EXERCISE 8.11 (15–20 minutes)

(a)

1.

2,100 units available for sale – 1,400 units sold = 700 units in the

ending inventory.

500 @ $4.58 =

$2,290

920

2.

sale = $4.44 weighted-average unit cost.

cost.

$9,324 cost of goods available for sale ÷ 2,100 units available for

(b)

1.

FIFO will yield the highest gross profit because this method will

yield the lowest cost of goods sold figure in the situation

presented. The company has experienced rising purchase prices

2.

FIFO will yield the highest ending inventory because FIFO uses the

most recent purchase prices to cost the ending inventory units.

EXERCISE 8.12 (15–20 minutes)

First-in, first-out

Average cost

Sales ……………………………………….

€1,000,000

€1,000,000

Cost of goods sold:

Inventory, Jan. 1 …………………

€120,000

€120,000

Purchases ………………………….

Cost of goods available ………

Inventory, Dec. 31 ……………….

Cost of goods sold ………..

Gross profit ……………………………..

Operating expenses …………………

*Purchases

6,000 @ €22 =

€132,000

10,000 @ €25 =

7,000 @ €30 =

**Computation of inventory, Dec. 31:

First-in, first-out:

7,000 units @ €30 =

€210,000

2,000 units @ €25 =

***Average cost:

6,000 @ €20 =

€120,000

6,000 @ €22 =

7,000 @ €30 =

Average cost/unit = €712,000 ÷ 29,000 = €24.55 (rounded)

EXERCISE 8.13 (15–20 minutes)

(a)

Inventory December 31, 2019 (unadjusted) ………………

$234,890

Transaction 2 …………………………………………………………

10,420

Transaction 3 …………………………………………………………

–0–

Transaction 4 …………………………………………………………

–0–

Transaction 5 …………………………………………………………

Transaction 6 …………………………………………………………

Transaction 7 …………………………………………………………

Transaction 8 …………………………………………………………

1,500

(b)

Transaction 3

Sales ……………………………………………………..

12,800

Accounts Receivable …………………………..

12,800

(To reverse sale entry in 2019)

Transaction 4

Purchases (Inventory) …………………………….

15,630

Accounts Payable …………………………..

15,630

merchandise in 2019)

Transaction 8

Sales Returns and Allowances ………………..

Accounts Receivable ………………………

EXERCISE 8.14 (10–15 minutes)

Current Year

Subsequent Year

1.

Working capital

No effect

No effect

Current ratio

No effect

Retained earnings

No effect

No effect

Net income

No effect

No effect

2.

Working capital

Overstated

No effect

Current ratio

Overstated

No effect

Retained earnings

Overstated

No effect

Net income

Overstated

3.

Working capital

Overstated

No effect

Current ratio

Overstated

No effect

Retained earnings

Overstated

No effect

Net income

Overstated

EXERCISE 8.15 (10–15 minutes)

(c)

Event

Effect of Error

Adjust Income

Increase (Decrease)

1.

Understatement of ending

inventory

Decreases net income

€22,000

3.

Overstatement of ending

Increases net income

EXERCISE 8.16 (15–20 minutes)

