EXERCISE 21.11 (20–30 minutes)

(a) The lease agreement has a bargain-purchase option. The collectibility of the

lease payments by Mooney is probable. The lease, therefore, qualifies as a sales-

type lease from the viewpoint of the lessor.

The lease payments associated with this lease are the periodic annual rents plus

the bargain purchase option. There is no residual value relevant to the lessor’s

accounting in this lease.

The lease receivable is computed as follows:

¥20,471.94 Annual rental payment

X 4.31213 PV of an annuity-due of 1 for n = 5, i = 8%

¥88,277.67 PV of periodic rental payments

(b) MOONEY LEASING (Lessor)

Lease Amortization Schedule

Date

Annual Lease

Payment Plus

BPO

Interest (8%)

on Lease

Receivable

Recovery

of Lease

Receivable

Lease

Receivable

5/1/19

¥91,000.00

5/1/19

¥ 20,471.94

¥20,471.94

70,528.06

55,698.36

5/1/22

5/1/23

¥91,000.00

EXERCISE 21.11 (Continued)

5/1/19

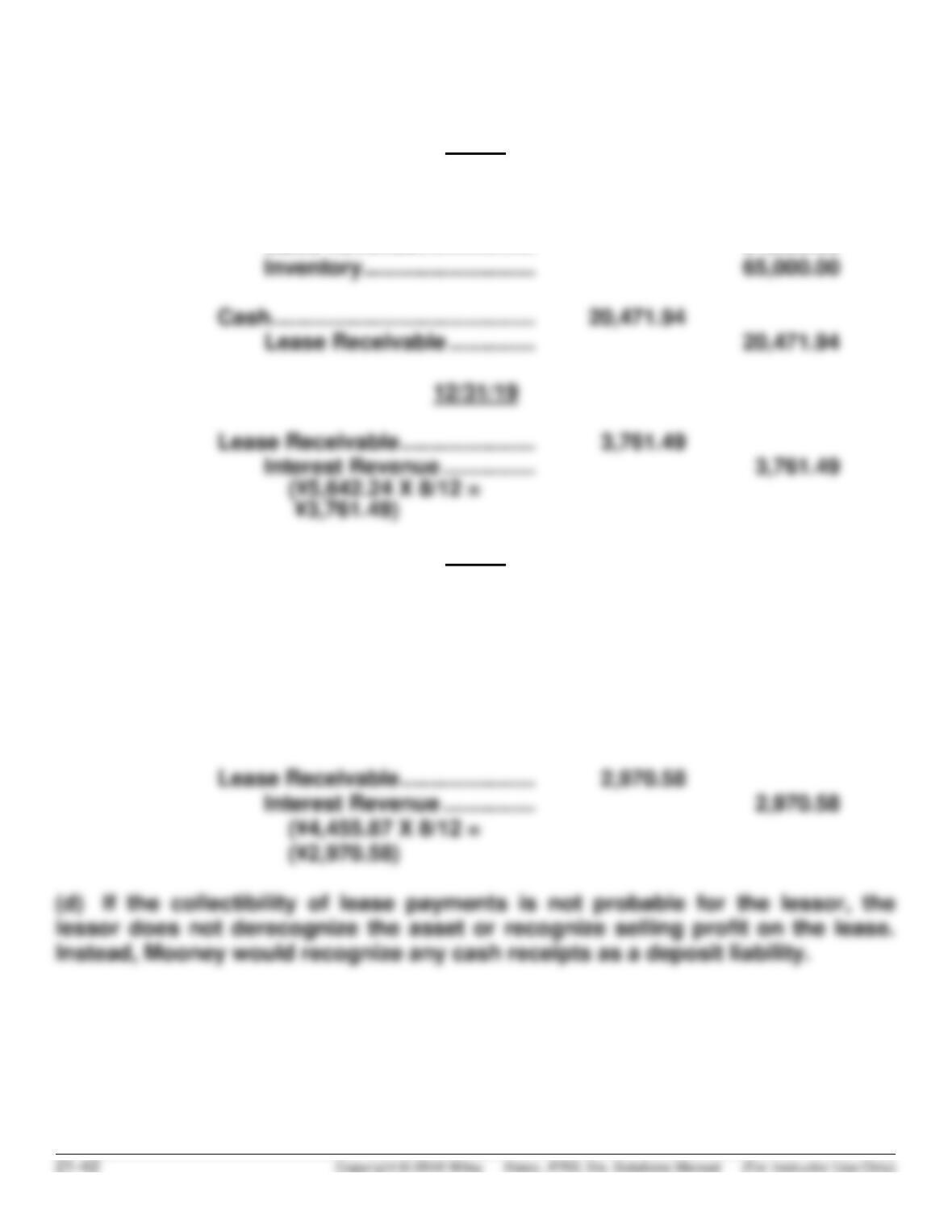

(c) Lease Receivable …………………. 91,000.00

Cost of Goods Sold ……………… 65,000.00

Sales Revenue ………………. 91,000.00

5/1/20

Cash……………………………………. 20,471.94

Lease Receivable ………….. 18,591.19

Interest Revenue …………… 1,880.75

(¥5,642.24 – ¥3,761.49)

12/31/20

EXERCISE 21.11 (Continued)

5/1/19

Cash …………………………………………………………………….. 20,471.94

Deposit Liability ……………………………………………… 20,471.94

EXERCISE 21.12 (20–25 minutes)

