CHAPTER 4

Income Statement and Related Information

ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC)

Topics

Questions

Brief

Exercises

Exercises

Problems

Concepts

for Analysis

1.

Income measurement

concepts.

1, 2, 3, 4, 5,

6, 7, 8, 9, 10,

11, 32

2, 3, 4, 6

Computation of net

income from balance

sheets and selected

accounts.

1, 3, 4, 5

1, 2, 3, 4, 8

3.

Condensed income

statements; earnings

per share.

12, 13, 14,

23, 25

1, 2, 4, 10

4, 5, 7, 8,

10, 11,

13, 17

3, 4, 6

1, 2, 5

4.

Detailed income

statements.

12, 14, 15,

16, 19, 20

3, 6

1, 5, 6,

7, 9

1, 2, 5

6

5.

Intraperiod tax

allocation.

21, 22, 24,

26, 27

9, 11, 13,

14, 16

2, 4, 7, 8

6.

Accounting changes;

discontinued

operations; prior

period adjustments;

errors.

16, 17, 18,

19, 24, 25,

27, 28, 29,

30

7, 8, 9

6, 8, 10, 11,

13, 14

4, 6, 7, 8

2, 3, 4, 5, 6

7.

Retained earnings

statement.

31

11, 12

9, 12,

16, 17

1, 2, 3,

5, 6, 7

8.

Comprehensive

income.

33, 34

13

15, 16,

7

Changes in equity.

ASSIGNMENT CLASSIFICATION TABLE (BY LEARNING OBJECTIVE)

Learning Objectives

Brief

Exercises

Exercises

Problems

Concepts

for

Analysis

1. Identify the uses and limitations

of an income statement.

1, 2, 3, 4,

5

5, 6, 7

6, 7, 8, 9, 11

6, 8

8, 9, 10

9, 10, 11, 13,

14, 15, 16, 17

6, 8

4. Explain the reporting of accounting

changes and errors.

8, 9, 12

8, 9, 12, 14

4, 5, 6, 7, 8

5, 6, 7

15, 16, 17,

6, 7

ASSIGNMENT CHARACTERISTICS TABLE

Item

Description

Level of

Difficulty

Time

(minutes)

E4.1

Compute income measures.

Simple

10–15

E4.2

Computation of net income.

Simple

18–20

E4.3

Income statement items.

Simple

25–35

E4.4

Income statement presentation.

Moderate

20–25

E4.5

Income statement.

Simple

20–25

E4.6

Income statement items.

Moderate

30–35

E4.7

Income statement.

Moderate

30–40

E4.8

Income statement, EPS.

Simple

15–20

E4.9

Simple

30–35

E4.10

Earnings per share.

Simple

20–25

E4.11

Condensed income statement—periodic inventory

method.

Moderate

20–25

E4.12

Retained earnings statement.

Simple

20–25

E4.13

Earnings per share.

Moderate

15–20

E4.14

Change in accounting principle.

Moderate

15–20

E4.15

Comprehensive income.

Simple

15–20

E4.16

Comprehensive income.

Moderate

15–20

E4.17

Various reporting formats.

Moderate

30–35

E4.18

Changes in equity.

Simple

10–15

P4.1

Income components.

Simple

5–10

P4.2

Income statement, retained earnings.

Moderate

30–35

P4.3

Income statement, retained earnings, periodic inventory.

Simple

25–30

P4.4

Income statement items.

Moderate

30–40

P4.5

Income statement, retained earnings.

Moderate

30–40

P4.6

Statement presentation.

Moderate

20–25

P4.7

Retained earnings statement, prior period adjustment.

Moderate

25–35

P4.8

Income statement.

Moderate

25–35

CA4.1

Identification of income statement deficiencies.

Simple

20–25

CA4.2

Earnings management.

Moderate

20–25

CA4.3

Earnings management

Simple

15–20

CA4.4

Income reporting items.

Moderate

30–35

CA4.5

Identification of income statement weaknesses.

Moderate

30–40

CA4.6

Classification of income statement items.

Moderate

20–25

CA4.7

Comprehensive income.

Simple

10–15

ANSWERS TO QUESTIONS

1. The income statement is important because it provides investors and creditors with information

that helps them predict the amount, timing, and uncertainty of future cash flows. It helps investors

and creditors predict future cash flows in a number of different ways. First, investors and creditors can

use the information on the income statement to evaluate the past performance of the enterprise.

