PROBLEM 23.3

MORTONSON PLC

Statement of Cash Flows

For the Year Ended December 31, 2019

(£ in thousands)

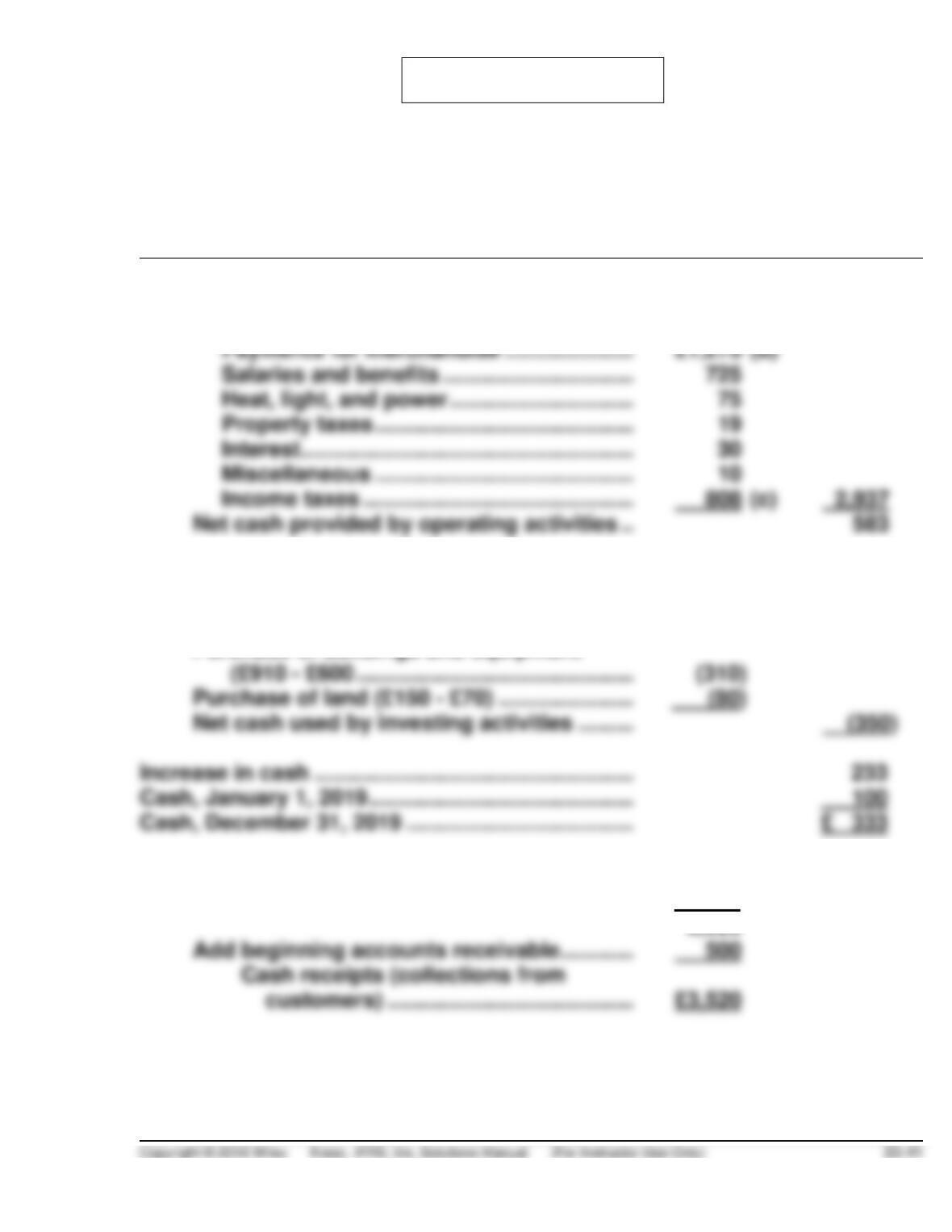

Cash flows from operating activities

Cash receipts from customers ………………..