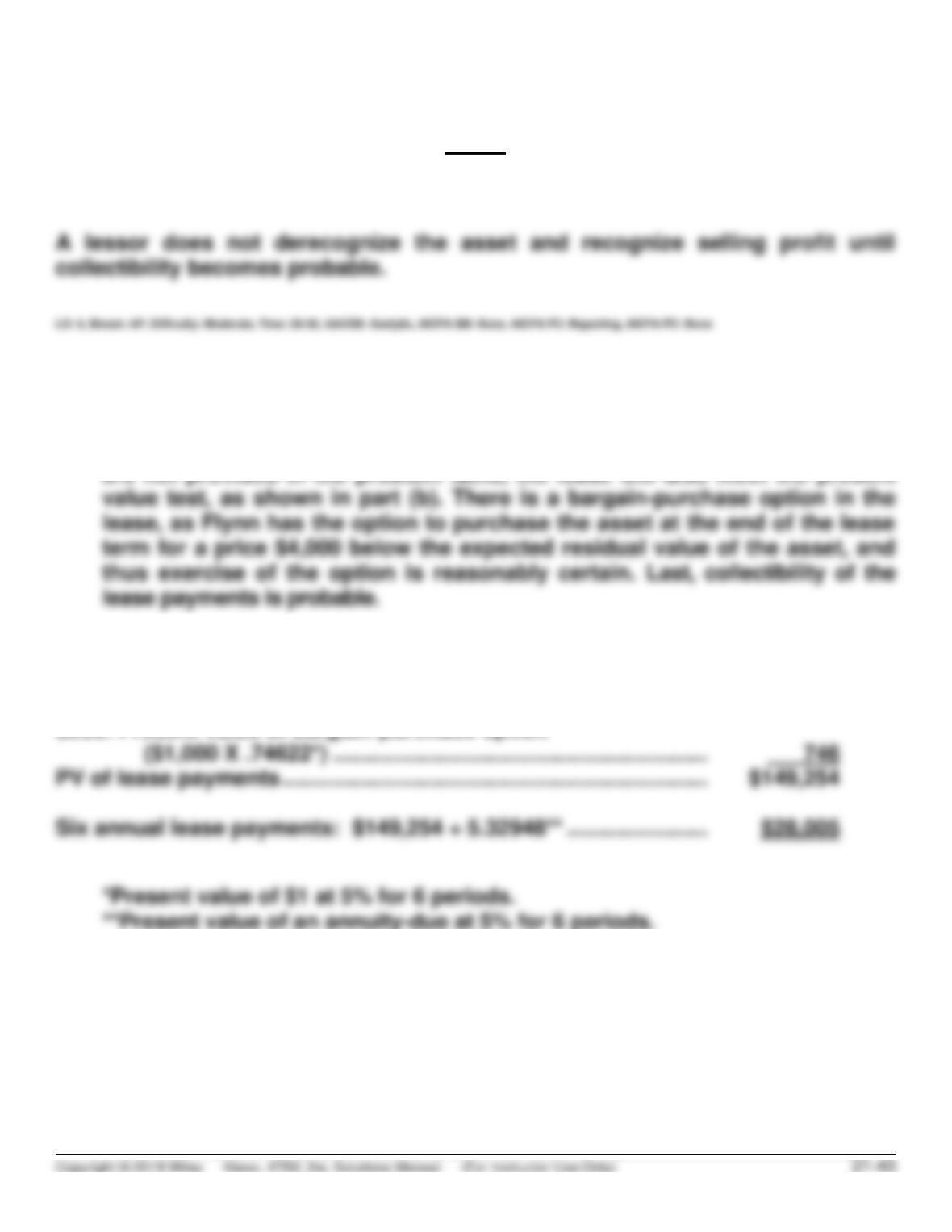

(a) This is a finance (sales-type) lease to Benson since the lease term is 75%

(6 ÷ 8) of the asset’s economic life. In addition, although the lease payments

(b) Computation of annual rental payment (by the lessor):

Fair value of leased asset ……………………………………………………… $150,000

Less: Present value of bargain-purchase option

EXERCISE 21.12 (Continued)

