CHAPTER 14

Non-Current Liabilities

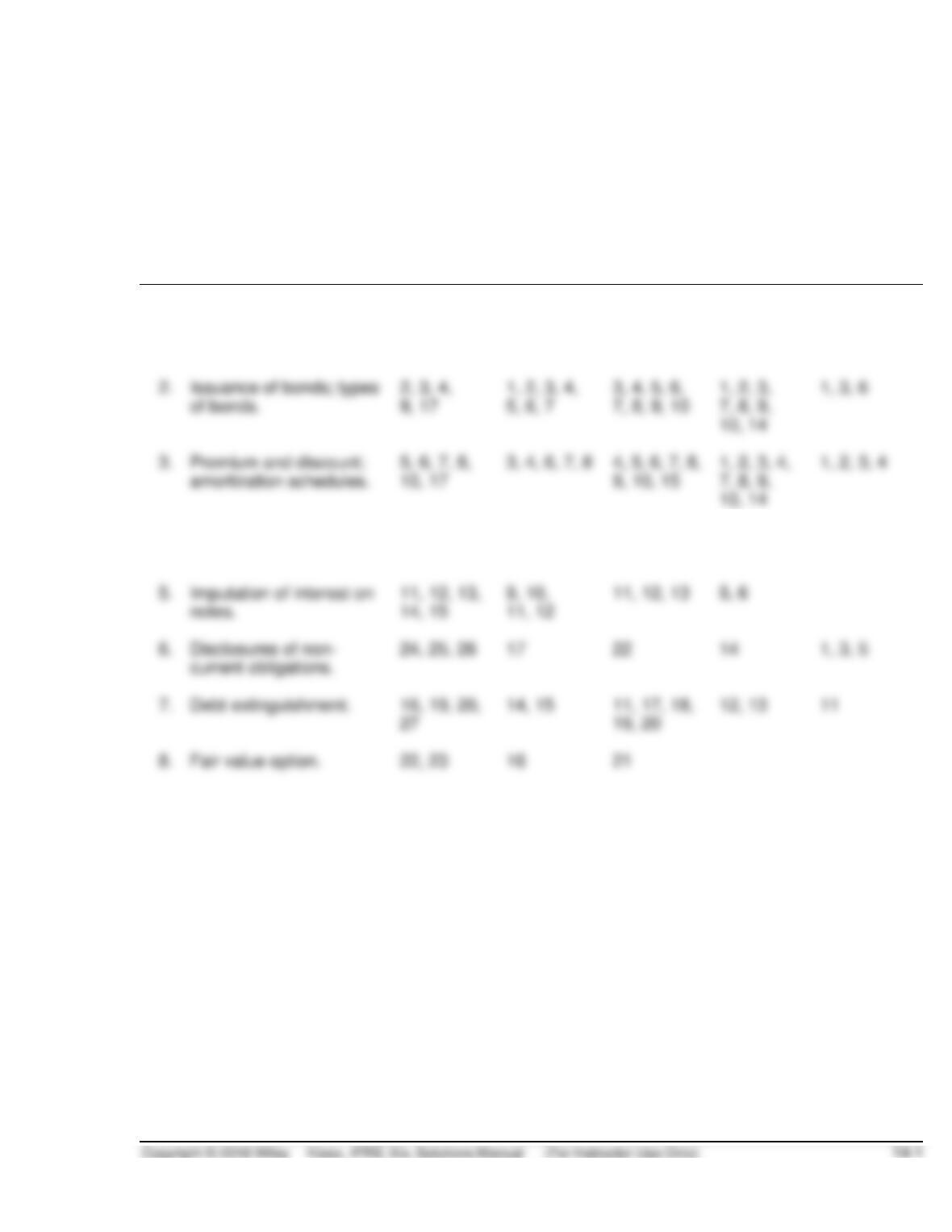

ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC)

Topics

Questions

Brief

Exercises

Exercises

Problems

Concepts

for Analysis

1.

