TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS

CA 21.1 (Time 15–25 minutes)

Purpose—to provide the student with an understanding of the theoretical reasons for requiring leases to be

CA 21.2 (Time 25–35 minutes)

Purpose—to provide an understanding of the factors underlying the accounting for a leasing arrangement from

CA 21.3 (Time 20–30 minutes)

CA 21.4 (Time 20–25 minutes)

Purpose—to provide the student with a lease arrangement with a bargain-purchase option in order to examine

the ethical issues of lease accounting.

CA 21.5 (Time 30–40 minutes)

Purpose—to develop a memo to your audit supervisor to discuss: (a) why you inspected the lease agreement,

*CA 21.6 (Time 15–25 minutes)

Purpose— The student is required to discuss the accounting issues related to a sale-leaseback.

SOLUTIONS TO CONCEPTS FOR ANALYSIS

CA 21.1

(a) The IASB believes that the reporting of an asset and liability for a lease arrangement is

consistent with the conceptual framework definition of assets and liabilities. That is, assets are

(b) Evans should account for this lease at its commencement as an asset and an obligation at an

amount equal to the present value at the beginning of the lease term of lease payments during

the lease term. From the information provided, this lease represents transfer of ownership.

(d) The right-of-use asset recorded under the finance lease should be classified on Evans’

December 31, 2019, statement of financial position as noncurrent and should be separately

identified by Evans in its statement of financial position or footnotes thereto. The related

CA 21.2

(a) (1) Since the given facts state that Sylvan (lessee) does not have access to information that

(2) The amount recorded as an asset on Sylvan’s books should be shown in the non-current

asset section of the statement of financial position as “Right–of-Use Asset” or another

similar title. At the same time as the asset is recorded, a corresponding liability (“Lease

Liability” or similar title) is recognized in the same amount. This liability is classified as both

(3) The lessee should make the following qualitative disclosures:

• Nature of its leases, including general description of those leases.

In addition the quantitative information that should be disclosed by the lessee is as follows:

• Total lease cost.

CA 21.2 (Continued)

(b) (1) Based on the given facts, Breton has entered into a sales-type lease. The discounted

present value of the lease payments is in excess of 90 percent of the fair value of the asset

at commencement of the lease arrangement and collectibility of lease payments is

probable.

(2) Breton should record a Lease Receivable for the present value of the lease payments and

the present value of the residual value. It might be noted that since the residual value is

(3) During the life of the lease, Breton will record payments received as a reduction in the

receivable. Interest is recognized as interest revenue by applying the implicit interest rate

(4) Breton must make the following disclosures with respect to this lease:

▪ Lease-related income, including profit and loss recognized at lease commencement for

sales-type leases, and Interest Income.

CA 21.3

(a) For Lease L, Santiago SA should record as a liability at the commencement of the lease an

amount equal to the present value of the lease payments during the lease term.

CA 21.3 (Continued)

(b) For Lease L, M, and N, Santiago Company should apply the finance lease method and allocate

CA 21.4

(a) The ethical issues are fairness and integrity of financial reporting versus profits and possibly

misleading financial statements. On one hand, if Buchanan can substantiate her position, it is

possible that the agreement should be recorded at the lower amount. On the other hand, if

*CA 21.5

Memorandum Prepared by: (Your Initials)

Date:

HOCKNEY PLC

December 31, 2019

Reclassification of Leased Auto

While performing a routine inspection of the client’s garage, I found a used automobile which was not

CA 21.5 (Continued)

Examining the noncancelable lease agreement entered into with Crown New and Used Cars on

January 1, 2019, I determined that the automobile should be capitalized as a finance lease because

its lease term is greater than 1 year.

I advised the client to capitalize this lease at the present value of its rental payments: £5,778 (the present

Right-of-Use Asset ………………………………………………………………… 5,778

Lease Liability ……………………………………………………………….. 5,778

To account for the first year’s payments as well as to reverse the original entries, I advised the client

to make the following entry:

*CA 21.6

(a) The major accounting issue is whether the transaction is a sale or a financing. To determine

whether it is a sale, the revenue recognition guidelines are used. That is, if control has passed

from seller to buyer then a sale has occurred. Conversely, if control has not passed from seller

to buyer the transaction is recorded as a financing (often referred to as a failed sale).

(b) This transaction should be reported as a financing as control of the leased asset has not passed

from the seller to the buyer. In essence, Perriman is borrowing money from the purchaser–

FINANCIAL REPORTING PROBLEM

(a) M&S uses both finance leases and operating leases.

(c) M&S disclosed future minimum rentals (in millions) under non-cancelable

operating lease agreements as of 30 March 2016, of:

Not later than one year ……………………………… £ 311.3

Later than one year and

COMPARATIVE ANALYSIS CASE

(a) Air France uses both finance leases and operating leases on its aircraft,

buildings, and other property, plant, and equipment.

