CHAPTER 5

Statement of Financial Position and Statement of Cash Flows

ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC)

Topics

Questions

Brief

Exercises

Exercises

Problems

Concepts

for Analysis

1.

2.

Classification of items

in the statement of

financial position and

other financial

statements.

11, 12, 13,

14, 15, 16,

18, 19

1, 2, 3, 4, 5,

6, 7, 8, 9,

10, 11

1, 2, 3, 8,

9, 10

1, 2

Disclosure principles,

uses of the statement

1, 2, 3, 4, 5,

6, 7, 10, 18,

3, 4

3.

Preparation of

statement of financial

position; issues of

format, terminology,

and valuation.

4, 7, 8, 9,

16, 17, 20

4, 5, 6, 7,

11, 12, 17

1, 2, 3, 4,

5, 6, 7

2, 3, 4, 5

Statement of cash

flows.

21, 22, 23,

24, 25, 26,

27, 28

12, 13, 14,

15, 16

13, 14, 15,

16, 17, 18

6, 7

6

ASSIGNMENT CLASSIFICATION TABLE (BY LEARNING OBJECTIVE)

Learning Objectives

Questions

Brief

Exercises

Exercises

Problems

Concepts

for

Analysis

1. Explain the uses, usefulness

limitations, and content of the

statement of financial

position.

1, 2, 3, 4, 5,

6, 7, 8, 9,

11, 12, 13,

14, 15, 16,

17, 18, 19

1, 2, 3, 4, 5,

6, 7, 8, 9,

10, 11

1, 2, 3, 4, 5

6, 7, 8, 9,

10, 11, 12,

17

2, 3, 4, 5,

6, 7

2, 3

3. Explain the purpose, content,

and presentation of the

statement of cash flows.

21, 22, 23,

24, 25, 26,

27, 28

12, 13, 14,

15, 16

13, 14, 15,

16, 17, 18

6,7

4, 5, 6

of information provided.

29, 30

18

6, 7

ASSIGNMENT CHARACTERISTICS TABLE

Item

Description

Level of

Difficulty

Time

(minutes)

E5.1

Statement of financial position classifications.

Simple

15–20

E5.2

Classification of statement of financial position accounts.

Simple

15–20

E5.3

Classification of statement of financial position accounts.

Simple

15–20

E5.4

Preparation of a classified statement of financial position.

Simple

30–35

E5.5

Preparation of a corrected statement of financial position.

Simple

30–35

E5.6

Corrections of a statement of financial position.

30–35

E5.7

Current assets section of the statement of financial position.

Moderate

15–20

E5.8

Current vs. non-term liabilities.

Moderate

10–15

E5.9

Current assets and current liabilities.

30–35

E5.10

Current liabilities.

Moderate

15–20

E5.11

Statement of financial position preparation.

Moderate

25–30

E5.12

Preparation of a statement of financial position.

Moderate

30–35

E5.13

Statement of cash flows—classifications.

Moderate

15–20

E5.14

Preparation of a statement of cash flows.

Moderate

25–35

E5.15

Preparation of a statement of cash flows.

Moderate

25–35

E5.16

Preparation of a statement of cash flows.

Moderate

25–35

E5.17

Preparation of a statement of cash flows and a

statement of financial position.

30–35

E5.18

Preparation of a statement of cash flows, analysis.

Moderate

25–35

P5.1

Preparation of a classified statement of financial position,

periodic inventory.

Moderate

30–35

P5.2

Statement of financial position preparation.

Moderate

35–40

P5.3

Statement of financial position adjustment and preparation.

Moderate

40–45

P5.4

Preparation of a corrected statement of financial position.

40–45

P5.5

Statement of financial position adjustment and preparation.

40–50

P5.6

Preparation of a statement of cash flows and

a statement of financial position.

35–45

P5.7

Preparation of a statement of cash flows and

a statement of financial position.

40–50

CA5.1

Reporting the financial effects of varied transactions.

Moderate

20–25

CA5.2

Current asset and liability classification.

Moderate

20–25

CA5.3

Identifying statement of financial position deficiencies.

