EXERCISE 11.6 (Continued)

2nd full year [25% X ($304,000 – $76,000)] = $57,000

EXERCISE 11.7 (25–35 minutes)

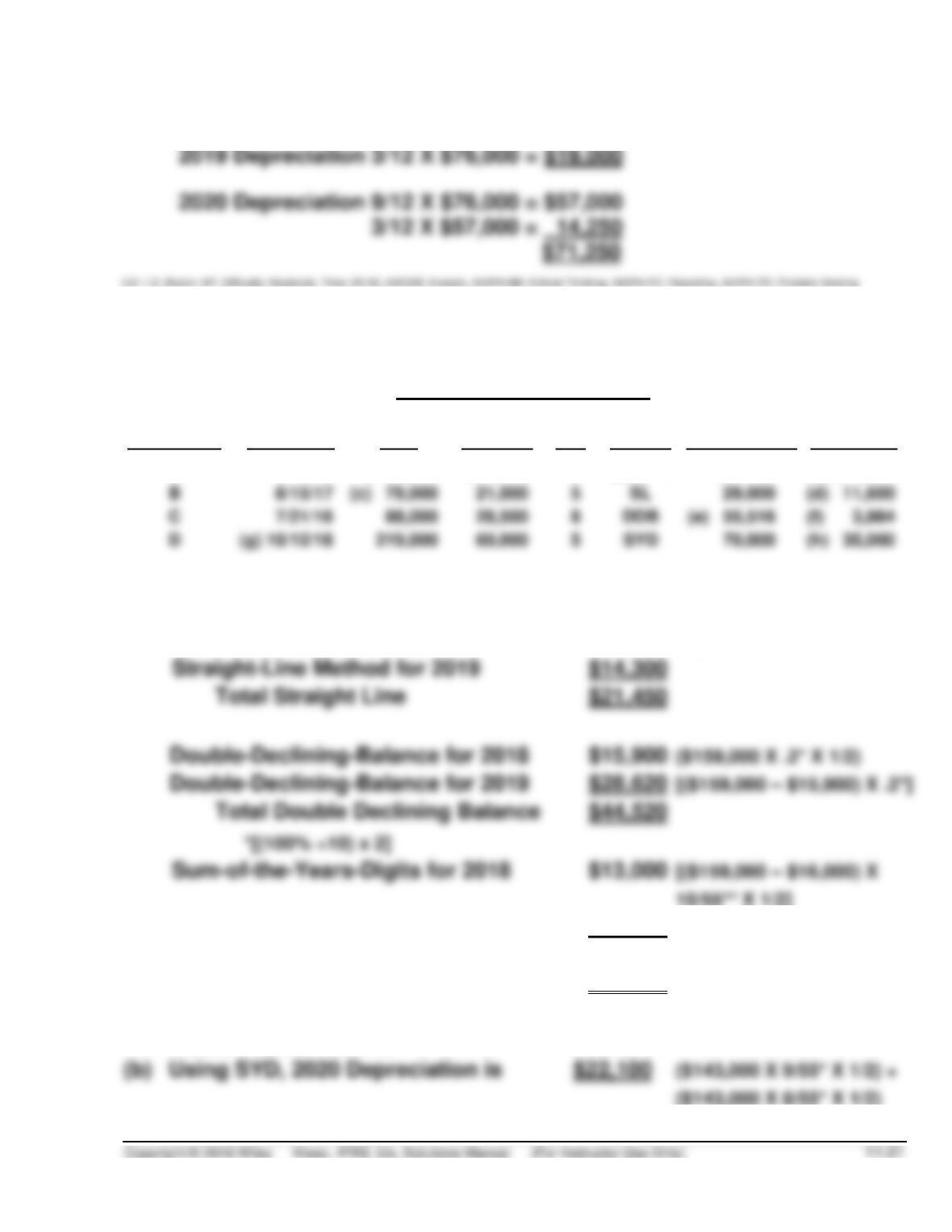

Methods of Depreciation

Description

Date

Purchased

Cost

Residual

Life

Method

Accum. Depr.

