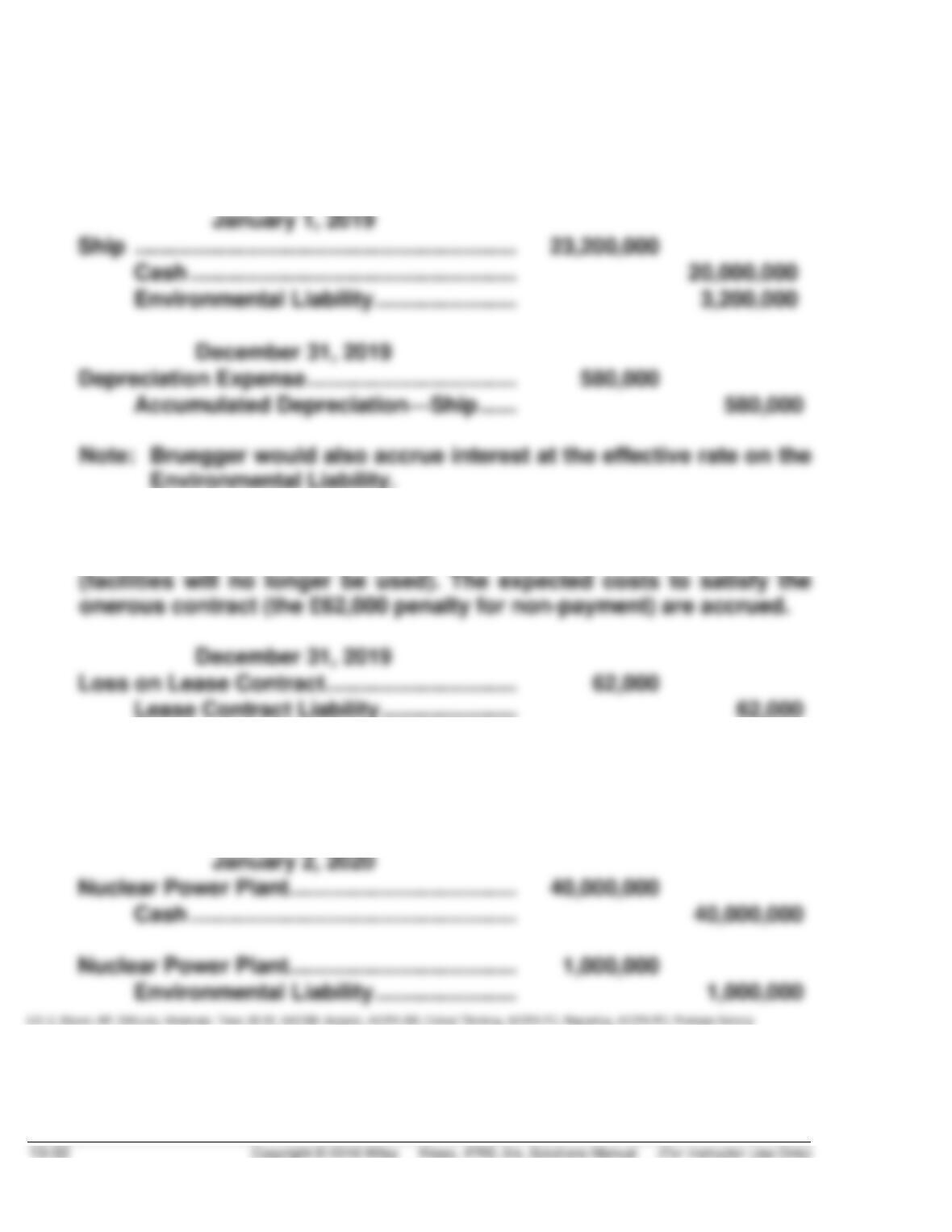

1. The present value of the major overhaul payments (£3,200,000) should

be included as part of the cost of the ship. The ship should be

recorded at £23,200,000.

2. The lease is considered an onerous contract because the unavoidable

costs of meeting the obligations under the lease exceed the benefits

3. The company should recognize the costs associated with dismantling

the plant upon building the plant as it has a legal obligation associated

with its retirement.

EXERCISE 13.21 (20–30 minutes)

1.

Total warranty liability at December 31, 2019 is $5,000,000 as

computed below

*Expected warranty costs

2.

The expected amount of $400,000 should be reported as income taxes

payable at December 31, 2019.

EXERCISE 13.22 (20–25 minutes)

#

Assets

Liabilities

Equity

Net Income

1.

I

I

NE

NE

2.

NE

NE

NE

NE

3.

NE

I

D

D

4.

I

I

NE

NE

6.

I

I

I

I

7.

D

I

D

D

8.

NE

I

D

D

9.

NE

I

D

D

10.

I

I

NE

NE

11.