1/1/19

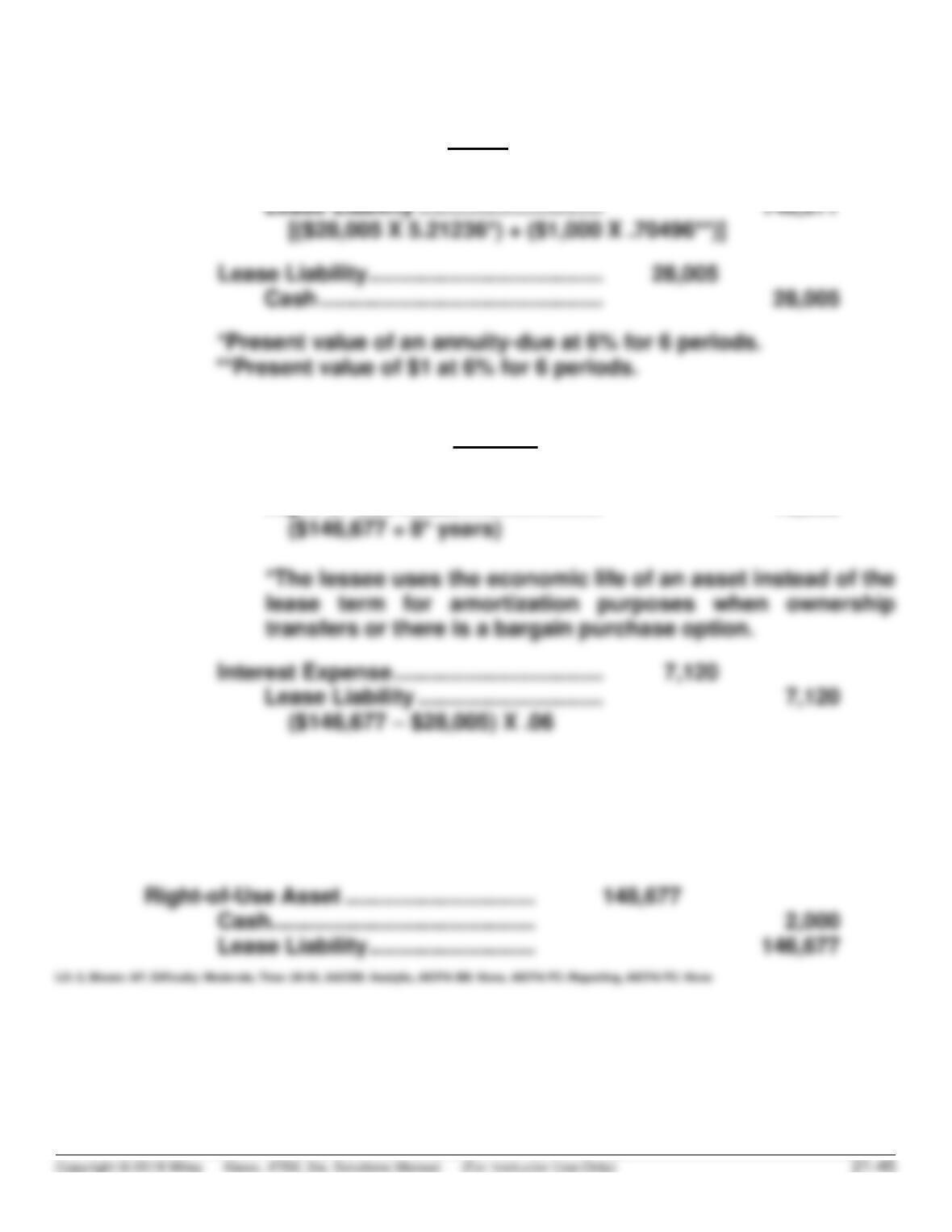

(c) Lease Receivable ………………………. 150,000*

Cost of Goods Sold …………………… 120,000

12/31/19

Lease Receivable ………………………. 6,100

Interest Revenue ………………… 6,100

[($150,000 – $28,005) X .05]

(d) If the collectibility of lease payments is not probable for the lessor, the

lessor does not derecognize the asset or recognize selling profit on the lease.

Instead, Bensen would recognize any cash receipts as a deposit liability.

EXERCISE 21.12 (Continued)

1/1/19

(e) Right-of-Use Asset ………………………… 146,677

12/31/19

Depreciation Expense ……………………. 18,335

Right-of–Use Asset ………………….. 18,335

(f) The value of the lease liability for the lessee is unaffected by any initial

direct costs incurred. However, the initial measurement of the right-of-use

asset must be adjusted for initial direct costs incurred. Thus, the initial

right-of–use asset should be measured at $148,677 ($146,677 + $2,000)

EXERCISE 21.13 (20-25 minutes)

(a) The lease will be classified as a sales-type lease for Phelps. While

ownership does not transfer at the end of the lease, there is no bargain purchase

option, the asset is not specialized, and the present value test is not met (see

calculation of lease liability for PV of lease payments), the lease term is greater

than 75% of the useful life of the asset (5 ÷ 6 = 83%).

The calculation of the lease receivable for Phelps is done as follows:

*This value should be used in performing the present value test. The lease fails

the present value test because £20,280 ÷ £23,000 = 88.2%, which is less than

90%.

*Rounded by £2.

The initial lease liability and right–of–use asset, from Walsh’s (lessee’s) point of

EXERCISE 21.13 (Continued)

(b)

Phelps’ Journal Entries

1/1/19

Lease Receivable ……………………….. 23,000*

Cash …………………………..……………… 4,703

Lease Receivable ……………….. 4,703

Walsh’s Journal Entries

1/1/19

Right-of–Use Asset ……………………… 20,280

Lease Liability ……………………. 20,280

EXERCISE 21.13 (Continued)

With respect to the initial measurement of the lease receivable, the lessor always

includes the residual value in the lease receivable, whether it is guaranteed or

not. Therefore, Phelps’ measurement of the lease receivable (£23,000) does not

change as a result of the guarantee.

(d) Walsh would need to include the present value of the amount probable to be

owed under the residual value guarantee in its initial measurement of the lease

liability. Because the expected residual value is less than the guaranteed

residual value, Walsh must include the present value of the difference, or the

amount it expects to pay Phelps at the end of the lease term. Thus, the initial

measurement of the lease liability and right-of-use asset would instead be:

EXERCISE 21.14 (20-25 minutes)

