PROBLEM 3.7 (Continued)

(c) 1. Total depreciable cost = €8,750 X 6 = €52,500.

PROBLEM 3.8

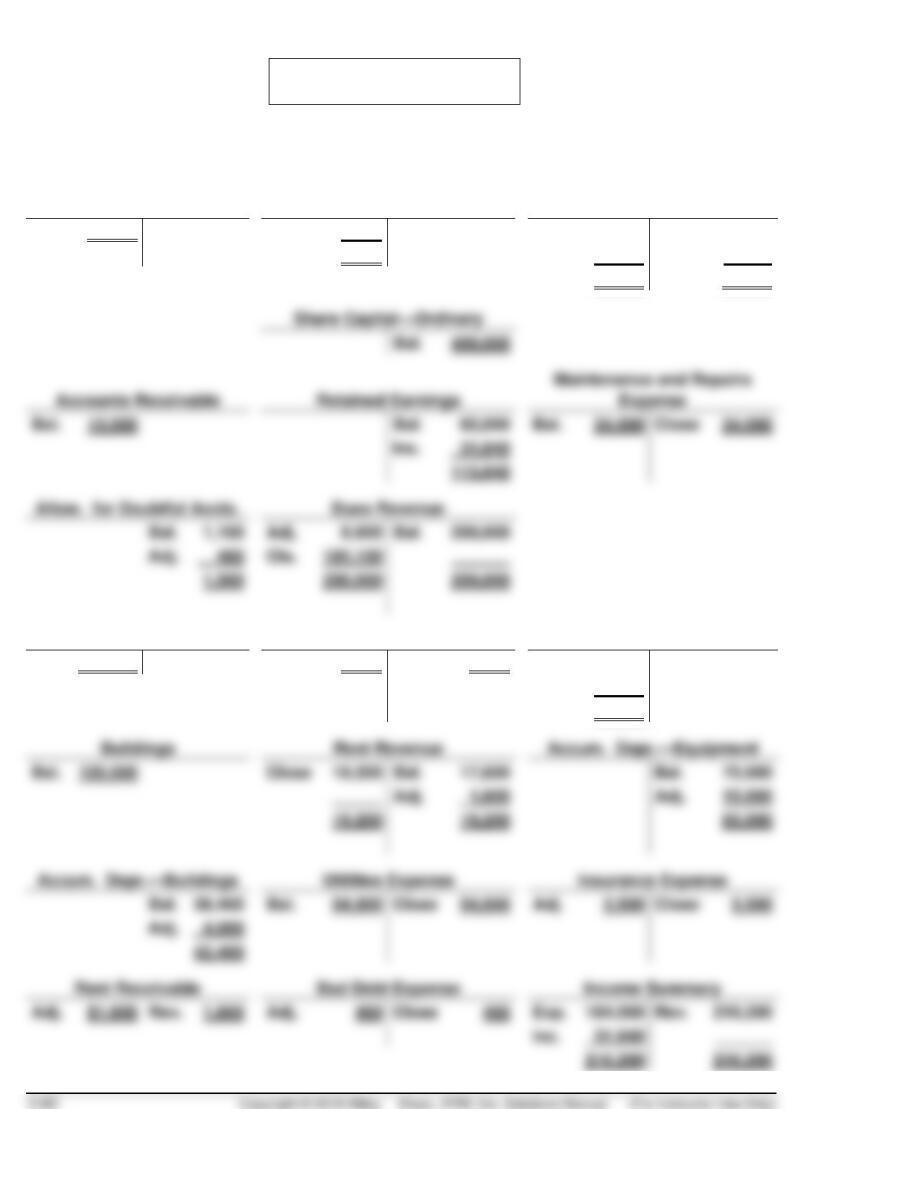

(a), (b), (d)

Cash

Prepaid Insurance

Salaries and Wages Expense

Bal.

15,000

Bal.

9,000

Adj.

3,500

Bal.

80,000

Close

83,600

5,500

Adj.

3,600

83,600

83,600

Bal.

Bal.

