PROBLEM 9.6 (Continued)

*Computation of Gross Profit Ratio

Net sales, 2017 …………………………………………

€390,000

Net sales, 2018 …………………………………………

530,000

Total net sales …………………………………

920,000

Beginning inventory ………………………………….

€ 66,000

Net purchases, 2017 ………………………………….

235,000

Net purchases, 2018 ………………………………….

280,000

Less: Ending inventory …………………………….

506,000

PROBLEM 9.7

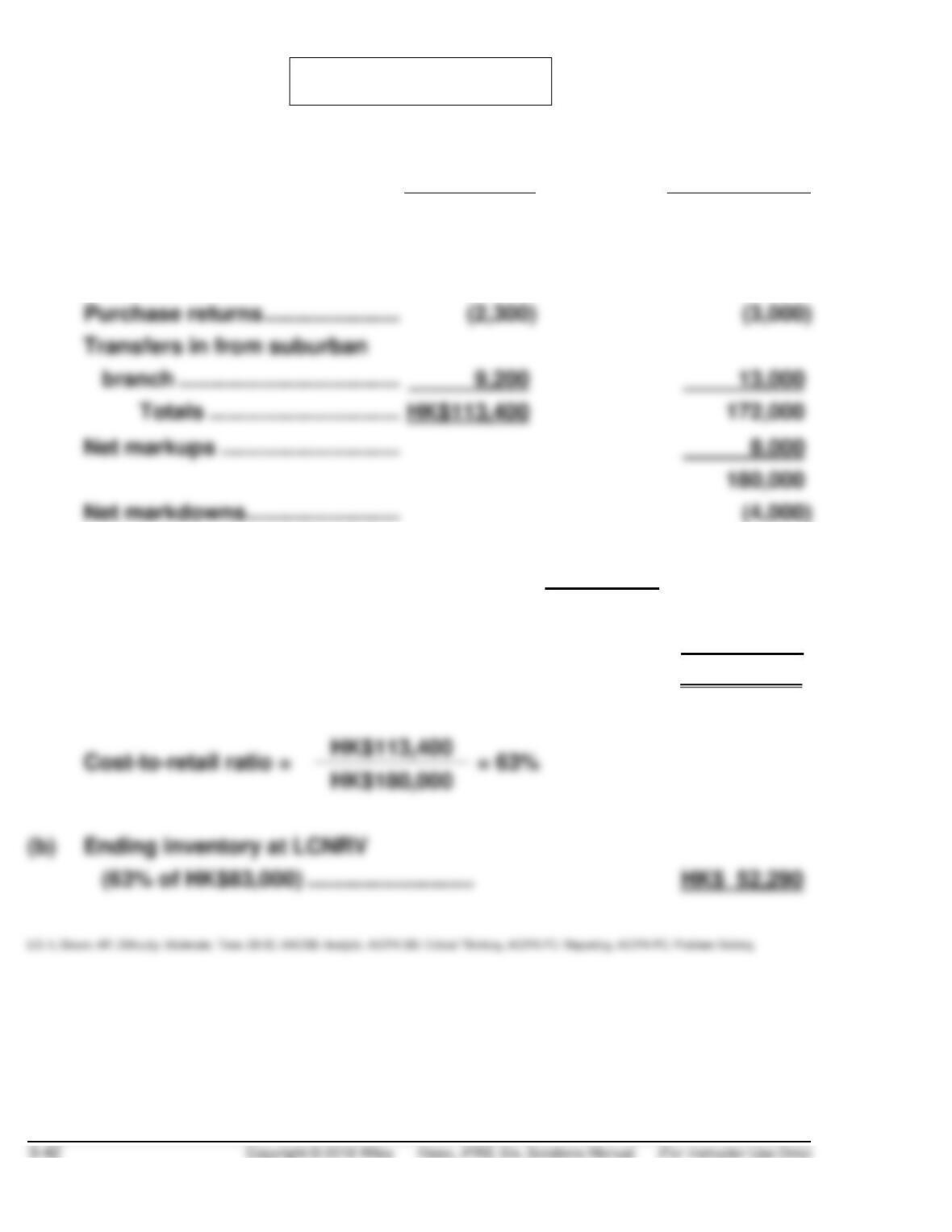

(a)

Cost

Retail

Beginning inventory ………………………..

HK$ 17,000

HK$ 25,000

Purchases ………………………………………

82,500

137,000

Freight-in ………………………………………..

7,000

Purchase returns …………………………..

Net markups …………………………..

180,000

Net markdowns …………………………..

Sales ………………………………………………

HK$(95,000)

Sales returns …………………………..