2. Information on past transactions can be used to identify important trends that, if continued, provide

information about future performance. If a reasonable correlation exists between past and future

3. Some situations in which changes in value are not recorded in income are:

(a) Unrealized gains or losses on non-trading equity investments,

(b) Changes in the market values of long-term liabilities, such as bonds payable,

4. Some situations in which application of different accounting methods or estimates lead to comparison

problems include:

(a) Inventory methods—weighted average vs. FIFO,

(b) Depreciation methods—straight-line vs. accelerated,

(c) Accounting for long-term contracts—percentage-of-completion vs. completed-contract,

Questions Chapter 4 (Continued)

5. The transaction approach focuses on the activities that have occurred during a given period and

instead of presenting only a net change, a description of the components that comprise the change

is included. In the capital maintenance approach, only the net change (income) is reflected whereas

6. Earnings management is often defined as the planned timing of revenues, expenses, gains and

losses to smooth out bumps in earnings. In most cases, earnings management is used to increase

income in the current year at the expense of income in future years. For example, companies

7. Earnings management has a negative effect on the quality of earnings if it distorts the information

in a way that is less useful for predicting future cash flows. Within the Conceptual Framework,

8. Caution should be exercised because many assumptions and estimates are made in accounting

and the net income figure is a reflection of these assumptions. If for any reason the assumptions are

9. The term “quality of earnings” refers to the credibility of the earnings number reported. Companies

that use aggressive accounting policies report higher income numbers in the short-run. In such

10. Income is increases in economic benefits during the accounting period in the form of inflows or

enhancements of assets or decreases of liabilities that result in increases in equity, other than

those relating to contributions from shareholders.

Questions Chapter 4 (Continued)

11. The definition of income includes both revenues and gains. Gains represent items that meet the

definition of income and may or may not arise in the ordinary activities of a company.

12. (1) Gross profit is the difference between revenue and cost of goods sold and is reported in the

13. Ahold would report the “settlement of securities class action” loss in the other income and expense

section of its income statement.

14. (1) Interest expense is reported on the income statement between income from operations and

15. The “nature of expense” classification uses a natural expense approach (such as direct labor

incurred, advertising expense, depreciation expense) without having to make arbitrary allocations.

16. (a) A loss on discontinued operations is reported net of tax in the income statement between

income from continuing operations and net income.

17. (a) The write-down of plant assets due to impairment should be shown as an other income and

expense item.

(b) The delivery expense on goods sold should be shown as a selling expense in the income

statement. It is an ordinary expense to the company and represents a cost of selling goods.

(c) If the amount is immaterial, it may be combined with the depreciation expense for the year

and included as a part of the depreciation expense appearing in the income statement. If the

amount is material, it should be shown in the retained earnings statement as an adjustment to

the beginning balance of retained earnings.

Questions Chapter 4 (Continued)

18. (a) The remaining book value of the equipment should be depreciated over the remainder of the

five-year period. The additional depreciation (£425,000) is not a correction of an error and is not

shown as an adjustment to retained earnings. The change is considered a change in estimate.

(b) The loss should be shown as an Other income and expense item.

19. (a) Other income and expense section.

(b) Expense section or other income and expense.

(c) Expense section, as a selling expense, but sometimes reflected as an administrative expense.

20. Both formats are acceptable. The amount of detail reported in the income statement is left to the

judgment of the company, whose goal in making this decision should be to present financial

statements which are most useful to decision makers. We want to present a simple, understand-

21. Intraperiod tax allocation should not affect the reporting of an unusual gain. The IASB reserves

22. Intraperiod tax allocation has no effect on reported net income, although it does affect the amounts

reported for various components of income. The effects on these components offset each other so

Questions Chapter 4 (Continued)

23. If Neumann has preference shares outstanding, the numerator in its computation may be incorrect.

A better description of “earnings per share” is “earnings per ordinary share.” The numerator should

include only the earnings available to ordinary shareholders. Therefore, the numerator should be:

24. A loss on the disposal of a component of a business is reported separately from continuing

25. The earnings per share trend is not negative. A loss on discontinued operations is a one-time

occurrence which is not expected to be reported in the future. Therefore, earnings per share on

26. Tax allocation within a period is the practice of allocating the income tax for a period to such items

as income before income tax, discontinued operations, and prior period adjustments.