13,000

Bal.

82,000

Bal.

24,000

Close

24,000

Inc.

Bal.

1,100

Adj.

8,900

Bal.

Adj.

Cls.

191,100

1,560

200,000

Land

Green Fees Revenue

Depr. Expense

Bal.

350,000

Close

5,900

Bal.

5,900

Adj.

4,000

Close

19,000

Adj.

15,000

19,000

Bal.

Close

Bal.

17,600

Bal.

70,000

Adj.

1,600

Adj.

15,000

19,200

85,000

Bal.

Bal.

Close

54,000

Adj.

3,500

Close

3,500

Adj.

Bad Debt Expense

Adj.

Rev.

1,600

Adj.

Close

Exp.

Rev.

PROBLEM 3.8 (Continued)

Salaries and Wages Payable

Unearned Dues Revenue

Bal.

(b)

-1-

Depreciation Expense ……………………………………………………….

4,000

Accumulated Depreciation—Buildings

(1/30 X £120,000) ……………………………………………………….

4,000

-2-

Depreciation Expense ……………………………………………………….

15,000

Accumulated Depreciation—Equipment

(10% X £150,000) ……………………………………………………….

15,000

-3-

Insurance Expense ……………………………………………………….

3,500

Prepaid Insurance ……………………………………………………….

3,500

-4-

Rent Receivable ……………………………………………………….

Rent Revenue

(1/11 X £17,600) ……………………………………………………….

-5-

Bad Debt Expense ……………………………………………………….

460

Allowance for Doubtful Accounts

[(£13,000 X 12%) – £1,100] …………………………..

460

-6-

Salaries and Wages Expense …………………………..

3,600

Salaries and Wages Payable …………………………..

-7-

Dues Revenue ……………………………………………………….

8,900

Unearned Dues Revenue …………………………..