to 2019

2020 Depr.

A

2/12/18

$159,000

$16,000

10

(a) SYD

$37,700

(b) $22,100

B

8/15/17

29,000

(d) 11,600

C

7/21/16

(e) 55,516

(f) 3,984

D

(g) 10/12/18

70,000

(h) 35,000

Machine A—Testing the methods

(a) Straight-Line Method for 2018

$ 7,150

[($159,000 – $16,000) ÷

10] X 1/2

Straight-Line Method for 2019

($159,000 X .2* X 1/2)

10/55** X 1/2]

Sum-of-the-Years-Digits for 2019

$24,700

($143,000 X 10/55** X 1/2) +

($143,000 X 9/55** X 1/2)

Total Sum-of-the-Years-Digits

$37,700

**[10 x (10 + 1)] ÷ 2

Method used must be

SYD

($143,000 X 9/55* X 1/2) +

EXERCISE 11.7 (Continued)

Machine B—Computation of the cost

(c) Asset has been depreciated for 2 1/2 years using the straight-line

method.

(e) 2016’s depreciation is

$11,000

($88,000 X .25* X .5)

2017’s depreciation is

$19,250

($88,000 – $11,000) X .25*

2018’s depreciation is

$14,438

($88,000 – $30,250) X .25*

2019’s depreciation is

$10,828

($88,000 – $44,688) X .25*

(f) Using DDB, 2020 Depreciation is limited to $3,984, which results in the

carrying value of the machine equal to the residual value.

($88,000 – $28,500 – $55,516)

Machine D—Computation of Year Purchased

(g) First Half Year using SYD =

$25,000

$45,000

($150,000 X 5/15** X .5) +

(h) Using SYD, 2020 Depreciation is

[($219,000 – $69,000) X

EXERCISE 11.8 (20–25 minutes)

