CHAPTER 8

Valuation of Inventories: A Cost-Basis Approach

ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC)

Topics

Questions

Brief

Exercises

Exercises

Problems

Concepts

for Analysis

1.

Inventory accounts;

determining quantities,

1, 2, 3, 4, 5,

6, 7, 8, 9,

1, 3, 9

1, 2, 3,

4, 5

1, 2, 3

1, 2, 3, 6,

2.

Perpetual vs. periodic.

2, 6

4, 5, 8, 9, 17,

20

4, 5, 6, 7.

8, 9

3.

Recording of discounts.

11, 14

6, 7

3

4

19, 20, 21,

22, 23

9, 10

5.

Inventory accounting

changes.

12

10

6.

Inventory errors.

17, 18

8, 9

13, 14, 15,

16

20, 21, 22,

23

ASSIGNMENT CLASSIFICATION TABLE (BY LEARNING OBJECTIVE)

Learning Objectives

Brief

Exercises

Exercises

Problems

Concepts

for Analysis

1.

Describe inventory

classifications and

different inventory

systems.

1, 2

1, 2, 3, 4

2

Identify the goods and

costs include in

inventory.

3, 9

1, 2, 3, 4, 5,

6, 7, 8

2, 3

1, 2, 3, 4

3.

Compare the cost flow

assumptions used to

account for inventories.

4, 5, 6, 7

8, 9, 10, 11,

19, 20, 21,

22, 23

1, 4, 5, 6,

7, 8, 9, 10

5, 6

4.

Determine the effects of

inventory errors on the

financial statements.

8, 9

13, 14, 15,

16

Describe the LIFO cost

flow assumption.

20, 21, 22,

7, 8, 9, 10

ASSIGNMENT CHARACTERISTICS TABLE

Item

Description

Level of

Difficulty

Time

(minutes)

E8.1

Inventoriable costs.

Moderate

15–20

E8.2

Inventoriable costs.

Moderate

10–15

E8.3

Inventoriable costs.

Simple

10–15

E8.4

Inventoriable costs—perpetual.

Simple

10–15

E8.5

Determining merchandise amounts—periodic.

Simple

10–20

E8.6

Purchases recorded net.

Simple

10–15

E8.7

Purchases recorded, gross method.

Simple

20–25

E8.8

Periodic versus perpetual entries.

Moderate

15–25

E8.9

FIFO and average cost determination.

Moderate

20–25

E8.10

FIFO and average cost inventory.

Moderate

15–20

E8.11

Compute FIFO and average cost—periodic.

Moderate

15–20

E8.12

FIFO and average cost—income statement presentation.

Simple

15–20

E8.13

Inventoriable costs-error adjustments

Moderate

15–20

E8.14

Inventory errors, periodic.

Simple

10–15

E8.15

Inventory errors.

Simple

10–15

E8.16

Inventory errors.

Moderate

15–20

E8.17

FIFO and LIFO—periodic and perpetual.

Moderate

15–20

E8.18

FIFO, LIFO, and average cost determination.

Moderate

20–25

E8.19

FIFO, LIFO, average cost inventory.

Moderate

15–20

E8.20

FIFO and LIFO, periodic and perpetual.

Simple

10–15

E8.21

FIFO and LIFO, income statement presentation.

Simple

15–20

E8.22

FIFO and LIFO effects.

Moderate

20–25

E8.23

FIFO and LIFO—periodic.

Simple

10–15

P8.1

Various inventory issues.

Moderate

25–35

P8.2

Inventory adjustments.

Moderate

25–35

P8.3

Purchases recorded gross and net.

Simple

20–25

P8.4

Compute specific identification, FIFO, and average cost.

30–40

P8.5

Compute FIFO and average cost.

25–35

and perpetual.

ASSIGNMENT CHARACTERISTICS TABLE (Continued)

Item

Description

Level of

Difficulty

Time

(minutes)

P8.7

Compute FIFO, LIFO, and average cost.

Complex

40–55

P8.8

Compute FIFO, LIFO, and average cost.

Complex

40–55

and perpetual.

P8.10

Financial statement effects of FIFO and LIFO.

Moderate

30–40

CA8.1

Inventoriable costs.

Moderate

15–20

CA8.2

Inventoriable costs.

Moderate

15–25

CA8.3

Inventoriable costs.

