EXERCISE 9.11 (5–10 minutes)

Unrealized Holding Gain or Loss—Income

EXERCISE 9.12 (15–20 minutes)

(a) If the commitment is material in amount, there should be a footnote in

the statement of financial position stating the nature and extent of the

(b) The drop in the market price of the commitment should be charged to

operations in the current year if it is material in amount. The following

entry would be made:

(c) Assuming the €12,000 market decline entry was made on December

31, 2019, as indicated in (b), the entry when the materials are received

in January 2020 would be:

EXERCISE 9.12 (Continued)

This entry records the raw materials at the current cost, eliminates the

EXERCISE 9.13 (8–13 minutes)

(1)

20%

= 16.67% OR 16 2/3%.

100% + 20%

(2)

25%

100% + 25%

(3)

(4)

50%

100% + 50%

EXERCISE 9.14 (10–15 minutes)

(a)

Inventory, May 1 (at cost) ………………………………..

€160,000

Purchases (at cost) …………………………………………

640,000

Purchase discounts ………………………………………..

(12,000)

Goods available (at cost) …………………………

Sales (at selling price) …………………………………….

Sales returns (at selling price) …………………………

Net sales (at selling price) ……………………………….

Less: Gross profit (25% of €930,000) ……………….

697,500

EXERCISE 9.14 (Continued)

(b) Gross profit as a percent of sales must be computed:

25%

= 20% of sales.

100% + 25%

Inventory, May 1 (at cost) …………………………..

€160,000

Purchases (at cost) ……………………………………

640,000

Purchase discounts …………………………………..

Freight-in ………………………………………………….

Goods available (at cost) ……………………

Sales (at selling price) ……………………………….

Sales returns (at selling price) ……………………

Net sales (at selling price) ………………………….

Less: Gross profit (20% of €930,000) ………….

186,000

744,000

EXERCISE 9.15 (15–20 minutes)

(a)

Merchandise on hand, January 1 ………………..

$ 38,000

Purchases …………………………………………………

92,000

Less: Purchase returns and allowances …….

(2,400)

Freight-in ………………………………………………….

3,400

Total merchandise available (at cost) ….

Cost of goods sold* …………………………………..

(90,000)

Ending inventory ……………………………………….

41,000

Less: Undamaged goods …………………………..

10,900

EXERCISE 9.15 (Continued)

(b)

Cost of goods sold = 66 2/3% of sales of $120,000 = $80,000

[$131,000 [as computed in (a)] – $80,000]

Less: Undamaged goods …………………………………………

Ending inventory (at cost) …………………………………………

$51,000

EXERCISE 9.16 (15–20 minutes)

Beginning inventory …………………………………………..

R$170,000

Purchases …………………………………………………………

450,000

620,000

Purchase returns ……………………………………………….

Goods available (at cost) ……………………………………

590,000

Sales …………………………………………………………………

Sales returns …………………………………………………….

Net sales …………………………………………………………..

Less: Gross profit (30% X R$626,000) ………………..

Estimated ending inventory (unadjusted for

damage) …………………………………………………………

151,800

Less: Goods on hand—undamaged (at cost)

R$21,000 X (1 – 30%) ………………………………..

Less: Goods on hand—damaged (at net

realizable value) ………………………………………

5,300

EXERCISE 9.17 (10–15 minutes)

Beginning inventory (at cost) ……………………………..

¥ 38,000

Purchases (at cost) ……………………………………………

90,000

Goods available (at cost) …………………………...

128,000

Sales (at selling price) ………………………………………..

¥116,000

Less sales returns ……………………………………………..

4,000

Net sales …………………………..………………………………

112,000

Less: Gross profit* (20% of ¥112,000) …………………

22,400

Net sales (at cost) ……………………………………

89,600

Estimated inventory (at cost) ……………………………..