Errors in Inventories

Year

Net

Income

Per Books

Add

Overstate-

ment Jan. 1

Deduct

Understate-

ment Jan. 1

Deduct

Overstate-

ment Dec. 31

Add

Understate-

ment Dec. 31

Corrected

Net Income

2015

HK$ 50,000

HK$5,000

HK$ 45,000

2016

52,000

HK$5,000

9,000

48,000

2017

54,000

9,000

74,000

2018

56,000

45,000

2019

58,000

60,000

2020

60,000

10,000

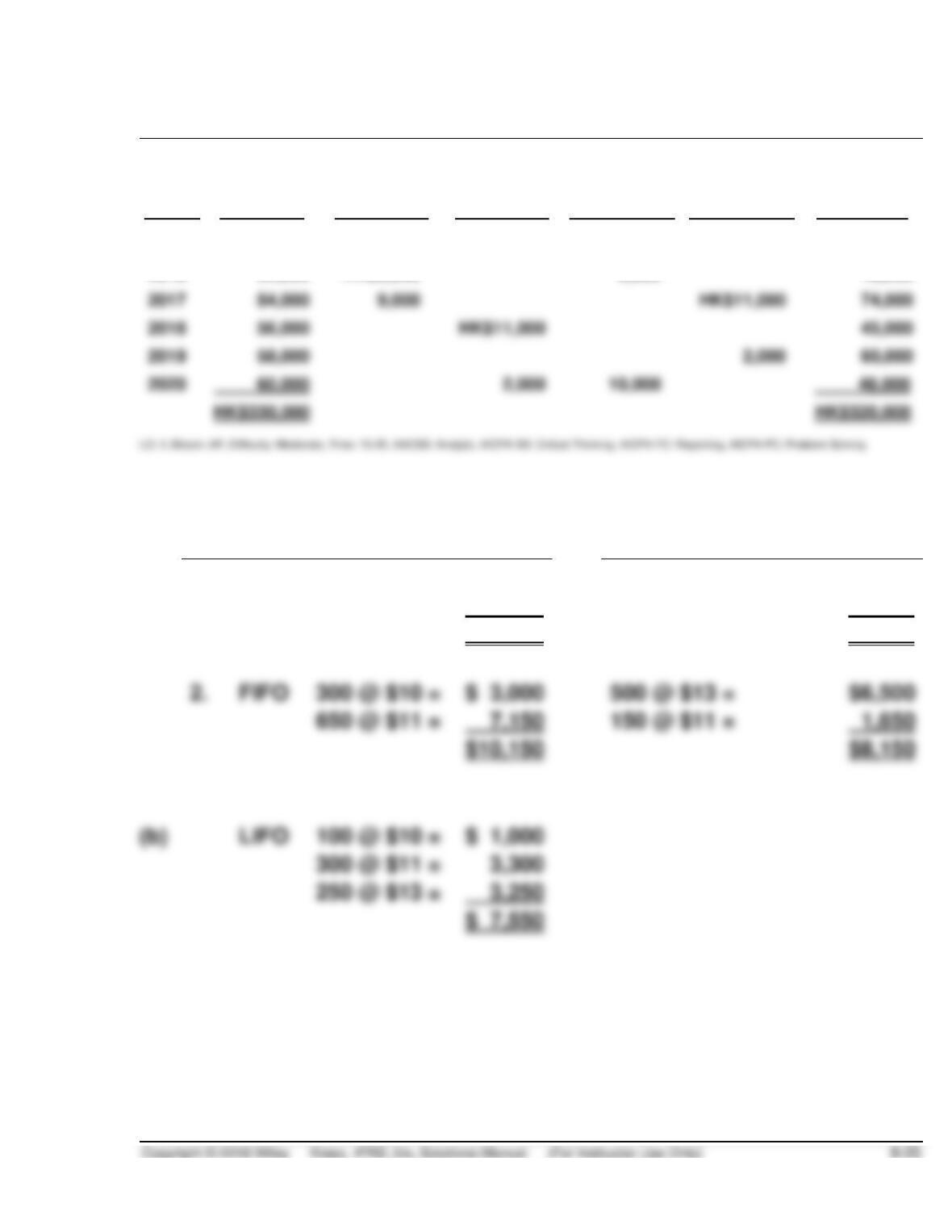

*EXERCISE 8.17 (15–20 minutes)

(a)

Cost of Goods Sold

Ending Inventory

1.

LIFO

500 @ $13 =

$ 6,500

300 @ $10 =

$3,000

450 @ $11 =

4,950

350 @ $11 =

3,850

$11,450

$6,850

2.

FIFO

300 @ $10 =

$ 3,000

500 @ $13 =

$6,500

650 @ $11 =

7,150

150 @ $11 =

1,650

(b)

LIFO

$ 1,000

300 @ $11 =

EXERCISE 8.17 (Continued)

(c)

Sales

$24,050

= ($24 X 200) + ($25 X 500) + ($27 X 250)

Cost of Goods Sold

Gross Profit (FIFO)

(d)

LIFO matches more current costs with revenue. When prices are rising

*EXERCISE 8.18 (20–25 minutes)

(a)

1.

LIFO

600 @ $6.00 =

$3,600

200 @ $6.08 =

1,216

$4,816

Total units

EXERCISE 8.18 (Continued)

*Units

Price

Total Cost

600

@

$6.00

=

$ 3,600

@

$6.08

=

800

@

$6.40

=

@

$6.50

=

700

@

$6.60

=

@

$6.79

=

3,395

(b)

1.

FIFO

500 @ $6.79 =

$3,395

300 @ $6.60 =

1,980

$5,375

2.