£3,520 (a)

Cash payments:

Payments for merchandise …………………

£1,270

(b)

Heat, light, and power …………………………

Property taxes ……………………………………

Interest ………………………………………………

Miscellaneous ……………………………………

Income taxes ……………………………………..

808

(c)

Net cash provided by operating activities ..

Cash flows from investing activities

Sale of non-trading equity investments

(£10 – £50) …………………………………………

40

Purchase of land (£150 – £70) ………………….

Net cash used by investing activities ………

Increase in cash …………………………………………….

Cash, January 1, 2019 …………………………………….

Purchase of buildings and equipment

(a) Sales revenue ………………………………………..

£3,800

Deduct ending accounts receivable …………

780

3,020

Add beginning accounts receivable …………

500

Cash receipts (collections from

PROBLEM 23.3 (Continued)

(b) Cost of goods sold …………………………..…….

£1,200

Add ending inventory …………………………....

720

Goods available for sale ………………….

Deduct beginning inventory ……………………

560

Purchases ………………………………………

Deduct ending accounts payable…………….

420

Add beginning accounts payable ……………

330

Cash purchases (payments for

(c) Income taxes …………………………………………

£818

Deduct ending income taxes payable ………

40

Add beginning income taxes payable ……..

30

PROBLEM 23.4

MICHAELS LTD

Statement of Cash Flows

For the Year Ended December 31, 2019

(Direct Method)

Cash flows from operating activities

Cash receipts:

Cash received from customers …………………….

£1,152,450a

Dividends received ………………………………………

2,400

£1,154,850

Cash payments:

Cash paid to suppliers …………………………………

Cash paid for operating expenses ………………..

Taxes paid …………………………………………………..

Interest paid ………………………………………………..

Net cash provided by operating activities ……………..

Cash flows from investing activities

Sale of short-term investments

(£8,000 + £4,000) ………………………………………

12,000

Sale of land (£175,000 – £125,000) + £8,000 ……

58,000

Net cash used by investing activities ……………

Cash flows from financing activities

Proceeds from issuance of ordinary shares ……

Principal payment on long-term debt …………….

Dividends paid …………………………………………….

Net cash used by financing activities ……………

(6,800)

Net increase in cash ……………………………………………

6,000

Cash, January 1, 2019 …………………………………………

4,000

Cash, December 31, 2019 ……………………………………

£ 10,000

Increase in Accounts Receivable …………………………

(7,550)

Cash received from customers …………………………..

Increase in Inventory ……………………………………………

PROBLEM 23.4 (Continued)

cOperating Expenses……………………………………..

£276,400

Depreciation/Amortization Expense ……………….

Decrease in Prepaid Rent ………………………………

Increase in Prepaid Insurance ………………………..

Increase in Supplies ………………………………………

Increase in Salaries and Wages Payable …………

dIncome Tax Expense …………………………………….

£39,400

Increase in Income Taxes Payable ………………….

(1,000)

Taxes paid ……………………………………………..

£38,400

£51,750

Decrease in Bond Payable ……………………………..

PROBLEM 23.5

(a)

Net Cash Flow from Operating Activities

Cash received from customers ………………………..

€524,8501

Cash payments:

Cash payments to suppliers ………………………..

€375,7502

Cash payments for operating expenses ……….

**Increase in accrued payables

(b) MARCUS AG

Statement of Cash Flows

For the Year Ended December 31, 2019

Cash flows from operating activities

Net income ……………………………………………….

€42,500

Adjustments to reconcile net income

to net cash provided by operating

activities:

Depreciation expense ………………………….

Gain on sale of investments ………………..

Loss on sale of machinery …………………..

Increase in accounts receivable (net) …..

Increase in inventory …………………………..

Increase in accounts payable ………………

Increase in accrued payables ………………

Net cash provided by operating activities …..