27. Tax allocation within a period (intraperiod) becomes necessary when a firm encounters such items

as discontinued operations or corrections of errors. Such allocation is necessary to bring about an

appropriate relationship between income tax expense and income from continuing operations,

discontinued operations etc.

Tax allocation within a period is handled by first computing the tax expense attributable to income

28. The assets, cash flows, results of operations, and activities of the plants closed would not appear to

be clearly distinguishable, operationally or for financial reporting purposes, from the assets, results of

29. Companies report corrections of errors as an adjustment (net of tax) to the beginning balance of

Questions Chapter 4 (Continued)

30. A change in accounting principle has no effect on the current year’s net income because it is

31. The major items reported in the retained earnings statement are: (1) adjustments of the beginning

balance for corrections of errors or changes in accounting principle, (2) the net income or loss for

32. IFRS is ordinarily concerned only with a “fair presentation” of business income. In contrast, taxable

income is a statutory concept which defines the base for raising tax revenues by the government,

and any method of accounting which meets the statutory definition will “clearly reflect” taxable

income as defined by relevant tax laws. It should be noted that many tax systems prohibit use of

the cash receipts and disbursements method as a method which will clearly reflect income in

accounting for purchases and sales if inventories are involved.

The cash receipts and disbursements method will not usually fairly present income because:

(1) The completed transaction, not receipt or disbursement of cash, increases or diminishes

33. Other comprehensive income may be displayed (reported) in one of two ways: (1) a single

continuous statement (one statement approach) or (2) consecutive statements of net income and

34.

GRIBBLE AG

Comprehensive Income Statement

For the Year Ended 2019

(in thousands of Euros)

Net income ………………………………………………………………………………………… €150

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 4.1

STARR LTD

Income Statement

For the Year 2019

Sales Revenue ……………………………………………………….

£540,000

Cost of goods sold ……………………………………………………

330,000

Gross profit ………………………………………………………………

210,000

Selling expenses ………………………………………………………

£120,000

Administrative expenses …………………………..………………

10,000

Income before income tax …………………………………………

Income tax ……………………………………………………………….

BRIEF EXERCISE 4.2

BRISKY CORPORATION

Income Statement

For the Year Ended December 31, 2019

Net sales ……………………………………………………….

$2,400,000

Cost of goods sold ………………………………………….

1,450,000

Gross profit ……………………………………………….

950,000

Selling expenses …………………………………………….