Moderate

20–25

CA5.5

Presentation of property, plant, and equipment.

Simple

20–25

CA5.6

Cash flow analysis.

40–50

ANSWERS TO QUESTIONS

1. The statement of financial position provides information about the nature and amounts of

investments in enterprise resources, obligations to enterprise creditors, and the owners’ equity in net

2. Solvency refers to the ability of an enterprise to pay its debts as they mature. For example, when a

company carries a high level of long-term debt relative to assets, it has lower solvency. Information

3. Financial flexibility is the ability of an enterprise to take effective actions to alter the amounts and

timing of cash flows so it can respond to unexpected needs and opportunities. An enterprise with a

4. Some situations in which estimates affect amounts reported in the statement of financial position

include:

(a) allowance for doubtful accounts.

(b) depreciable lives and estimated residual values for plant and equipment.

5. An increase in inventories increases current assets, which is in the numerator of the current ratio.

Therefore, inventory increases will increase the current ratio. In general, an increase in the current

ratio indicates a company has better liquidity, since there are more current assets relative to

6. Liquidity describes the amount of time that is expected to elapse until an asset is converted into

cash or until a liability has to be paid. The ranking of the assets given in order of liquidity is:

(1) (d) Short-term investments.

Questions Chapter 5 (Continued)

7. The major limitations of the statement of financial position are:

(a) The values stated are generally historical and not at fair value.

8. Some items of value to companies such as Louis Vitton or adidas are the value of research and

development (new products that are being developed but which are not yet marketable), the value

of the “intellectual capital” of its workforce (the ability of the companies’ employees to come up with

new ideas and products in the changing industries), and the value of the company reputation or

9. Classification in financial statements helps users by grouping items with similar characteristics and

separating items with different characteristics. Current assets are expected to be converted to

10. Separate amounts should be reported for accounts receivable and notes receivable. The amounts

should be reported gross, and an amount for the allowance for doubtful accounts should be

11. No. Non-trading equity securities should be reported as a current asset only if management

expects to convert them into cash as needed within one year or the operating cycle, whichever is

12. The relationship between current assets and current liabilities is that current liabilities are those

13. The total selling price of the season tickets is £20,000,000 (10,000 X £2,000). Of this amount,

£8,000,000 has been earned by 12/31/19 (8/20 X £20,000,000). The remaining £12,000,000

Questions Chapter 5 (Continued)

14. Working capital is the excess of total current assets over total current liabilities. This excess is

sometimes called net working capital. Working capital represents the net amount of a company’s

15. (a) Equity. “Treasury shares (at cost).”

Note: This is a reduction of total equity.

(b) Current Assets. Included in “Cash.”

(c) Investments. “Land held as an investment.”

16. (a) Allowance for doubtful accounts should be deducted from accounts receivable in current

assets.

(b) Inventory held on consignment should not appear on the consignee’s statement of financial

position except possibly as a note to the financial statements.

17. (a) Trade accounts receivable should be stated at their estimated amount collectible, often

referred to as net realizable value. The method most generally followed is to deduct from the

total accounts receivable the amount of the allowance for doubtful accounts.

Questions Chapter 5 (Continued)

18. Assets are defined as probable future economic benefits obtained or controlled by a particular

entity as a result of past transactions or events. If a building is leased under a finance or capital

19. Battle is incorrect. Retained earnings is a source of assets, but is not an asset itself. For example,

even though the funds obtained from issuing a note payable are invested in the business, the note

20. The notes should appear as non-current liabilities with full disclosure as to their terms. Each year,

as the profit is determined, notes of an amount equal to two-thirds of the year’s profits should be

21. The purpose of a statement of cash flows is to provide relevant information about the cash receipts

and cash payments of an enterprise during a period. It differs from the statement of financial

22. The difference between these two amounts may be due to increases in current assets (e.g., an

increase in accounts receivable from a sale on account would result in an increase in revenue and

23. The difference between these two amounts could be due to noncash charges that appear in the

income statement. Examples of noncash charges are depreciation, depletion, and amortization of

24. Operating activities involve the cash effects of transactions that enter into the determination of

net income. Investing activities include making and collecting loans and acquiring and disposing

Questions Chapter 5 (Continued)

25. (a) Net income is adjusted downward for the net increase in the accounts receivable (¥39,000 –

¥34,000) by deducting ¥5,000 from ¥90,000 and reporting net cash provided by operating

activities as ¥85,000.