2,400

(92,600)

Inventory losses due to

breakage …………………………..

(400)

Ending inventory at retail ………………..

HK$ 83,000

(b)

Ending inventory at LCNRV

(63% of HK$83,000) ………………………

HK$ 52,290

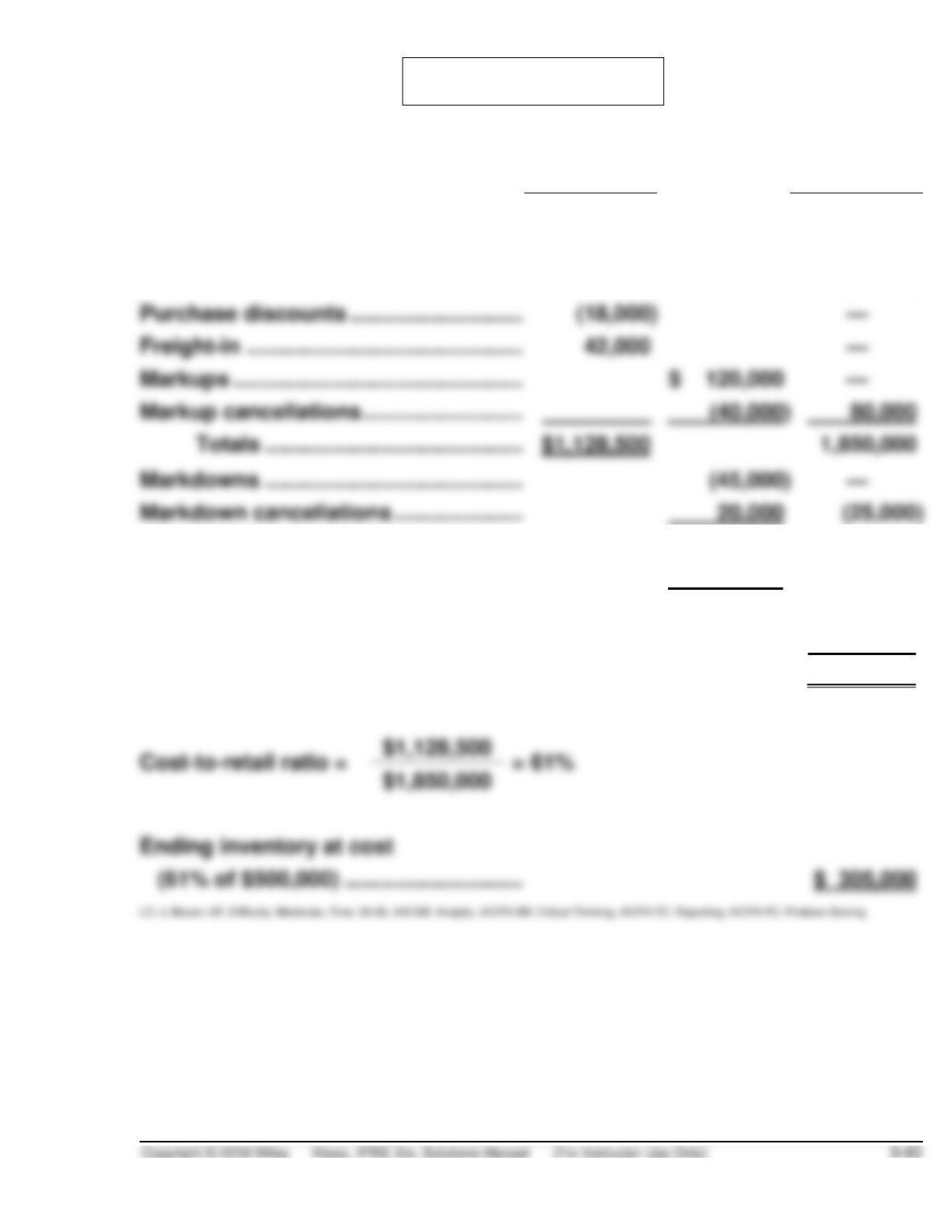

PROBLEM 9.8

Cost

Retail

Beginning inventory ……………………….

$ 250,000

$ 390,000

Purchases ……………………………………..

914,500

1,460,000

Purchase returns …………………………...

(60,000)

(80,000)

Purchase discounts ……………………….

(18,000)

—

—

Markups …………………………..……………

$ 120,000

—

Markup cancellations ……………………..

80,000

Markdowns ……………………………………

(45,000)

—

Markdown cancellations …………………

20,000

(25,000)

Sales ……………………………………………..