$280,000

Administrative expenses …………………………………

212,000

492,000

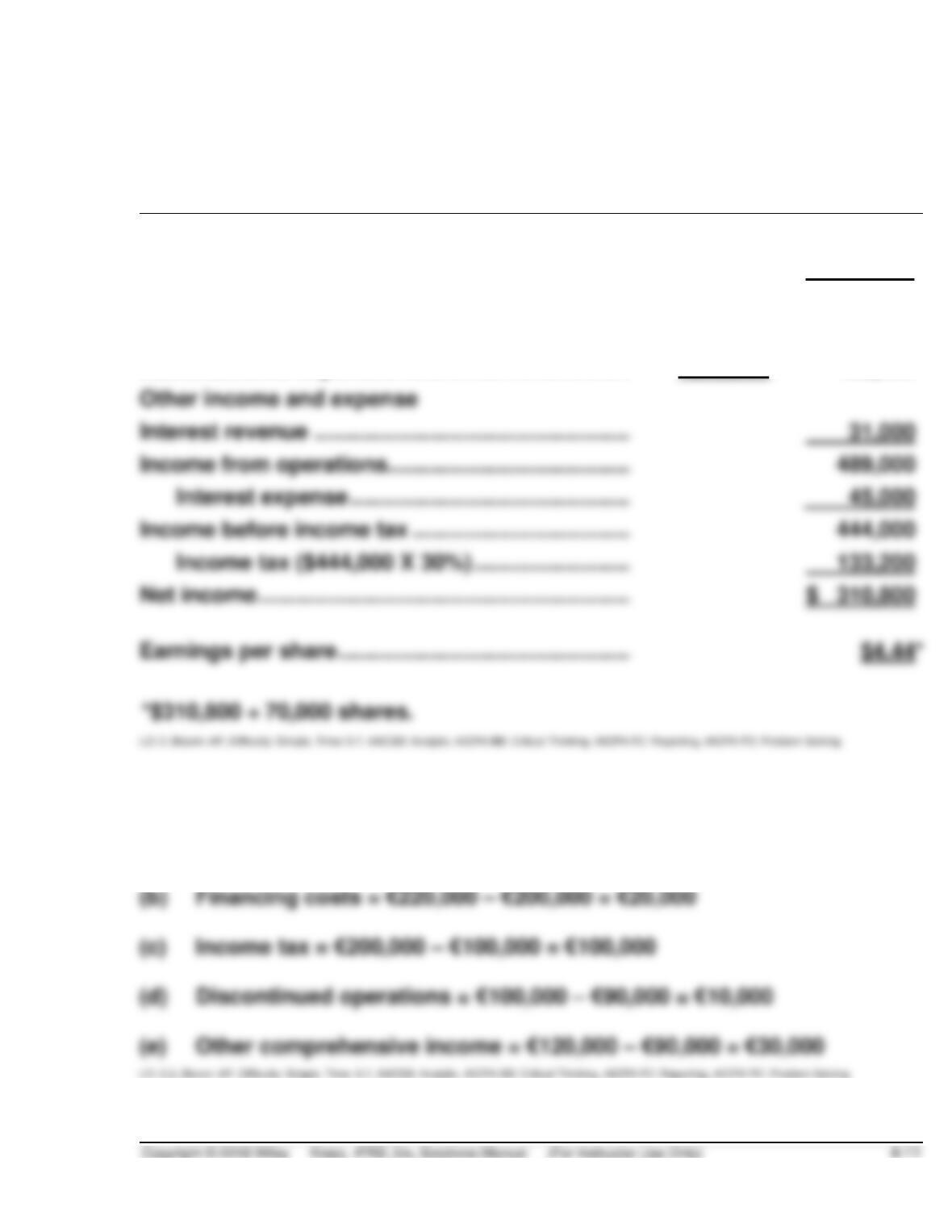

Other income and expense

Interest revenue ……………………………………………..

31,000

Income from operations…………………………………..

489,000

Interest expense ………………………………………..

Income before income tax ……………………………….

444,000

Income tax ($444,000 X 30%) ………………………

133,200

BRIEF EXERCISE 4.3

(a) Other income and expense = €800,000 – €500,000 – €220,000 = €80,000

BRIEF EXERCISE 4.4

1. Income from operations = HK$100,000 – HK$55,000 – HK$10,000 +

HK$30,000 = HK$65,000

BRIEF EXERCISE 4.5

BRIEF EXERCISE 4.6

1. Income from operations

2. Income before income tax

BRIEF EXERCISE 4.7

Income from continuing operations ……………………..

£10,600,000

Discontinued operations

restaurant division (net of tax) …………………

Loss from disposal of restaurant division

(net of tax) ………………………………………………

Net income …………………………………………………………

£10,096,000

Earnings per share ……………………………………………..

Income from continuing operations …………….

Discontinued operations, net of tax ……………..

Loss from operation of discontinued

BRIEF EXERCISE 4.8

2019

2018

2017

Income before income tax

$180,000

$145,000

$170,000

Income tax (30%)

54,000

43,500

51,000

Net income

$126,000

$101,500

$119,000

BRIEF EXERCISE 4.9

Vandross would not report any cumulative effect because a change in estimate

BRIEF EXERCISE 4.10

BRIEF EXERCISE 4.11

TSUI LTD

Retained Earnings Statement

For the Year Ended December 31, 2019

Retained earnings, January 1 …………………………………….

NT$ 675,000

Add: Net income ……………………………………………………..

1,400,000

2,075,000

Less: Cash dividends ………………………………………………

75,000

BRIEF EXERCISE 4.12

TSUI LTD

Retained Earnings Statement

For the Year Ended December 31, 2019

Retained earnings, January 1, as reported …………………….

NT$ 675,000

prior period (net of tax) ……………………………………….

Retained earnings, January 1, as adjusted ……………………

Add: Net income ……………………………………………………….

Less: Cash dividends ………………………………………………….

