CA 16.7

Dear Mr. Dolan:

I hope that the following brief explanation helps you understand why your warrants were not included in

Rhode’s earnings per share calculations.

However, corporations that have outstanding a variety of other securities—convertible bonds,

convertible preference shares, share options, and share warrants—have a complex capital structure.

Because these securities could be converted to ordinary shares they have a potentially “dilutive” effect

on EPS.

In order not to mislead users of financial information, the accounting profession insists that EPS

If we assume that Rhode exercises 30,000 warrants at $30, the company does not simply add 30,000

shares to ordinary shares outstanding; rather, for diluted EPS, Rhode is assumed to purchase and

retire 36,000 [(30,000 X $30) ÷ $25] treasury shares at $25 with the proceeds. Therefore, if you add the

30,000 exercised warrants to the ordinary shares outstanding and then subtract the 36,000 shares

Sincerely,

Ms. Smart Student

FINANCIAL REPORTING PROBLEM

(a) See note 13.

1. Under M&S’s share-based compensation plan 10,437,215 options

were granted during 2016.

4. The options expire 3 years after the date of grant.

(b)

(In millions—except per share)

2016

2015

Weighted average ordinary shares

1,642.2

1,646.9

Diluted earnings per share

24.8p

29.5p

COMPARATIVE ANALYSIS CASE

(a) adidas pays employees a salary and a cash performance bonus based

on net income. adidas does not have a stock option plan.

(b)

2015

201,536

14,940

2014

208,776

14,940

(c)

Diluted Earnings Per Share

(in millions)