Moderate

25–35

CA8.4

Accounting treatment of purchase discounts.

15–25

CA8.5

Average cost and FIFO.

15–20

CA8.6

Inventory choices—ethical issues

Moderate

20–25

ANSWERS TO QUESTIONS

1. In a merchandising concern, inventory normally consists of only one category, that is the product

awaiting resale. In a manufacturing concern, inventories consist of raw materials, work in process,

2. (a) Inventories are unexpired costs and represent future benefits to the owner. A statement of

financial position includes a listing of all unexpired costs (assets) at a specific point in time.

Because inventories are assets owned at the specific point in time for which a statement of

3. In a perpetual inventory system, data are available at any time on the quantity and dollar amount

of each item of material or type of merchandise on hand. A physical inventory means that

4. No. Mishima, Inc. should not report this amount on its statement of financial position. As

5. Product financing arrangements are essentially off-balance-sheet financing devices. These arrange-

ments make it appear that a company has sold its inventory or never taken title to it so they can

6. (a) Inventory.

(b) Not shown, possibly in a note to the financial statements if material.

7. Yang can consider the inventory sold if it can reasonably estimate the amount of returns. The

8. Holland can consider goods sold with right of return as revenue if it can reasonably estimate the

returns. Holland will consider the goods sold as long as it can estimate bad debts accurately.

LO: 2, Bloom: C, Difficulty: Simple, Time: 3-5, AACSB: Communication, AICPA BB: None, AICPA FC: Reporting, AICPA PC: Communication

Questions Chapter 8 (Continued)

9. Cost, which has been defined generally as the price paid or consideration given to acquire an

asset, is the primary basis for accounting for inventories. As applied to inventories, cost means the

10. By their nature, product costs “attach” to the inventory and are recorded in the inventory account.

These costs are directly connected with the bringing of goods to the place of business of the buyer

and converting such goods to a salable condition. Such charges would include freight charges on

goods purchased, other direct costs of acquisition, and labor and other production costs incurred

11. Cash discounts (purchase discounts) should not be accounted for as income when payments are

made. Income should be recognized when a performance obligation is satisfied (when the

12. Companies usually expense interest costs. Interest costs are considered a cost of financing and

are generally expensed as incurred. IFRS indicates that companies should only capitalize interest

13. Biestek should account for the usual spoilage as a cost of its inventory, but the unusual spoilage

14. €60.00, €63.00, €61.80. (Freight-In not included for discount because it might be paid to different

party.)

LO: 1,2, Bloom: AP, Difficulty: Simple, Time: 5-7, AACSB: Analytic, AICPA BB: Critical Thinking, AICPA FC: Reporting, AICPA PC: Problem Solving

15. Arguments for the specific identification method are as follows:

(1) It provides an accurate and ideal matching of costs and revenues because the cost is specifi–

cally identified with the sales price.

Questions Chapter 8 (Continued)

Arguments against the specific identification method include the following:

(1) The cost of using it restricts its use to goods of high unit value.

16. The first-in, first-out method approximates the specific identification method when the physical flow

of goods is on a FIFO basis. When the goods are subject to spoilage or deterioration, FIFO is

particularly appropriate. In comparison to the specific identification method, an attractive aspect of

FIFO is the elimination of the danger of artificial determination of income by the selection of

advantageously priced items to be sold. The basic assumption is that costs should be charged in

the order in which they are incurred. As a result, the inventories are stated at the latest costs.

Where the inventory is consumed and valued in the FIFO manner, there is no accounting recognition

of unrealized gain or loss. A criticism of the FIFO method is that it maximizes the effects of price

fluctuations upon reported income because current revenue is matched with the oldest costs which are

17. Beckham should explain to the Swiss president that an error in the ending inventory of 2019 also

affects the beginning inventory of 2020. For example, understating the 2019 ending inventory

18. This omission would have no effect upon the net income for the year, since the purchases and the

ending inventory are understated in the same amount. With respect to financial position, both the

*19. In times of rising prices, LIFO results in lower income, lower taxes, and lower inventory on the

statement of financial position. In times of falling prices, the results are just the opposite.

LO: 5, Bloom: K, Difficulty: Simple, Time: 3-5, AACSB: Communication, AICPA BB: None, AICPA FC: Reporting, AICPA PC: Communication

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 8.1

RIVERA A.S.