LIFO

100 @ $6.00 =

$ 600

200 @ $6.08 =

500 @ $6.79 =

3,395

(c)

Total merchandise available for sale

$33,655

Less inventory (FIFO)

5,375

*EXERCISE 8.19 (15–20 minutes)

(a) MILLS COMPANY

Computation of Inventory for Product Zone

Under FIFO Inventory Method

March 31, 2019

Units

Unit Cost

Total Cost

March 26, 2019 ………………………….

600

$12.00

$ 7,200

February 16, 2019 ……………………..

January 25, 2019 (portion) …………

1,000

(b) MILLS COMPANY

Computation of Inventory for Product Zone

Under LIFO Inventory Method

March 31, 2019

Units

Unit Cost

Total Cost

January 5, 2019 (portion) …………..

8,100

*EXERCISE 8.19 (Continued)

(c) MILLS COMPANY

Computation of Inventory for Product Zone

Under Weighted Average Inventory Method

March 31, 2019

Units

Unit Cost

Total Cost

Beginning inventory ………………….

600

$ 8.00

$ 4,800

January 5, 2019 ………………………..

1,100

9.00

9,900

January 25, 2019 ………………………

February 16, 2019 ……………………..

8,800

March 26, 2019 ………………………….

$43,700

Weighted-average cost

($43,700 ÷ 4,400) …………………….

$ 9.93*

March 31, 2019, inventory ………….

1,500

$ 9.93

*EXERCISE 8.20 (10–15 minutes)

(a)

(1)

400 @ $30 =

$12,000

110 @ $25 =

2,750

$14,750

(2)

400 @ $20 =

$ 8,000

110 @ $25 =

2,750

$10,750

(b)

(1)

FIFO

$14,750 [same as (a)]

(2)

LIFO

100 @ $20 =

400 @ $30 =

*EXERCISE 8.21 (15–20 minutes)

First-in, first-out

Last-in, first-out

Sales ……………………………………….

$1,000,000

$1,000,000

Cost of goods sold:

Inventory, Jan. 1 …………………

$120,000

$120,000

Purchases ………………………….

Cost of goods available ………

Inventory, Dec. 31 ……………….

Cost of goods sold ………..

Gross profit ……………………………..

Operating expenses …………………

*Purchases

6,000 @ $22 =

$132,000

10,000 @ $25 =

7,000 @ $30 =

**Computation of inventory, Dec. 31:

First-in, first-out:

$210,000

2,000 units @ $25 =

50,000

***Last-in, first-out:

6,000 units @ $20 =

$120,000

3,000 units @ $22 =

66,000

*EXERCISE 8.22 (20–25 minutes)

MICKIEWICZ CORPORATION

Schedules of Cost of Goods Sold

For the First Quarter Ended March 31, 2019

Schedule 1

First-in, First-out

Schedule 2 Last-in,

First-out

Beginning inventory ……………………

$ 40,000

$ 40,000

Plus purchases …………………………..

Cost of goods available for sale …..

Less ending inventory ………………..

65,700

61,000

Schedules Computing Ending Inventory

Units

Beginning inventory ……………………………………………………………..

10,000

Plus purchases …………………………………………………………………….

35,000

Units available for sale …………………………………………………………

45,000

Less sales ($150,000 ÷ 5) …………………………..………………………….

30,000

The unit computation is the same for both assumptions, but the cost as–

signed to the units of ending inventory are different.

First-in, First-out (Schedule 1)

Last-in, First-out (Schedule 2)

at $4.40 =

at $4.00 =

at $4.30 =

at $4.20 =

*EXERCISE 8.23 (10–15 minutes)

(a)

FIFO Ending Inventory 12/31/15

76 @ $10.89* =

$ 827.64

34 @ $11.88** =

403.92

(b)

LIFO Cost of Goods Sold—2015

76 @ $10.89 =

$ 827.64

90 @ $14.85* =

5 @ $15.84** =

79.20

(c) FIFO matches older costs with revenue. When prices are declining, as

in this case, this results in a higher amount for cost of goods sold.

TIME AND PURPOSE OF PROBLEMS

Problem 8.1 (Time 25–35 minutes)

Purpose—to provide a multipurpose problem with trade discounts, goods in transit, comparative FIFO

and average cost computations, and inventoriable cost identification.