Correction for overstatement of expenses in

BRIEF EXERCISE 4.13

(a) Net income (Dividend revenue) ………………………..

¥3,000,000

(c) Unrealized holding gain

(Other comprehensive income) ………………………..

¥4,000,000

(d) Accumulated other comprehensive income,

January 1, 2019 ……………………………………………

¥ 0

¥4,000,000

SOLUTIONS TO EXERCISES

EXERCISE 4.1 (10–15 minutes)

Sales revenue ……………………………………………………………….. €310,000

Cost of goods sold ………………………………………………………… 140,000

Gross profit …………………………………………………………………… 170,000

Selling and administrative expenses ………………………………. 50,000

Other income and expense

Net income ……………………………………………………………………. €132,000

Unrealized gain on non-trading equity securities …………….. 10,000

Comprehensive income …………………………………………………. €142,000(d)

EXERCISE 4.2 (15–20 minutes)

Computation of net income

Change in assets:

Change in liabilities:

Change in equity:

EXERCISE 4.2 (Continued)

Change in equity accounted

for as follows:

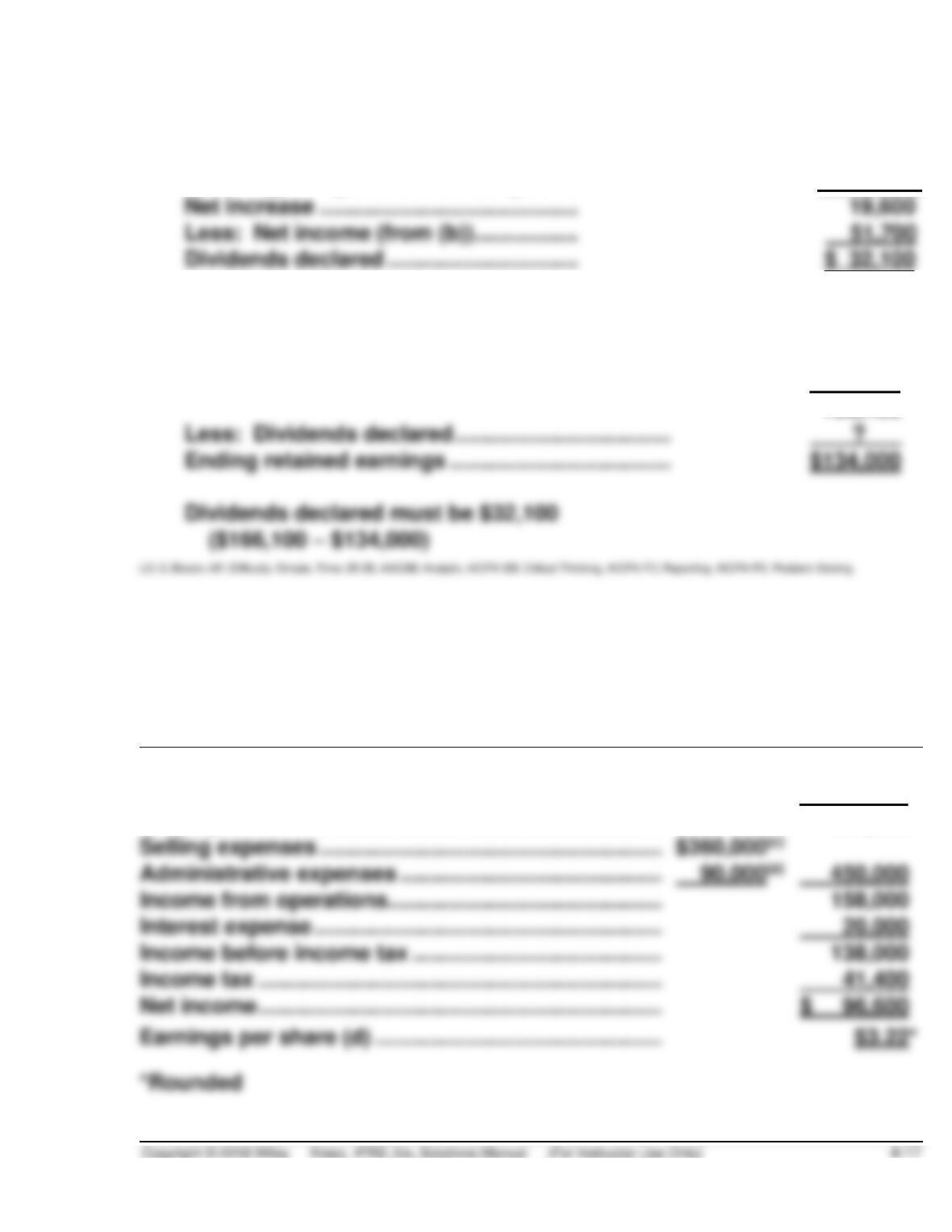

Net increase ………………………………………………….