(b) The issuance of the shares (10,000 x ¥115) is a financing activity. The issuance is reported

as follows:

26. The company appears to have good liquidity and reasonable financial flexibility. Its current cash

debt coverage is 1.20

€1,200,000

€1,000,000

, which indicates that it can pay off its current liabilities in a

27. Free cash flow = Net cash provided by operating activities – Capital expenditures – Dividends =

28. Free cash flow is net cash provided by operating activities less capital expenditures and dividends.

The purpose of free cash flow analysis is to determine the amount of discretionary cash flow a

29. A Summary of Significant Accounting Policies is usually the first note to the financial statements. It

Questions Chapter 5 (Continued)

30. Companies use two methods to disclose pertinent information in the statement of financial

SOLUTIONS TO BRIEF EXERCISES

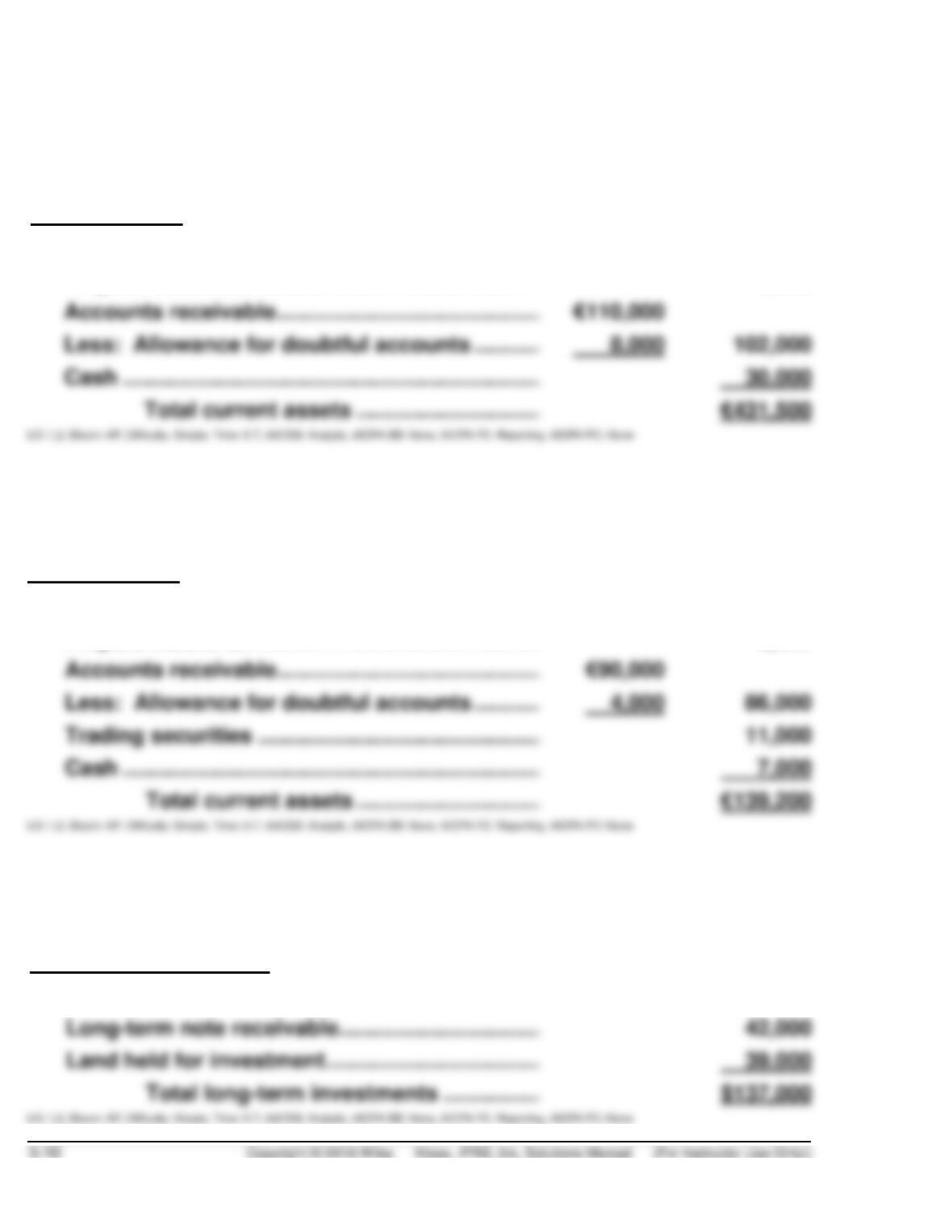

BRIEF EXERCISE 5.1

Current assets

Inventory …………………………..………………………….

€290,000

Prepaid insurance …………………………………………

9,500

Accounts receivable ………………………………………

Less: Allowance for doubtful accounts ………….

Cash …………………………………………………………….

30,000

BRIEF EXERCISE 5.2

Current assets

Inventory ………………………………………………………

€30,000

Prepaid insurance …………………………………………

5,200

Accounts receivable ………………………………………

Less: Allowance for doubtful accounts ………….

Trading securities …………………………………………

Cash …………………………………………………………….

7,000

BRIEF EXERCISE 5.3

Long-term investments

Held-for-collection securities …………………………..

$ 56,000

Long-term note receivable……………………………….

