CHAPTER 21

Accounting for Leases

ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC)

Topics

Questions

Brief

Exercises

Exercises

Problems

Concepts

for

Analysis

1. Rationale for leasing.

1, 2, 3

28, 29

18, 19

6

4. Special Issues

Other lease costs;

26, 27

15, 16, 21,

22, 23, 24,

25

9, 16, 17

6, 7, 8, 12,

13, 14

3, 4, 5

ASSIGNMENT CLASSIFICATION TABLE (BY LEARNING OBJECTIVE)

Learning

Objectives

Questions

Brief

Exercises

Exercises

Problems

Concepts for

Analysis

1. Describe the

environment

related to

leasing

transactions.

1, 2, 3

3. Explain the

accounting for

leases by

lessors.

11, 13,

6, 7, 8, 9,

6, 7, 9,

2, 5

2. Explain the

4, 5, 6, 7,

1, 2, 3, 4,

1, 2, 3, 4, 7,

1, 2, 3, 4,

1, 2, 3, 4 5

accounting for

sale-leaseback

transactions.

28, 29

18, 19

6

4. Discuss the

accounting and

reporting for

special

10, 21,

23, 26,

27

22, 23, 24,

25

6, 9, 10, 11,

12, 14, 16,

17

1, 2, 7, 8,

12, 13, 14

3, 4, 5

ASSIGNMENT CHARACTERISTICS TABLE

Item

Description

Level of

Difficulty

Time

(minutes)

E21.1

Lessee Entries; No Residual Value

Moderate

15–20

E21.2

Lessee Entries; Lease with Unguaranteed Residual

Value

Moderate

15–20

E21.3

Lessee Computations and Entries; Lease with

Guaranteed Residual Value

Moderate

20–25

E21.4

Lessee Entries; Lease and Unguaranteed Residual

Value

Moderate

20–30

E21.5

Computation of Rental; Journal Entries for Lessor

15–25

E21.6

Lessor Entries; Sales-Type Lease with Option to

Purchase

Moderate

20–25

E21.7

Moderate

15–20

E21.8

Lessor Entries; Sales-Type Lease

Moderate

15–20

E21.9

Lessee Entries; Initial Direct Costs

Moderate

20–25

E21.10

Lessee Entries with Bargain-Purchase Option

Moderate

20–30

E21.11

Lessor Entries with Bargain-Purchase Option

Moderate

20–30

E21.12

Lessee-Lessor Entries; Sales-Type Lease with a

Bargain Purchase Option

Moderate

20–25

E21.14

Lessee Entries; Initial Direct Costs

20–25

E21.15

Moderate

20–30

Moderate

20–25

E21.17

Lessor Accounting for an Operating Lease

Moderate

25–30

*E21.18

Sale-Leaseback

Moderate

20–30

*E21.19

Lessee-Lessor, Sale-Leaseback

Moderate

20–30

P21.1

Lessee Entries.

Simple

20–25

P21.2

Lessee Entries and Statement of Financial Position

Presentation.

Simple

20–30

P21.3

Lessee Entries and Statement of Financial Position

Finance Lease.

Moderate

35–45

P21.4

Lessee Entries, Lease with Monthly Payments.

P21.5

Basic Lessee Accounting with Difficult PV Calculation

P21.6

Lessee-Lessor Entries, Finance Lease with a

Guaranteed Residual Value.

P21.7

Lessor Computations and Entries, Sales-Type Lease

with Guaranteed Residual Value.

P21.8

Lessee Computations and Entries, Lease with

Guaranteed Residual Value.

Complex

30–40

P21.9

Lessor Computations and Entries, Sales-Type Lease

with Unguaranteed Residual Value.

Complex

30–40

P21.10

Lessee Computations and Entries, Finance Lease with

Unguaranteed Residual Value.

Complex

30–40

P21.11

Lessee-Lessor Accounting for Residual Values.

30–40

P21.12

Lessee-Lessor Entries, Statement of Financial Position

Presentation, Finance and Sales-Type Lease.

35–45

P21.13

Statement of Financial Position and Income Statement

35–45

P21.14

Operating lease.

Moderate

30–40

P21.15

Lessee-Lessor Entries, Operating Lease with an

Unguaranteed Residual Value.

Moderate

30–40

CA21.1

Lessee accounting and reporting.