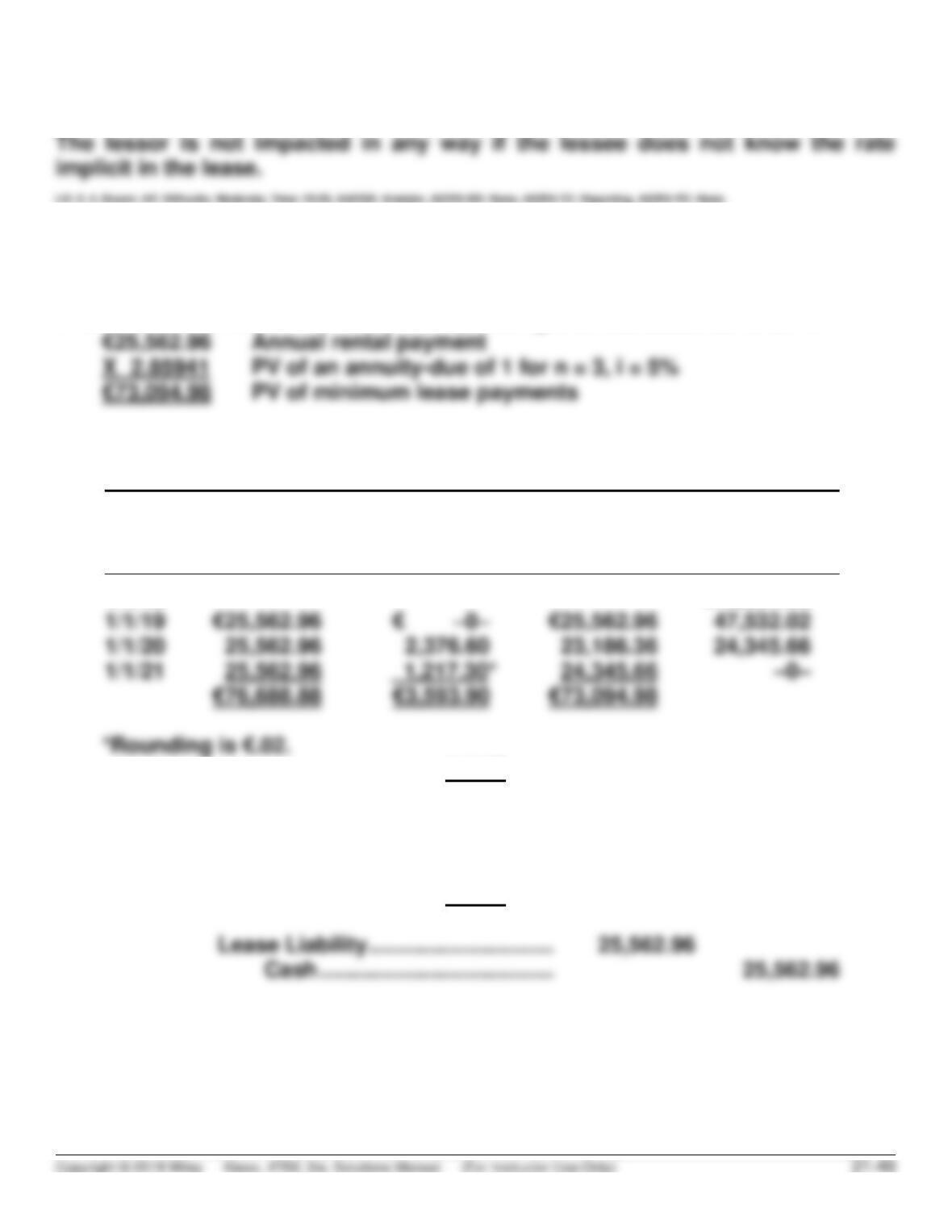

If the lessee is unaware of the rate implicit in the lease, it should use its

incremental borrowing rate to calculate the present value of the lease payments

EXERCISE 21.14 (Continued)

EXERCISE 21.15 (20–30 minutes)

The lessee determines the lease liability and right–of-use asset as follows:

(a) PLOTE AG (Lessee)