PROBLEM 23.5 (Continued)

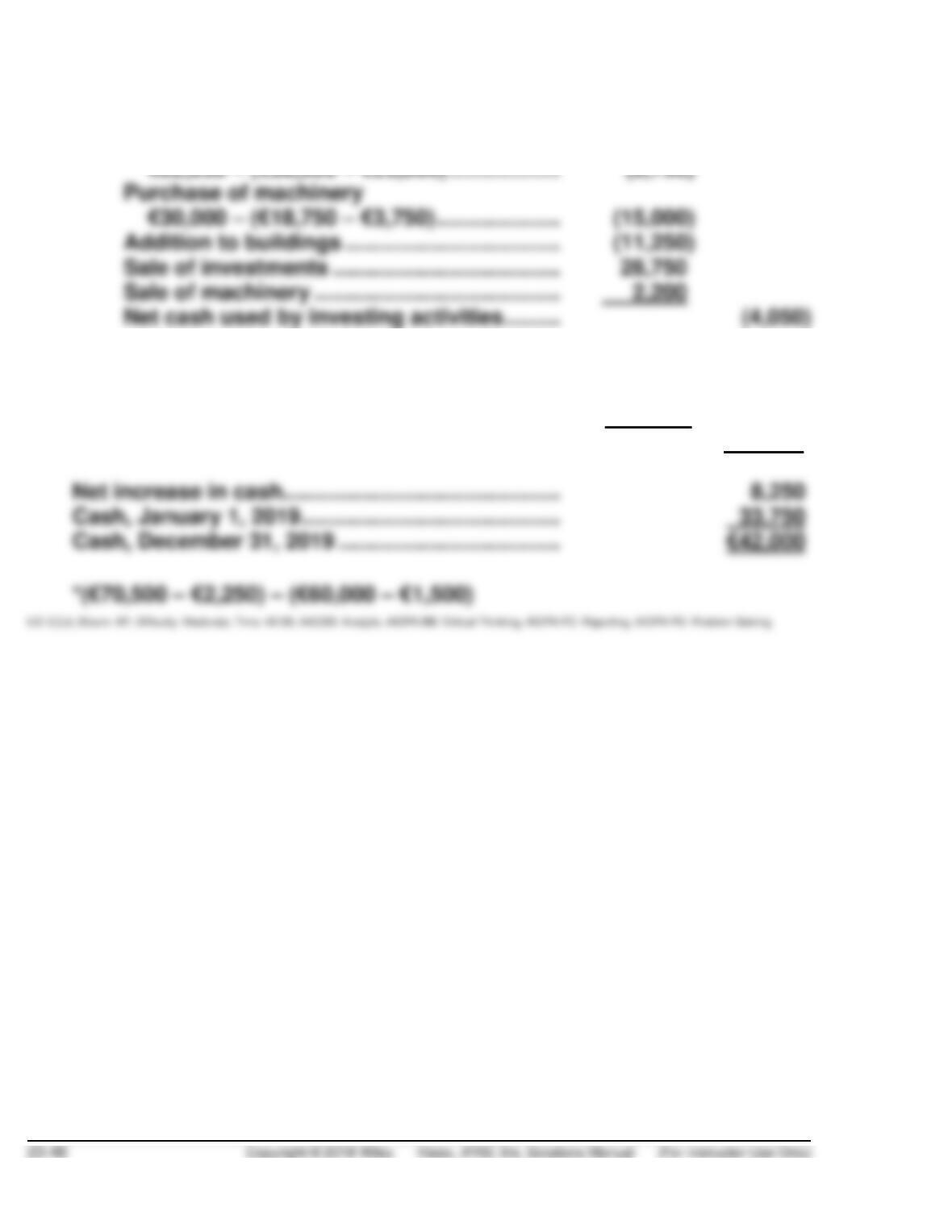

Cash flows from investing activities

Addition to buildings ……………………………..

Sale of investments …………………………..…..

Sale of machinery ………………………………….

Net cash used by investing activities ………

Purchase of equity investments

Cash flows from financing activities

Reduction in long-term notes payable …….

(10,000)

Cash dividends paid …………………………..….