Non-current liability;

classification; definitions.

1, 10, 11,

19, 20, 22,

23, 24

1, 2

10

1, 2, 3

2.

Issuance of bonds; types

of bonds.

2, 3, 4,

9, 17

1, 2, 3, 4,

5, 6, 7

3, 4, 5, 6,

7, 8, 9, 10

1, 2, 3,

7, 8, 9,

10, 14

1, 3, 6

3.

Premium and discount;

amortization schedules.

5, 6, 7, 8,

10, 17

3, 4, 6, 7, 8

4, 5, 6, 7, 8,

9, 10, 15

1, 2, 3, 4,

7, 8, 9,

10, 14

1, 2, 3, 4

4.

Retirement and refunding

of debt.

18, 21

13

14, 15, 16

2, 7, 8, 9,

10, 14

3, 4, 5

5.

Imputation of interest on

notes.

11, 12, 13,

14, 15

9, 10,

11, 12

11, 12, 13

5, 6

6.

Disclosures of non-

current obligations.

24, 25, 26

17

22

14

1, 3, 5

7.

Debt extinguishment.

16, 19, 20,

14, 15

11, 17, 18,

19, 20

12, 13

11

Fair value option.

22, 23

ASSIGNMENT CLASSIFICATION TABLE (BY LEARNING OBJECTIVE)

Learning Objectives

Brief

Exercises

Exercises

Problems

Concepts

for

Analysis

1. Describe the nature of bonds and

indicate the accounting for bond

issuances.

1, 2, 3, 4,

5, 6, 7, 8

1, 2, 3, 4, 5,

6, 7, 8, 9, 10,

14, 15, 16

1, 2, 3, 4, 7,

8, 9, 10, 14

1, 2, 3, 4,

6

notes payable.

9, 10, 11, 12

11, 12, 13

5, 6

3. Describe the accounting for the

extinguishment of non-current

liabilities.

13, 14, 15

14, 15, 16,

17, 18, 19, 20

2, 7, 8, 9,

10, 11, 12,

13, 14

3, 4

analyze non-current liabilities.

16, 17

21, 22

7, 14

1, 2, 3, 4,

5

ASSIGNMENT CHARACTERISTICS TABLE

Item

Description

Level of

Difficulty

Time

(minutes)

E14.1

Classification of liabilities.

Simple

15–20

E14.2

Classification.

Simple

15–20

E14.3

Entries for bond transactions.

Simple

15–20

E14.4

Entries for bond transactions.

Simple

15–20

E14.5

Entries for bond transactions.

Simple

15–20

E14.6

Amortization schedule.

Simple

15–20

E14.7

Determine proper amounts in account balances.

Moderate

15–20

E14.8

Entries and questions for bond transactions.

Moderate

20–30

E14.9

Entries for bond transactions.

Moderate

15–20

E14.10

Information related to various bond issues.

Simple

20–30

E14.11

Entries for zero-interest-bearing notes.

Simple

15–20

E14.12

Imputation of interest.

Simple

15–20

E14.13

Imputation of interest with right.

Moderate

15–20

E14.14

Entry for retirement of bond; bond issue costs.

Simple

20–25

E14.15

Entries for retirement and issuance of bonds.

Simple

12–16

E14.16

Entries for retirement and issuance of bonds.

Simple

10–15

E14.17

Settlement of debt.

Moderate

15–20

E14.18

Loan modification.

Moderate

20–30

E14.19

Loan modification.

Moderate

25–30

E14.20

Entries for settlement of debt.

Moderate

20–25

E14.21

Fair value option.

Moderate

20–25

E14.22

Simple

10–15

P14.1

Analysis of amortization schedule and interest entries.

Simple

15–20

P14.2

Issuance and retirement of bonds.

Moderate

25–30

P14.3

Negative amortization.

Moderate

20–30

P14.4

Effective-interest method.