(1,410,000)

—

Sales returns …………………………………

97,500

(1,312,500)

Inventory losses due to breakage ……

(4,500)

Employee discounts ………………………

(8,000)

Ending inventory at retail ……………….

$ 500,000

$1,128,500

$1,850,000

(61% of $500,000) ………………………..

PROBLEM 9.9

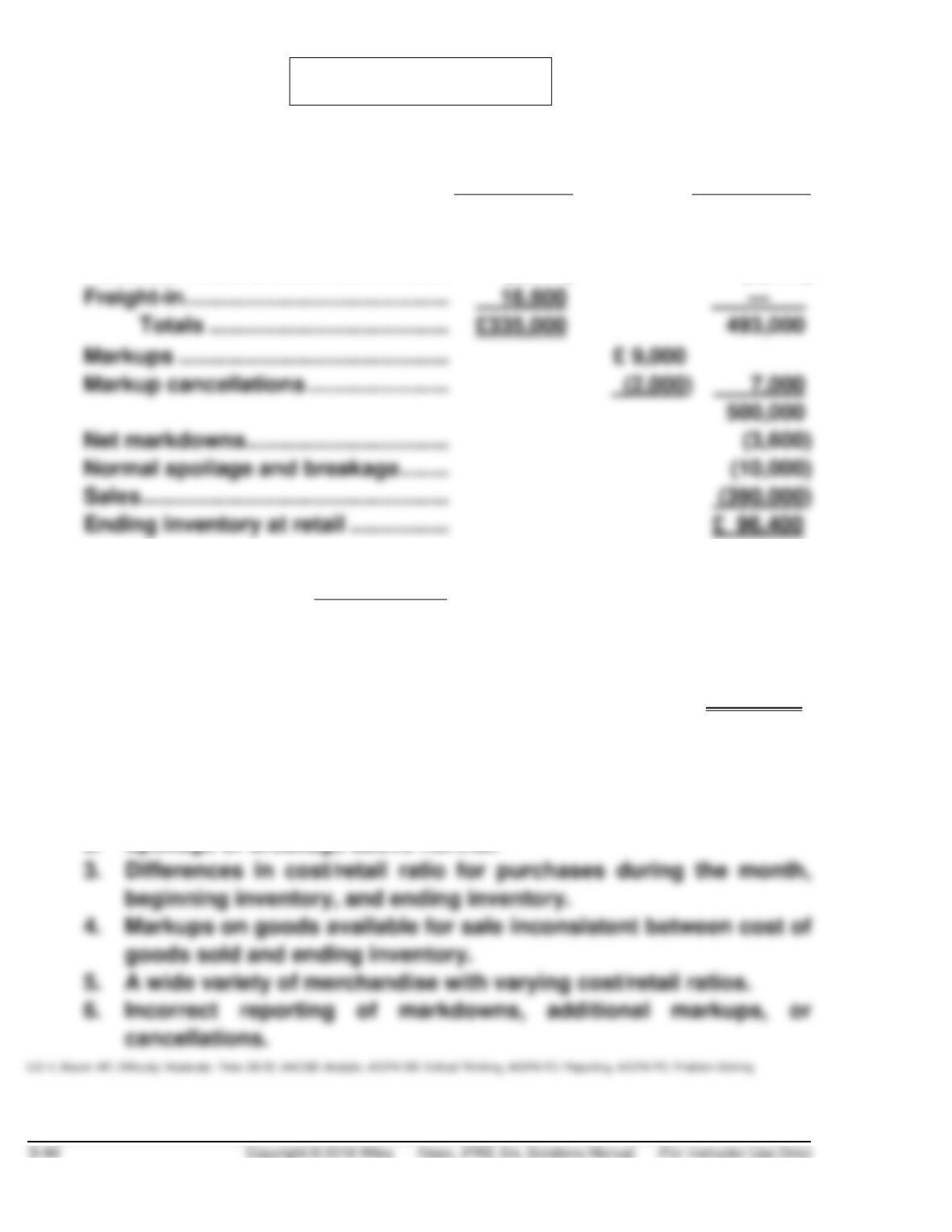

(a)

Cost

Retail

Inventory (beginning) …………………..

£ 52,000

£ 78,000

Purchases …………………………………..

272,000

423,000

Purchase returns …………………………

(5,600)

(8,000)

16,600

Totals …………………………………

Markups …………………………..…………

Markup cancellations …………………..

7,000

500,000

Net markdowns …………………………...

(3,600)

Normal spoilage and breakage ……..

Sales …………………………………………..

Ending inventory at retail …………….

Cost-to-retail ratio =

£335,000

= 67%

£500,000

Ending inventory at LCNRV

(67% of £96,400) ……………………….