Moderate

15–25

CA21.2

Lessor and lessee accounting and disclosure.

Moderate

25–35

CA21.3

Lessee accounting.

Moderate

20–30

CA21.4

Lease capitalization, bargain-purchase option.

Moderate

20–25

CA21.5

Short-Term lease vs. finance lease.

Moderate

20–30

Sale-Leaseback.

Moderate

15–25

ANSWERS TO QUESTIONS

1. The major lessor groups in the United States are banks, captives, and independents. Banks are the

largest players in the leasing business. Captives are subsidiaries whose primary business is to perform

leasing operations for the parent company. They have the point of sale advantage in finding leasing

2. (a) Possible advantages of leasing for the lessee:

1. Leasing may be more flexible in that the lease agreement may contain less restrictive

provisions than the bond indenture.

Assuming that funds are readily available through debt financing, there may not be great advantages (in

addition to the above-mentioned) to signing a noncancelable, long-term lease. One additional advantage

of leasing is its availability when other debt financing is unavailable.

(b) Given the new reporting standard on leasing the financial statement effects of a long-term

noncancelable lease versus the purchase of the asset are somewhat similar. That is assets under a

3. Possible advantages of leasing for a lessor:

1. It often provides profitable interest margins.

2. It can stimulate sales of a lessor’s product whether it be from a dealer (lessor) or a

4. The discount rate used by the lessee in the present value test and for valuing the lease liability is the

implicit interest rate used by the lessor. This rate is defined as the discount rate that, at the

commencement of the lease, causes the aggregate present value of the lease payments and

Questions Chapter 21 (Continued)

5. Paul Singer is for the most part correct. As long as the lease has a lease term of over 12 months and the

lease is not low value, Paul is correct that the lease must be recognized on the statement of financial

6. (a) Residual value is the expected value of the leased asset at the end of the lease term.

(b) A guaranteed residual value is a guarantee made to a lessor that the value of the leased asset

7. A bargain purchase option is a lease purchase option in which the lessee can buy the asset for a price

that is significantly lower than the underlying asset’s expected fair value at the date the option becomes

exercisable, thus making the exercise of the option reasonably certain. A bargain renewal option is

essentially the same conceptually as a bargain purchase option, except the option is to renew the lease

8. The lease liability is recorded at the present value of the lease payments. This includes the periodic

rental payments made by the lessee, bargain-purchase option if any, and amounts probable to be owed

9. Wonda Stone is correct in her interpretation. For purposes of lease classification by the lessor the

present value of the guaranteed residual value is used in determining whether the present value (90%)

Questions Chapter 21 (Continued)

10. The right–of-use asset is initially measured as the same amount as the lease liability (i.e. present value of

lease payments), adjusted for initial direct costs, prepayments and lease incentives. Initial direct costs

11. Variable lease payments should be included at the level of the index/rate at the commencement date.

Increases or decreases in the index should not be assumed when valuing the lease liability. Thus, for the

12. The lessee records a right-of-use asset and lease liability at commencement of the lease. The lessee

then recognizes interest expense on the lease liability over the life of the lease using the effective

interest method and records depreciation expense on the right-of-use asset generally on a straight-line

13. A low value lease is a lease of an underlying asset with a value of $5,000 or less. Rather than recording

a right-of-use asset and lease liability, a lessee may elect to expense the lease payments as incurred.

LO: 2, Bloom: AP, Difficulty: Simple, Time: 3-5, AACSB: Reflective Thinking, AICPA BB: None, AICPA FC: Reporting, AICPA PC: None

14. A short-term lease is a lease that, at the commencement date, has a lease term of 12 months or less.

15. If a bargain-purchase option exists, the lessee must increase the present value of the lease payments by

the present value of the option price. This is the case for both classification and initial measurement of

16. From the standpoint of the lessor, leases will (with few exceptions) be classified for accounting purposes as

either (a) operating leases or (b) finance (sales-type) leases.

A finance (sales-type) lease meets one or more of the following five tests:

Questions Chapter 21 (Continued)

3. The lease term is a major part of the remaining economic life of the underlying asset (i.e. equal to

75% or more of the estimated economic life of the property),

If none of the above five tests are met, the lease will be treated as an operating lease. The IASB

concluded that by meeting any one of the lease classification tests, the lessor transfers control of the

leased asset and therefore satisfies a performance obligation, which is required for revenue recognition

17. (a) If a lease is for a major part of the economic life of the lease, the lease is classified as a finance

lease. In practice, 75% of the economic life of the asset is generally used to meet this classification test.

