CHAPTER 20

Accounting for Pensions and

Postretirement Benefits

LEARNING OBJECTIVES

1. Discuss the fundamentals of pension plan accounting.

2. Use a worksheet for employer’s pension plan entries.

CHAPTER REVIEW

1. Chapter 20 discusses the various aspects of accounting for the cost of pension plans.

associated with a pension plan.

Nature of Pension Plans

2. (L.O. 1) A pension plan is an arrangement whereby an employer provides benefits

(payments) to employees after they retire for services they provided while they were

3. Pension plans can be contributory or noncontributory. In a contributory plan, the

employees bear part of the cost of the stated benefits or voluntarily make payments to

increase their benefits. If the plan is noncontributory, the employer bears the entire cost.

Types of Pension Plans

4. The most common types of pension arrangements are defined contribution plans and

defined benefit plans. In a defined contribution plan, the employer agrees to contribute a

certain sum each period based on a formula. The formula might consider such factors as

5. A defined benefit plan defines the benefits that the employee will receive at the time of

retirement. The formula that is typically used provides for the benefits to be a function of

the level of compensation near retirement and of the number of years of service. The

provided by actuaries.

Measures of Liability

6. Most accountants agree that an employer’s pension obligation is the deferred

compensation obligation it has to its employees for their services under the terms of the

pension plan. However, there are three ways to measure this liability. One approach is to

base the obligation on the vested benefits current employees are entitled to receive

7. Regardless of the approach used, the estimated future benefits to be paid are discounted

to present value. However, the profession adopted the defined benefit obligation –

Components of Pension Expense

8. The net defined benefit obligation (asset) (also referred to as the funded status) is

the deficit or surplus related to a defined pension plan. The deficit or surplus is often

referred to as the funded status of the plan. If the defined benefit obligation is greater

9. Accounting for pension plans requires measurement of the cost and its identification with

the appropriate time periods. The determination of pension cost is very complicated

because it is a function of a number of factors. These factors are identified and described

below.

Service Cost. This is either current service cost or past service cost. This component

1. Apply an actuarial valuation method.

Net Interest. Because a pension is a deferred compensation arrangement, it is recorded on a

discounted basis. Net interest is computed by multiplying the discount rate by the

defined benefit obligation and the plan assets.

Remeasurement. Remeasurements are gains and losses related to the defined benefit

obligation (changes in discount rate or other actuarial assumptions) and gains or

In summary, pension expense is comprised of two components: (1) service cost and

(2) net interest.

Pension plan assets are usually investments in shares, bonds, other securities, and real

estate that a company holds to earn a reasonable rate of return.

Actual Return on Plan Assets is the increase in the pension fund assets arising

from interest, dividends, and realized and unrealized changes in the fair value of the

Fair value of plan assets, January 1, 2019 ……………………. £4,200,000

Plus: Contributions to plan during period ………………………. 300,000

Plus: Actual return…………………………………………….. 210,000

The Pension Worksheet

10. (L.O. 2) In illustrating the accounting for these factors the text material makes use of

a work sheet approach. The worksheet is unique to pension accounting and is utilized to

a. The left–hand “General Journal Entries” columns of the worksheet record entries in the

b. On the first line of the worksheet, the beginning balances (if any) are recorded.

Subsequently, transactions and events related to the pension plan are recorded, using

most effective means of keeping track of complicated computations.

2019 Entries and Worksheet

11. To illustrate the use of a worksheet, the following facts apply to Zarle Company for the

year 2019:

Plan assets, 1/1/19 ……………………………………………… €100,000

Defined benefit obligation, 1/1/19 ………………………….. €100,000

Pension Worksheet for 2019

General

Journal

Entries

Memo

Record

Items

Annual

Pension

Expense

Cash

Pension

Asset/

Liability

Defined

Benefit

Obligation

Plan

Assets

Balance Jan. 1, 2019

—

100,000

Cr.

100,000

Dr.

(a) Service cost

9,000 Dr.

9,000 Cr.

(b) Interest expense

10,000 Cr.

8,000

8,000

112,000

Cr.

111,000

Dr.