Moderate

40–50

P14.5

Entries for zero-interest-bearing note.

Simple

15–25

P14.8

Comprehensive bond problem.

Moderate

50–65

P14.9

Issuance of bonds between interest dates, retirement.

Moderate

20–25

P14.10

Entries for life cycle of bonds.

Moderate

20–25

P14.11

Modification of debt.

Moderate

15–20

ASSIGNMENT CHARACTERISTICS TABLE (Continued)

Item

Description

Level of

Difficulty

Time

(minutes)

CA14.1

Bond theory: statement of financial position

presentations, interest rate, premium.

Moderate

25–30

CA14.2

Various non-current liability conceptual issues.

Moderate

10–15

CA14.4

Bond theory: amortization and gain or loss recognition.

20–25

CA14.5

Off-balance-sheet financing.

Moderate

20–30

ANSWERS TO QUESTIONS

1. (a) Funds might be obtained through long-term debt from the issuance of bonds, and from the

signing of long-term notes and mortgages.

(b) A bond indenture is a contractual agreement (signed by the issuer of bonds) between the

2. If the entire bond matures on a single date, the bonds are referred to as term bonds. Mortgage

bonds are secured by real estate. Collateral trust bonds are secured by the securities of other

corporations. Debenture bonds are unsecured. The interest payments for income bonds depend on

the existence of operating income for the issuing company. Callable bonds may be called and

3. (a) Yield rate—the rate of interest actually earned by the bondholders; it is synonymous with the

effective and market rates.

4. (a) Maturity value—the face value of the bonds; the amount which is payable upon maturity.

(b) Face value—synonymous with par value and maturity value.

Questions Chapter 14 (Continued)

5. A discount on bonds payable results when investors demand a rate of interest higher than the rate

stated on the bonds. The investors are not satisfied with the nominal interest rate because they

can earn a greater rate on alternative investments of equal risk. They refuse to pay par for the

6. The amortization of a bond premium decreases interest expense while the amortization of a bond

discount increases interest expense over the life of a bond.

LO: 1, Bloom: K, Difficulty: Simple, Time: 3-5, AACSB: None, AICPA BB: None, AICPA FC: Reporting, AICPA PC: Communication

7. Bond discount and bond premium are amortized on an effective-interest basis. The effective–

interest method results in an increasing or decreasing amount of interest each period. This is

8. The annual interest expense will decrease each period throughout the life of the bonds. Under the

effective-interest method the interest expense each period is equal to the effective or yield interest

9. Bond issuance costs should be recorded as a reduction to the issue amount of the bond payable

and amortized into expense over the life of the bond, through an adjustment to the effective-

interest rate.

LO: 1, Bloom: K, Difficulty: Simple, Time: 3-5, AACSB: None, AICPA BB: None, AICPA FC: Reporting, AICPA PC: Communication

10. Amortization of bond discount will increase interest expense. A discount on bonds payable results

when investors demand a rate of interest higher than the rate stated on the bonds. The investors

11. The entire arrangement must be evaluated and an appropriate interest rate imputed. This is done

by (1) determining the fair value of the property, goods, or services exchanged or (2) determining

12. If a note is issued for cash, the present value is assumed to be the cash proceeds. If a note is

issued for noncash consideration, the present value of the note should be measured by the fair

Questions Chapter 14 (Continued)

13. When a debt instrument is exchanged in a bargained transaction entered into at arm’s length, the

stated interest rate is presumed to be fair unless: (1) no interest rate is stated, or (2) the stated

14. Imputed interest is the interest factor (a rate or amount) assumed or assigned which is different

from the stated interest factor. It is necessary to impute an interest rate when the stated interest

rate is presumed to be unreasonable. The imputed interest rate is used to establish the present

15. A fixed-rate mortgage is a note that requires payment of interest by the mortgagor at a rate that

does not change during the life of the note. A variable-rate mortgage is a note that features an

16. Three different types of situations result with extinguishments (1) Settlement in cash;

(2) Exchanging assets or securities; and (3) Modification of terms.