£163,000

Increase in shares …………………………………

£138,000

Decrease in retained earnings due to

dividend declaration ………………………….

Net increase accounted for …………………………...

EXERCISE 4.3 (25–35 minutes)

(a)

Total net revenue:

Sales revenue ………………………….

$400,000

Less: Sales discounts …………….

$ 7,800

Sales returns …………………

20,200

Net sales …………………………………

Dividend revenue …………………….

Rental revenue ………………………..

6,500

(b)

Net income:

Total net revenue (from a) ………..

$457,300

Expenses:

Cost of goods sold …………….

$184,400

Selling expenses ……………….

99,400

Administrative expenses ……

Interest expense ………………..

12,700

Total expenses …………….

Income before income tax ………..

Income tax ………………………………

26,600

EXERCISE 4.3 (Continued)

(c)

Dividends declared:

Ending retained earnings …………

$134,000

Beginning retained earnings …….

(114,400)

Net increase ……………………………………

Less: Net income (from (b)) ……………..

Dividends declared ………………………….

$ 32,100

ALTERNATE SOLUTION (for (c))

Beginning retained earnings ………………………….

$114,400

Add: Net income ………………………………………….

51,700

166,100

Less: Dividends declared ……………………………..

?

Ending retained earnings ………………………………

$134,000

Dividends declared must be $32,100

($166,100 – $134,000)

EXERCISE 4.4 (20–25 minutes)

DUNBAR INC.

Income Statement

For Year Ended December 31, 2019

Net sales ($1,125,000(b) – $17,000) …………………………..

$1,108,000

Cost of goods sold …………………………………………………..

500,000

Gross profit ……………………………………………………………..

608,000

Selling expenses ……………………………………………………..

Administrative expenses ………………………………………….

450,000

Income from operations……………………………………………

158,000

Interest expense ………………………………………………………

20,000

Income before income tax ………………………………………..

138,000

Income tax …………………………..………………………………….

41,400

EXERCISE 4.4 (Continued)

Determination of amounts

(a) Administrative expenses

=

18% of cost of goods sold

=

18% of $500,000

=

$90,000

(b) Gross sales X 8%

=

administrative expenses

=

$90,000 ÷ 8%

Gross sales

=

$1,125,000

(c) Selling expenses

=

four times administrative expenses.

(since selling expenses are 4/5

of selling and administrative

expenses, selling expenses are

4 times administrative expenses.)

=

4 X $90,000

=

$360,000

(d) Earnings per share $3.22 ($96,600 ÷ 30,000)

EXERCISE 4.5 (20–25 minutes)

WEBSTER PLC

Income Statement

For the Year Ended December 31, 2019

(In thousands, except earnings per share)