* €9,000 – 8,000 = €1,000

**€112,000 – 111,000 = €1,000

12. (L.O. 3) Past service cost (PSC) is the change in the present value of the defined

benefit obligation resulting from a plan amendment or a curtailment. For example, a plan

amendment arises when a company decides to provide additional benefits to existing

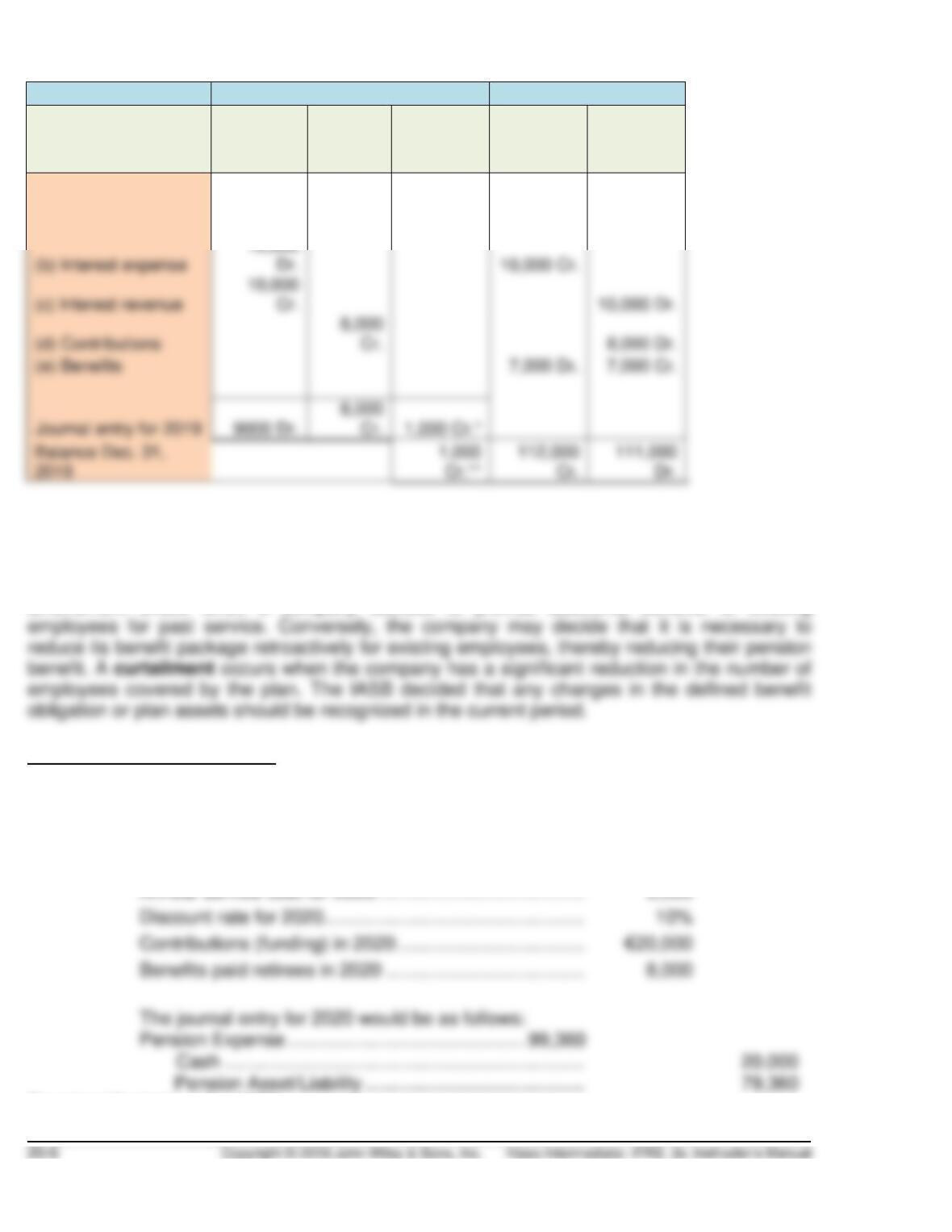

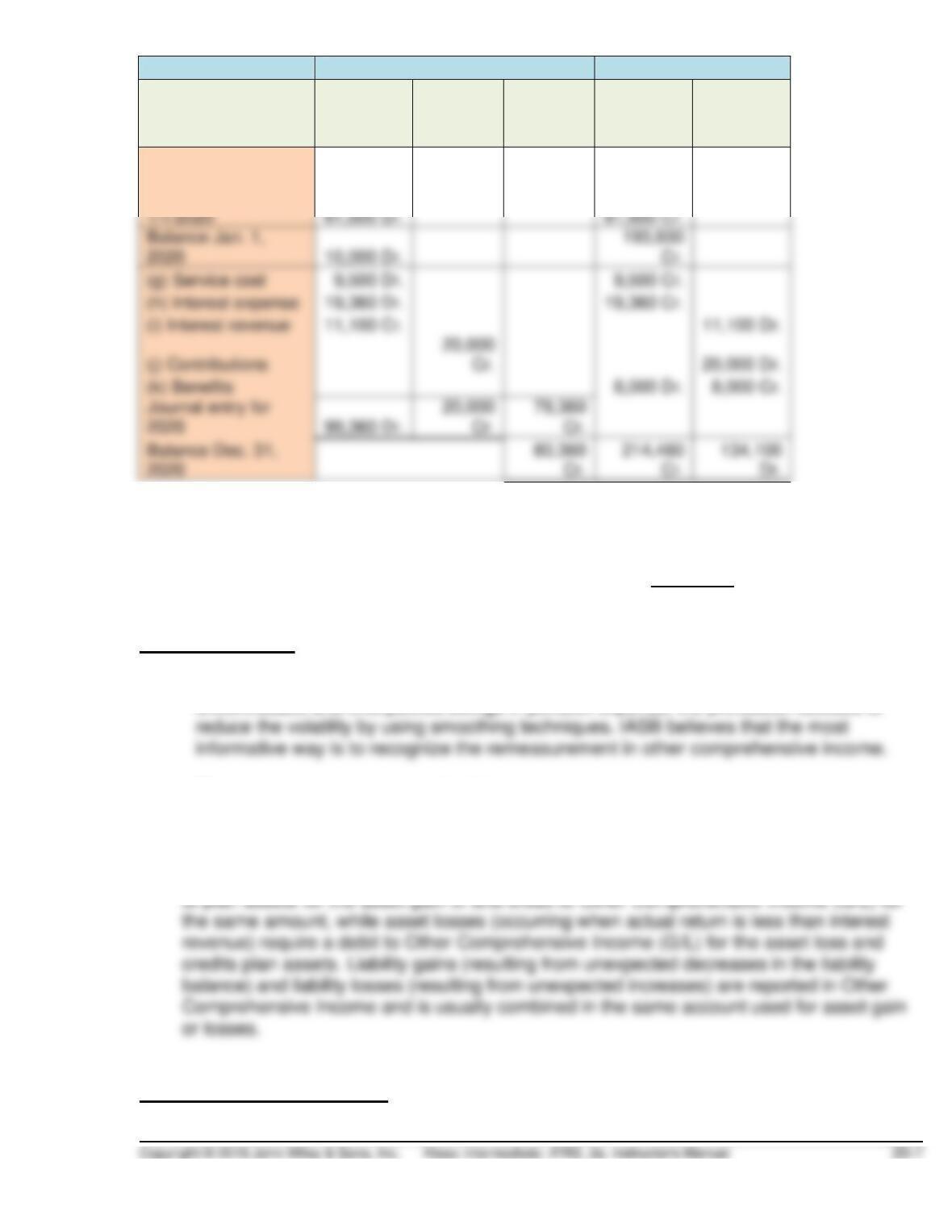

2020 Entries and Worksheet

13. To illustrate the use of a worksheet with amortization of unrecognized past service costs,

the following facts apply to Zarle Company for the year 2020:

Present value of past service benefits granted l/l/20 …. €81,600

Pension Worksheet for 2020

General

Journal

Entries

Memo

Record

Items

Annual

Pension

Expense

Cash

Pension

Asset/

Liability

Defined

Benefit

Obligation

Plan

Assets

Balance Dec. 31,

2020

1,000 Cr.

112,000

Cr.

100,000

Dr.

Balance Jan. 1,

2020

193,600

Cr.