LO: 3, Bloom: K, Difficulty: Simple, Time: 3-5, AACSB: None, AICPA BB: None, AICPA FC: Reporting, AICPA PC: Communication

17. The call feature of a bond issue grants the issuer the privilege of purchasing, after a certain date

at a stated price, outstanding bonds for the purpose of reducing indebtedness or taking advantage

18. It is sometimes desirable to reduce bond indebtedness in order to take advantage of lower

prevailing interest rates. Also, the company may not want to make a very large cash outlay all at

once when the bonds mature.

Questions Chapter 14 (Continued)

19. A transfer of noncash assets (real estate, receivables, or other assets) or the issuance of the

debtor’s stock can be used to settle a debt obligation in an extinguishment. In these situations, the

20. (a) The creditor will grant concessions in debt modification situation because it appears to be

the more likely way to ensure the highest possible collection on the loan.

(b) The creditor might grant the debtor any one or a combination of the following concessions:

1. Reduce the face amount of the debt.

21. The debtor will record a gain when the discounted restructured cash flows are less than the

22. The fair value option gives companies the choice to record their non-current liabilities at fair value.

The controversy in applying the fair value option involves companies recording an unrealized gain

23. Unrealized Holding Gain or Loss-Income ……………………………………………….. 2,600

24. The required disclosures at the statement of financial position date are future payments for sinking

fund requirements and the maturity amounts of long-term debt during each of the next five years.

LO: 4, Bloom: K, Difficulty: Simple, Time: 3-5, AACSB: None, AICPA BB: None, AICPA FC: Reporting, AICPA PC: Communication

25. Off-balance-sheet financing is an attempt to borrow monies in such a way that the obligations are

not recorded. Reasons for off-balance-sheet financing are:

Questions Chapter 14 (Continued)

26. Forms of off-balance-sheet financing include (1) investments in non-consolidated subsidiaries for

27. Under IFRS, a parent company does not have to consolidate a subsidiary company that is less

than 50 percent owned. In such cases, the parent therefore does not report the assets and

liabilities of the subsidiary. All the parent reports on its statement of financial position is the

investment in the subsidiary. As a result, users of the financial statements may not understand

that the subsidiary has considerable debt for which the parent may ultimately be liable if the

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 14.1

Present value of the principal

¥500,000 X .37689 …………………………………………………

Present value of the interest payments

¥22,500 X 12.46221 ……………………………………………….

BRIEF EXERCISE 14.2

(a)

Cash ………………………………………………………………………

300,000

Bonds Payable ……………………………………………….

300,000

(b)

Interest Expense …………………………………………………….

Cash (€300,000 X 10% X 6/12) ………………………….

(c)

Interest Expense …………………………………………………….

Interest Payable ……………………………………………..

BRIEF EXERCISE 14.3

(a)

Cash (€300,000 X 1.0811) …………………………………………

324,330

Bonds Payable ……………………………………………….

324,330

(b)

Interest Expense (€324,330 X 8% X 6/12)…………………..

Bonds Payable (€15,000 – €12,973) …………………………..

Cash (€300,000 X 10% X 6/12) ………………………….

Bonds Payable ……………………………………………………….

BRIEF EXERCISE 14.4

(a)

Cash (€300,000 X .926393)………………………………………..

277,918

Bonds Payable ………………………………………………..