That is, if the lease term is 75% or greater of the economic life of the asset, the lease is classified as a

finance lease.

18. A lease receivable is defined as the present value of the periodic rental payments plus any guaranteed

residual value. A net investment in the lease includes not only the components of the lease receivable but

19. Under the operating method, each rental receipt of the lessor is recorded as lease revenue. The

underlying leased asset is still recognized on the statement of financial position of the lessor and

depreciated in the normal manner. In addition to depreciation, any other related costs to the lease

arrangement (i.e. insurance, maintenance, taxes, etc.) are recorded in the period incurred.

LO: 3, Bloom: K, Difficulty: Simple, Time: 3-5, AACSB: Reflective Thinking, AICPA BB: None, AICPA FC: Reporting, Measurement, AICPA PC: None

20. Under a finance (sales-type) lease, lessors report in the income statement Sales Revenue and Cost of

Goods Sold (and resultant gross profit) at commencement of the lease. During the lease term Interest

Questions Chapter 21 (Continued)

21. Walker Company can use the finance (sales-type) lease method if the lease meets one or more of the

following five tests:

(1) The lease transfers ownership of the property to the lessee,

(2) The lease contains a bargain-purchase option,

22. Metheny Group should recognize the present value of the lease payments (normal sales price) as sales

revenue, and the carrying amount (book value) of the asset as cost of goods sold. Thus, the gross profit

23. Although not part of the classification tests, the lessor must also determine whether the collectibility of

payments from the lessee is probable, as it has implications for the subsequent accounting of the lease.

24. (a) (1) The lessee’s accounting for a lease with an unguaranteed residual value is the same as the

accounting for a lease with no residual value. That is, unguaranteed residual values are not

included in the lessee’s lease payments, either for classification or measurement purposes.

(b) The value of the lease liability may be made up of two components—the periodic rental payments

and amounts probable to be owed under a guaranteed residual value. That is, if the expected

residual value at the end of the lease term is less than the guaranteed residual value, then the

25. The amount to be recovered by the lessor is the same whether the residual value is guaranteed or

unguaranteed. Therefore, the amount of the periodic rental payments is set the same way by the lessor

Questions Chapter 21 (Continued)

26. Initial direct costs are the incremental costs of a lease that would not have been incurred had the lease not

been executed. For the lessee, some costs that are included in the right-of–use asset are commissions,

legal fees from the execution of the lease, lease documentation preparation costs incurred after the

27. Lessees and lessors must provide additional qualitative and quantitative disclosures to help financial

statement users to assess the amount, timing, and uncertainty of future cash flows. Qualitative lease

disclosures include the nature of the leases, how variable lease payments are determined, the existence

*28. In a sale-leaseback arrangement, a company (the seller-lessee) transfers an asset to another company

(the buyer-lessor) and then leases that asset back from the buyer-lessor. In order to qualify for sale-

leaseback treatment, the initial transfer of the asset must be such that the seller-lessee gives up control

*29. The sale and subsequent lease will receive sale-leaseback accounting treatment. The initial transfer of

the asset was a sale, and the seller-lessee gave control of the asset to the buyer-lessor. In addition, the

subsequent leaseback is classified as an operating lease, and thus Sanchez never takes control of the

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 21.1

The lease payments in the lease arrangement will include both the annual fixed

payments of $800,000 each year, plus the €11,000,000 bargain purchase option

BRIEF EXERCISE 21.2

The lease payments for years 1 and 2 will be $1,700 ($2,000 annual rental minus

BRIEF EXERCISE 21.3

Variable payments in a lease are not considered in determining the initial value

of the lease liability and right–of–use asset. Because the lease payments are

based on 4% of net sales, these payments are considered variable, as they are

BRIEF EXERCISE 21.4

12/31/18

Right-of–Use Asset ($41,933 X 3.57710*) …………………. 150,000**

Lease Liability ……………………………………………….. 150,000

Cash ……………………………………………………………… 41,933

BRIEF EXERCISE 21.4 (Continued)

*Present value of an annuity-due of 1 for 4 periods at 8%.