8,900

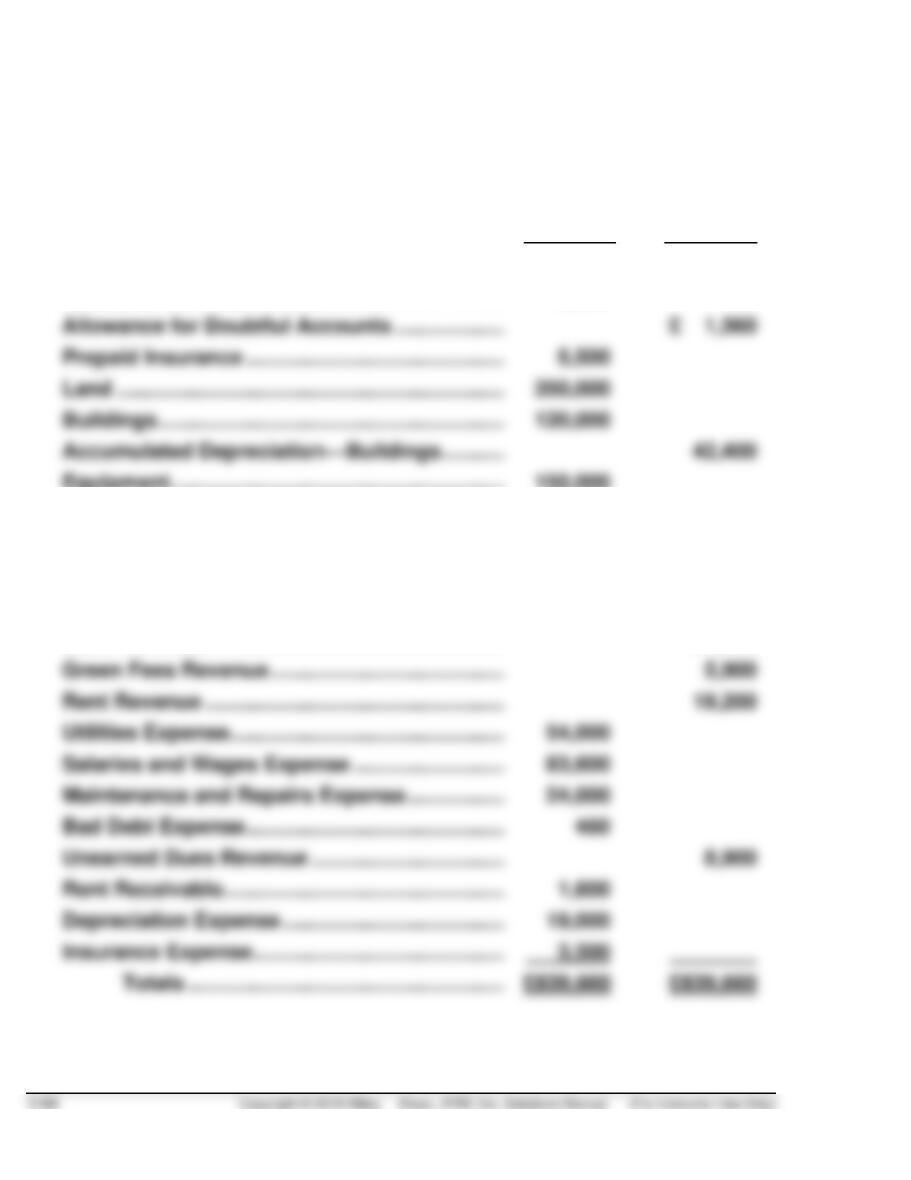

*PROBLEM 3.8 (Continued)

(c) KO GOLF CLUB, INC.

Adjusted Trial Balance

December 31, XXXX

Dr.

Cr.

Cash ……………………………………………………………………

£ 15,000

Accounts Receivable ……………………………………………

13,000

Allowance for Doubtful Accounts ………………………….

Land ……………………………………………………………………

350,000

Buildings ……………………………………………………….

120,000

Accumulated Depreciation—Buildings …………………..

Equipment ……………………………………………………….

150,000

Accumulated Depreciation—Equipment ………………..

85,000

Salaries and Wages Payable …………………………..

3,600

Share Capital—Ordinary ……………………………………….

400,000

Retained Earnings ………………………………………………..

82,000

Dues Revenue………………………………………………………

191,100

Green Fees Revenue …………………………………………….

5,900

Rent Revenue ………………………………………………………

19,200

Utilities Expense …………………………………………………..

54,000

Salaries and Wages Expense …………………………..

83,600

Maintenance and Repairs Expense ………………………..

24,000

Bad Debt Expense ………………………………………………..

Unearned Dues Revenue ………………………………………

8,900

Rent Receivable ……………………………………………………

Depreciation Expense …………………………………………..

19,000

Insurance Expense ……………………………………………….

*PROBLEM 3.8 (Continued)

(d)

December 31

Dues Revenues ……………………………………………………….

191,100

Green Fees Revenue …………………………..…………………………..

5,900

Rent Revenue ……………………………………………………….

Income Summary ……………………………………………………….

Income Summary ……………………………………………………….

184,560

Utilities Expense ……………………………………………………….

Bad Debt Expense ……………………………………………………….

Salaries and Wages Expense …………………………..

Maintenance and Repairs Expense …………………………..

Depreciation Expense ……………………………………………………….

Insurance Expense ……………………………………………………….

Income Summary (216,200 – 184,560) …………………………..

Retained Earnings ……………………………………………………….