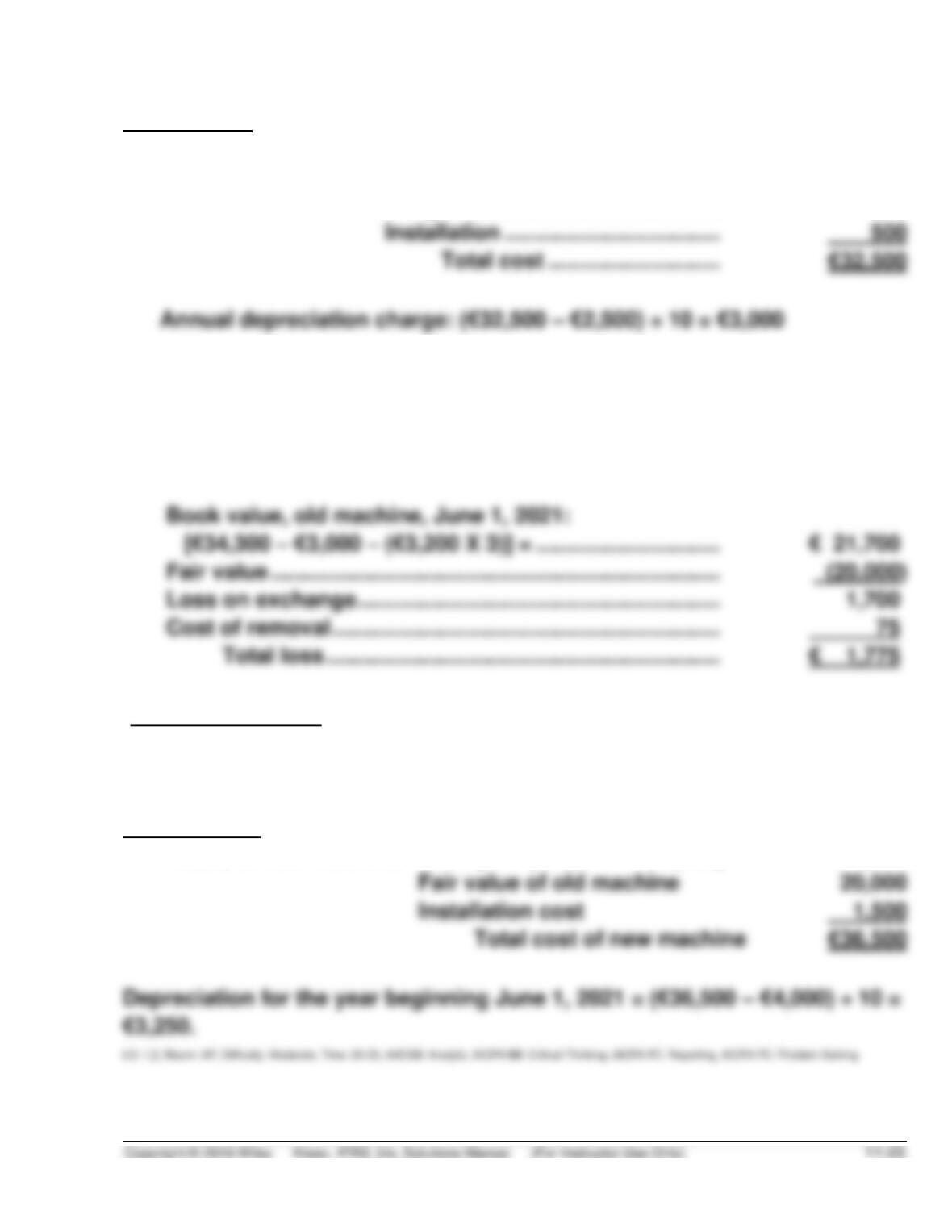

Old Machine

June 1, 2017

Purchase ………………………………..

€31,800

Freight ……………………………………

200

Installation ……………………………..

On June 1, 2018, debit the old machine for €2,700 and reduce the book

value by €900; the revised total cost is €34,300 (€32,500 + €2,700 – €900);

thus the revised annual depreciation charge is: (€34,300 – €2,500 –

€3,000) ÷ 9 = €3,200.

Book value, old machine, June 1, 2021:

[€34,300 – €3,000 – (€3,200 X 3)] = …………………………

Fair value ……………………………………………………………….

Loss on exchange …………………………………………………..

Cost of removal ………………………………………………………

(Note to instructor: The above computation is done to determine whether

there is a gain or loss from the exchange of the old machine with the new

machine and to show how the cost of removal might be reported.

New Machine

Basis of new machine

Cash paid (€35,000 – €20,000)

€15,000

Fair value of old machine

Installation cost

EXERCISE 11.9 (15–20 minutes)

(a)

Component

Cost

Estimated

Residual

Depreciable

Cost

Estimated

Life

Depreciation

per Year

A

¥ 40,500

¥ 5,500

¥ 35,000

10

¥ 3,500

B

33,600

4,800

28,800

9

3,200

C

36,000

3,600

32,400

8

4,050

D

19,000

1,500

17,500

7

2,500

E

2,500

21,000

6

3,500

Depreciation Expense ……………………………………………..

16,750

Accumulated Depreciation—Equipment …………..

(b)

Equipment ……………………………………………………….

40,000

Accumulated Depreciation—Equipment …………………..

19,200*

Loss on Disposal of Equipment …………………………..

Equipment ……………………………………………………..

Cash …………………………..…………………………..

EXERCISE 11.10 (10–15 minutes)

Sum-of-the–years’-digits =

8 X (8 + 1)

= 36

2

EXERCISE 11.11 (10–15 minutes)

(a) No correcting entry is necessary because changes in estimate are

handled in the current and prospective periods.

(b) Revised annual charge

Book value as of 1/1/2020 [$52,000 – (*$6,000 X 5)] = $22,000

Accumulated Depreciation—Equipment ……………

EXERCISE 11.12 (20–25 minutes)

(a) 1993–2002—(€1,900,000 – €60,000) ÷ 40 = €46,000/yr.

(d) Revised annual depreciation

Building

Book value: (€1,900,000 – €1,288,000*) …………..

€612,000

Residual value ………………………………………………

Remaining useful life ……………………………………..

Annual depreciation ………………………………………

€ 17,250

EXERCISE 11.12 (Continued)

Addition

Book value: (€470,000 – €270,000**) ……………….

€200,000

Residual value ……………………………………………….

Remaining useful life ……………………………………..

Annual depreciation ……………………………………….

EXERCISE 11.13 (15–20 minutes)

(a) $2,400,000 ÷ 40 = $60,000

(b)

Loss on Disposal of Plant Assets …………………………..

90,000

Accumulated Depreciation—Buildings

($180,000 X 20/40) ………………………………………………..

90,000

Buildings ……………………………………………………….

Buildings ……………………………………………………….