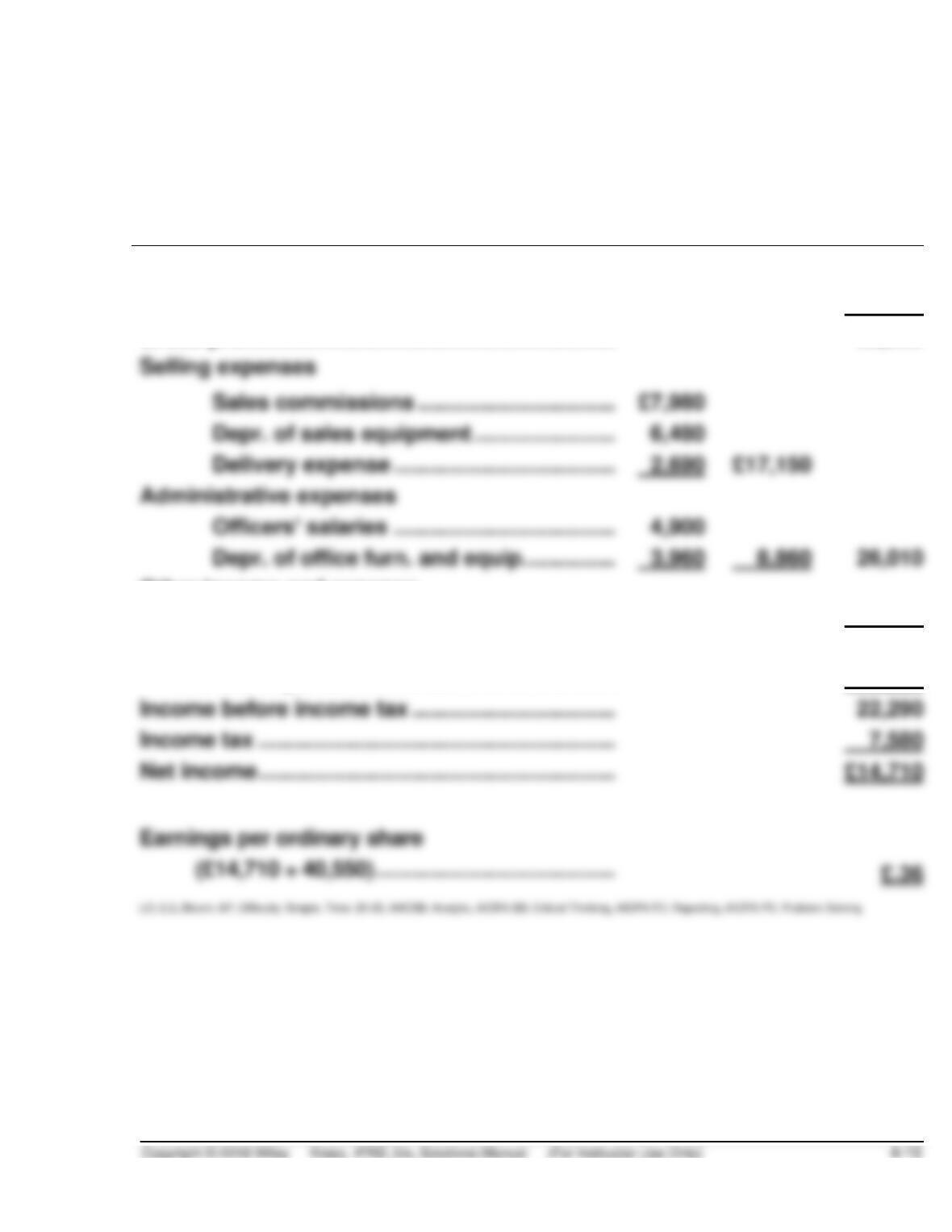

Sales revenue ……………………………………………..

£96,500

Cost of goods sold ………………………………………

63,570

Gross profit …………………………………………………

32,930

Sales commissions …………………………..

Depr. of sales equipment …………………..

Delivery expense ………………………………

Administrative expenses

Officers’ salaries ………………………………

Other income and expense

Rent revenue ………………………………………

17,230

Income from operations……………………………….

24,150

Interest expense …………………………………….

1,860

Income before income tax …………………………...

22,290

Income tax …………………………..……………………..

7,580

EXERCISE 4.6 (30–35 minutes)

PARNEVIK ASA

Income Statement

For the Year Ended December 31, 2019

Revenue

Sales revenue …………………………………………………..

€1,280,000

Less: Sales returns and allowances ………………….

€150,000

Sales discounts ………………………………………

45,000

195,000

Net sales revenue ……………………………………………..

Cost of goods sold ……………………………………………

621,000

Gross profit ……………………………………………………….

464,000

Selling expenses ……………………………………………

194,000

Admin. and general expenses …………………………

97,000

291,000

Other Income and Expense

Loss from impairment of plant assets …………………

(120,000)

Interest revenue ……………………………………………….

86,000

(34,000)

Income from operations …………………………………………..

139,000

Interest expense ………………………………………………

Income before income tax ……………………………………….

79,000

Income tax (€79,000 X .34) …………………………..

Net income ……………………………………………………….

Earnings per share (€52,140 ÷ 100,000) ………………………