Statement of Financial Position (Partial)

December 31

Current assets

Inventories

Finished goods ……………………………………

₺170,000

Work in process ………………………………….

Raw materials ……………………………………..

Prepaid insurance ………………………………………

Receivables (net) ………………………………………..

Cash ………………………………………………………….

BRIEF EXERCISE 8.2

Inventory (150 X €34) ……………………………………………….

5,100

Accounts Payable …………………………………………..

5,100

Accounts Payable (6 X €34) ……………………………………..

Inventory ……………………………………………………….

Accounts Receivable (125 X €50) …………………………..

6,250

Sales ………………………………………………………………

6,250

Cost of Goods Sold (125 X €34)…………………………..

4,250

BRIEF EXERCISE 8.3

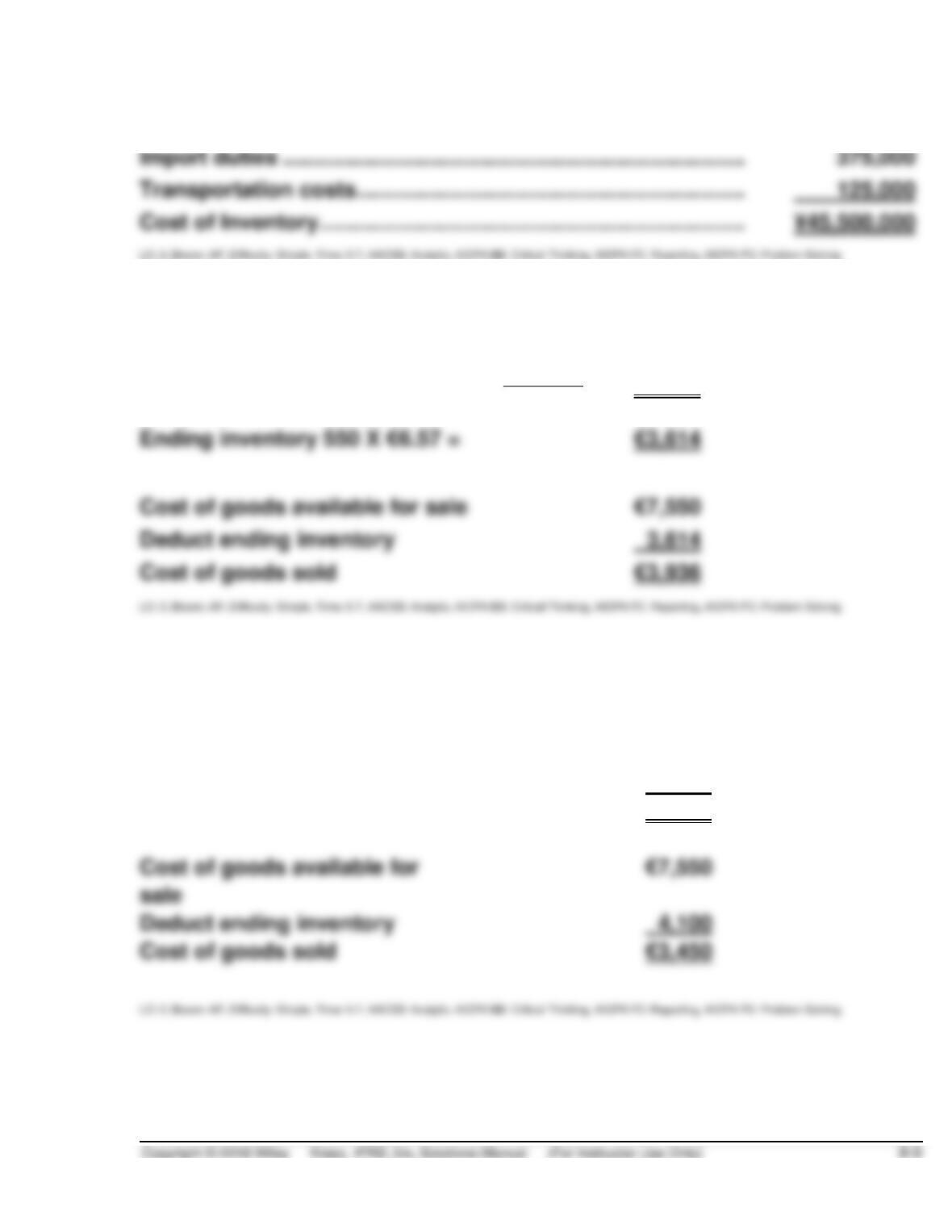

Purchase price ………………………………………………………………

¥45,000,000

Import duties …………………………………………………………………

Transportation costs ………………………………………………………

125,000

BRIEF EXERCISE 8.4

Weighted average cost per unit

€7,550

=

€ 6.57

1,150

Cost of goods available for sale

Deduct ending inventory

BRIEF EXERCISE 8.5

Ending inventory:

June 23

400 X €8

=

€3,200

June 15

150 X €6

=

900

€4,100

Deduct ending inventory

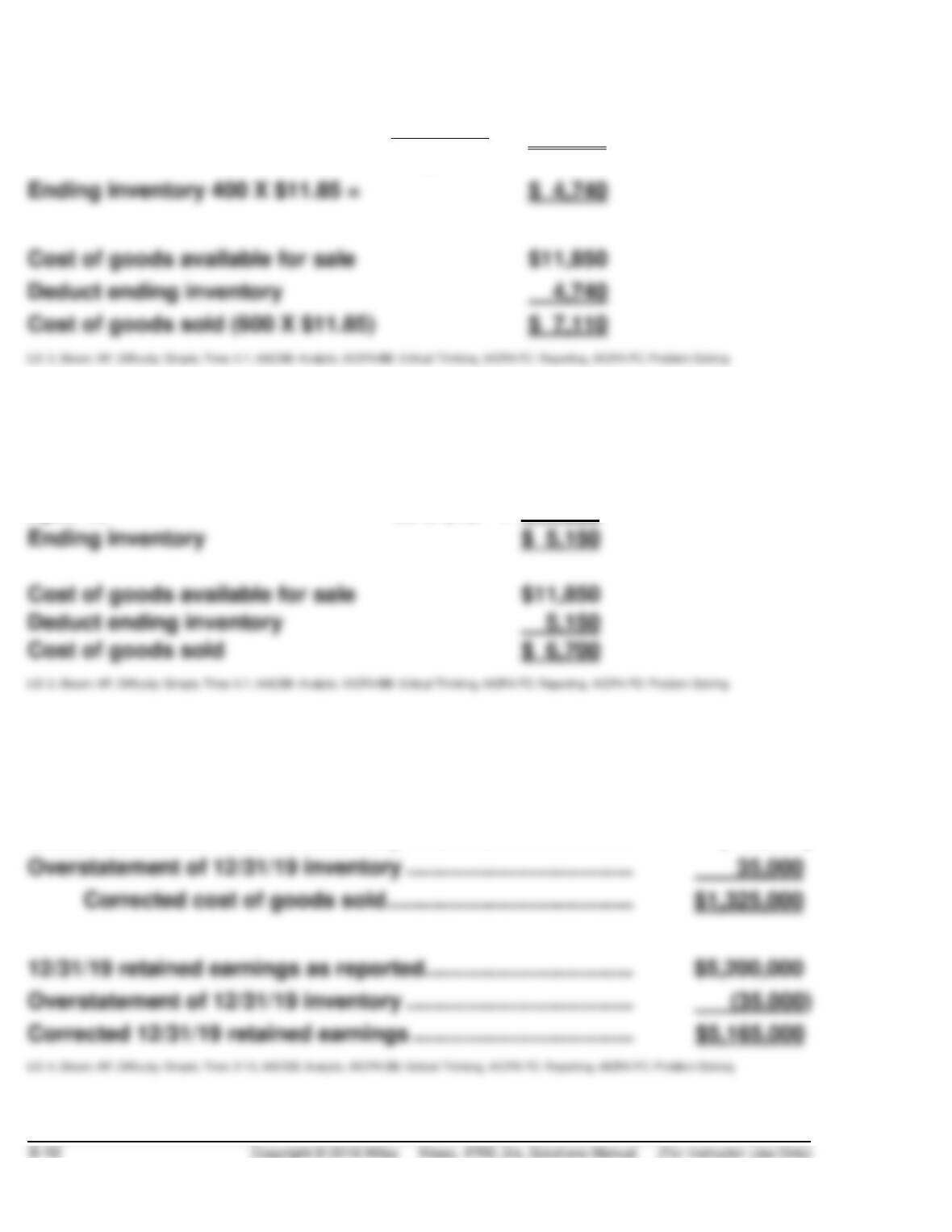

BRIEF EXERCISE 8.6

Weighted average cost per unit

$11,850

=

$ 11.85

1,000

Cost of goods available for sale

Deduct ending inventory

BRIEF EXERCISE 8.7

Ending inventory:

April 23

350 X $13

=

$ 4,550

April 15

50 X $12

=

600

Ending inventory

$ 5,150

Cost of goods available for sale

$11,850

Deduct ending inventory

5,150

BRIEF EXERCISE 8.8

Cost of goods sold as reported ……………………………………….