Cash …………………………..…………………………..

Note: The most appropriate entry would be to remove the old roof and

record a loss on disposal, because the cost of the old roof is given.

Another alternative would be to debit Accumulated Depreciation on the

EXERCISE 11.13 (Continued)

(c) No entry necessary.

(d) (Assume the cost of the old roof is removed)

Building ($2,400,000 – $180,000 + $300,000) …………………….

$2,520,000

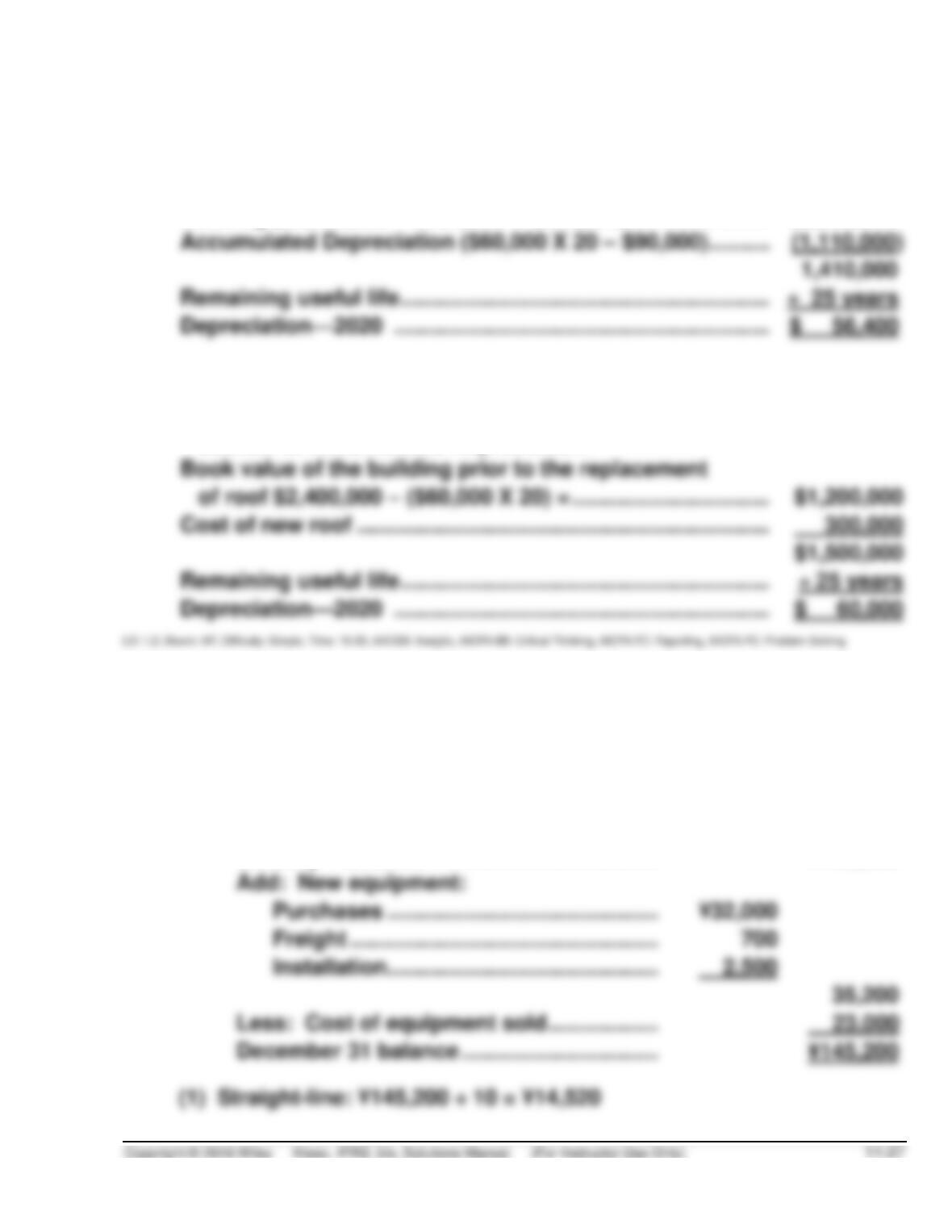

Accumulated Depreciation ($60,000 X 20 – $90,000) …………

Remaining useful life ……………………………………………………..