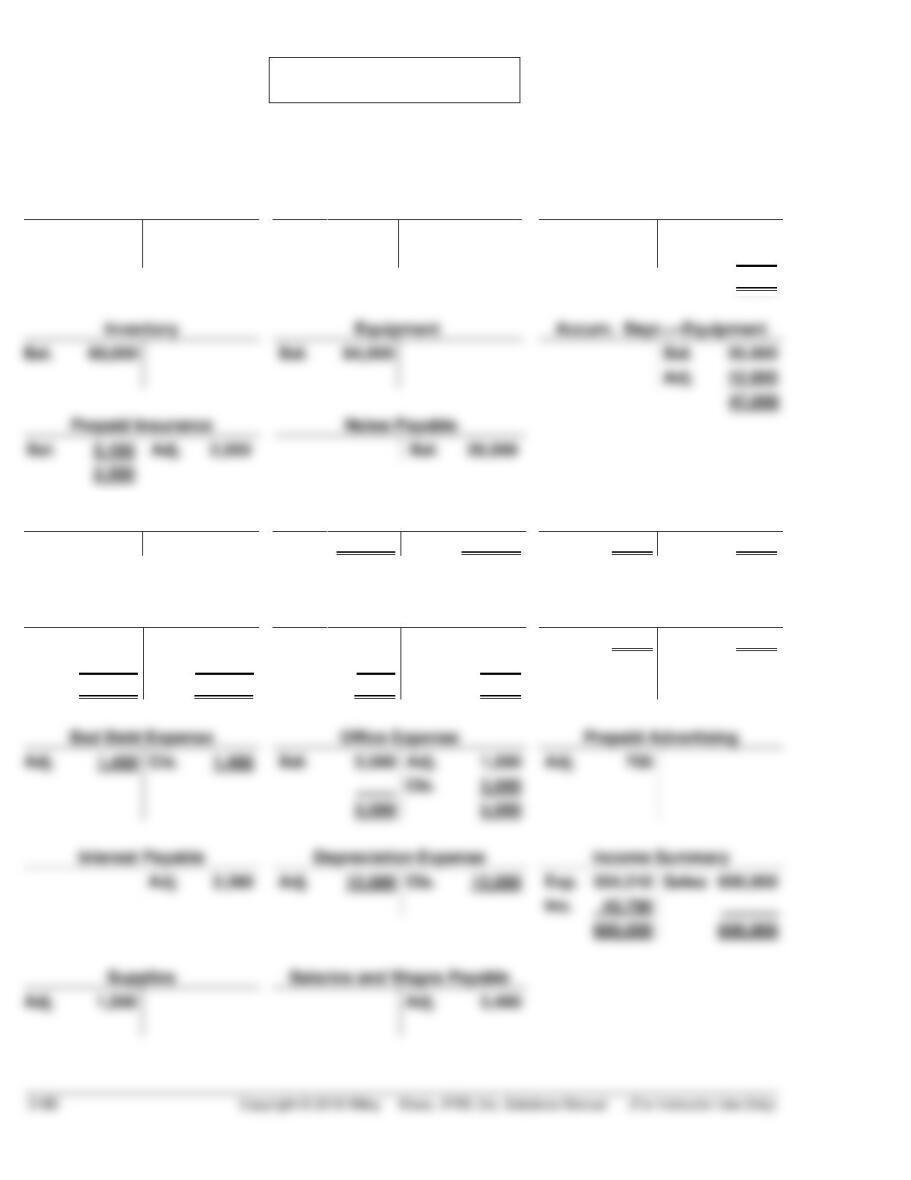

PROBLEM 3.9

(a), (b), (c)

Cash

Accounts Receivable

Allow. for Doubtful Accts.

Bal.

18,500

Bal.

32,000

Bal.

700

Adj.

1,400

2,100

Bal.

Bal.

Bal.

Adj.

12,000

47,000

Notes Payable

28,000

Share Capital—Ordinary

Sales Revenue

Insurance Expense

Bal.

80,600

Cls.

600,000

Bal.

600,000

Adj.

2,550

Cls.

2,550

Salaries and Wages

Expense

Advertising Expense

Interest Expense

Bal.

115,000

Cls.

117,400

Bal.

6,700

Adj.

700

Adj.

3,360

Cls.

3,360

Adj.

2,400

Cls.

6,000

117,400

117,400

6,700

6,700

Office Expense

Adj.

Cls.

Bal.

5,000

Adj.

1,500

Adj.

700

Cls.

3,500

5,000

5,000

Adj.

Adj.

Cls.

Exp.

554,210

Sales

600,000

Inc.

600,000

Adj.

Adj.