$1,400,000

Overstatement of 12/31/18 inventory ……………………………….

(110,000)

Overstatement of 12/31/19 inventory ……………………………….

12/31/19 retained earnings as reported…………………………….

Overstatement of 12/31/19 inventory ……………………………….

BRIEF EXERCISE 8.9

December 31 inventory per physical count ………………………

$200,000

22,000

*BRIEF EXERCISE 8.10

Ending inventory:

April 1 250 X $10 =

$ 2,500

April 15 150 X $12 =

1,800

Cost of goods available for sale

$11,850

Deduct ending inventory

4,300

SOLUTIONS TO EXERCISES

EXERCISE 8.1 (15–20 minutes)

Items 2, 3, 5, 8, 10, 13, 14, 16, and 17 would be reported as inventory in the

financial statements.

The following items would not be reported as inventory:

1. Cost of goods sold in the income statement.

4. Not reported in the financial statements.

6. Cost of goods sold in the income statement.

EXERCISE 8.2 (10–15 minutes)

Inventory per physical count …………………………………………………

$441,000

Goods in transit to customer, f.o.b. destination ……………………..

+ 33,000

Goods in transit from vendor, f.o.b. shipping point…………………

+ 51,000

EXERCISE 8.3 (10–15 minutes)

1. Include. Title to merchandise passes to customer only when it is

shipped.

4. Do not include. Goods received on consignment remain the property

of the consignor.

EXERCISE 8.4 (10–15 minutes)

1.

Raw Materials Inventory …………………………….

8,100

Accounts Payable ……………………………..

8,100

2.

No adjustment necessary.

3.

Raw Materials Inventory …………………………….

Accounts Payable ……………………………..

4.

Accounts Payable ……………………………………..

7,500

Raw Materials Inventory …………………….

7,500

5.

Raw Materials Inventory …………………………….

Accounts Payable ……………………………..

EXERCISE 8.5 (10–20 minutes)

2018

2019

2020

Sales ………………………………………………

£290,000

£360,000

£410,000

Sales Returns …………………………………

6,000

13,000

10,000

Net Sales ………………………………………..

284,000

347,000

400,000

Beginning Inventory ………………………..

32,000

37,000**

Ending Inventory …………………………….

37,000

34,000

Purchases ………………………………………

247,000

260,000

Purchase Returns and Allowances …..

5,000

10,000

8,000

12,000

Cost of Good Sold …………………………..

238,000

256,000

Gross Profit on Sales ………………………

91,000

97,000

*This was given as the beginning inventory for 2019.

EXERCISE 8.6 (10–15 minutes)

(a)

May 10

Purchases ……………………………………………………….

19,600

Accounts Payable

(£20,000 X .98) …………………………..

19,600

May 11

Purchases ……………………………………………………….

14,850

Accounts Payable

(£15,000 X .99) …………………………..

14,850

May 19

Accounts Payable …………………………..

19,600

Cash ……………………………………………………….

19,600

May 24

Purchases ……………………………………………………….

11,270

Accounts Payable

11,270

EXERCISE 8.6 (Continued)

(b)

May 31

Purchase Discounts Lost …………………………..

150

Accounts Payable

(£15,000 X .01) ……………………………………………..

(Discount lost on purchase

of May 11, £15,000, terms

1/15, n/30)

EXERCISE 8.7 (20–25 minutes)

(a)

Feb. 1

Inventory [¥12,000 – (¥12,000 X 10%)] ………………………

10,800

Accounts Payable …………………………..

10,800

Feb. 4

Accounts Payable

[¥3,000 – (¥3,000 X 10%)] …………………………..

2,700

Inventory……………………………………………………….

2,700

Feb. 13

Accounts Payable (¥10,800 – ¥2,700) ……………………….

8,100

Inventory (3% X ¥8,100) …………………………..