277,918

(b)

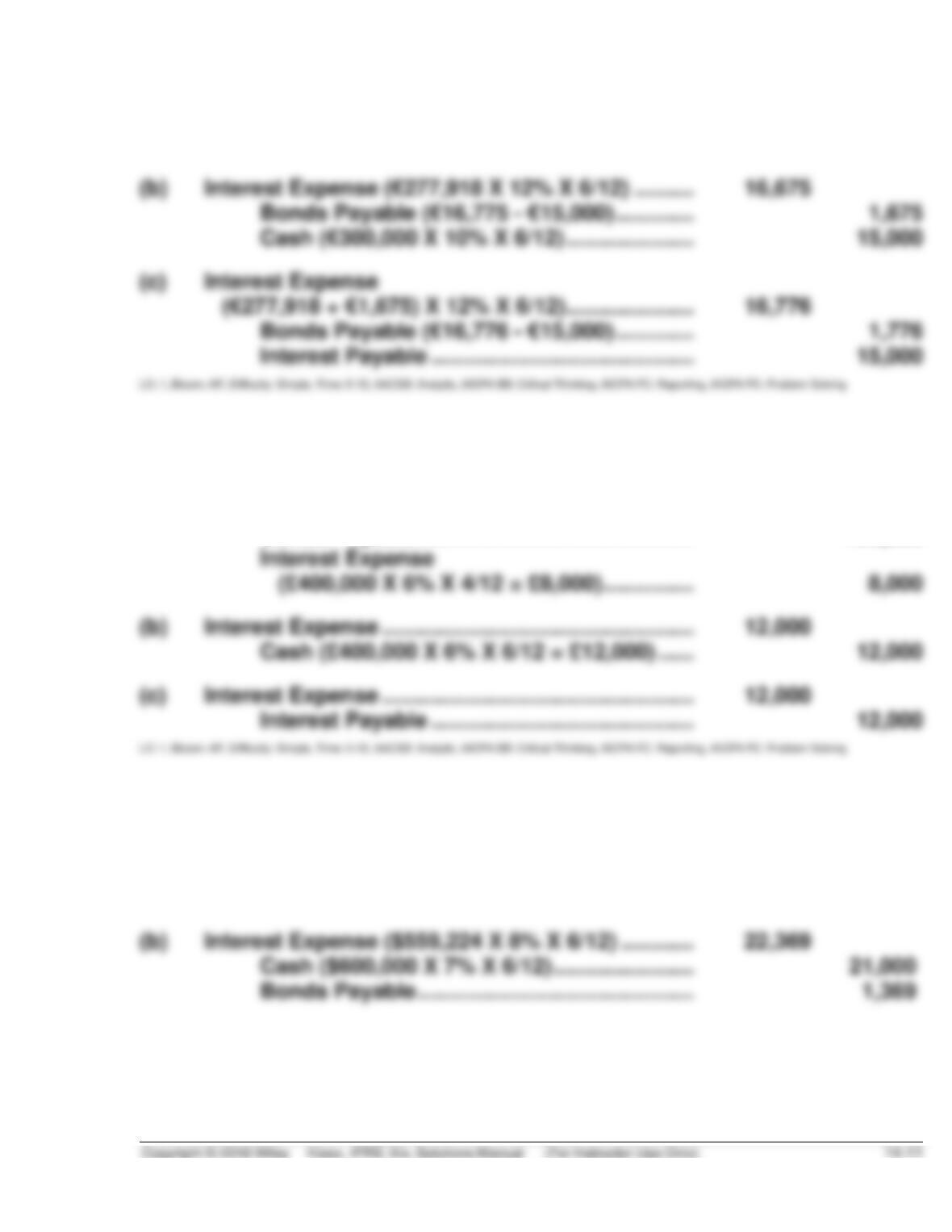

Interest Expense (€277,918 X 12% X 6/12) …………………

Bonds Payable (€16,775 – €15,000) ……………………

Cash (€300,000 X 10% X 6/12) …………………………..

Bonds Payable (€16,776 – €15,000) ……………………

Interest Payable ………………………………………………

BRIEF EXERCISE 14.5

(a)

Cash (£400,000 + £8,000) ………………………………………….

408,000

Bonds Payable ………………………………………………..

400,000

Interest Expense

(£400,000 X 6% X 4/12 = £8,000) ……………………..

(b)

Interest Expense ……………………………………………………..