Land held for investment …………………………………

39,000

BRIEF EXERCISE 5.4

Property, plant, and equipment

Land ……………………………………………………….…..

$ 71,000

Buildings …………………………………………………….

Less: Accumulated depreciation-buildings …….

Equipment …………………………………………………..

Less: Accumulated depreciation-equipment …..

BRIEF EXERCISE 5.5

Intangible assets

Goodwill ………………………………………………………

£150,000

Patents ……………………………………………………….

Franchises …………………………………………………..

BRIEF EXERCISE 5.6

Intangible assets

Capitalized development costs ……………………..

$ 18,000

Goodwill ………………………………………………………

50,000

Franchises …………………………………………………..

47,000

Patents ……………………………………………………….

Trademarks …………………………………………………

10,000

BRIEF EXERCISE 5.7

Current liabilities

Notes payable ………………………………………………

$ 22,500

Accounts payable ………………………………………..

Salaries and wages payable ………………………….

Income taxes payable …………………………..………

Total current liabilities ……………………….

BRIEF EXERCISE 5.8

Current liabilities

Accounts payable ………………………………………..

₤220,000

Advances from customers …………………………..

41,000

Salaries and wages payable ………………………….

27,000

Interest payable ……………………………………………

12,000

Provision for warranties ……………………………….

Income taxes payable …………………………..………

Total current liabilities ……………………….

BRIEF EXERCISE 5.9

Non-current liabilities

Bonds payable ……………………………………………..

₤371,000

Pension liability ……………………………………………

Provision for warranties ……………………………….

Total non-current liabilities …………………

₤752,000

LO: 1,2, Bloom: AP, Difficulty: Simple, Time: 5-7, AACSB: Analytic, AICPA BB: None, AICPA FC: Reporting, AICPA PC: None