Lease Amortization Schedule

Date

Annual Lease

Payment

Interest (5%) on

Liability

Reduction

of Lease

Liability

Lease

Liability

1/1/19

€73,094.98

1/1/19

€25,562.96

€76,688.88

1/1/19

(b) Right-of-Use Asset …………………. 73,094.98

Lease Liability …………………. 73,094.98

1/1/19

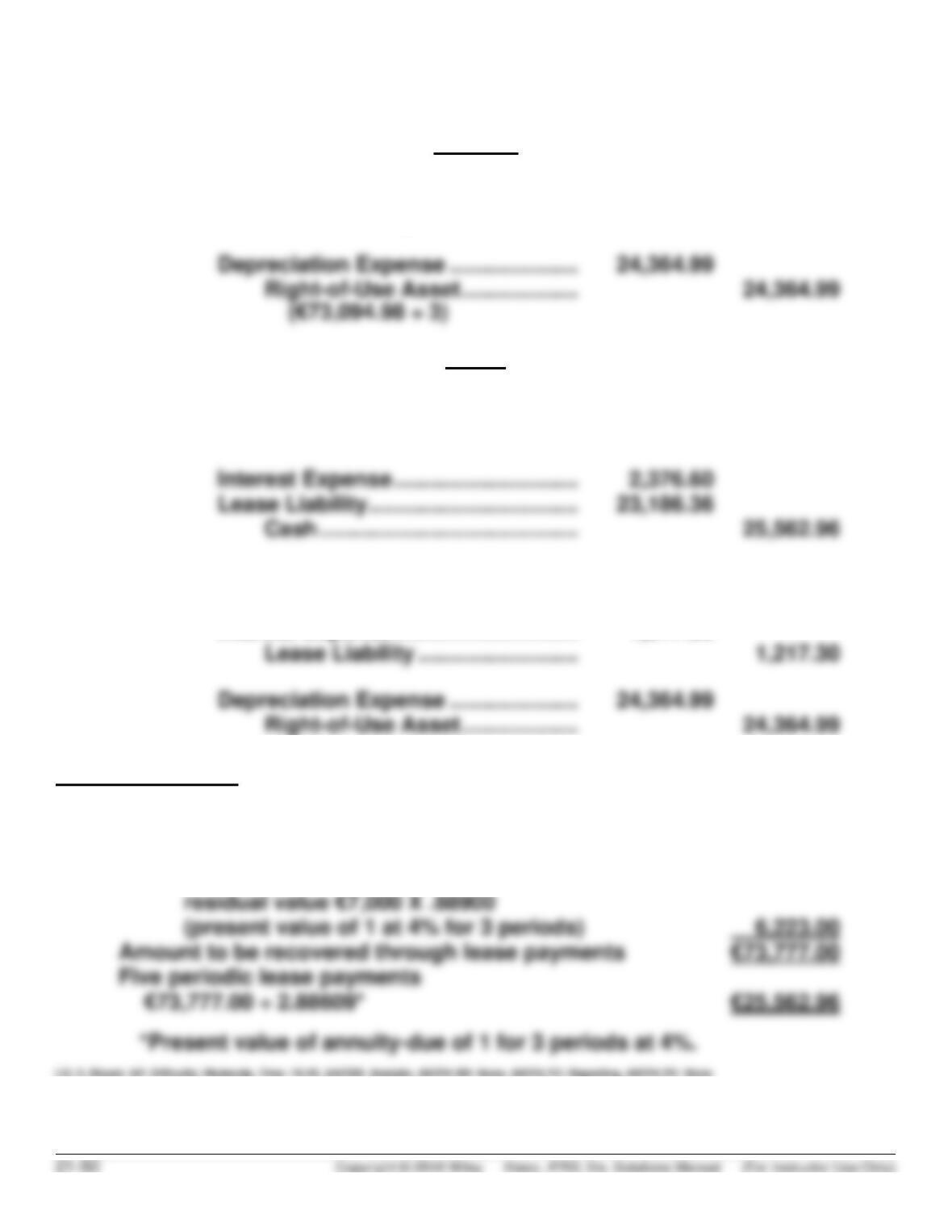

EXERCISE 21.15 (Continued)

12/31/19

Interest Expense ………………………… 2,376.60

Lease Liability …………………….. 2,376.60

1/1/20

Lease Liability ……………………………. 2,376.60

Interest Expense …………………. 2,376.60

12/31/20

Interest Expense ………………………… 1,217.30

Note to instructor:

1. The lessor sets the annual rental payment as follows:

Fair value of leased asset to lessor €80,000.00

Less: Present value of unguaranteed

EXERCISE 21.16 (20-25 minutes)

(a) The calculation for the present value of lease payments is as follows:

€4,892 Annual rental payment

The lessee applies the finance lease method, based on the following

amortization schedule.

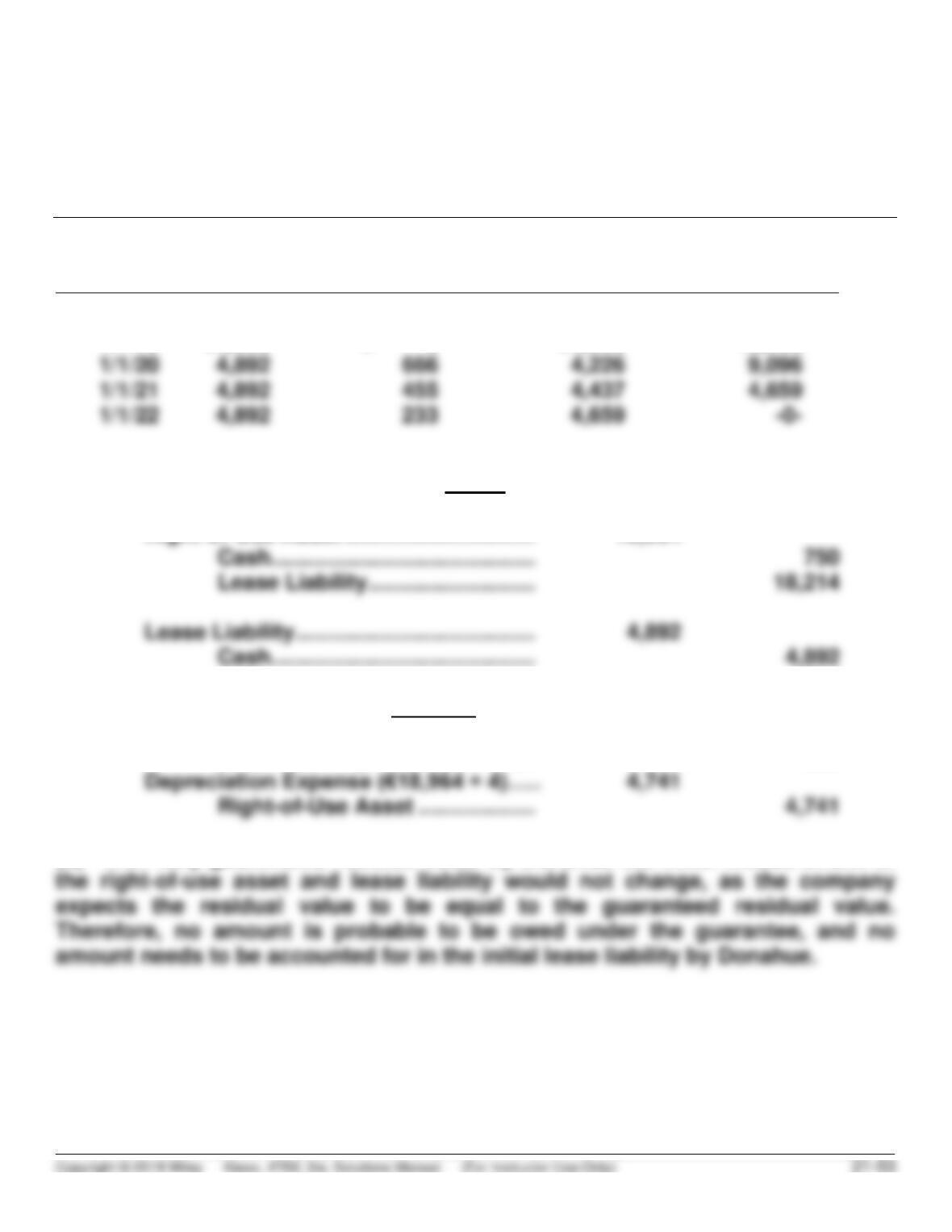

DONAHUE SA

Lease Amortization Schedule

Annuity-Due Basis

Date

Annual

Payment

Interest (5%) on

Liability

Reduction

of Lease

Liability

Lease Liability

1/1/19

€18,214

1/1/19

1/1/22

EXERCISE 21.16 (Continued)