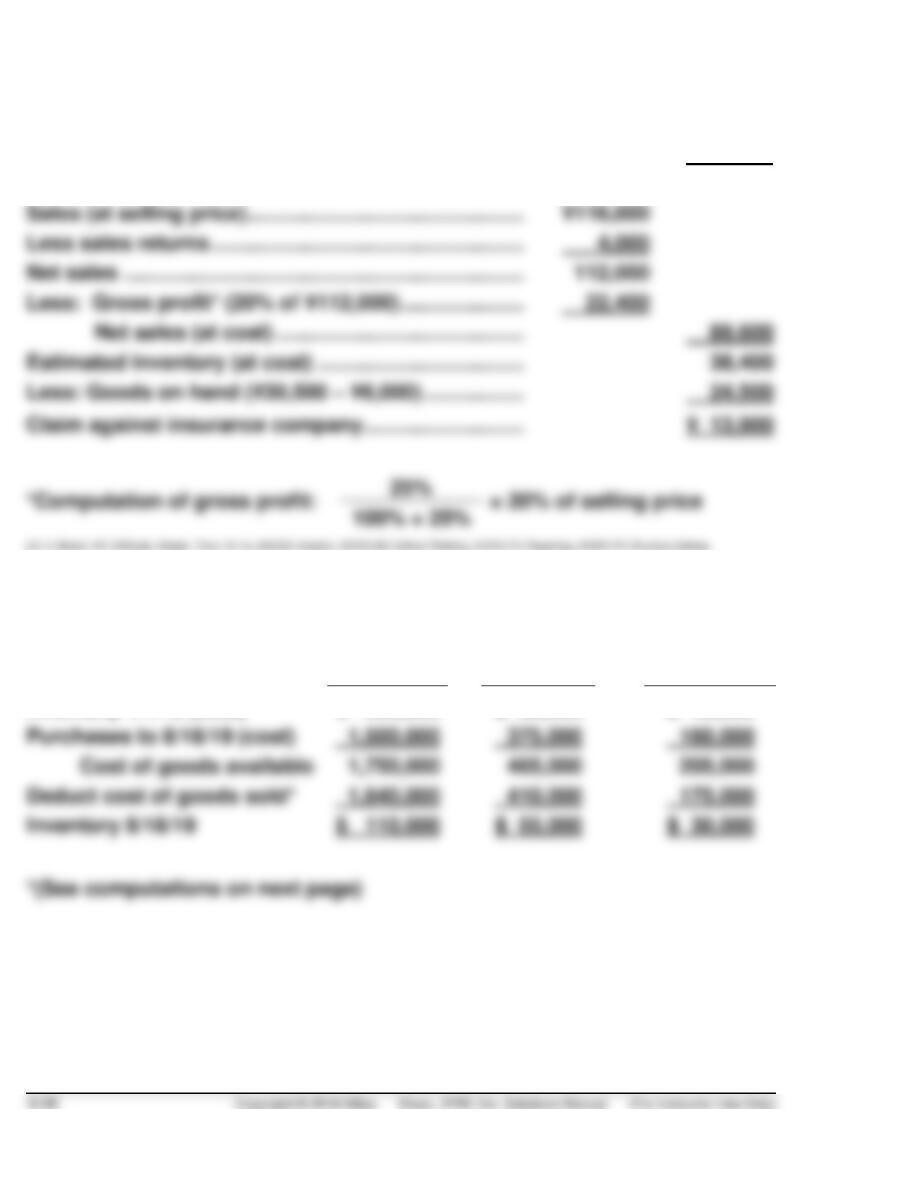

EXERCISE 9.18 (15–20 minutes)

Lumber

Millwork

Hardware

Inventory 1/1/19 (cost)

$ 250,000

$ 90,000

$ 45,000

Purchases to 8/18/19 (cost)

Cost of goods available

Deduct cost of goods sold*

Inventory 8/18/19

$ 110,000

$ 55,000

EXERCISE 9.18 (Continued)

Computation for cost of goods sold:*

*Alternative computation for cost of goods sold:

Markup on selling price: Cost of goods sold:

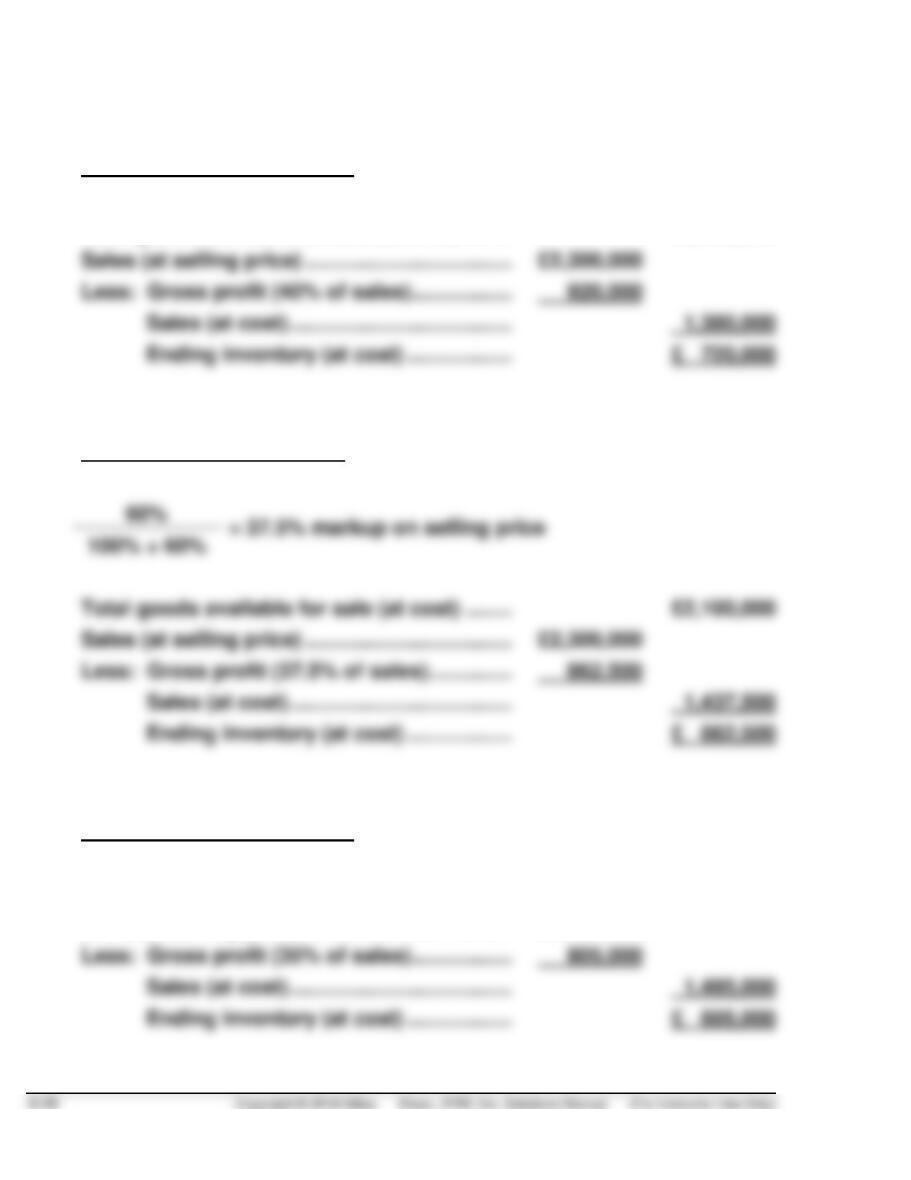

EXERCISE 9.19 (20–25 minutes)

Ending inventory:

(a)

Gross profit is 40% of sales

Total goods available for sale (at cost) ……..

£2,100,000

Sales (at selling price) ……………………………..

£2,300,000

Less: Gross profit (40% of sales) ……………..