Cash (£400,000 X 6% X 6/12 = £12,000) ……………..

(c)

Interest Expense ……………………………………………………..

Interest Payable ………………………………………………

BRIEF EXERCISE 14.6

(a)

Cash ……………………………………………………………………….

559,224

Bonds Payable ………………………………………………..

559,224

(b)

Interest Expense ($559,224 X 8% X 6/12) …………………..

Cash ($600,000 X 7% X 6/12) …………………………..

Bonds Payable ………………………………………………..

BRIEF EXERCISE 14.6 (Continued)

(c)

Interest Expense *

[($560,593 X 8% X 6/12 = $22,424)] …………………………

22,424

Interest Payable ……………………………………………..

Bonds Payable ……………………………………………….

BRIEF EXERCISE 14.7

(a)

Cash ……………………………………………………….

644,636

Bonds Payable ……………………………………………….

644,636

(b)

Interest Expense ($644,636 X 6% X 6/12)…………………..

Bonds Payable ……………………………………………………….

Cash ($600,000 X 7% X 6/12) …………………………..

(c)

Interest Expense

($642,975 X 6% X 6/12 = $19,289) …………………………..

Bonds Payable ……………………………………………………….

Interest Payable ……………………………………………..

BRIEF EXERCISE 14.8

Interest Expense ……………………………………………………..

6,446,360*

Bonds Payable (HK$7,000,000 – HK$6,446,360) …………

553,640

Interest Payable ………………………………………………

7,000,000**

*HK$644,636,000 X 6% X 2/12 = HK$6,446,360

**HK$600,000,000 X 7% X 2/12 = HK$7,000,000

BRIEF EXERCISE 14.9

(a)

Cash ……………………………………………………………………….

100,000

Notes Payable …………………………………………………

100,000

(b)

Interest Expense ……………………………………………………..

Cash (€100,000 X 10% = €10,000) ……………………..

10,000

BRIEF EXERCISE 14.10

(a)

Cash ……………………………………………………………………….

47,664

Notes Payable …………………………………………………

47,664

(b)

Notes Payable …………………………………………………

BRIEF EXERCISE 14.11

(a)

Equipment ……………………………………………………….

31,495

Notes Payable …………………………………………………

31,495

(b)

Interest Expense ($31,495 X 12%)…………………………..

Cash ($40,000 X 5%) ………………………………………..

Notes Payable ($3,779 – $2,000) ………………………..

BRIEF EXERCISE 14.12

Cash ………………………………………………………………………

60,000

Notes Payable [€60,000 X .63552 (PVF4, 12%)] ……..

38,131

Unearned Sales Revenue (€60,000 – €38,131) …

21,869

BRIEF EXERCISE 14.13

Bonds Payable ($500,000 + $15,000) …………………………

515,000

Gain on Extinguishment of Debt ………………………

Cash (.99 X $500,000) ………………………………………

495,000

BRIEF EXERCISE 14.14

Notes Payable …………………………………………………………

100,000

Share Capital—Ordinary ………………………………….

20,000

(€4.75 – €1) X 20,000 …………………………………….

75,000

[€100,000 – (€20,000 + €75,000)] …………………..

BRIEF EXERCISE 14.15

(a)

Present value of restructured cash flows:

Present value of principal €90,000 due in

4 years at 12% [(€90,000 X .63552 (PVF4, 12%)] …………

Present value of interest €7,200 paid annually

for 4 years at 12% (€7,200 X 3.03735) …………………….

Fair value of note ……………………………………………………

Notes Payable (Old) ………………………………………………..

100,000

Gain on Extinguishment of Debt ………………………

Notes Payable (New) ……………………………………….

(b)

Interest Expense (€79,066 X 12%) …………………………..

9,488

Cash (€90,000 X 8%) ……………………………………….

Notes Payable ………………………………………………..

BRIEF EXERCISE 14.16

(a)

Unrealized loss = HK$17,500 – HK$16,000 = HK$1,500

(b)

Unrealized Holding Gain or Loss—Income ………………..

