COMPARATIVE ANALYSIS CASE (Continued)

Using foreign debt to finance operations is subject to the risk of

FINANCIAL STATEMENT ANALYSIS CASE 1

COMMONWEALTH EDISON CO.

(a) Due to the markdown from 99.803 to 99.25, Commonwealth Edison

would record a slightly larger discount and, of course, receive and

(b) In the same Wall Street Journal article, the following explanation was

provided for Commonwealth Edison’s bond markdown and slow sale:

“Commonwealth had the misfortune to begin its giant

offering only hours before investor sentiment was soured

Other economic events that can and do affect the price of securities

issued are:

1. A change in the Federal Reserve’s lending rate.

2. A change in the bank prime rate.

FINANCIAL STATEMENT ANALYSIS CASE 1 (Continued)

Of course, noneconomic, political, or other world events can also affect

the day-to-day sale of securities.

The “recent rebound in industrial productivity” mentioned in the

FINANCIAL STATEMENT ANALYSIS CASE 2

Eurotec

(a) Answers will vary. The company may have decided to refinance in

order to free cash needed for some other purpose, to reduce current

cash needs, or to leave a credit line available for quick access.

(b) The investor probably enjoys a higher interest rate than that obtained

Bonds Payable ……………………………………………………….

Cash ……………………………………………………….

(c)

Cash [(€250,000,000 X 1.02) +

(€95,000,000 X .99)] ………………………………………………

349,050,000

Bonds Payable ……………………………………………….

349,050,000

Cash ……………………………………………………….

Bonds Payable ……………………………………………….

255,000,000

Cash ……………………………………………………….

Bonds Payable ……………………………………………….

FINANCIAL STATEMENT ANALYSIS CASE 2 (Continued)

(d) Answers will vary. One advantage would be that it is a bond whose

ACCOUNTING, ANALYSIS, AND PRINCIPLES

ACCOUNTING

Bond calculations:

PV of bonds at issuance = (€1,500 X PVF10,6) + (€1,500 X 0.05 X PVF – OA10,6)