**Rounded by $1.

12/31/19

Interest Expense [($150,000 – $41,933) X 8%] ………….. 8,645

BRIEF EXERCISE 21.5

12/31/19

Interest Expense [(€300,000 – €48,337) X 8%] ………….. 20,133

BRIEF EXERCISE 21.6

1/1/19

Right-of–Use Asset ………………………………………………… 33,975*

Lease Liability ……………………………………………….. 33,975

BRIEF EXERCISE 21.6 (Continued)

12/31/19

Interest Expense [(£33,975 – £5,300) X 8%] …………….. 2,294

Lease Liability ……………………………………………….. 2,294

BRIEF EXERCISE 21.7

Fair value of leased asset £70,000

Less: Present value of guaranteed residual value

BRIEF EXERCISE 21.8

Fair value of leased asset $47,000

Less: Present value of lessor’s expected residual value*

($30,000 X .79209**) 23,763

BRIEF EXERCISE 21.9

Lease Receivable (4.99271* X £30,044) …………………… 150,001

Cost of Goods Sold ………………………………………………. 120,000

Sales Revenue ……………………………………………….. 150,001

BRIEF EXERCISE 21.10

Cash …………………………………………………………………….. 30,044

BRIEF EXERCISE 21.11

Lease Receivable (€40,800 X 4.31213*) …………………… 175,935

Cost of Goods Sold ………………………………………………. 120,000

Sales Revenue ……………………………………………….. 175,935

BRIEF EXERCISE 21.12

Cash …………………………………………………………………….. 40,800

Deposit Liability* ……………………………………………. 40,800

BRIEF EXERCISE 21.13

Lease Receivable ………………………………………………….. 57

Interest Revenue ……………………………………………. 57

Inventory………………………………………………………………. 1,000

Lease Receivable …………………………………………… 1,000

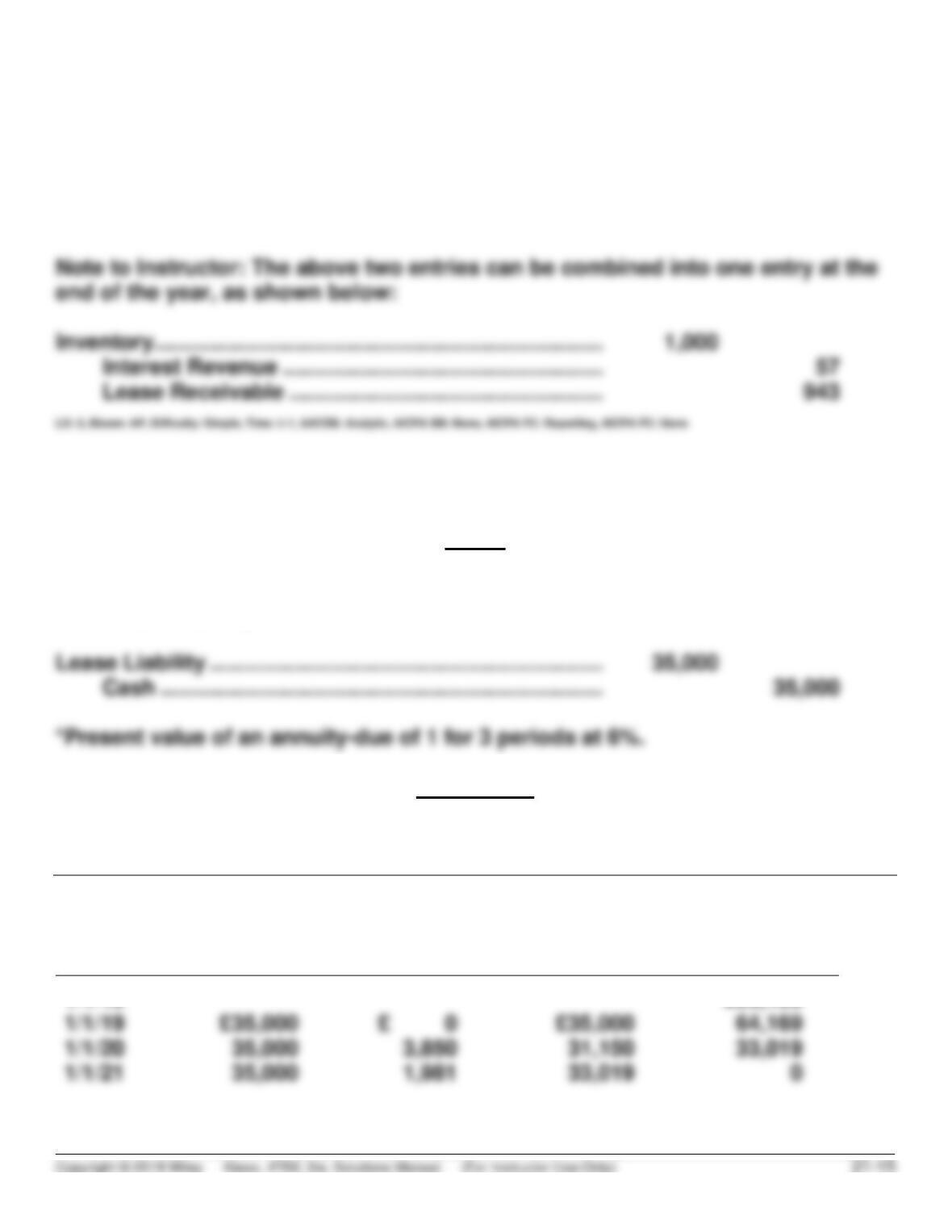

BRIEF EXERCISE 21.14

1/1/19

Right-of–Use Asset (2.83339* X £35,000) …………………. 99,169

Lease Liability ……………………………………………….. 99,169

Schedule A

KINGSTON PLC

Lease Amortization Schedule

Annuity-Due Basis

Date

Annual Payment

Interest (6%)

on Liability

Reduction

of Lease

Liability

Lease Liability

1/1/19

£99,169

BRIEF EXERCISE 21.14 (Continued)