BRIEF EXERCISE 5.10

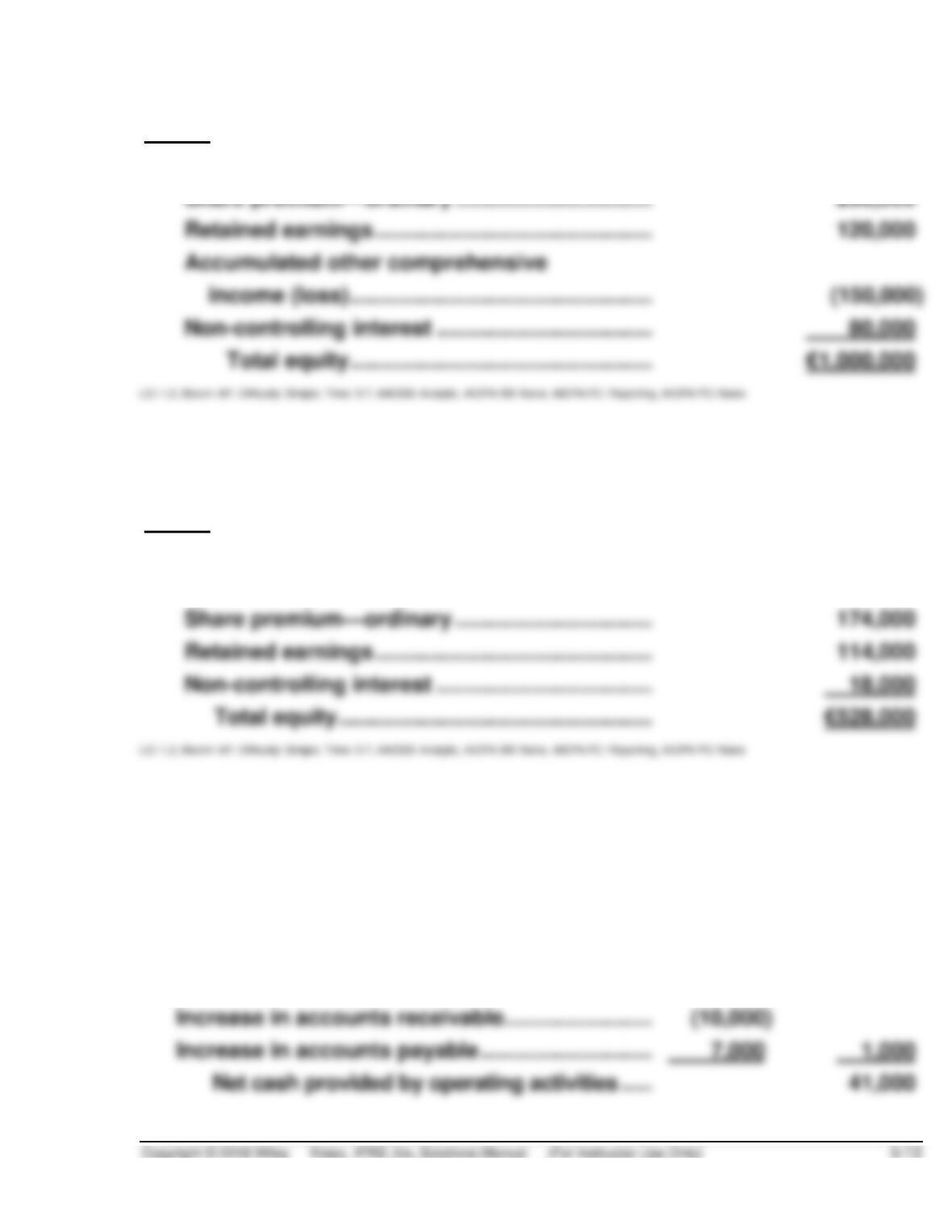

Equity

Share capital—ordinary ………………………………..

€ 750,000

Share premium—ordinary …………………………..

200,000

Retained earnings ………………………………………..

income (loss) ……………………………………………

Non-controlling interest ……………………………….

Total equity ……………………………………………

€1,000,000

BRIEF EXERCISE 5.11

Equity

Share capital—preference …………………………..

€152,000

Share capital—ordinary ………………………………..

70,000

Share premium—ordinary …………………………..

174,000

Retained earnings ………………………………………..

Non-controlling interest ……………………………….

Total equity ……………………………………………..

€528,000

BRIEF EXERCISE 5.12

Cash Flow Statement

Cash flows from operating activities

Net income ………………………………………………….

$40,000

Depreciation expense ………………………………….

$ 4,000

Increase in accounts receivable ……………………

Increase in accounts payable ……………………….

7,000

1,000

BRIEF EXERCISE 5.12 (Continued)

Cash flows from investing activities

Purchase of equipment ………………………………..

(8,000)

Cash flows from financing activities

Issue notes payable …………………………………….