(21,125)

Net cash used by financing activities ………

(31,125)

Net increase in cash………………………………………

Cash, January 1, 2019 ……………………………………

PROBLEM 23.6

(a) Both the direct method and the indirect method for reporting cash

flows from operating activities are acceptable in preparing a statement

of cash flows according to IFRS; however, the IASB encourages the

use of the direct method. Under the direct method, the statement of

(b) The Statement of Cash Flows for Chapman Company, for the year ended

May 31, 2019, using the direct method, is presented below.

CHAPMAN COMPANY

Statement of Cash Flows

For the Year Ended May 31, 2019

Cash flows from operating activities

Cash received from customers ………………….

$1,238,250

Cash payments:

To suppliers ……………………………………..

$684,000

To employees …………………………………..

For other expenses …………………………..

For interest ……………………………………….

For income taxes ………………………………

43,000

Net cash provided by operating activities …..

Cash flows from investing activities

Purchase of plant assets…………………………...

Cash flows from financing activities

Cash received from ordinary shares issue ….

$ 20,000

Cash paid

For dividends ……………………………………

(105,000)

To retire bonds payable …………………….

Net cash used by financing activities …………

Net increase in cash ………………………………………….

Cash, June 1, 2018 ……………………………………………

20,000

PROBLEM 23.6 (Continued)

Note 1: Non-cash investing and financing activities:

Issuance of ordinary shares for plant assets $70,000.

Supporting Calculations:

Collections from customers

Sales ……………………………………………………….

$1,255,250

Less: Increase in accounts receivable ………

17,000

Cash collected from customers ……….

$1,238,250

Cash paid to suppliers …………………………………….

Less: Decrease in inventory ……………………..

Increase in accounts payable ………….

8,000

Cash paid to suppliers …………………….

$ 684,000

Cash paid to employees

Salary expense …………………………………………

$ 252,100

Add: Decrease in salaries and wages

payable…………………………………………

24,750

Cash paid to employees …………………..

$ 276,850

Cash paid for other expenses

Other expenses ………………………………………..

$ 8,150

Add: Increase in prepaid expenses …………..

2,000

Cash paid for other expenses …………..

$ 10,150

Cash paid for interest

Interest expense ……………………………………….

$ 75,000

Less: Increase in interest payable …………….

2,000

Cash paid for interest ……………………..

$ 73,000

Cash paid for income taxes:

Income tax expense (given)……………………….

PROBLEM 23.6 (Continued)

(c) The calculation of the cash flow from operating activities for Chapman

Company, for the year ended May 31, 2019, using the indirect method,

is presented below.

CHAPMAN COMPANY

Statement of Cash Flows

For the Year Ended May 31, 2019

Cash flows from operating activities

Net income ………………………………………………..

$130,000

Adjustments to reconcile net income to net

cash provided by operating activities:

Depreciation expense ………………………..

Decrease in merchandise inventory…….

Increase in accounts payable ……………..

Increase in interest payable ………………..

Increase in accounts receivable ………….

Increase in prepaid expenses ……………..

PROBLEM 23.7

(a) Net Cash Provided by Operating Activities

Cash receipts from customers

HK$925,000 (1)

Cash payments:

Cash payments to suppliers

Cash payments for operating expenses

Cash payments for income taxes

Net cash provided by operating activities

(1) (Sales Revenue) less (Increase in Accounts Receivables)

HK$950,000 – HK$25,000 = HK$925,000

(2) (Cost of Goods Sold) plus (Increase in Inventory) less

(Increase in Accounts Payable)

HK$600,000 + HK$14,000 – HK$6,000 = HK$608,000

(3) (Operating Expenses) less (Depreciation Expense) less

(Bad Debt Expense)

HK$45,000 – HK$2,000 = HK$43,000

PROBLEM 23.7 (Continued)