adidas

Puma

ACCOUNTING, ANALYSIS, AND PRINCIPLES

ACCOUNTING

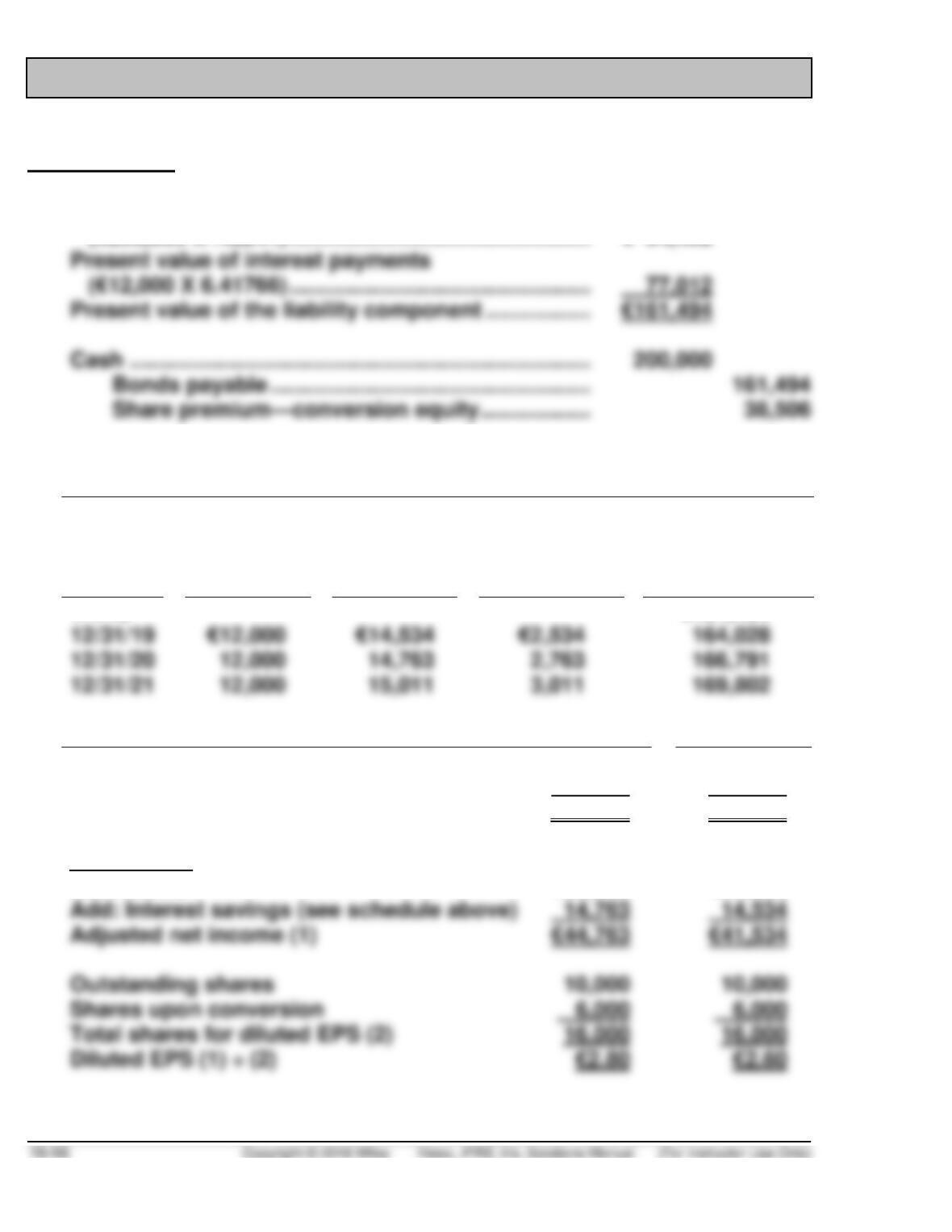

(a) Present value of principal:

(€200,000 X .42241) …………………………………………. € 84,482

Amortization Schedule

Date

Cash Paid

Interest

Expense

(9%)

Discount

Amortized

Carrying Value

of Bonds

1/1/19

€161,494

12/31/19

(b)

Basic EPS

2020

2019

Net income

€30,000

€27,000

Outstanding shares

÷10,000

÷10,000

Basic EPS

€ 3.00

€ 2.70

Diluted EPS

Net income

€30,000

€27,000

Add: Interest savings (see schedule above)

Adjusted net income (1)

€44,763

€41,534

Outstanding shares

Shares upon conversion

Total shares for diluted EPS (2)

Diluted EPS (1) ÷ (2)

ACCOUNTING, ANALYSIS, AND PRICIPLES (Continued)