(b) Some of Air France’s leases are longer than five years. Some characteristics

of the leases are the assets held under a finance lease are recognized as

(c) Future minimum commitments under capital leases are set forth below (in

millions):

2015

2014

One year ………………………………………

€ 583

€ 655

(d) At year-end 2015, the present value of minimum lease payments under

capital leases was €3,789 million. Imputed interest deducted from the future

minimum annual rental commitments was €260 million.

COMPARATIVE ANALYSIS CASE (Continued)

(f) British Airways uses leases for its aircraft fleet and property and equipment,

while Air France uses leases for its aircraft, buildings, and other property,

FINANCIAL STATEMENT ANALYSIS CASE

(a) The total obligations under finance leases at year-end 2015 for Delhaize is €555

million (the present value of the future lease payments).

(b) The total rental expense for Delhaize in 2015 was €352,000,000.

(c) To estimate the present value of the operating leases, the same portion of

Total operating lease payments due …………………………... €1,563,000

Less estimated interest ……………………………………………… 697,254

Estimated present value of net operating

lease payments ……………………………………………………… € 865,746

This answer is an approximation. This answer is somewhat incorrect

because the proportion of payments after five years may be different

ACCOUNTING, ANALYSIS, AND PRINCIPLES

Accounting

(a) The lease liability is computed as follows:

Present value of lease payments

Therefore Salaur makes the following journal entries at the commencement date.

1/1/19

SALAUR SpA

Lease Amortization Schedule

Annuity-Due Basis

Date

Annual

Payment

Interest (12%)

on Liability

Reduction

of Lease

Liability

Lease Liability

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

The entry to record lease expense in 2019 is as follows.

12/31/19

Interest Expense …………………….. 620.03

(b) With the bargain purchase option, Salaur computes the lease liability and

right-of–use asset, as follows.

Present value of lease payments

Salaur makes the following entries at lease commencement.

1/1/19

Right-of-Use Asset ………………… 8,295.34

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

SALAUR SpA

Lease Amortization Schedule

Date

Annual Lease

Payment Plus

BPO

Interest

(12%) on

Liability

Reduction

of Lease

Liability

Lease

Liability

1/1/19

€8,295.34

1/1/19

1/1//22

12/31/19

Interest Expense ……………………. 628.57

Lease Liability ………………… 628.57

Analysis

While all leases with terms longer than one year are capitalized (recorded on the

statement of financial position), the amounts differ depending on whether the

lease is classified as a finance or operating lease. As indicated in the entries

above, the right-of-use asset increases and the denominator of the return on

assets ratio (ROA = Net income ÷ Average assets) will increase, but by different

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

This reporting is in contrast to prior IFRS, under which many operating leases

Principles

The fundamental quality is faithful representation. The lease criteria are

designed to report leases according to their economic substance. Thus, if

RESEARCH CASE

(a) (1) According to IFRS 16, (paragraphs 26-28), a lessee shall measure the

lease liability at the present value of the lease payments that are not paid at

The lease payments included in the measurement of the lease liability

comprise the following payments for the right to use the underlying asset

during the lease term that are not paid at the commencement date:

(a) fixed payments less any lease incentives receivable;

(b) variable lease payments that depend on an index or a rate, initially

Variable lease payments that depend on an index or a rate described in

paragraph 27(b) include, for example, payments linked to a consumer price

index, payments linked to a benchmark interest rate (such as LIBOR) or

payments that vary to reflect changes in market rental rates.

(2) (paragraphs 23-24) Initial measurement of the right-of-use asset shall

comprise:

(a) the amount of the initial measurement of the lease liability;

(b) any lease payments made at or before the commencement date, less

RESEARCH CASE (Continued)

(b) According to IFRS 16 (paragraphs 18-19), an entity shall determine the lease

term as the non-cancellable period of a lease, together with both:

1. periods covered by an option to extend the lease if the lessee is reasonably

In assessing whether a lessee is reasonably certain to exercise an option to

extend a lease, or not to exercise an option to terminate a lease, an entity shall

(c) IFRS 16 (paragraph 44) indicates that a lessee shall account for a lease

modification as a separate lease if both:

(a) the modification increases the scope of the lease by adding the right to

GAAP CONCEPTS AND APPLICATION

GAAP21.1

The accounting for leases is found in Accounting Standards Codification section

842, which was updated in February 2016.

GAAP21.2

The following are similarities and differences between lease accounting under

IFRS and U.S. GAAP.

Similarities

• Both GAAP and IFRS share the same objective of recording leases by

lessees and lessors according to their economic substance—that is,

according to the definitions of assets and liabilities.