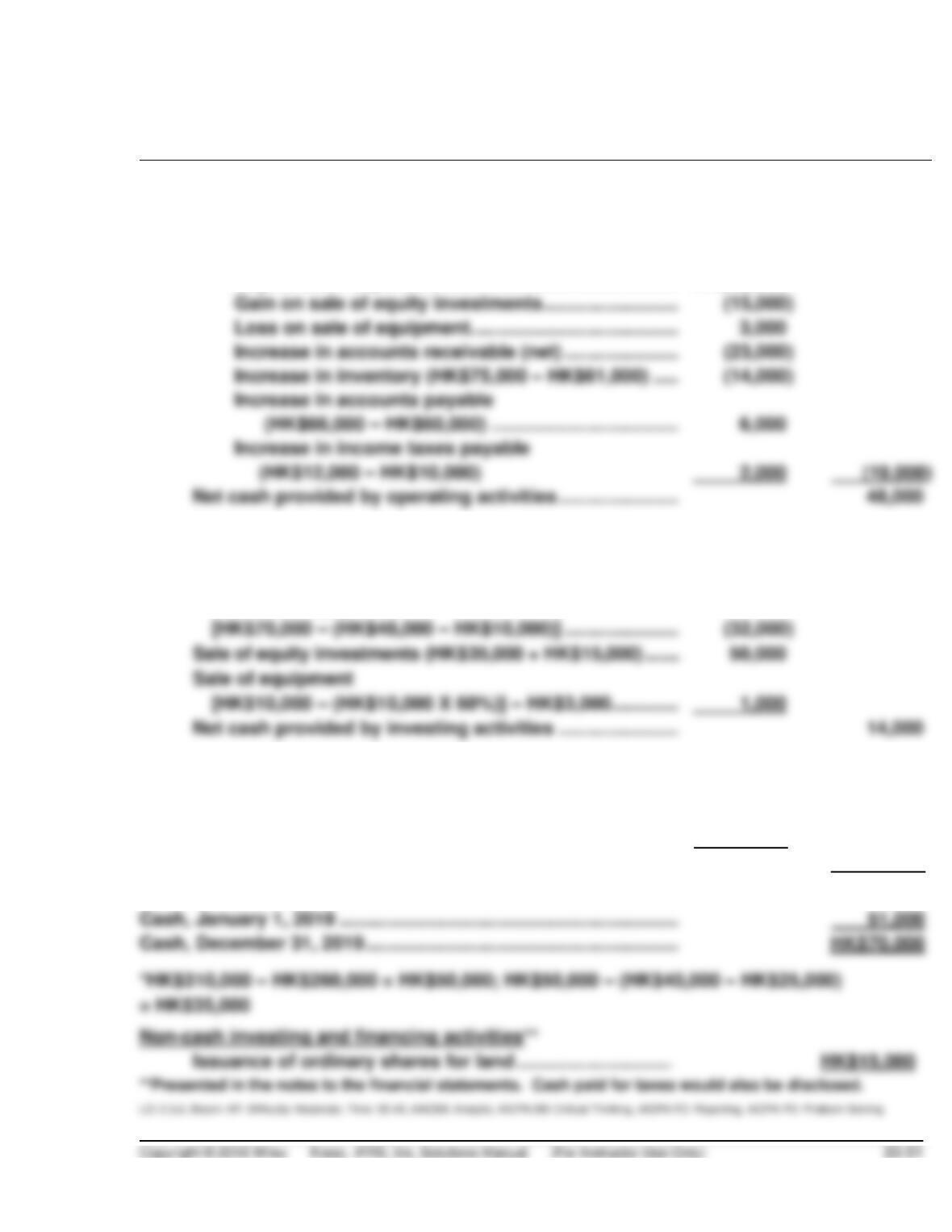

(b) SHI GROUP

Statement of Cash Flows

For the Year Ended December 31, 2019

Cash flows from operating activities

Net income ………………………………………………………………..

HK$67,000

Adjustments to reconcile net income

to net cash provided by operating activities:

Depreciation expense ………………………………………….

HK$22,000

Gain on sale of equity investments ………………………

Loss on sale of equipment …………………………………..

Increase in accounts receivable (net) …………………..