Cash ……………………………………………………….

7,857

(b)

Feb. 1

Purchases [¥12,000 – (¥12,000 X 10%)] …………………….

10,800

Accounts Payable …………………………..

10,800

Feb. 4

Accounts Payable

[¥3,000 – (¥3,000 X 10%)] …………………………..

2,700

Purchase Returns and Allowances ………………….

2,700

Feb. 13

Accounts Payable (¥10,800 – ¥2,700) ……………………….

8,100

Cash ……………………………………………………….

7,857

EXERCISE 8.7 (Continued)

(c)

Purchase price (list) ……………………………………

¥12,000

Less: Trade discount (10% X ¥12,000) …………

1,200

Price on which cash discount based ……………

Less: Cash discount (3% X ¥10,800) ……………

324

EXERCISE 8.8 (15–25 minutes)

(a)

Jan. 4

Accounts Receivable ……………………….

640

Sales (80 X $8) …………………………

640

Jan. 11

Purchases ($150 X $6.50) …………………

975

Accounts Payable ……………………

975

Jan. 13

Accounts Receivable ……………………….

1,050

Sales (120 X $8.75) …………………..

1,050

Jan. 20

Purchases (160 X $7) ……………………….

1,120

Accounts Payable ……………………

1,120

Jan. 27

Accounts Receivable ……………………….

900

Sales (100 X $9) ……………………….

900

Jan. 31

Inventory ($7 X 110) …………………………

770

Cost of Goods Sold ………………………….

1,925*

Purchases ($975 + $1,120) ………..

2,095

Inventory (100 X $6) …………………

600

EXERCISE 8.8 (Continued)

(b)

Sales ($640 + $1,050 + $900)………………

$2,590

Cost of goods sold …………………………...

1,925

Gross profit ……………………………………..

$ 665

(c)

Jan. 4

Accounts Receivable …………………………..

640

Sales (80 X $8) …………………………..

640

Cost of Goods Sold…………………………………………………

480

Inventory (80 X $6) …………………………..

Jan. 11

Inventory ……………………………………………………….

975

Accounts Payable (150 X $6.50) …………………………..

975

Jan. 13

Accounts Receivable …………………………..

1,050

Sales (120 X $8.75) …………………………..

1,050

Cost of Goods Sold…………………………………………………

770

(100 X $6.50)] …………………………..

Jan. 20

Inventory ……………………………………………………….

1,120

Accounts Payable (160 X $7) …………………………..

1,120

Jan. 27

Accounts Receivable …………………………..

900

Sales (100 X $9) …………………………..

900

Cost of Goods Sold…………………………………………………

(d)

Sales ……………………………………………….

$2,590

Cost of goods sold

EXERCISE 8.9 (20–25 minutes)

(a)

1.

FIFO

500 @ $6.79 =

$3,395

300 @ $6.60 =

2.

Average cost

Total cost

=

$33,655*

= $6.35 average cost per unit

Total units

5,300

(b)

1.

FIFO

500 @ $6.79 =

$3,395

300 @ $6.60 =

EXERCISE 8.9 (Continued)

2. Average cost.

Purchased

Sold

Balance

Date

No. of

units

Unit

cost

No. of

units

Unit

cost

No. of

units

Unit

cost

Amount

April 1

600

$6.0000

$3,600

3

500

$6.000

100

6.0000

600

4

1,500

$6.08

1,600

6.0750

9,720

8

800

6.40

2,400

6.1833

14,840

9

1,300

6.1833

1,100

6.1833

6,802

600

6.1833

500

6.1833

3,092

1,200

6.50

1,700

6.4071

10,892

700

6.60

2,400

15,512

1,200

6.4633

1,200

6.4633

7,756

900

6.4633

300

6.4633

1,939

500

6.79

800

6.6675

5,334

EXERCISE 8.10 (15–20 minutes)