(g) Service cost

(h) Interest expense

(i) Interest revenue

(j) Contributions

(k) Benefits

Journal entry for

Balance Dec. 31,

214,460

134,100

(f) Additional PSC

The pension reconciliation schedule is as follows:

Defined benefit obligation (Credit) €(214,460)

Plan assets at fair value (Debit) 134,100

Pension asset/liability (Credit) (80,360)

Remeasurements

14. (L.O. 4) Because of the concern to companies that pension plans would have

uncontrollable and unexpected swings in pension expense, the profession decided to

Remeasurements are generally of two types:

1. Gains and losses on plan assets.

2. Gains and losses on the defined benefit obligation.

Asset gains (occurring when actual return is greater than interest revenue) require a debit

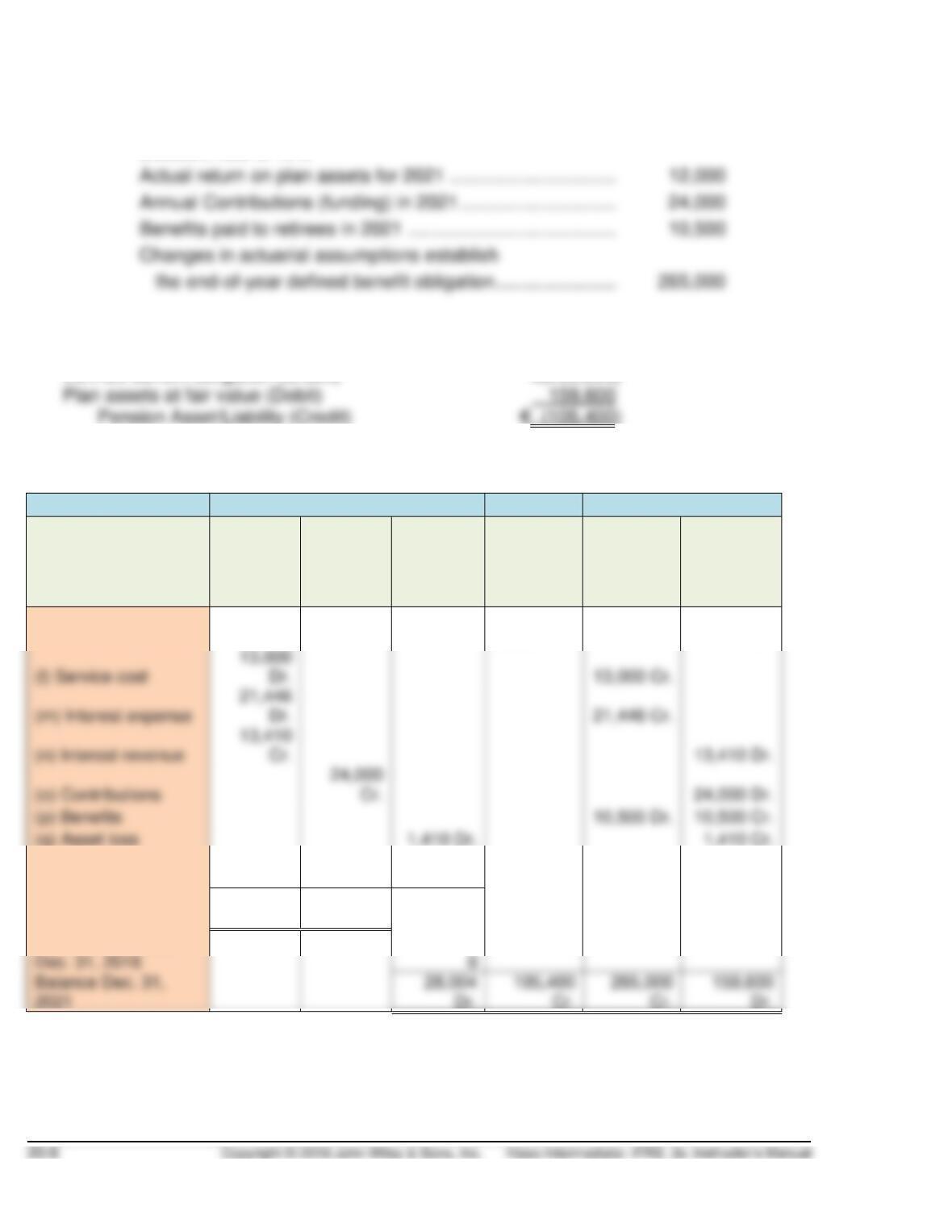

2021 Entries and Worksheet

17. Continuing the Zarle Company illustration into 2021, the following facts apply to the

pension plan:

Annual service cost for 2021 ………………………………………. € 13,000

Discount rate is 10%

The pension reconciliation schedule is as follows:

Defined benefit obligation (Credit) €(265,000)

The 2021 worksheet would be completed as follows:

General

Journal

Entries

Memo

Record

Items

Annual

Pension

Expense

Cash

OCI –

Gain/Loss

Pension

Asset/

Liability

Defined

Benefit

Obligation

Plan

Assets

Balance Jan. 1, 2021

80,360 Cr.