Note to Instructor:

If it is assumed that the cost of the new roof is

debited to Accumulated Depreciation:

Book value of the building prior to the replacement

of roof $2,400,000 – ($60,000 X 20) = …………………………..

Cost of new roof ……………………………………………………………

Remaining useful life ……………………………………………………..

EXERCISE 11.14 (20–25 minutes)

(a)

Maintenance and Repairs Expense …………………………..

500

Equipment ………………………………………………………

500

(b)

The proper ending balance in the asset account is:

January 1 balance ……………………………….

¥133,000

Add: New equipment:

Purchases ……………………………………..

Freight …………………………..………………

700

Installation ……………………………………..

Less: Cost of equipment sold ………………

23,000

EXERCISE 11.14 (Continued)

(2) Sum-of-the-years’-digits: 10 + 9 + 8 + 7 + 6 + 5 + 4 + 3 + 2 + 1 = 55

EXERCISE 11.15 (25–35 minutes)

(a)

2014

2015–2020

Incl.

2021

Total

(1)

$240,000 – $21,000 = $219,000

$219,000 ÷ 12 = $18,250

per yr. ($50 per day)

$ 3,400

(2)

0

109,500

18,250

127,750

(3)

18,250

109,500

0

127,750

(4)

9,125

109,500

9,125

127,750

(5)

4/12 of $18,250

6,083

109,500

3/12 of $18,250

4,563

120,146

(6)

109,500

0

109,500

(b) The most accurate distribution of cost is given by methods 1 and 5 if it

is assumed that straight-line depreciation is satisfactory. Reasonable

EXERCISE 11.16 (10–15 minutes)

(a) [(€6,000 + €10,000 + €34,000) – 0] ÷ 10 = €5,000

(b)

Component

Tires

Transmission

EXERCISE 11.17 (10–15 minutes)

(a)

Component

Depreciation Expense

Building structure

€4,200,000 ÷ 60 =

€ 70,000

Building engineering

Building external works

700,000 ÷ 30 =

(b) Building Engineering ……………………………….. 2,300,000

Accumulated Depreciation—Building

EXERCISE 11.18 (10–15 minutes)

(a)

December 31, 2019

Loss on Impairment ………………………………………………..

1,000,000

Accumulated Depreciation—Equipment …………..

1,000,000

Cost …………………………………………

€9,000,000

Accumulated depreciation ………..

Carrying amount ………………………

Recoverable amount*………………..

(b)

December 31, 2020

Depreciation Expense ……………………………………………..

1,750,000

Accumulated Depreciation—Equipment …………..

1,750,000

New carrying amount ………………..

€7,000,000

Useful life …………………………………

(c) Accumulated Depreciation—Equipment ……………. 750,000

EXERCISE 11.19 (15–20 minutes)

(a)

Loss on Impairment ………………………………………………..

3,600,000

Accumulated Depreciation—Equipment …………..

3,600,000

Cost …………………………………………

€9,000,000

Accumulated depreciation ………..

Carrying amount ………………………

Less: Recoverable amount ……….

EXERCISE 11.19 (Continued)

(b) No entry necessary. Depreciation is not taken on assets intended to be

sold.

(c)

Accumulated Depreciation—Equipment …….

680,000

Recovery of Loss on Impairment ………

680,000

Fair value …………………………………………………

Less: Cost of disposal……………………………..

Carrying amount ………………………………………

Recovery of impairment loss …………………….

EXERCISE 11.20 (15–20 minutes)

(a)

December 31, 2019

Loss on Impairment …………………………………………………

200,000

Accumulated Depreciation—Equipment ……………

200,000

(b) It should be reported in the other income and expense section in the

income statement.