£ 64,588

(b) The difference between the inventory estimate per retail method and

the amount per physical count may be due to:

1. Theft losses (shoplifting or pilferage).

2. Spoilage or breakage above normal.

PROBLEM 9.10

(a) The inventory section of Maddox’s statement of financial position at

November 30, 2019, including required footnotes, is presented below.

Also presented below are supporting calculations.

Current assets

Inventory Section (Note 1.)

Finished goods (Note 2.) ……………………..

Work-in-process ………………………………….

Raw materials ……………………………………..

Factory supplies………………………………….

Note 1. Lower-of-cost (first-in, first-out) or-net realizable value is

Note 2. Seventy-five percent of bar end shifters finished goods

inventory in the amount of $136,500 ($182,000 X .75) is

PROBLEM 9.10 (Continued)

Supporting Calculations

Finished

Goods

Work-in–

Process

Raw

Materials

Factory

Supplies

Down tube shifters at NRV …………

$266,000

Bar end shifters at cost ……………..

182,000

$108,700

Remaining items at NRV ……………

Supplies at cost ………………………..

(b) The decline in the net realizable value of inventory below cost may be

reported using one of two alternate methods, the cost-of-goods-sold

method or the loss method. The decline in the net realizable value of

(c) Purchase contracts for which a firm price has been established should

be disclosed on the financial statements of the buyer. If the contract

price is greater than the current market price and a loss is expected

PROBLEM 9.11

(a) Schedule A

Item

On Hand

Quantity

Cost

NRV

Lower-of-Cost-

or-NRV

A

1,100

NT$7.50

NT$9.00

NT$7.50

B

800

8.20

8.10

8.10

E

1,400

6.40

6.00

6.00

Schedule B

Item

Cost

Lower-of-Cost-or-NRV

Difference

A

1,100 X NT$7.50 = NT$8,250

1,100 X NT$7.50 = NT$8,250

None

B

800 X NT$8.10 = NT$6,480

C

1,000 X NT$5.60 = NT$5,600

1,000 X NT$5.45 = NT$5,450

D

1,000 X NT$3.80 = NT$3,800

1,000 X NT$3.80 = NT$3,800

None

1,400 X NT$6.40 = NT$8,960

1,400 X NT$6.00 = NT$8,400

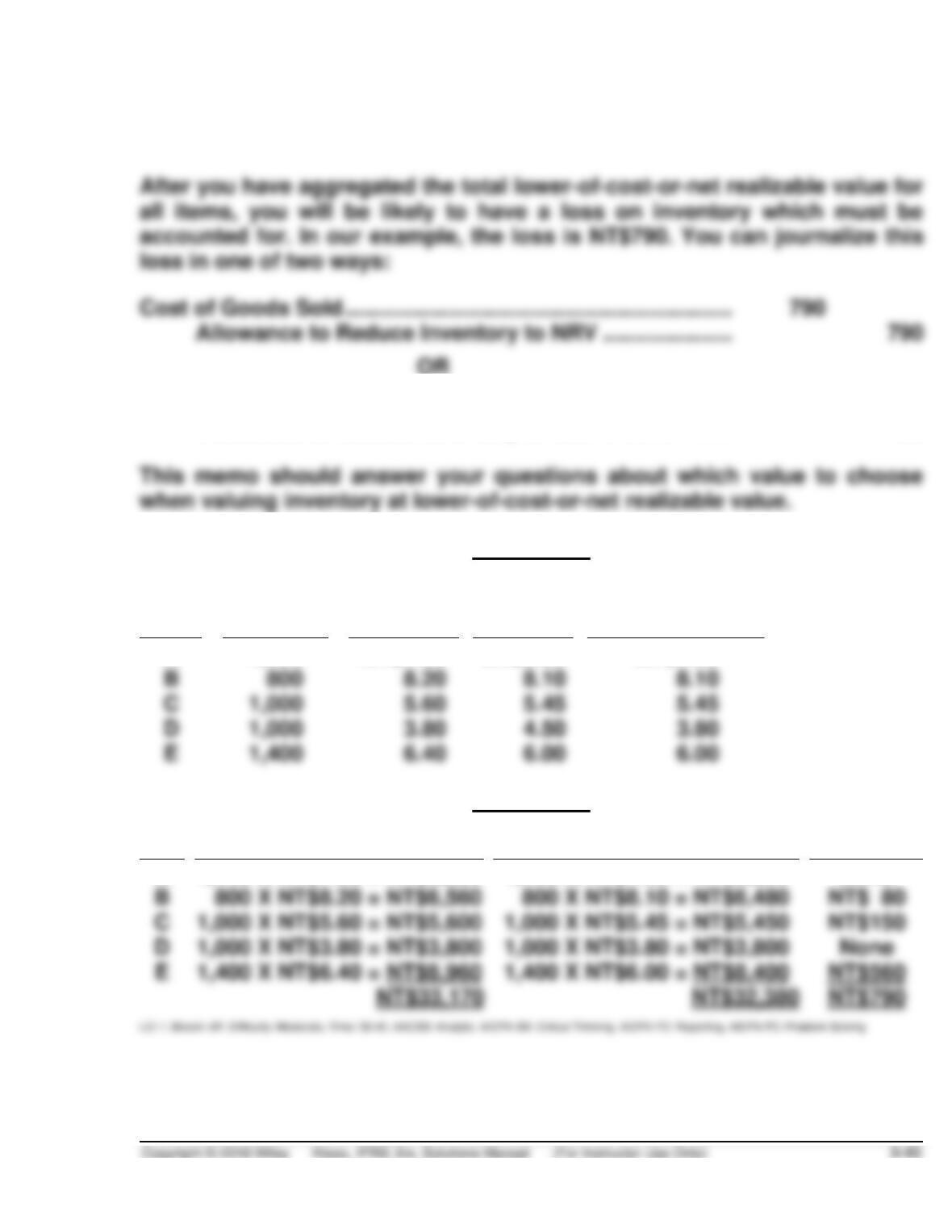

(b) Cost of Goods Sold ……………………………………………………….

790

Allowance to Reduce Inventory to NRV ……………………..

790

Loss Due to Decline of Inventory to NRV …………………………

790

PROBLEM 9.11 (Continued)

(c)

To: Jay Shin, Clerk

From: Accounting Manager

This memo responds to your questions regarding our use of lower–of-cost-

or-net realizable value for inventory valuation. Simply put, value inventory

at whichever is the lower: the actual cost or the net realizable value of the

inventory at the time of valuation.

The term net realizable value, on the other hand, is more complicated. As