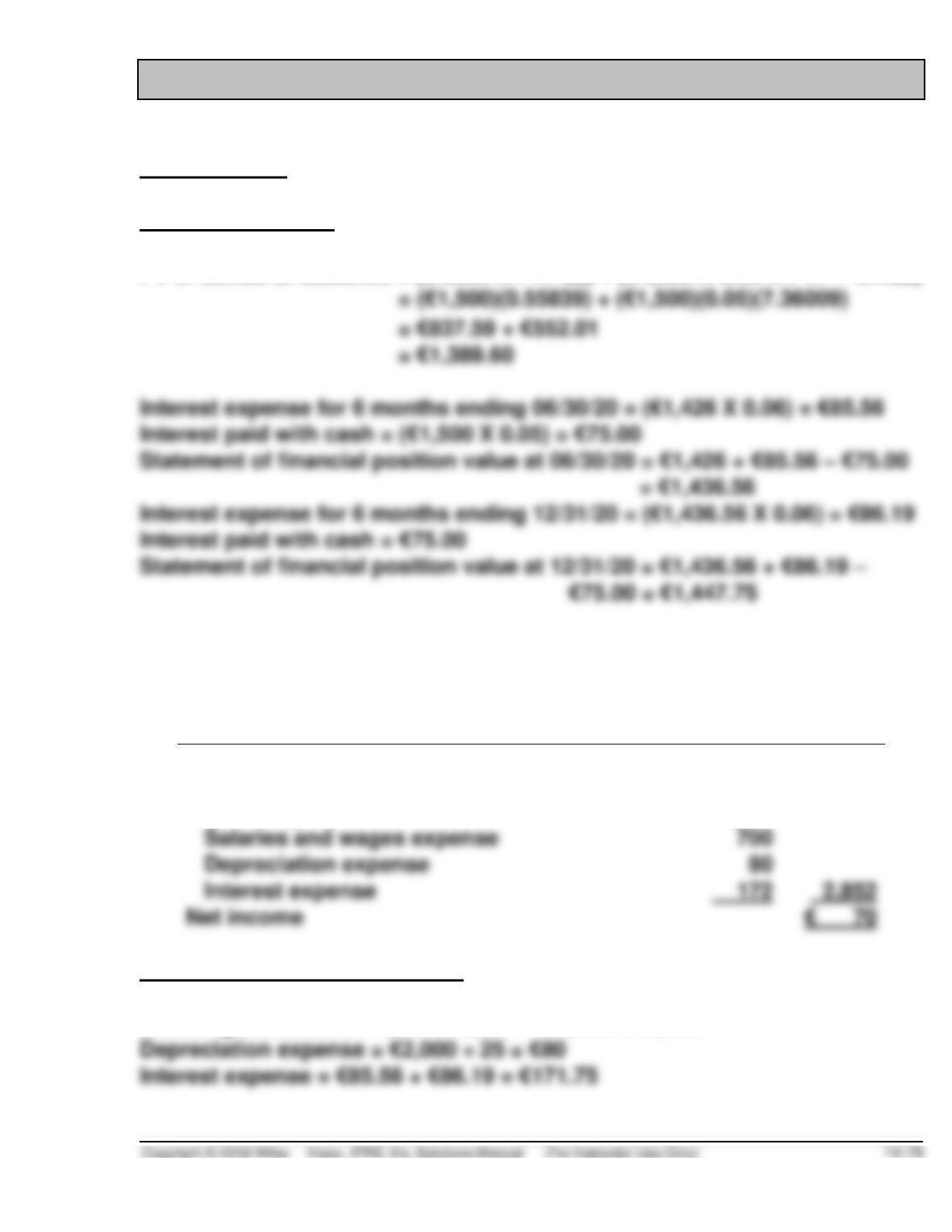

BUGANT SA

INCOME STATEMENT

for the year ended 12/31/20

Sales

€2,922

Expenses:

Cost of goods sold

€1,900

Salaries and wages expense

Depreciation expense

Net income

Income statement calculations:

Cost of goods sold = €1,800 + €2,000 – €1,900 = €1,900

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

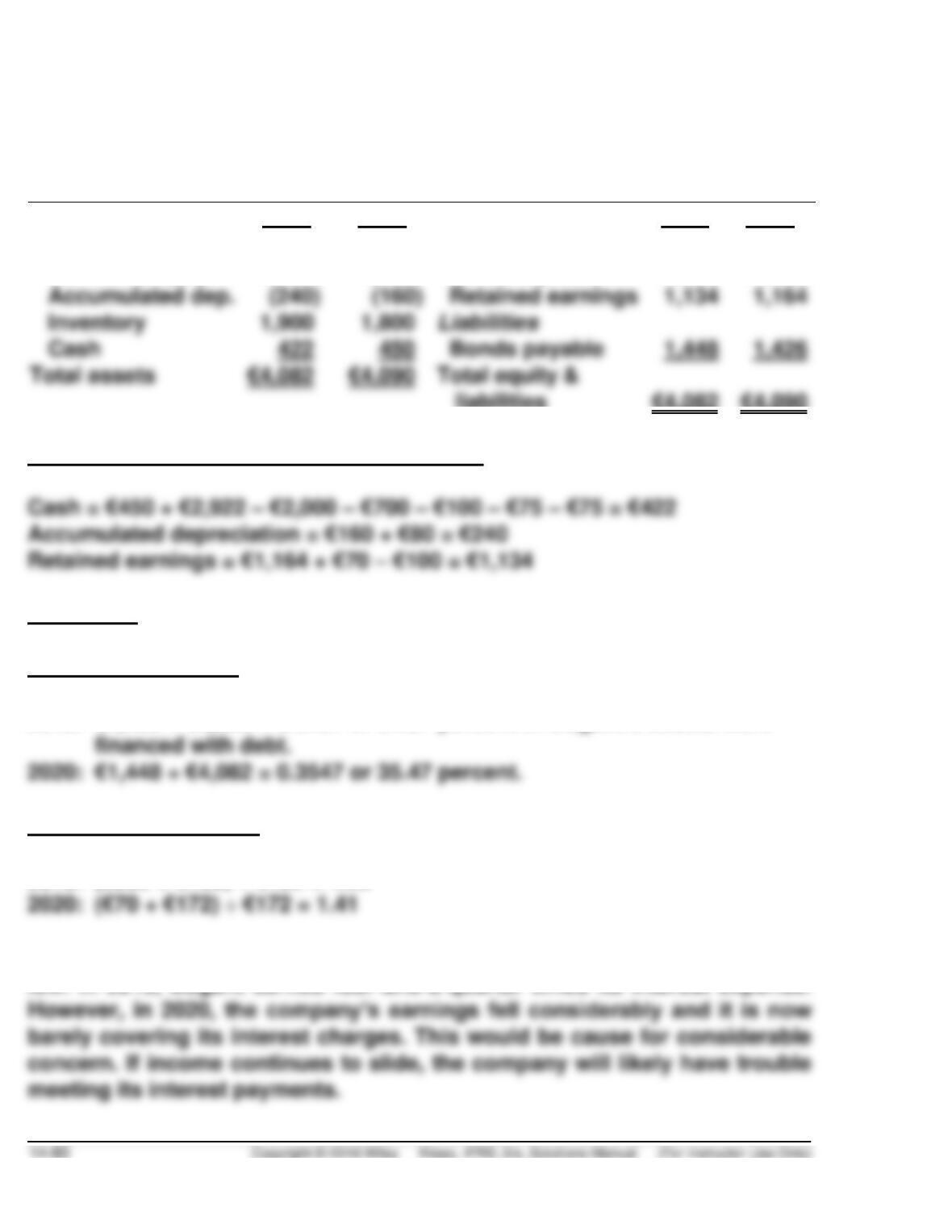

BUGANT, SA

STATEMENT OF FINANCIAL POSITION

DECEMBER 31

2020

2019

2020

2019

Assets

Equity

Plant and equip.

€2,000

€2,000

Share capital

€1,500

€1,500

Accumulated dep.

Retained earnings

Inventory

Liabilities

Cash

Bonds payable

liabilities

€4,082

€4,090

Statement of financial position calculations:

ANALYSIS

Debt-to–assets ratio:

2019: €1,426 ÷ €4,090 = 0.3487 or 34.87 percent of Bugant’s assets were

Times interest earned:

2019: (€550 + €169) ÷ €169 = 4.25

Less than half of Bugant’s financing comes from debt, which is relatively

low. In 2019, Bugant earned four-and-a-quarter times its interest expense.

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

Note that interest expense in this problem is larger than the company’s

yearly cash interest payments. Cash payments for interest are €150 per

PRINCIPLES

One could argue that this represents a classic trade-off between relevance

and faithful representation. Many people think that the fair values of

companies’ assets and liabilities are relevant to making investing and

On the other hand, one might argue that fair values of debt are not really

relevant if the company will not pay off the debt early.

RESEARCH CASE

According to IFRS9:

(a) 5.1.1 Except for trade receivables within the scope of paragraph 5.1.3,

at initial recognition, an entity shall measure a financial asset or

(b) 3.3 Derecognition of financial liabilities

3.3.1 An entity shall remove a financial liability (or a part of a financial

3.3.2 An exchange between an existing borrower and lender of debt

instruments with substantially different terms shall be accounted for

3.3.3 The difference between the carrying amount of a financial

liability (or part of a financial liability) extinguished or transferred to

RESEARCH CASE (Continued)

B3.3.6 For the purpose of paragraph 3.3.2, the terms are substantially

different if the discounted present value of the cash flows under the

new terms, including any fees paid net of any fees received and

discounted using the original effective interest rate, is at least 10 per

GAAP CONCEPTS AND APPLICATION

GAAP14.1. Similarities are as follows:

• As indicated above, U.S. GAAP and IFRS have similar

liability definitions. Both also classify liabilities as current

and non-current.

• Much of the accounting for bonds and long-term notes is

liabilities for future losses.

Differences are as follows:

• Under U.S. GAAP, companies must classify a refinancing

as current only if it is completed before the financial

statements are issued. IFRS requires that the current

portion of long-term debt be classified as current unless an

agreement to refinance on a long-term basis is completed

before the reporting date.

GAAP CONCEPTS AND APPLICATION (Continued)

• U.S. GAAP uses the term troubled debt restructurings and

develops recognition rules related to this category. IFRS

generally assumes that all restructurings should be

considered extinguishments of debt.

GAAP14.2. (1) Cash …………………………………………………… 92,608

Discount on Bonds Payable ………………… 7,392

Bonds Payable ………………………………. 100,000

(2) Interest Expense ($92,608 X 11%) …………. 10,187

GAAP CONCEPTS AND APPLICATION (Continued)

GAAP14.3. As indicated in the Global Accounting Insights of Chapter 2,

the IASB and FASB are working on a conceptual framework

project, part of which will examine the definition of a liability.