Increase in inventory (HK$75,000 – HK$61,000) ……

(HK$12,000 – HK$10,000)

Net cash provided by operating activities ……………………

Cash flows from investing activities

Purchase of equity investments

[HK$55,000 – (HK$85,000 – HK$35,000)] …………………..

(5,000)

Sale of equity investments (HK$35,000 + HK$15,000) ……..

Sale of equipment

Net cash provided by investing activities ……………………

Purchase of equipment

Cash flows from financing activities

Payment of LT notes payable (HK$62,000 –HK$70,000)

(8,000)

Cash dividends paid [(HK$95,000 + HK$67,000) –HK$92,000]

(70,000)

Issuance of ordinary shares ……………………………………….

35,000*

Net cash used by financing activities ………………………….

(43,000)

Net increase in cash ……………………………………………………….…..

19,000

Cash, January 1, 2019 …………………………………………………………

51,000

Non-cash investing and financing activities**

PROBLEM 23.8

(a) GRECO CORPORATION

Statement of Cash Flows

For the Year Ended December 31, 2019

Cash flows from operating activities

Net income …………………………………………………. $15,750(a)

Adjustments to reconcile net income to net

cash provided by operating activities:

Loss on sale of equipment ……………………. $ 5,200(b)

Cash flows from investing activities

Sale of equity investments ………………………….. 4,500

Sale of equipment ………………………………………. 2,500

Purchase of equipment (cash) …………………….. (15,000)

Increase in cash ……………………………………………… 25,500

Cash, January 1, 2019 …………………………………….. 13,000

Supplemental disclosures of cash flow information:

Cash paid during the year for:

Interest …………………………………… $2,000

Income taxes …………………………... $5,000

PROBLEM 23.8 (Continued)

Non-cash investing and financing activities:**

Retired notes payable by issuing ordinary shares ….. $ 5,000

Supporting Computations:

(a) Ending retained earnings ……………………………………… $20,750

Beginning retained earnings …………………………………. (5,000)

Net income ……………………………………………………. $15,750

(b) (1) For a severely financially troubled firm:

Operating: Probably a small cash inflow or a cash outflow.

(2) For a recently formed firm which is experiencing rapid growth:

Operating: Probably a cash inflow.

LO: 2,4, Bloom: AP, Difficulty: Moderate, Time: 30–40, AACSB: Analytic, AICPA BB: Critical Thinking, AICPA FC: Reporting, AICPA PC: Problem Solving

TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS

CA 23.1 (Time 30–35 minutes)

CA 23.2 (Time 30–35 minutes)

CA 23.3 (Time 30–35 minutes)

Purpose—to help a student identify whether a transaction creates a cash inflow or a cash outflow. The

CA 23.4 (Time 20–30 minutes)

Purpose—to help the student identify the sections of the statement of cash flows. The student is

CA 23.5 (Time 30–40 minutes)

Purpose—to identify and explain reasons and purposes for preparing a statement of cash flows, to

CA 23.6 (Time 20–30 minutes)

Purpose—provides the student the opportunity to examine the effects of a securitization on the statement

SOLUTIONS TO CONCEPTS FOR ANALYSIS

CA 23.1

(a) The main purpose of the statement of cash flows is to provide information about cash receipts and

(b) The following are weaknesses in form and format of Maloney Corporation’s Statement of Sources

and Uses of Cash:

1. The title of the statement should be Statement of Cash Flows.

the employee share option plans, and for changes in current assets and liabilities.

3. The format used should separate the cash flows into investing, financing, and operating

activities. Non-cash investing and financing activities, if significant, should be shown in a note to

the financial statements.

4. Individual items should not be grouped together, as was the case for the $14,000 item.

(c) 1. (i) The $25,000 share-option plan wage and salary expense should be included in the

2. The expenditures for plant asset acquisitions should not be reported net of the proceeds from

3. Share dividends or share splits need not be disclosed in the statement because these

transactions do not significantly affect financial position.

4. The issuance of the 16,000 ordinary shares in exchange for the preference shares should be

5. The presentation of the combined total of depreciation and depletion is probably acceptable.

The general rule is that related items should be shown separately in proximity when the result