12/31/19

Interest Expense …………………………..………………………. 3,850

Lease Liability ……………………………………………….. 3,850

BRIEF EXERCISE 21.15

1/1/19

Cash …………………………………………………………………….. 35,000

Unearned Lease Revenue ……………………………….. 35,000

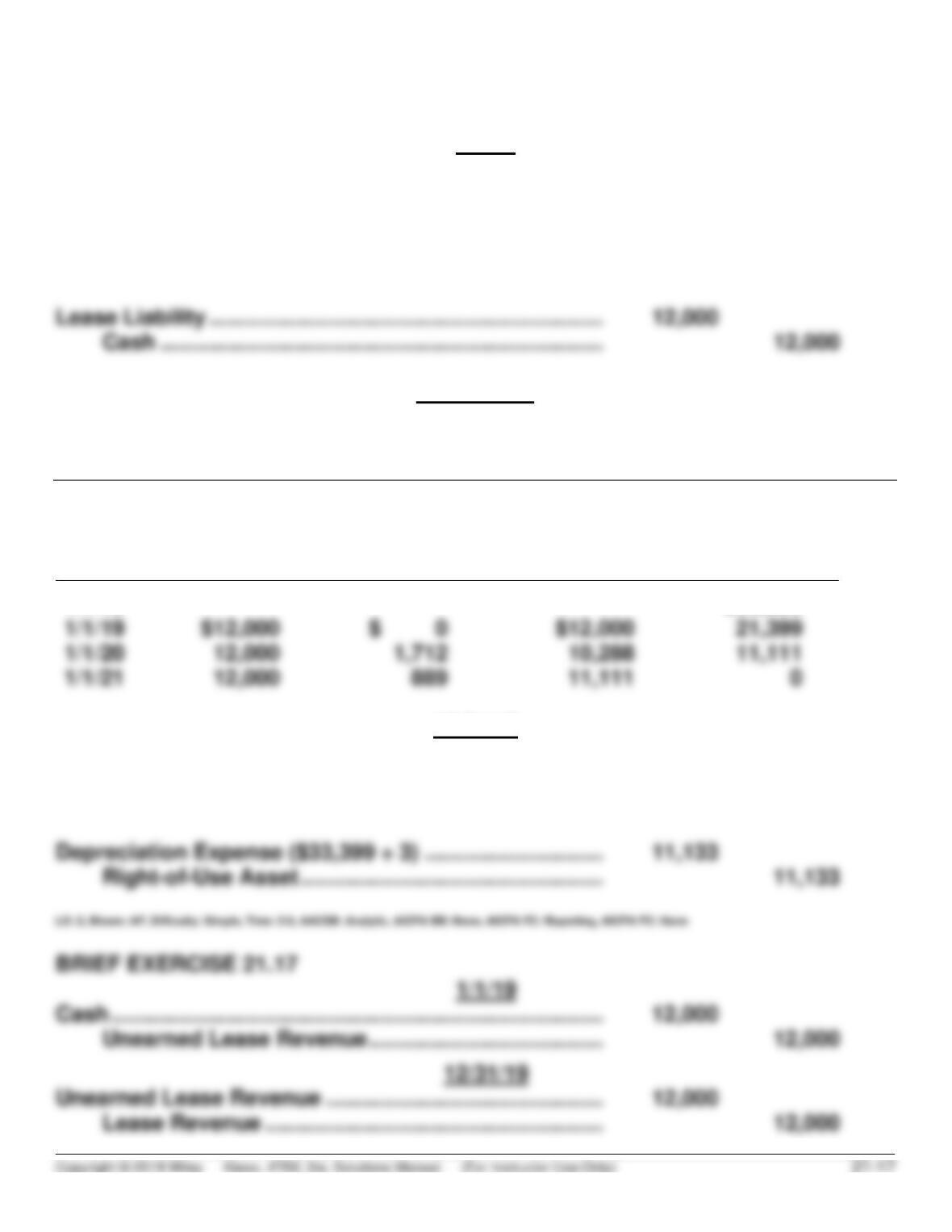

BRIEF EXERCISE 21.16

1/1/19

Right-of–Use Asset (2.78326* X $12,000) …………………. 33,399

Lease Liability ……………………………………………….. 33,399

*Present value of an annuity-due of 1 for 3 periods at 8%.

Schedule A

RODGERS CORPORATION

Lease Amortization Schedule

Annuity-Due Basis

Date

Annual

Payment

Interest (8%) on

Liability

Reduction

of Lease

Liability

Lease Liability

1/1/19

$33,399

12/31/19

Interest Expense …………………………..………………………. 1,712

Lease Liability ……………………………………………….. 1,712

BRIEF EXERCISE 21.17 (Continued)

Depreciation Expense …………………………………………… 6,000

Accumulated Depreciation–

Leased Equipment [$60,000 ÷ 10] ……………………. 6,000

LO: 3, Bloom: AP, Difficulty: Simple, Time: 3-5, AACSB: Analytic, AICPA BB: None, AICPA FC: Reporting, AICPA PC: None

BRIEF EXERCISE 21.18

BRIEF EXERCISE 21.19

(a) The value of the lease liability would remain the same if the only fact changed

(b) Following from the above reasoning, if the expected residual value drops to

£5,000 and Escapee guarantees a residual of £9,000, Escapee will need to

account for the difference between the expected and guaranteed residual