2,400

PROBLEM 3.9 (Continued)

(b)

-1-

Bad Debt Expense ……………………………………………………….

1,400

Allowance for Doubtful Accounts …………………………..

1,400

-2-

Depreciation Expense (€84,000 ÷ 7) …………………………..

Accumulated Depreciation—Equipment …………………………..

12,000

-3-

Insurance Expense ……………………………………………………….

Prepaid Insurance ……………………………………………………….

2,550

-4-

Interest Expense ……………………………………………………….

Interest Payable ……………………………………………………….

-5-

Salaries and Wages Expense …………………………..………………………

2,400

Salaries and Wages Payable …………………………..

2,400

-6-

Prepaid Advertising ……………………………………………………….

Advertising Expense ……………………………………………………….

-7-

Supplies …………………………………………………………………………………

Office Expense ……………………………………………………….

PROBLEM 3.9 (Continued)

(c)

Dec. 31

Sales Revenue ……………………………………………………….

600,000

Income Summary ……………………………………………………….

600,000

Dec. 31

Income Summary ……………………………………………………….

554,210

Cost of Goods Sold ……………………………………………………….

408,000

Advertising Expense …………………………..…………………………..

Salaries and Wages Expense …………………………..

Office Expense (€5,000 – €1,500) …………………………..

Insurance Expense ……………………………………………………….

Bad Debt Expense ……………………………………………………….

Depreciation Expense ……………………………………………………….

Interest Expense ……………………………………………………….

Dec. 31

Income Summary (€600,000 – €554,210) …………………………..

Retained Earnings ……………………………………………………….

*PROBLEM 3.10

(a) LAKELAND SALES AND SERVICE

Income Statement

For the Month Ended January 31, 2019

(1)

Cash Basis

(2)

Accrual Basis

Revenues ……………………………………………………….

£ 75,000

£98,400*

Expenses

Cost of computers & printers:

Purchased and paid …………………………..

Cost of goods sold …………………………..

Salaries and wages …………………………..

Rent ……………………………………………………….

Other operating expenses ……………………….

Total expenses …………………………..

106,500

*(£2,550 X 30) + (£3,600 X 4) + (£500 X 15) or (£75,000 + £23,400)