(b) 1/1/19

Right-of–Use Asset …………………………. 18,214

Lease Liability ……………………… 18,214

12/31/19

Interest Expense …………………………….. 666

12/31/20

Interest Expense …………………………….. 455

1/1/20

Lease Liability ………………………………… 4,892

Cash……………………………………. 4,892

(c) Initial direct costs do not affect the value of the lease liability, but they do

change the value of the right–of–use asset. The initial measurement of the right–

EXERCISE 21.16 (Continued)

DONAHUE SA

Lease Amortization Schedule

Annuity-Due Basis

Date

Annual

Payment

Interest (5%) on

Liability

Reduction

of Lease

Liability

Lease Liability

1/1/19

€18,214

1/1/19

€4,892

€ 0

€4,892

13,322

1/1/20

1/1/21

1/1/22

1/1/19

Right-of–Use Asset …………………………. 18,964

12/31/19

Interest Expense …………………………….. 666

Lease Liability ……………………… 666

(d) With fully guaranteed residual value by Donahue the initial measurement of

EXERCISE 21.16 (Continued)

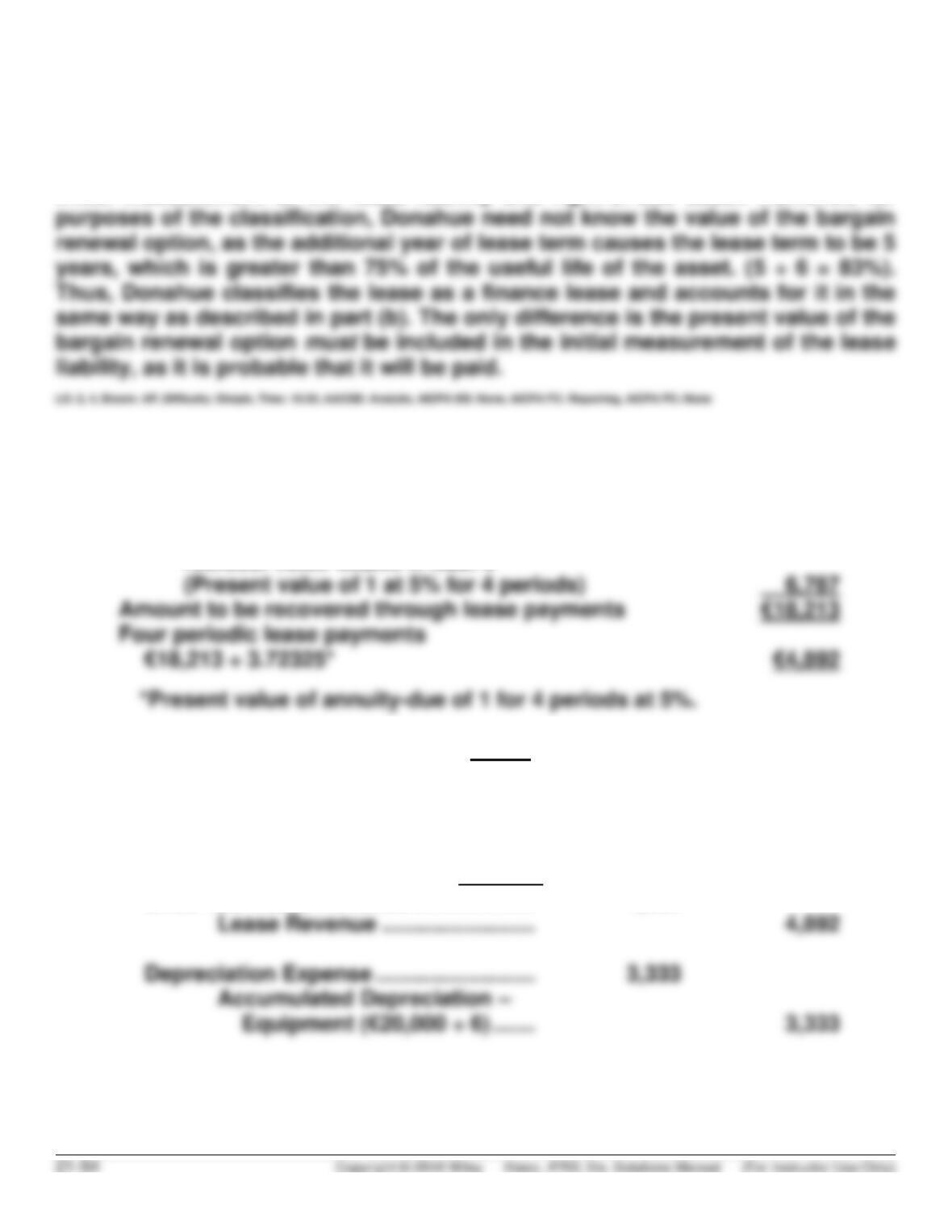

(e) A bargain renewal option would cause Donahue to take the additional year

(and payment) into account when determining how to classify the lease and the

initial measurement of the lease liability and right-of-use asset. However, for

EXERCISE 21.17 (25-30 minutes)