Notes Payable …………………………………………………

BRIEF EXERCISE 14.17

Non-current liabilities

Bonds Payable, due January 1, 2027 ………………..

Current liabilities

Interest Payable ………………………………………………

SOLUTIONS TO EXERCISES

EXERCISE 14.1 (15–20 minutes)

(a) Current liability if current assets are used to satisfy the debt.

(b) Current liability, €250,000; non-current liability, €750,000.

(c) Current liability.

EXERCISE 14.2 (15–20 minutes)

(a) Interest expense (credit balance)—Reclassify to interest payable on

statement of financial position.

(b) Bond issue costs—Reduction of the issue amount of the bond payable.

EXERCISE 14.3 (15–20 minutes)

1.

Divac SA:

(a)

1/1/19

Cash ……………………………………………………….

300,000

Bonds Payable …………………………..

300,000

(b)

7/1/19

Interest Expense

(€300,000 X 9% X 3/12) …………………………..

Cash ……………………………………………………….

(€300,000 X 9% X 3/12) …………………………..

Interest Payable …………………………..

2.

Verbitsky AG:

(a)

6/1/19

Cash ……………………………………………………….

210,000

Bonds Payable …………………………..

200,000

Interest Expense

(€200,000 X 12% X 5/12) …………………………..

(b)

7/1/19

Interest Expense …………………………..

Cash (€200,000 X 12% X 6/12) ………………………….

(c)

12/31/19

Interest Expense …………………………..

Interest Payable …………………………..

EXERCISE 14.4 (15–20 minutes)

(a)

1/1/19

Cash (€800,000 X 1.19792) …………………………..

958,336

Bonds Payable ……………………………………………….

958,336

(b)