Problem 8.2 (Time 25–35 minutes)

Problem 8.3 (Time 20–25 minutes)

Problem 8.4 (Time 30–40 minutes)

Purpose—to provide a problem where the student must compute the inventory using a FIFO, specific

Problem 8.5 (Time 25–35 minutes)

Purpose—to provide a problem where the student must compute the inventory using a FIFO and

Problem 8.6 (Time 20–25 minutes)

Purpose—to provide a problem where the student must compute cost of goods sold using FIFO and

average cost, under both a periodic and perpetual system.

*Problem 8.7 (Time 40–55 minutes)

Purpose—to provide a problem where the student must compute the inventory using a FIFO, LIFO, and

*Problem 8.8 (Time 40–55 minutes)

Purpose—to provide a problem where the student must compute the inventory using a FIFO, LIFO, and

be explained.

*Problem 8.9 (Time 25–35 minutes)

Purpose—to provide a problem where the student must compute cost of goods sold using FIFO, LIFO,

and weighted average, under both a periodic and perpetual system.

*Problem 8.10 (Time 30–40 minutes)

SOLUTIONS TO PROBLEMS

PROBLEM 8.1

1. €175,000 – (€175,000 X .20) = €140,000;

2. €1,100,000 + €69,000 = €1,169,000. The €69,000 of goods in transit on

3. Because no date was associated with the units issued or sold, the

periodic (rather than perpetual) inventory method must be assumed.

FIFO inventory cost:

1,000 units at €24

€ 24,000

1,000 units at 23

23,000

Average cost:

1,500 at €21

€ 31,500

2,000 at 22

3,500 at 23

1,000 at 24

24,000

PROBLEM 8.1 (Continued)

4. The inventoriable costs for 2019 are:

Merchandise purchased …………………………...

€909,400

Add: Freight-in ………………………………………..

Purchase discounts …………………….

PROBLEM 8.2

DIMITRI COMPANY

Schedule of Adjustments

December 31, 2019

Inventory

Accounts

Payable

Net Sales

Initial amounts

$1,520,000

$1,200,000

$8,150,000

Adjustments:

1.

NONE

NONE

(40,000)

2.

76,000

76,000

NONE

3.

30,000

NONE

NONE

4.

32,000

NONE

(47,000)

5.

26,000

NONE

NONE

6.

27,000

NONE

NONE

7.

NONE

56,000

NONE

8.

4,000

8,000

Total adjustments

195,000

140,000

(87,000)

1. The $31,000 of tools on the loading dock were properly included in the

2. The $76,000 of goods in transit from a vendor to Dimitri were shipped

f.o.b. shipping point on 12/29/19. Title passes to the buyer as soon as

3. The work-in-process inventory sent to an outside processor is Dimitri’s

PROBLEM 8.2 (Continued)

4. The tools costing $32,000 were recorded as sales ($47,000) in 2019.

However, these items were returned by customers on December 31, so

5. The $26,000 of Dimitri’s tools shipped to a customer f.o.b. destination

are still owned by Dimitri while in transit because title does not pass on

6. The goods received from a vendor at 5:00 p.m. on 12/31/19 should be

included in the ending inventory, but were not included in the physical

7. The $56,000 of goods received on 12/26/19 were properly included in

8. Since one-half of the freight-in cost ($8,000) pertains to merchandise

properly included in inventory as of 12/31/19, $4,000 should be added

PROBLEM 8.3

(a)

1.

8/10

Purchases ………………………………………………………

12,000

Accounts Payable……………………………………

12,000

8/13

Accounts Payable …………………………………………..

Purchase Returns and Allowances …………..

Purchases ………………………………………………………

16,000

Accounts Payable……………………………………

16,000

8/25

Purchases ………………………………………………………

20,000

Accounts Payable……………………………………

20,000

8/28

Accounts Payable …………………………………………..

16,000

2. Purchases—addition in cost of goods sold section of income

statement.

(b)

1.

8/10

Purchases ………………………………………………………

11,760

Accounts Payable (£12,000 X .98) …………….

11,760

8/13

Accounts Payable …………………………………………..

PROBLEM 8.3 (Continued)

8/15

Purchases ………………………………………………………

15,840

Accounts Payable (£16,000 X .99) …………….

15,840

8/25

Purchases ………………………………………………………

19,600

Accounts Payable (£20,000 X .98) …………….

19,600

Accounts Payable …………………………………………..

15,840

Purchase Discounts Lost ………………………………..

Cash ………………………………………………………

16,000

2.

8/31

Purchase Discounts Lost ………………………………..

216

Accounts Payable

(.02 X [£12,000 – £1,200]) ………………………

216

3.