(a) Fair value of leased asset to lessor €25,000

Less: Present value of unguaranteed

residual value €8,250 X .82270

(b) 1/1/19

Cash ……………………………………………… 4,892

Unearned Lease Revenue …….. 4,892

12/31/19

Unearned Lease Revenue ……………….. 4,892

EXERCISE 21.17 (Continued)

(c) Even though the expected residual value declined, the fact that Donahue

has guaranteed a residual value of €8,250 leads Rauch to calculate rental

payments based on the same amount as if a residual value of $8,250 were

unguaranteed. That is, Rauch will look to recover through the lease payments

(d) A fully guaranteed residual value by Donahue would cause the lease to be

classified as a sales-type lease by Rauch. As a result, Rauch would recognize

sales revenue and a lease receivable at the commencement of the lease for the

(e) A bargain renewal option also would cause the lease to be classified as a

sales-type lease by Rauch, as it would cause the lease term to be 83% (5 ÷ 6 =

83%) of the economic life of the asset. Thus, the accounting for the lease by

Rauch would be essentially the same as explained in part (d). However, as sales

revenue, Rauch would only recognize the present value of the lease payments

*EXERCISE 21.18 (20–30 minutes)

Humphrey’s Restaurants (Seller-Lessee)

1/1/19

Cash ……………………………………………. 680,000

Equipment …………………………….. 600,000

Gain on Sale of Equipment …….. 80,000

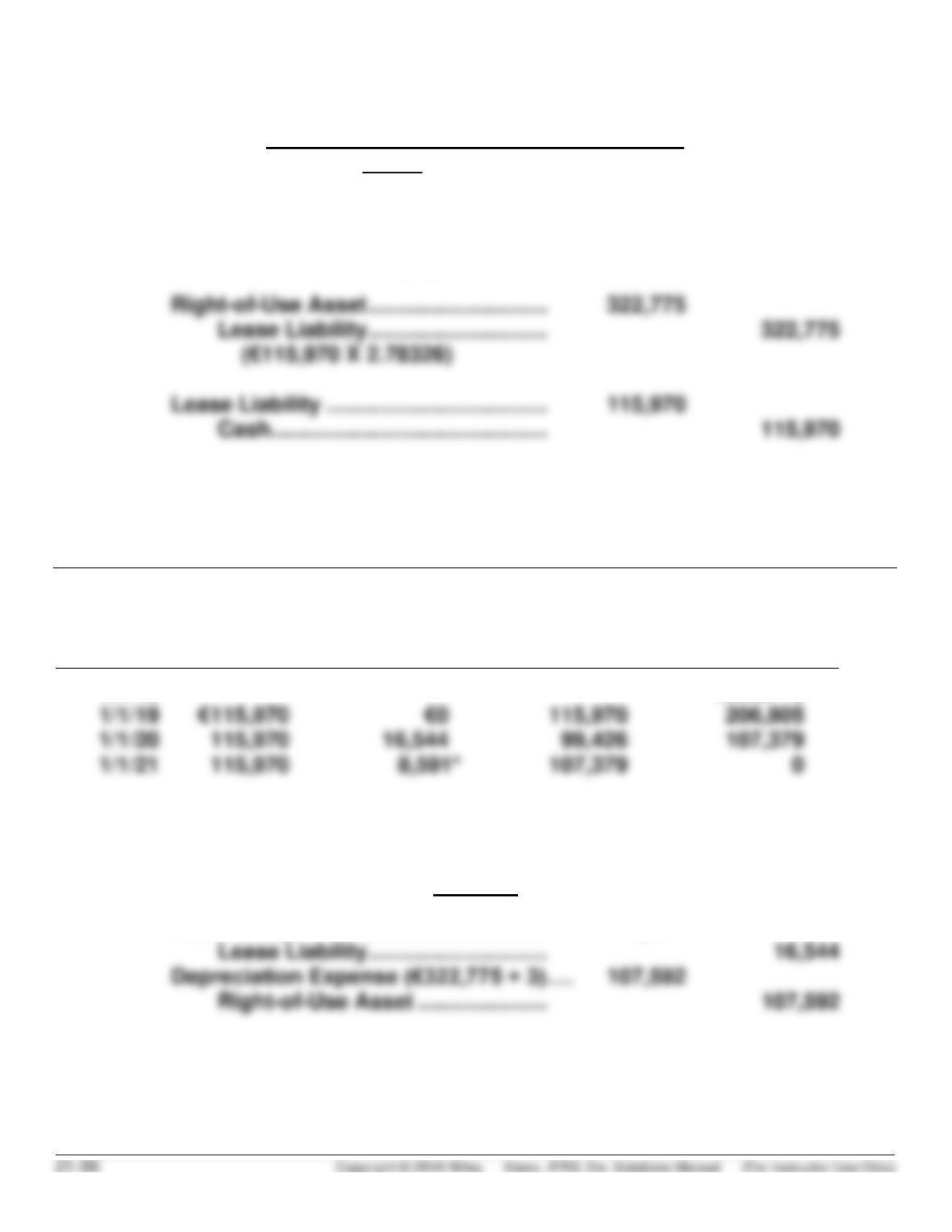

HUMPHREY’S RESTAURANTS NV

Lease Amortization Schedule

Annuity-Due Basis

Date

Annual

Payment

Interest (8%) on

Liability

Reduction

of Lease

Liability

Lease Liability

1/1/19

€322,775

*Rounded by €1.