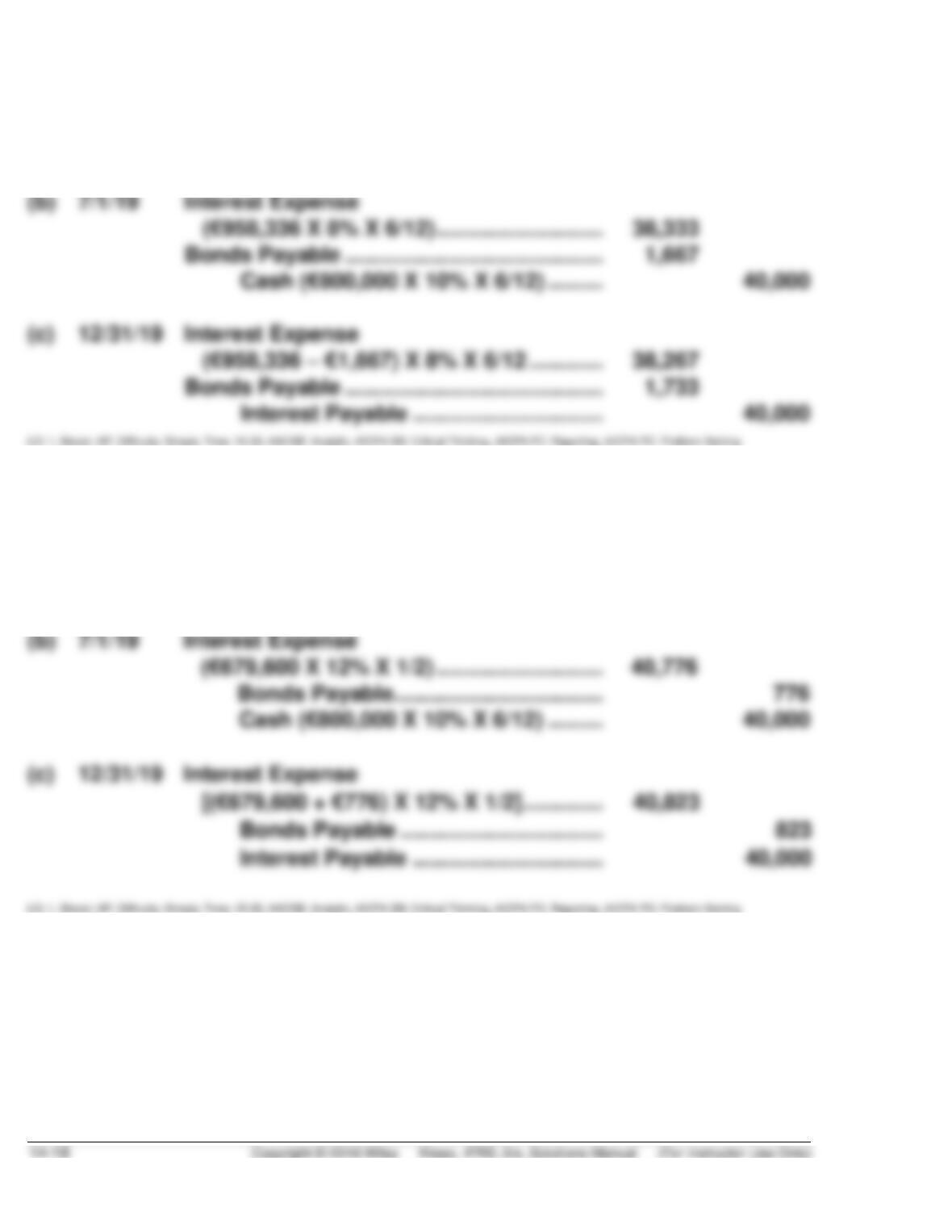

7/1/19

Interest Expense

(€958,336 X 8% X 6/12) …………………………..

Bonds Payable ……………………………………………………….

Cash (€800,000 X 10% X 6/12) ………………………….

(c)

12/31/19

Interest Expense

(€958,336 – €1,667) X 8% X 6/12 …………………………..

Bonds Payable ……………………………………………………….

Interest Payable …………………………..

EXERCISE 14.5 (15–20 minutes)

(a)

1/1/19

Cash (€800,000 X .8495) …………………………..

679,600

Bonds Payable ……………………………………………….

679,600

(b)

7/1/19

Interest Expense

(€679,600 X 12% X 1/2) …………………………..

Bonds Payable ………………………………………………..

Cash (€800,000 X 10% X 6/12) ………………………….

EXERCISE 14.6 (15–20 minutes)

The effective-interest or yield rate is 12%. It is determined through trial and

error using Table 6-2 for the discounted value of the principal [(£1,702,290 =

Schedule of Discount Amortization

Effective-Interest Method (12%)

Year

Cash

Paid

Interest

Expense

(@12%)

Discount

Amortized

(3 – 2)

Carrying

Amount of

Bonds

(1)

(2)

(3)

(4)

Jan. 1, 2019

—

—

—

£2,783,724.00

Dec. 31, 2019

£300,000

£334,046.88

*

£34,046.88

2,817,770.88

Dec. 31, 2019

2,855,903.39

Dec. 31, 2021

2,898,611.80

Dec. 31, 2022

2,946,445.22

Dec. 31, 2023

3,000,000.00

EXERCISE 14.7 (15–20 minutes)

(a)

Bond selling price ($2,500,000 X 1.06231) ……………………

$ 2,655,775

July 1, 2019

Interest expense reported ($2,655,775 X 10% X 6/12) ……

$ 132,789

$265,342

(b)

June 30, 2019

Carrying amount of bonds ………………………………………….

$562,500

Effective-interest rate for the period from June 30

to October 31, 2019 (.10 X 4/12) ………………………………..

X.033333

(c)

October 1, 2019

Cash ($853,382 + $72,000) ………………………………………….

925,382

Bonds payable …………………………………………………..

853,382

Interest Expense ($800,000 X 12% X 9/12) ……………

72,000