value in calculating the initial lease liability as follows:

BRIEF EXERCISE 21.19 (Continued)

Note to Instructor: The measurement of the lease liability/right-of-use asset

BRIEF EXERCISE 21.20

12/31/2018

Right-of–Use Asset ………………………………………………… 215,544*

Lease Liability ……………………………………………….. 215,544

*Present value of an annuity-due of 1 for 6 periods at 6%.

**Present value of 1 for 6 periods at 6%.

***The lessee need only include in the initial lease liability the amount of the

BRIEF EXERCISE 21.21

12/31/18

Lease Receivable ………………………………………………….. 222,593*

Cost of Goods Sold ………………………………………………. 180,000

BRIEF EXERCISE 21.21 (Continued)

Cash …………………………………………………………………….. 40,000

Lease Receivable …………………………………………… 40,000

12/31/19

Cash …………………………………………………………………….. 40,000

BRIEF EXERCISE 21.22

Lease Liability

In calculating the lease liability, Forrest must determine which of the executory

costs are considered a component of the lease (to be considered in the

measurement of the lease liability).

• The real estate taxes in this case are variable payments and therefore are not

PV of rental payments (4.31213* X $4,638): $20,000

Right-of–Use Asset

The right-of–use asset is initially measured the same as the lease liability, though it

is also adjusted for any initial direct costs, prepaid rent, and lease incentives