12/31/19

Interest Expense ………………………….. 16,544

EXERCISE 21.18 (Continued)

Liquidity Finance (Buyer-Lessor)*

1/1/19

Equipment ……………………………………. 680,000

Cash …………………………………… 680,000

*EXERCISE 21.19 (20–30 minutes)

(a) The situation described is a simple sale of equipment. Only one entry for

the sale of the equipment is required:

1/1/19

(b) The situation described is known as a failed sale. That is, the terms of the

EXERCISE 21.19 (Continued)

1/1/19

Cash …………………………………………….. 520,000.00

Note Payable ……………………….. 520,000.00

(c) The situation described is considered a sale-leaseback agreement for

financial reporting purposes. That is, the terms of the lease meet the criteria

1/1/19

Cash …………………………………………….. 520,000

Equipment …………………………... 400,000

Gain on Disposal of Equipment 120,000

EXERCISE 21.19 (Continued)

ZARLE INC.

Lease Amortization Schedule

Annuity-Due Basis

Date

Annual

Payment

Interest (5%) on

Liability

Reduction

of Lease

Liability

Lease Liability

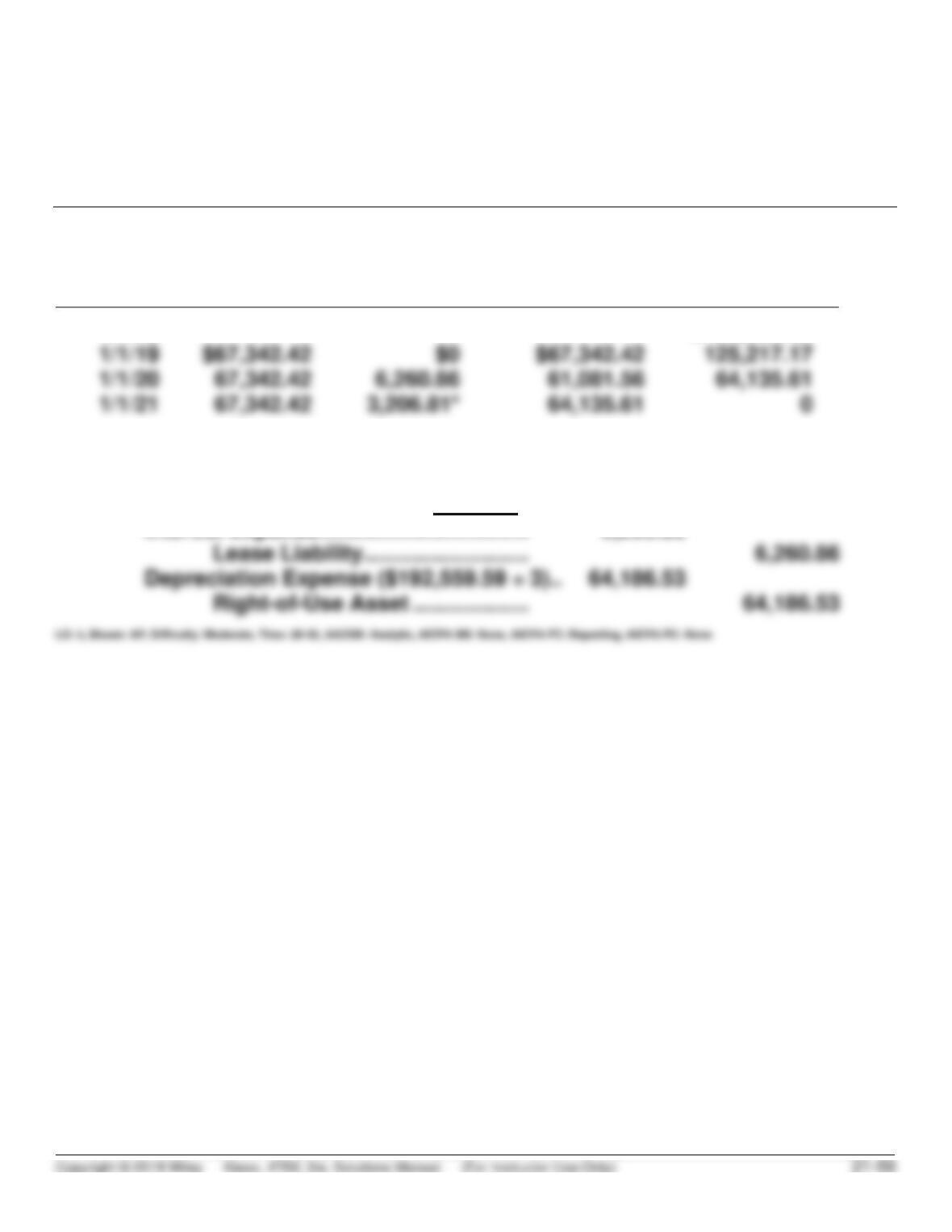

1/1/19

$192,559.59

*Rounded $.03

12/31/19

Interest Expense ……………………………. 6,260.86

TIME AND PURPOSE OF PROBLEMS

Problem 21.1 (Time 25–35 minutes)

Problem 21.2 (Time 20–30 minutes)

Purpose—to develop an understanding of the accounting by the lessee for a lease. The student is required to

explain the relationship between the capitalized amount of leased equipment and the leasing arrangement.

Problem 21.3 (Time 25–30 minutes)

Purpose—to develop an understanding of the accounting for a lessee in an annuity-due arrangement. The

Problem 21.4 (Time 20–30 minutes)

Problem 21.5 (Time 20–25 minutes)

Problem 21.6 (Time 20–25 minutes)

Purpose—to develop an understanding of the accounting principles used in a finance (sales-type) lease for

Problem 21.7 (Time 30–40 minutes)

Purpose—to develop an understanding of a sales-type lease with a guaranteed residual value. The student

Problem 21.8 (Time 30–40 minutes)

Purpose—to develop an understanding of a lease with a guaranteed residual value. The student computes the