NE

I

D

D

12.

I

I

I

I

13.

D

D

NE

NE

14.

NE

I

D

D

15.

D

NE

D

D

16.

NE

D

I

I

LO: 4, Bloom: AP, Difficulty: Moderate, Time: 20-25, AACSB: Analytic, AICPA BB: Critical Thinking, AICPA FC: Reporting, AICPA PC: Problem Solving

EXERCISE 13.23 (10–15 minutes)

(a)

Current ratio =

Current Assets

=

¥210,000

= 3.00 times

Current Liabilities

¥70,000

Current ratio measures the short-term ability of the company to meet

its currently maturing obligations.

(c)

Debt to assets =

Total Liabilities

=

¥210,000

= 48.84%

Total Assets

¥430,000

This ratio provides the creditors with some idea of the corporation’s

ability to withstand losses without impairing the interests of creditors.

(d)

¥25,000

= 5.81%

EXERCISE 13.24 (20–25 minutes)

(a)

(1)

Current ratio =

¥733,000

= 3.05

¥240,000

Acid-test ratio =

= 1.21

(4) Inventory turnover =

¥800,000 ÷

¥360,000 + ¥440,000

= 2 times (or approximately

2

every 183 days)

(b) Financial ratios should be evaluated in terms of industry peculiarities

and prevailing business conditions. Although industry and general

business conditions are unknown in this case, the company appears

EXERCISE 13.25 (15–25 minutes)

(a)

(1)

€318,000 ÷ €87,000 = 3.66 times

(3)

€1,400,000 ÷ $95,000 = 14.74 times (or approximately 25 days).

(4) €210,000 ÷ 52,000 (€260,000 ÷ €5) = €4.04

(b) (1) No effect on current ratio, if already included in the allowance

for doubtful accounts.

(2) Weaken current ratio by reducing current assets.

TIME AND PURPOSE OF PROBLEMS

Problem 13.1 (Time 25–30 minutes)

Purpose—to present the student with an opportunity to prepare journal entries for a variety of situations

Problem 13.2 (Time 25–35 minutes)

Purpose—to present the student with the opportunity to prepare journal entries for several different

Problem 13.3 (Time 20–30 minutes)

Purpose—to present the student with an opportunity to prepare journal entries for four weekly payrolls.

The student must compute income tax to be withheld, and social security tax.

Problem 13.4 (Time 20–25 minutes)

Purpose—to provide the student with the opportunity to prepare journal entries for a monthly payroll.

Problem 13.5 (Time 15–20 minutes)

Purpose—to provide the student with an opportunity to prepare journal entries and statement of

Problem 13.6 (Time 10–20 minutes)

Purpose—to provide the student with a basic problem covering the sales-warranty method. The student

Problem 13.7 (Time 25–35 minutes)

Purpose—to provide the student with an opportunity to prepare journal entries for warranty costs. The

student is also required to indicate the proper statement of financial position disclosures for the year of

sale.

Problem 13.8 (Time 15–25 minutes)

Purpose—to provide the student with a basic problem in accounting for premium offers. The student is

Time and Purpose of Problems (Continued)

Problem 13.9 (Time 30–45 minutes)

Purpose—to present the student with a slightly complicated problem related to accounting for premium

offers. The problem is more complicated in that coupons redeemed are accompanied by cash payments,

Problem 13.10 (Time 25–30 minutes)

Purpose—to present the student with the problem of determining the proper amount of and disclosure

Problem 13.11 (Time 35–45 minutes)

Purpose—to provide the student with a comprehensive problem dealing with contingent liabilities. The

Problem 13.12 (Time 20–30 minutes)

Purpose—to provide the student with a problem to calculate warranty expense, warranty liability, premium

expense, inventory of premiums, and estimated premium liability.

Problem 13.13 (Time 25–35 minutes)

Problem 13.14 (Time 20–25 minutes)

Purpose—to present the student with a comprehensive problem in determining the amounts of various

SOLUTIONS TO PROBLEMS

PROBLEM 13.1

(a) February 2

Purchases (€70,000 X 98%) ……………………………..

68,600

Accounts Payable …………………………………..

68,600

February 26

Accounts Payable …………………………………………..

68,600

Purchase Discounts Lost ………………………………..

Cash ……………………………………………………..

70,000

April 1

Trucks ……………………………………………………………

50,000

Cash ……………………………………………………..

Notes Payable ………………………………………..

August 1

Retained Earnings (Dividends Declared) …………..

300,000

Dividends Payable ………………………………….

300,000

September 10

Dividends Payable …………………………………………..

300,000

Cash ……………………………………………………..

(b) December 31

1. No adjustment necessary

2. Interest Expense (€46,000 X 12% X 9/12) ………

Interest Payable ……………………………………..

3. No adjustment necessary