(c) Accumulated Depreciation—Equipment …………….. 45,000

EXERCISE 11.20 (Continued)

(d) To determine whether an asset is impaired, on an annual basis,

companies review the asset for indicators of impairment—that is, a

decline in the asset’s cash-generating ability through use or sale. If

EXERCISE 11.21 (10–15 minutes)

Cost per barrel of oil:

Initial payment =

€600,000

=

€2.40

250,000

Rental =

Premium, 5% of €65 =

EXERCISE 11.22 (15–20 minutes)

Depletion base: €1,250,000 + €90,000 – €100,000 + €200,000 = €1,440,000

EXERCISE 11.23 (15–20 minutes)

(a)

$850,000 + $170,000 + $40,000* – $100,000

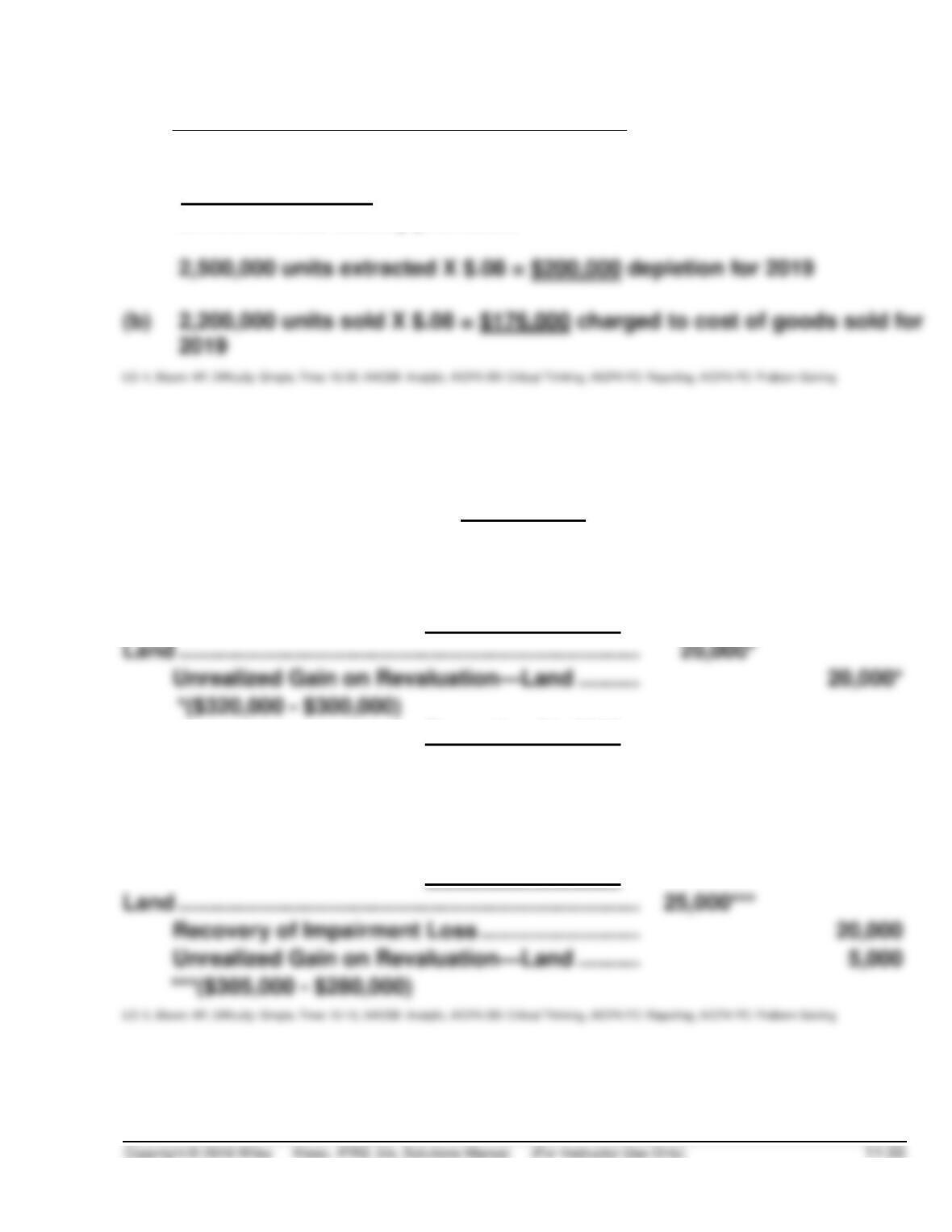

= $.08 depletion per unit

12,000,000

*Note to instructor: The $40,000 should be depleted because it is an

environmental liability provision.