Differences

• There is no classification test for lessees under IFRS 16. Thus, lessees

account for all leases using the finance lease method; that is, leases

GAAP CONCEPTS AND APPLICATION (Continued)

• In addition to the short term lease exception, IFRS has an additional lessee

recognition and measurement exemption for leases of assets of low value

GAAP21.3

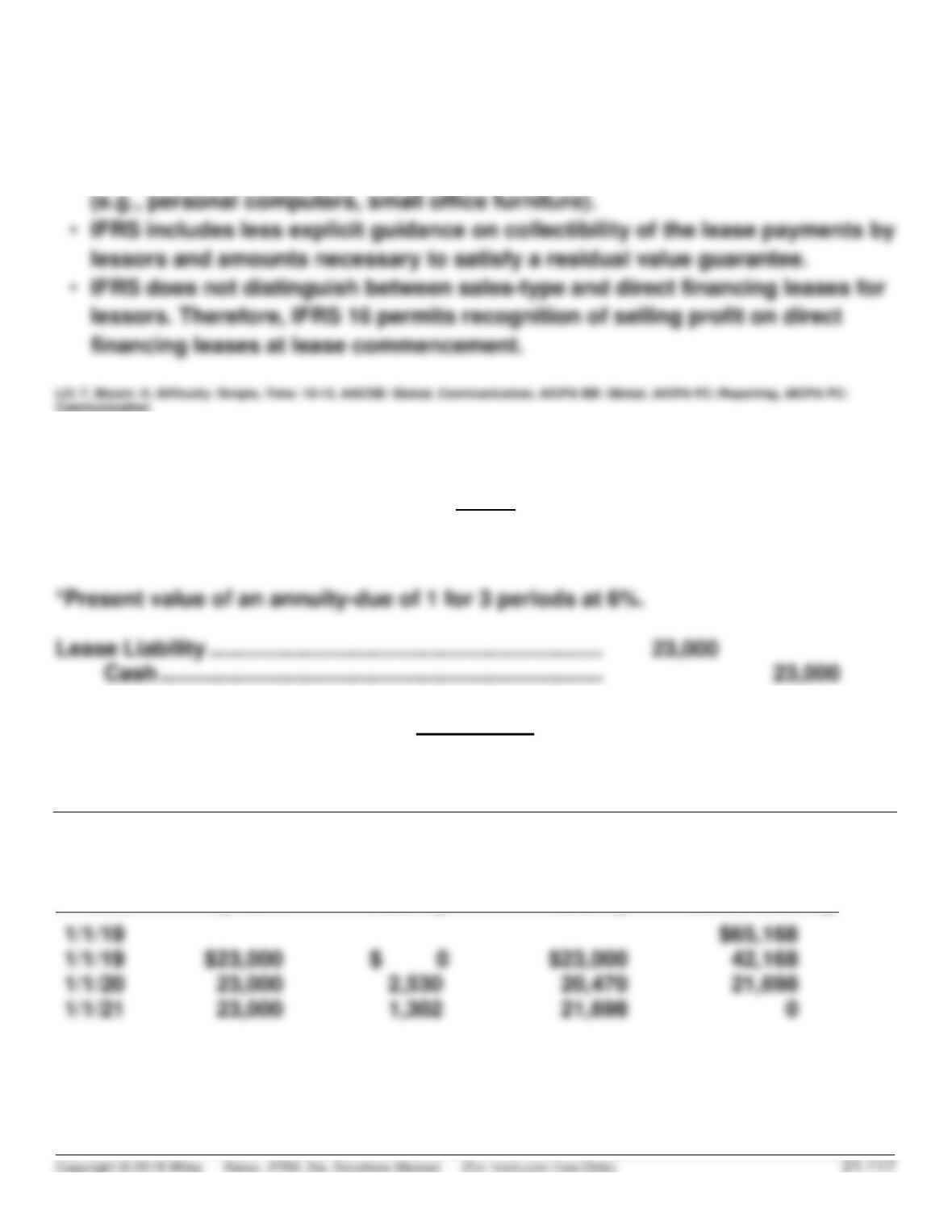

1/1/19

Right-of–Use Asset (2.83339* X $23,000) …………………. 65,168

Lease Liability ………………………………………………. 65,168

Schedule A

LEBRON JAMES CORPORATION

Lease Amortization Schedule

Annuity-Due Basis

Date

Annual

Payment

Interest (6%) on

Liability

Reduction

of Lease

Liability

Lease Liability

GAAP CONCEPTS AND APPLICATION (Continued)

Schedule B

Lease Expense Schedule

Date

(A)

Lease Expense

(Straight-Line)

(B)

Interest (6%) on

Lease Liability

(C)

Amortization

of ROU Asset

(A–B)

Carrying Value

of ROU Asset

1/1/19

$65,168

12/31/20

12/31/19

Lease Expense ……………………………………………………… 23,000

Lease Liability (Schedule A) ……………………… 2,530*