920,000

(b)

Gross profit is 60% of cost

Total goods available for sale (at cost) ……..

£2,100,000

Sales (at selling price) ……………………………..

£2,300,000

Less: Gross profit (37.5% of sales) …………..

862,500

(c)

Gross profit is 35% of sales

Total goods available for sale (at cost) ……..

£2,100,000

Sales (at selling price) ……………………………..

£2,300,000

Less: Gross profit (35% of sales) ……………..

805,000

EXERCISE 9.19 (Continued)

(d)

Gross profit is 25% of cost

Total goods available for sale (at cost) ……..

Sales (at selling price) ……………………………..

Less: Gross profit (20% of sales) ……………..

EXERCISE 9.20 (20–25 minutes)

(a)

Cost

Retail

Beginning inventory…………………………………

R$ 58,000

R$100,000

Purchases ……………………………………………….

122,000

200,000

Net markups ……………………………………………

—

Totals ……………………………………………..

320,000

Net markdowns ……………………………………….

Sales price of goods available ………………….

290,000

Deduct: Sales …………………………………………

(b)

1.

R$180,000 ÷ R$300,000 = 60%

2.

3.

4.

EXERCISE 9.20 (Continued)

(c)

1.

Method 3.

2.

Method 3.

3.

Method 3.

EXERCISE 9.21 (12–17 minutes)

Cost

Retail

Beginning inventory …………………….

€ 200,000

€ 280,000

Purchases …………………………………..

1,425,000

2,140,000

Totals …………………………………

1,625,000

2,420,000

Add: Net markups

Markups …………………………….

Markup cancellations ………….

Deduct: Net markdowns

Markdowns …………………………

Markdown cancellations ………

Sales price of goods available ……..

2,470,000

Deduct: Sales ……………………………..

2,250,000

Cost-to-retail ratio =

€1,625,000

= 65%

€2,500,000

EXERCISE 9.22 (20–25 minutes)

Cost

Retail

Beginning inventory …………………………

£30,000

£ 46,500

Purchases ……………………………………….

55,000

88,000

Purchase returns ……………………………..

(3,000)

Freight on purchases ……………………….

2,400

Totals ……………………………………..

85,400

Add: Net markups

Markups …………………………………

£10,000

Markup cancellations ………………

(1,500)

Net markups ……………………………………

8,500

Deduct: Net markdowns

Markdowns ……………………………..

9,300

Markdown cancellations …………..

(2,800)

Net markdowns ……………………………….

6,500

Sales price of goods available ………….

Deduct: Net sales (£95,000 – £2,000) ….

93,000

EXERCISE 9.23 (10–15 minutes)

(a) Inventory turnover:

2015

TIME AND PURPOSE OF PROBLEMS

Problem 9.1 (Time 10–15 minutes)

Purpose—to provide the student with an understanding of the lower-of–cost-or–net realizable value

Problem 9.2 (Time 25–30 minutes)

Purpose—to provide the student with an understanding of the lower-of–cost-or-net realizable value

Problem 9.3 (Time 30–35 minutes)

Problem 9.4 (Time 15–20 minutes)

Purpose—to provide a problem that requires entries for recording the unrealized gains and losses on

biological assets and harvested assets.

Problem 9.5 (Time 20–30 minutes)

Problem 9.6 (Time 40–45 minutes)

Purpose—to provide the student with a complex problem involving a fire loss where the gross profit

Problem 9.7 (Time 20–30 minutes)

Purpose—to provide the student with a problem on the retail inventory method. The problem is relatively

straightforward although transfers-in from other departments as well as the proper treatment for normal

spoilage complicate the problem. A good problem that summarizes the essentials of the retail inventory

method.