Same as part (a) (2) except:

(c)

The second method is better theoretically because it results in the

inventory being carried net of purchase discounts, and purchase

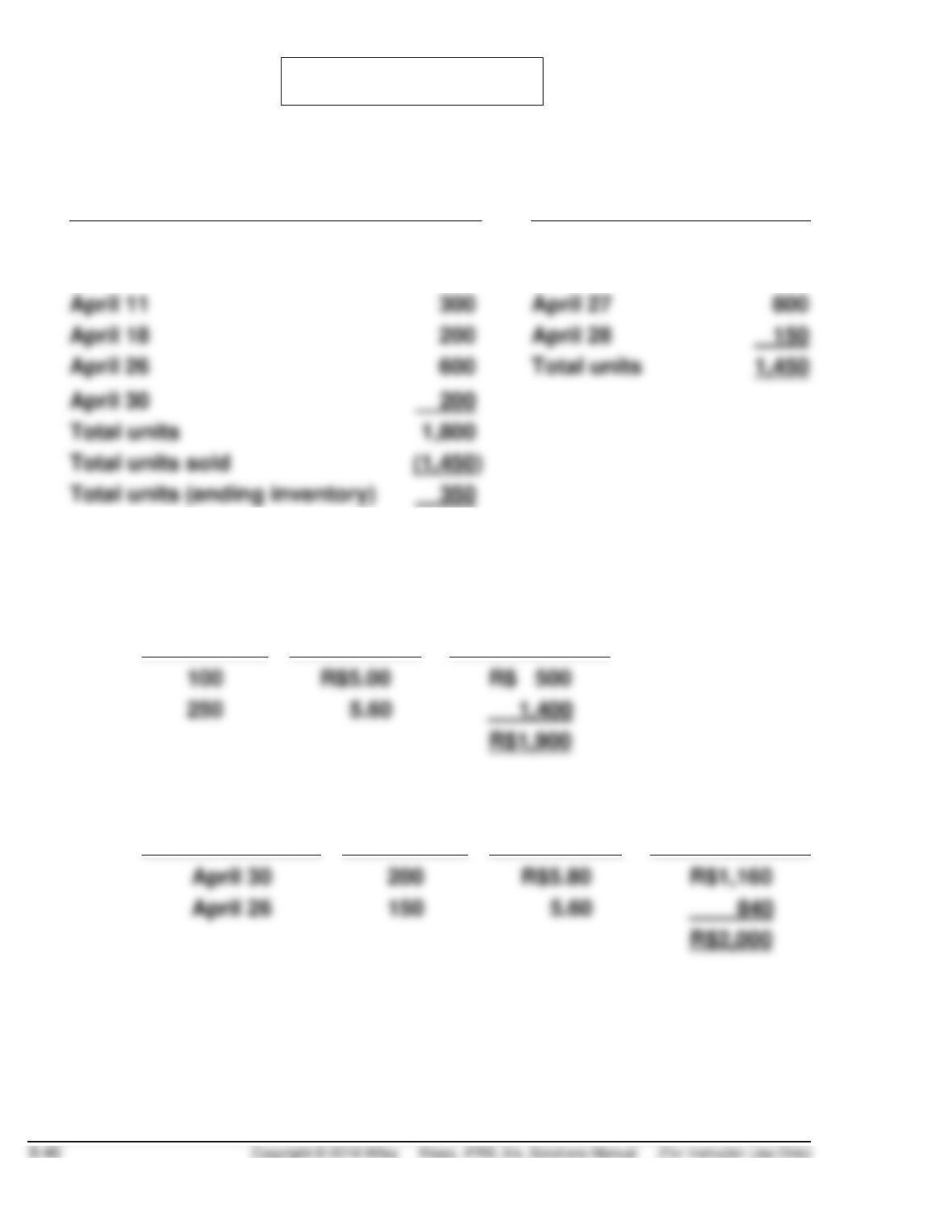

PROBLEM 8.4

(a)

Purchases

Total Units

Sales

Total Units

April 1 (balance on hand)

100

April 5

300

April 4

400

April 12

200

April 11

300

April 27

800

April 18

200

April 28

April 30

Total units

Total units sold

(1,450)

350

Assuming costs are not computed for each withdrawal:

1. Specific identification.

No. Units

Unit Cost

Total Cost

2. First-in, first-out.

Date of Invoice

No. Units

Unit Cost

Total Cost