214,460

Cr.

134,100

Dr.

(l) Service cost

13,000

(m) Interest expense

21,446

(n) Interest revenue

Cr.

13,410 Dr.

(o) Contributions

24,000

Cr.

24,000 Dr.

(p) Benefits

10,500 Dr.

10,500 Cr.

(q) Asset loss

1,410 Cr.

(r) Liability loss

26,594

Dr.

8,000 Cr.

Journal entry for

2021

21,036

Dr.

24,000

Cr.

28,004

Dr.

25,040 Cr.

26,594 Cr.

Dec. 31, 2016

Balance Dec. 31,

28,004

159,600

Accumulated OCI,

18. The IASB is silent as to whether the Accumulated Other Comprehensive Income

19. A company reports the pension asset/liability as an asset or a liability in

the statement of financial position at the end of a reporting period. The

20. In the notes, a company is required to disclose information that (a) explains

characteristics of its defined benefit plans and risks associated with them, (b)

Other Post-Retirement Benefits

21. (L.O. 6) Companies often provide other types of non-pension postretirement

benefits, such as life insurance outside a pension plan, medical care, and legal

and tax services. The accounting for these other types of postretirement benefits

LECTURE OUTLINE

The material in this chapter can be covered in four class periods. Accounting for the costs of

pension plans is technically complex and conceptually challenging for most students. The use

of the pension work sheet illustrated in the textbook is very helpful in organizing and presenting

the major components of pension expense.

A. The Nature of Pension Plans. Discuss the following:

1. Definition of pension plan: an arrangement whereby an employer provides benefits

2. (L.O. 1) Employer vs. plan accounting. Employer sponsors the plan, incurs the cost, and

makes contributions. The plan receives the contributions, administers plan assets, and

makes benefit payments to recipients.

a. Funding. Employer payments to funding agency.

b. Contributory vs. noncontributory.

(1) Contributory: employees bear part of the cost of the stated benefits.

3. Types of pension plans.

a. Defined contribution plans: employer’s contribution is defined; there is no

4. The role of actuaries in pension accounting.

5. The pension obligation: deferred compensation obligation an employer has to its

employees.

a. Vested benefits: benefits employee is entitled to even if no further services rendered.

B. Net Defined Benefit Obligation (Asset).

6. The net defined benefit obligation (asset) is also referred to as the funded status

7. In the statement of financial position, companies report the net defined benefit

obligation/asset (funded status), which is the defined benefit obligation less the fair

value of plan assets (if any). Changes in the net defined benefit obligation (asset) are

C. (L.O. 2) Use a Worksheet for Employer’s Pension Plan Entries.

8. Companies may use a worksheet unique to pension accounting. This worksheet

D. (L.O. 3) Explain the accounting for past service costs.

9. Past service cost is the change in the value of the defined benefit obligation

resulting from a plan amendment or a curtailment. Past service costs are

E. (L.O. 4) Explain the accounting for remeasurements.

10. Remeasurements arise from (1) gains and losses on plan assets and (2) gains

and losses on the defined benefit obligation. The gains and losses on plan assets

11. All remeasurements are reported in other comprehensive income. These

amounts are not recycled into income in subsequent periods.

F. (L.O. 5) Describe the requirements for reporting pension plans in financial statements.

12. A company reports the pension asset/liability as an asset or a liability in

the statement of financial position at the end of a reporting period. The

13. In the notes, a company is required to disclose information that (a) explains

characteristics of its defined benefit plans and risks associated with them, (b)

G. (L.O. 6) Explain the accounting for other postretirement benefits.

14. Companies often provide other types of non-pension postretirement

benefits, such as life insurance outside a pension plan, medical care, and legal