Problem 9.8 (Time 20–30 minutes)

Purpose—to provide the student with a problem on the retail inventory method. This problem is similar

Problem 9.9 (Time 20–30 minutes)

Time and Purpose of Problems (Continued)

Problem 9.10 (Time 30–40 minutes)

Problem 9.11 (Time 30–40 minutes)

Purpose—to provide the student with an opportunity to write a memo explaining what is net realizable

SOLUTIONS TO PROBLEMS

PROBLEM 9.1

Item

Cost

Net

Realizable

Value*

Lower-of–

Cost-or–

NRV

A

€470

€ 450

€450

B

C

D

PROBLEM 9.2

(a) 1. The balance in the Allowance to Reduce Inventory to NRV at May

31, 2019, should be £15,200, as calculated in Exhibit 1 below.

Cost

NRV

LCNRV

Aluminum siding

£ 70,000

£ 56,000

£ 56,000

Cedar shake siding

86,000

84,800

Louvered glass doors

Thermal windows

2. For the fiscal year ended May 31, 2019, the gain that would be

recorded due to the change in the Allowance to Reduce Inventory

PROBLEM 9.2 (Continued)

(b) The use of the lower-of-cost-or-net realizable value (LCNRV) rule is

based on both the expense recognition principle and the concept of

PROBLEM 9.3

(a)

Cost-of-Goods-Sold Method

December 31, 2020

Cost of Goods Sold …………………………………………………

68,000

Allowance to Reduce Inventory to NRV ……………

($780,000 – $712,000)

December 31, 2021

Allowance to Reduce Inventory to NRV

[($905,000 – $830,000) – $68,000] …………………..

(b)

Loss Method

December 31, 2020

Loss Due to Decline of Inventory to NRV ………………….

68,000

Allowance to Reduce Inventory to NRV ……………

($780,000 – $712,000)

December 31, 2021

Loss Due to Decline of Inventory to NRV ………………….

Allowance to Reduce Inventory to NRV

[($905,000 – $830,000) – $68,000] …………………..

PROBLEM 9.4

(a)

Biological Assets—Grape Vineyard …………………..

15,000

Unrealized Holding Gain or Loss – Income …

15,000

(b)

Grape Inventory ……………………………………………….

30,000

Unrealized Holding Gain or Loss – Income …

30,000

(c)

Cash ……………………………………………………………….

35,000

Cost of Goods Sold ………………………………………….

30,000

Sales Revenue ………………………………………….

35,000

(d)

Unrealized Holding Gain or Loss – Income ………..

€15,000

Unrealized Holding Gain or Loss – Income ………..

30,000

Gross Profit on Sold Grapes …………………………….

5,000

Total Effect on Income ……………………………………..

€50,000

PROBLEM 9.5

Beginning inventory ……………………………………………..

¥ 80,000

Purchases ……………………………………………………………

290,000

370,000

Purchase returns ………………………………………………….

(28,000)

Total goods available ……………………………………………

342,000

Sales ……………………………………………………………………

Less: Gross profit (35% of ¥394,000) …………………….

(256,100)

Ending inventory (unadjusted for damage) …………….

Less: Goods on hand—undamaged

(¥30,000 X [1 – 35%]) …………………………………..

19,500

Inventory damaged ………………………………………………

Less: Residual value of damaged inventory ………….