you have already noticed, this value is the estimated selling price minus

any estimated costs to complete and sell the item. This net realizable value

is then compared to the actual cost in determining the lower–of-cost-or–net

realizable value.

PROBLEM 9.11 (Continued)

Proceed in the same way, always choosing the lowest among cost, and net

realizable value.

Cost of Goods Sold ………………………………………………………

790

Allowance to Reduce Inventory to NRV …………………

790

OR

Loss Due to Decline of Inventory to NRV ……………………….

790

Allowance to Reduce Inventory to NRV …………………

790

Schedule A

Item

On Hand

Quantity

Cost

NRV

Lower-of– Cost-

or-NRV

A

1,100

NT$7.50

NT$9.00

NT$7.50

C

1,000

5.45

Schedule B

Item

Cost

Lower-of-Cost-or-NRV

Difference

A

1,100 X NT$7.50 = NT$8,250

1,100 X NT$7.50 = NT$8,250

None

D

1,000 X NT$3.80 = NT$3,800

1,000 X NT$3.80 = NT$3,800

None

TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS

CA 9.1 (Time 15–25 minutes)

CA 9.2 (Time 20–30 minutes)

Purpose—to provide the student with an opportunity to examine ethical issues related to lower–of-cost-

or-net realizable value on an individual-product basis. A relatively straightforward case.

CA 9.3 (Time 15–20 minutes)

CA 9.4 (Time 25–30 minutes)

Purpose—to provide the student with an opportunity to discuss the main features of the retail inventory

CA 9.5 (Time 15–25 minutes)

Purpose—the student discusses which costs are inventoriable, the theoretical arguments for the lower-

CA 9.6 (Time 10–15 minutes)

Purpose—to provide the student with a case that allows examination of ethical issues related to the

recording of purchase commitments.

SOLUTIONS TO CONCEPTS FOR ANALYSIS

CA 9.1

(a) The purpose of using the LCNRV method is to reflect the decline of inventory value below its

original cost. A departure from cost is justified on the basis that a loss of utility should be reported

as a charge against the revenues in the period in which it occurs.

(d) Conceptually, the LCNRV method has some deficiencies. First, decreases in the value of the asset

and the charge to expense are recognized in the period in which loss in utility occurs—not in the

period of sale. On the other hand, increases in the value of the asset are recognized only at the

point of sale. This situation is inconsistent and can lead to distortions in the presentation of income

data.

CA 9.2

(a) The accountant’s ethical responsibility is to provide fair and complete financial information. In this

case, the cost-of–goods-sold method distorts the cost of goods sold and hides the decline in

market value.