EXERCISE 11.24 (10–15 minutes)

During 2019

Land ………………………………………………………………… 300,000

Cash …………………………………………………………. 300,000

December 31, 2019

December 31, 2020

Unrealized Gain on Revaluation—Land ……………… 20,000

Loss on Impairment ………………………………………….. 20,000

Land ……………………………………………………….… 40,000**

**($280,000 – $320,000)

December 31, 2021

EXERCISE 11.25 (10–15 minutes)

Value at

December 31

Other

Comprehensive

Income

Accumulated Other

Comprehensive

Income

Recognized in

Net Income

2017

¥50,000

¥50,000

—

2018

2019

2020

2021

EXERCISE 11.26 (15–20 minutes)

December 31, 2017

Land (¥450,000 – ¥400,000) ……………………………….. 50,000

Unrealized Gain on Revaluation—Land ………. 50,000

December 31, 2018

December 31, 2019

Land (¥385,000 – ¥360,000) ……………………………….. 25,000

Recovery of Impairment Loss ……………………. 25,000

EXERCISE 11.27 (10–15 minutes)

(a) January 1, 2018

Equipment…………………………………………………….. 12,000

Cash ……………………………………………………… 12,000

(b) December 31, 2019

Depreciation Expense ……………………………………. 2,000

Accumulated Depreciation—Equipment ….. 2,000

EXERCISE 11.28 (15–20 minutes)

(a) Asset turnover:

EXERCISE 11.28 (Continued)

(c) Profit margin on sales:

£676

= 6.56%

£10,301

*EXERCISE 11.29 (20–25 minutes)

(a) December 31, 2017

Depreciation Expense ……………………………………. 1,000

Accumulated Depreciation—Equipment …… 1,000

EXERCISE 11.29 (Continued)

December 31, 2019

Depreciation Expense (¥8,800 ÷ 8) ………………….. 1,100

Accumulated Depreciation—Equipment ….. 1,100

December 31, 2020

Depreciation Expense ……………………………………. 1,100

Accumulated Depreciation—Equipment ….. 1,100

(b) Su would probably not use revaluation accounting for assets whose fair

value is lower than their carrying value. When the fair value of property and

TIME AND PURPOSE OF PROBLEMS

Problem 11.1 (Time 25–30 minutes)

Purpose—to provide the student with an opportunity to compute depreciation expense using a number of

Problem 11.2 (Time 25–35 minutes)

Purpose—to provide the student with an opportunity to compute depreciation expense using the following

Problem 11.3 (Time 40–50 minutes)

Purpose—to provide the student with an opportunity to compute depreciation expense using a number of

Problem 11.4 (Time 45–60 minutes)

Purpose—to provide the student with an opportunity to correct the improper accounting for trucks and

determine the proper depreciation expense. The student is required to compute separately the errors

arising in determining or entering depreciation or in recording transactions affecting Semitrucks.

Problem 11.5 (Time 25–35 minutes)

Purpose—to provide the student with a comprehensive problem related to property, plant, and equipment.

Problem 11.6 (Time 45–60 minutes)

Purpose—to provide the student with an opportunity to solve a complex problem involving a number of

Problem 11.7 (Time 30–35 minutes)

Purpose—to provide the student with the opportunity to solve a moderate problem involving a machinery

Problem 11.8 (Time 25–35 minutes)

Purpose—to provide the student with an opportunity to compute depreciation expense using a number of

Problem 11.9 (Time 15–25 minutes)

Purpose—to provide the student with an opportunity to analyze impairments for assets to be used and

assets to be disposed of.

Time and Purpose of Problems (Continued)

Problem 11.10 (Time 30–35 minutes)

Problem 11.11 (Time 15–20 minutes)

Purpose—to provide the student with a problem involving depletion and computation of profit or loss. The

student is asked to explain how to account for exploration and evaluation costs.

Problem 11.12 (Time 25–30 minutes)

Purpose—to provide the student with a problem involving the computation of estimated depletion and

depreciation costs associated with a tract of mineral land. The student must compute depletion and de–

*Problem 11.13 (Time 20–25 minutes)

Purpose—to provide the student with the opportunity to record land revaluation adjustments for 3 years.