8,150

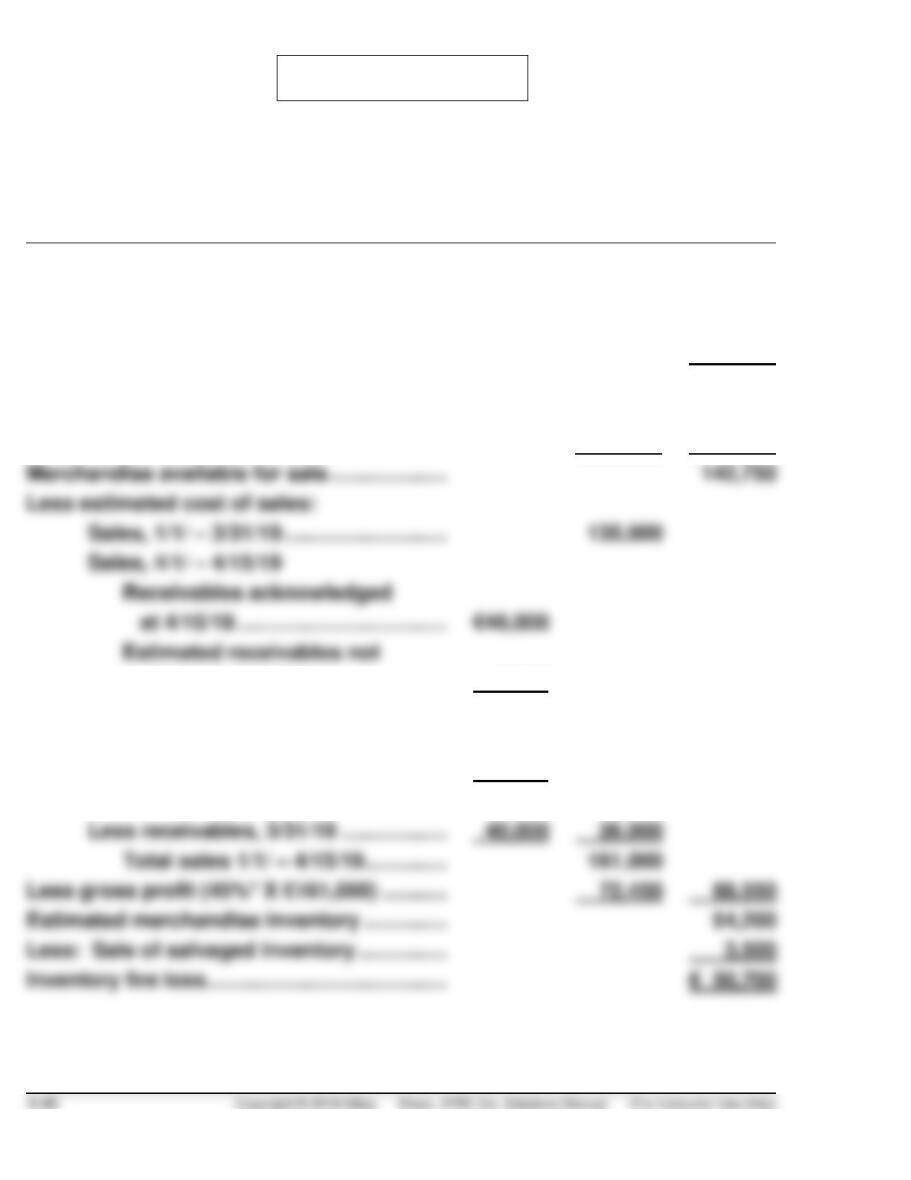

PROBLEM 9.6

STANISLAW ASA

Computation of Inventory Fire Loss

April 15, 2019

Inventory, 1/1/19 …………………………………….

€ 75,000

Purchases, 1/1/ – 3/31/19…………………………

52,000

April merchandise shipments paid ………….

3,400

Unrecorded purchases on account ………….

15,600

Total …………………………………………….

146,000

Less: Shipments in transit ……………………..

€ 2,300

Merchandise returned ………………….

950

3,250

Merchandise available for sale ………………..

142,750

Less estimated cost of sales:

Sales, 1/1/ – 3/31/19 ……………………….

135,000

Sales, 4/1/ – 4/15/19

Receivables acknowledged

at 4/15/19 ………………………………

Estimated receivables not

acknowledged ………………………

8,000

Total ……………………………………….

54,000

Add collections, 4/1/ – 4/15/19

(€12,950 – €950) ………………………….

12,000

Total ……………………………………….

66,000

Less receivables, 3/31/19 ………………

40,000

26,000

Total sales 1/1/ – 4/15/19 …………..

161,000

Less gross profit (45%* X €161,000) ………..

72,450

88,550

Estimated merchandise inventory …………..

54,200

Less: Sale of salvaged inventory ……………

3,500