(c) Conversion Expense (€50 X 200) ………………………… 10,000

ANALYSIS

EPS Presentation

2020

2019

Net income

€30,000

€27,000

Diluted EPS

€ 2.80

€ 2.60

EPS standards are important to analysts who rely on reported earnings per

PRINCIPLES

IFRS for convertible debt primarily differs from U.S. GAAP on convertible

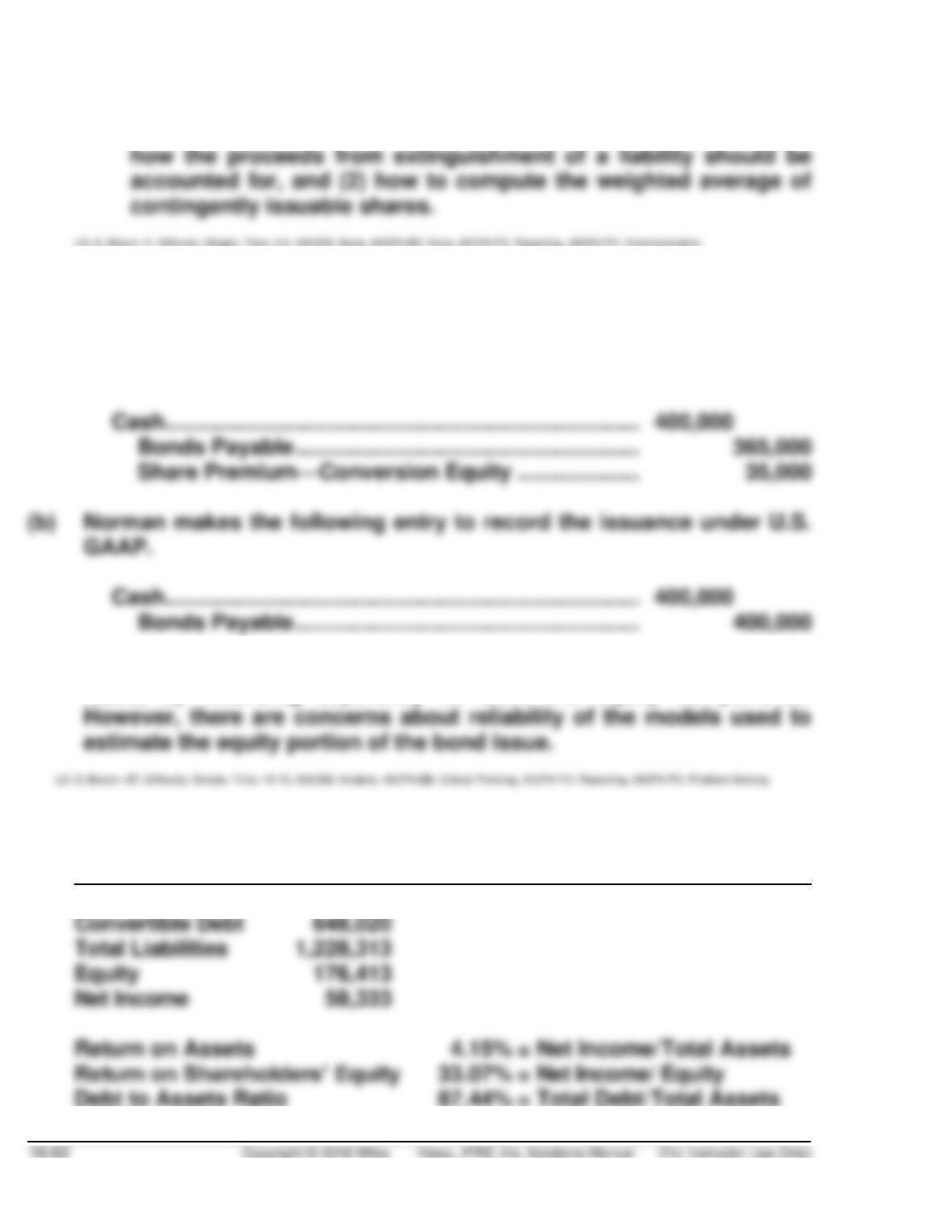

Cash ……………………………………………………………………….. 200,000

Bonds Payable…………………………………………………… 200,000

ACCOUNTING, ANALYSIS, AND PRICIPLES (Continued)

Supporters of the IFRS treatment would argue that separating the bond

issue into liability and equity components provides more representationally

faithful information in the financial statements. That is, the resulting

financial statements do a better job of representing the underlying

economics of the transaction. When bond investors buy bonds with a

RESEARCH CASE

(a) IFRS 2 addresses the accounting for share-based payment

compensation plans.

(b) The objectives for accounting for stock compensation are (as stated by

IFRS 2, paragraph 1): The objective of this IFRS is to specify the

financial reporting by an entity when it undertakes a share-based

(c) When the goods or services received or acquired in a share-based

payment transaction do not qualify for recognition as assets, they shall

be recognised as expenses (par.8).

For equity-settled share-based payment transactions, the entity shall

measure the goods or services received, and the corresponding

RESEARCH CASE (Continued)

Typically, shares, share options or other equity instruments are

granted to employees as part of their remuneration package, in

addition to a cash salary and other employment benefits. Usually, it is

part of basic remuneration, e.g. as an incentive to the employees to

remain in the entity’s employ or to reward them for their efforts in

improving the entity’s performance. By granting shares or share

options, in addition to other remuneration, the entity is paying

additional remuneration to obtain additional benefits. Estimating the

GAAP CONCEPTS and APPLICATION

16.1. Similarities

• U.S. GAAP and IFRS follow the same model for recognizing

share-based compensation: The fair value of shares and options

awarded to employees is recognized over the period to which the

employees’ services relate.

• Although the calculation of basic and diluted earnings per share

Differences

• A significant difference between U.S. GAAP and IFRS is the

accounting for securities with characteristics of debt and equity,

• Related to employee share-purchase plans, these plans under

U.S. GAAP are often considered non-compensatory and therefore

no compensation is recorded. However, certain conditions must

GAAP Concepts and Application (Continued)

• Other EPS differences relate to (1) the treasury-share method and

16.2.

(a) Under IFRS, Norman must “bifurcate” (split out) the equity

component—the value of the conversion option—of the bond issue.

Under IFRS, the convertible bond issue is recorded as follows.

(c) IFRS provides a more faithful representation of the impact of the bond

issue, by recording separately its debt and equity components.

16.3

(a) Account

Current Liabilities $ 554,114

Concepts and Application (Continued)

(b) Sepracor is doing very well. Its ROA and ROE are above the industry

average. However, its debt level is quite high, compared to the

(c) Under IFRS, the debt and equity components of a convertible bond are

separately recorded as liabilities and equity. Assuming a liability

Reclassified:

Account

Current Liabilities $554,114

Convertible Debt 398,020

Total Liabilities 978,313 [$1,228,313 – ($648,020 – $398,020)]