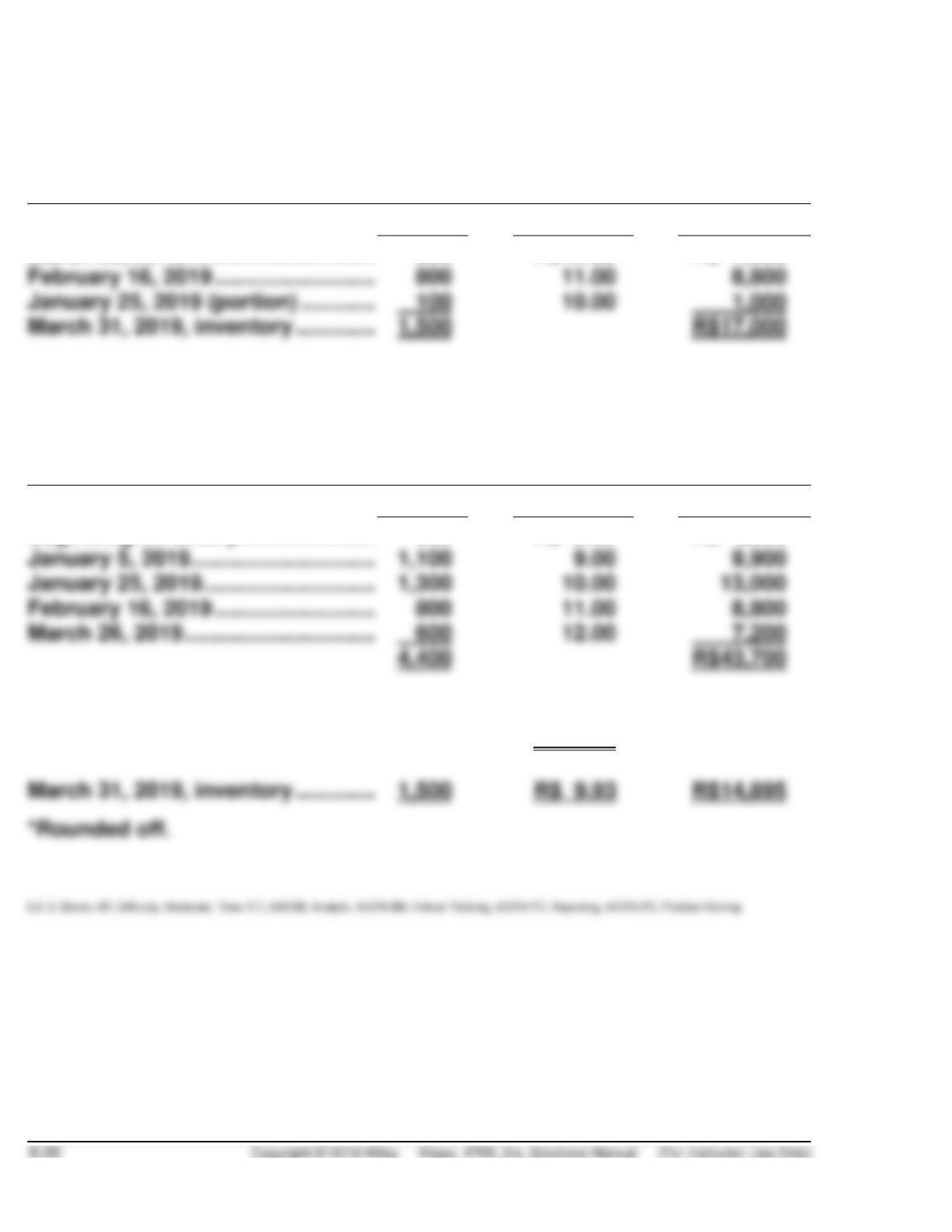

(a) ESPLANADE SA

Computation of Inventory for Product BAP

Under Specific Identification Inventory Method

March 31, 2019

Units

Unit Cost

Total Cost

EXERCISE 8.10 (Continued)

(b) ESPLANADE SA

Computation of Inventory for Product BAP

Under FIFO Inventory Method

March 31, 2019

Units

Unit Cost

Total Cost

March 26, 2019 ………………………….

600

R$12.00

R$ 7,200

February 16, 2019 ……………………..

January 25, 2019 (portion) …………

March 31, 2019, inventory ………….

(c) ESPLANADE SA

Computation of Inventory for Product BAP

Under Weighted-Average Inventory Method

March 31, 2019

Units

Unit Cost

Total Cost

Beginning inventory ………………….

600

R$ 8.00

R$ 4,800

January 5, 2019 …………………………

January 25, 2019 ……………………….

1,300

February 16, 2019 ……………………..

Weighted-average cost

($43,700 ÷ 4,400) …………………….

R$ 9.93*

March 31, 2019, inventory ………….