**(£1,500 X 40) + (£2,500 X 6) + (£300 X 25)

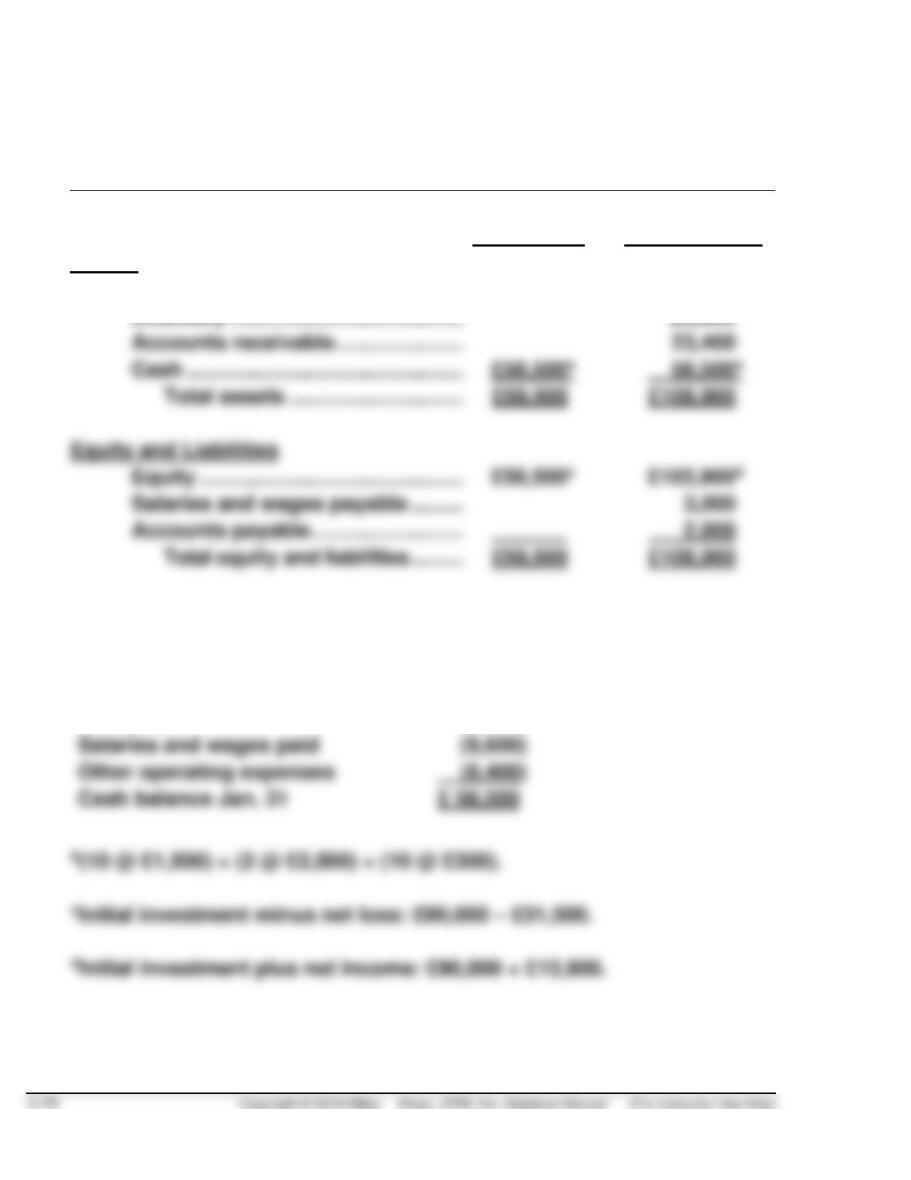

*PROBLEM 3.10 (Continued)

(b) LAKELAND SALES AND SERVICE

Statement of Financial Position

As of January 31, 2019

(1)

Cash Basis

(2)

Accrual Basis

Assets

Prepaid rent …………………………..……………….

£ 4,000

Inventory …………………………..……………………

Accounts receivable …………………………..

Cash ………………………………………………………

Total assets …………………………..

Equity and Liabilities

Equity …………………………………………………….

Salaries and wages payable …………………….

Accounts payable …………………………..

Total equity and liabilities …………………….

aOriginal investment £ 90,000

Cash sales 75,000

Cash purchases (82,500)

Rent paid (6,000)

*PROBLEM 3.10 (Continued)

(c) 1. The £23,400 in receivables from customers is an asset and a future

cash flow resulting from sales that is ignored. The cash basis

under states the amount of revenues and inflow of assets in

January from the sale of computers and printers by £23,400.

4. Rent expense on the cash basis is overstated by £4,000 under the

cash basis. This prepayment is an asset in the form of two

months’ future right to the use of office, showroom, and repair

space and should appear on the statement of financial position.

3-72 Copyright © 2018 Wiley Kieso, IFRS, 3/e, Solutions Manual (For Instructor Use Only)

16,900

21,000

6,000

16,900

21,000

6,000

(e)

Utilities Expense

Prop. Taxes Expense

Interest Payable

(a) COOKE NV

Worksheet

For the Year Ended September 30, 2019

Statement of

Financial

Position

Cr.

50,000

108,700

1,000

Dr.

37,400

14,000

Income

Statement

Cr.

280,500

Dr.

109,000

Adjusted Trial

Balance

Cr.

50,000

108,700

1,000

280,500

Dr.

37,400

14,000

109,000

Adjustments

Cr.

2,000

(d)

Dr.

Trial Balance

Cr.

50,000

108,700

1,000

278,500

Dr.

37,400

14,000

109,000

Account Titles

Cash

Mortgage Payable

Share capital-ordinary

Retained Earnings

Dividends

Service Revenue

Salaries and Wages Expense

Maintenance and Repairs

80,000

120,000

14,600

80,000

120,000

120,000

Land

Equipment

Accounts Payable