Dividends paid …………………………………………….

Net cash provided by financing activities …

LO: 3, Bloom: AP, Difficulty: Simple, Time: 5-7, AACSB: Analytic, AICPA BB: None, AICPA FC: Reporting, AICPA PC: None

BRIEF EXERCISE 5.13

Cash flows from operating activities

Net income ………………………………………………….

HK$151,000

Depreciation expense ……………………………………….

HK$44,000

Increase in accounts receivable …………………………

Increase in accounts payable …………………………….

40,500

Adjustments to reconcile net income to net cash

BRIEF EXERCISE 5.14

Cash flows from investing activities

Sale of land and building …………………………………..

R$191,000

Purchase of land ………………………………………………

Purchase of equipment ……………………………………..

BRIEF EXERCISE 5.15

Cash flows from financing activities

Issuance of ordinary shares ………………………………

R$147,000

Purchase of treasury shares ……………………………..

(40,000)

Payment of cash dividend …………………………………

(95,000)

Retirement of bonds …………………………………………

BRIEF EXERCISE 5.16

Free Cash Flow Analysis

Net cash provided by operating activities …………..

R$400,000

Less: Purchase of equipment…………………………..

(53,000)

Purchase of land* …………………………………..

(37,000)

SOLUTIONS TO EXERCISES

EXERCISE 5.1 (15–20 minutes)

(a) If the investment in preference shares is readily marketable and held

(b) Treasury shares should be shown as a reduction of total equity.

(c) Equity.

EXERCISE 5.1 (Continued)

(j) Current asset.

EXERCISE 5.2 (15–20 minutes)

1.

(c)

11.

(c)

2.

(a) (3)

12.

(e)

3.

(e)

13.

(b)

4.

(e)

14.

(c)

5

(a) (2)

15.

(a) (2)

6.

(b)

16.

(a) (1)

7.

(e)

17.

(b)

8.

(a) (3)

18.

(b)

9.

(b)

19.

(d)

10.

(b)

20.

(e)

EXERCISE 5.3 (15–20 minutes)

1.

(e)

10.

(g)

2.

(a)

11.

(e)

3.

(g)

12.

(g)

4.

(e)

13.

(e)

5

(g)

14.

(k)

6.

(h)

15.

(g)

7.

(i)

16.

8.

(c)

17.

(b)

9.

(e)

EXERCISE 5.4 (30–35 minutes)

GULISTAN AG

Statement of Financial Position

December 31

Assets

Non-current assets

Long-term investments

Land held for future plant site ……………….

XXX

Cash restricted for plant expansion ……….

Total long-term investments ……….

€XXX

Long-term investment in

Property, plant, and equipment

Buildings ……………………………………………..

XXX

Less: Accum. depreciation—

buildings ………………………………

XXX

XXX

Intangible assets

Total non-current assets …………….

Current assets

Inventories

Finished goods ……………………………….

€XXX

Work in process ……………………………..

XXX

Raw materials …………………………………

XXX

XXX

Accounts receivable …………………………….

XXX

accounts …………………………..……….

Notes receivable (short-term) ………………..

XXX

Receivables—officers …………………………..

XXX

Cash ……………………………………………………

XXX

Less: Cash restricted for plant

EXERCISE 5.4 (Continued)

Equity and Liabilities

Equity

Share capital—ordinary ………………………………

€ XXX

Share premium—ordinary …………………………..

XXX

Retained earnings

Less: Treasury shares, at cost ……………………

XXX

Total equity ……………………………………..

Non-current liabilities

Bonds payable, due in four years ………………..

Long-term note payable ………………………………

Total non-current liabilities ……………….

Current liabilities

Notes payable, short-term …………………………..

XXX

Salaries and wages payable ………………………..

XXX

Unearned service revenue …………………………..

XXX

Unearned rent revenue ………………………………..

Total current liabilities ………………………

XXX

Total liabilities ………………………………….

Total Equity and liabilities ………………………………..

Note to instructor: An assumption made here is that cash included the

cash restricted for plant expansion. If it did not, then a subtraction from