*Problem 11.14 (Time 25–35 minutes)

Purpose—to provide the student with an opportunity to record equipment revaluation adjustments for

SOLUTIONS TO PROBLEMS

PROBLEM 11.1

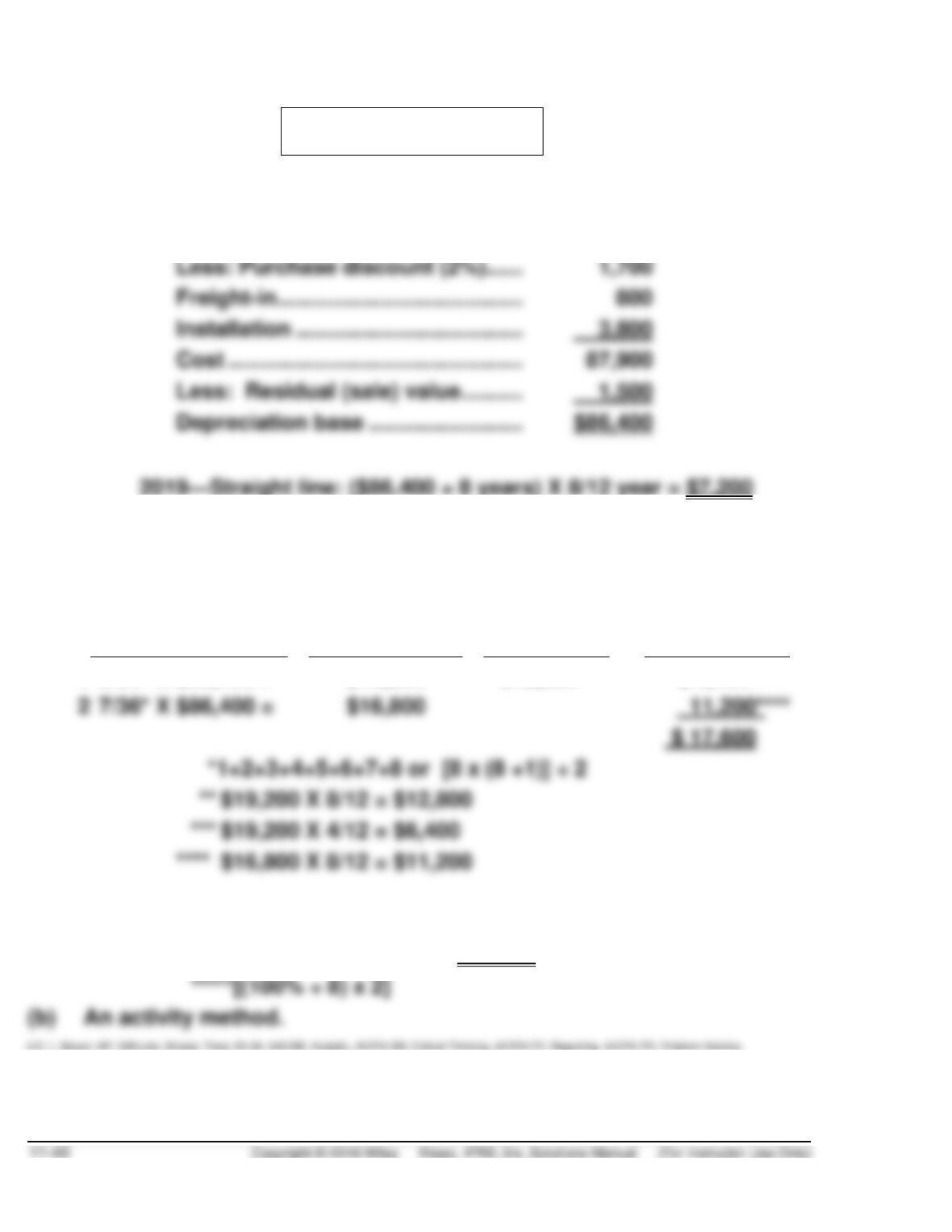

(a) 1. Depreciable Base Computation:

Purchase price………………………….

$85,000

Less: Purchase discount (2%) ……

Installation ……………………………….

3,800

Cost …………………………………………

Less: Residual (sale) value ……….

1,500

2. Sum-of-the-years’-digits for 2020

Machine Year

Total

Depreciation

2019

2020

1

8/36* X $86,400 =

$19,200

$12,800**

$ 6,400***

2

7/36* X $86,400 =

$16,800

****

3. Double-declining-balance for 2019

($87,900 X 25%***** X 8/12) = $14,650