PROBLEM 16.5

(a) Meng Group has a simple capital structure since it does not have any

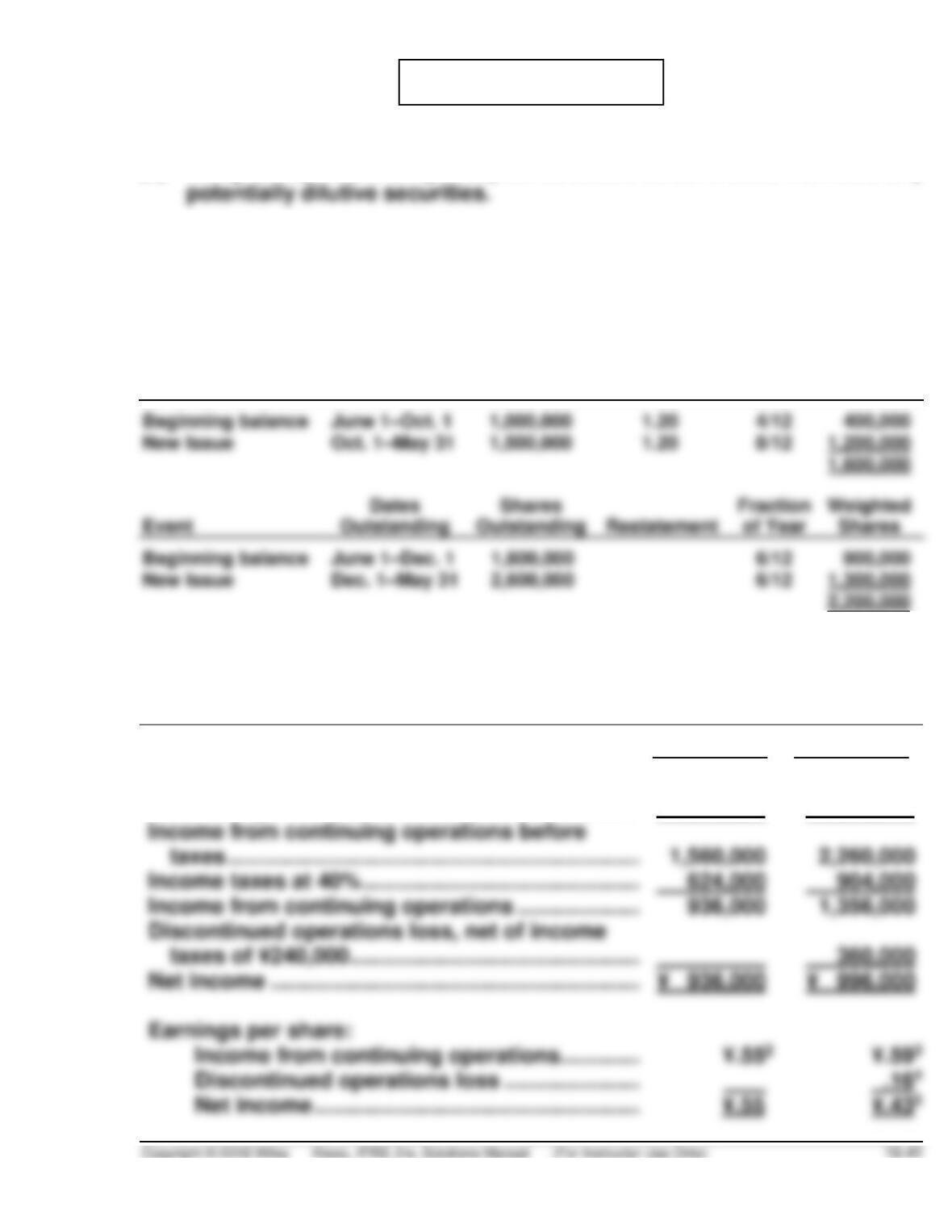

(b) The weighted-average number of shares that Ming Group would use in

calculating earnings per share for the fiscal years ended May 31, 2019,

and May 31, 2020, is 1,600,000 and 2,200,000 respectively, calculated

as follows:

Event

Dates

Outstanding

Shares

Outstanding

Restatement

Fraction

of Year

Weighted

Shares

(c) MENG GROUP

Comparative Income Statement

For Fiscal Years Ended May 31, 2019 and 2020

2019

2020

Income from operations ……………………………………

¥1,800,000

¥2,500,000

Interest expense1 ……………………………………………..

240,000

240,000

Income taxes at 40% …………………………………………

624,000

904,000

Earnings per share:

PROBLEM 16.5 (Continued)

1Interest expense = ¥2,400,000 X .10

= ¥240,000

2Earnings per share

=

=

1,600,000

=

¥.55 per share

*Preference dividends = (No. of Shares X Par Value X Dividend %)

= (20,000 X ¥50 X .06)

= ¥60,000 per year

3Earnings per share

=

=

¥.59 per share

=

¥.16 per share

5Earnings per share

=

Net Income – Preference Dividends

Weighted-Average Ordinary Shares

=

¥996,000 – ¥60,000

2,200,000

=

¥.43

PROBLEM 16.6

(a) The number of shares used to compute basic earnings per share is

4,951,000, as calculated below.

Event

Dates

Outstanding

Shares

Outstanding

Restatement

Fraction

of Year

Weighted

Shares

Conversion of

Issued shares for

building

Aug. 1–Nov. 1

Beginning Balance,

including 5% share

(b) The number of shares used to compute diluted earnings per share is

5,791,000, as shown below.

Number of shares to compute basic earnings per

(c) The numerator in the basic earnings per share calculation for the year

ended December 31, 2020, is $10,350,000, as computed below.

After-tax net income ……………………………………. $11,550,000

PROBLEM 16.7

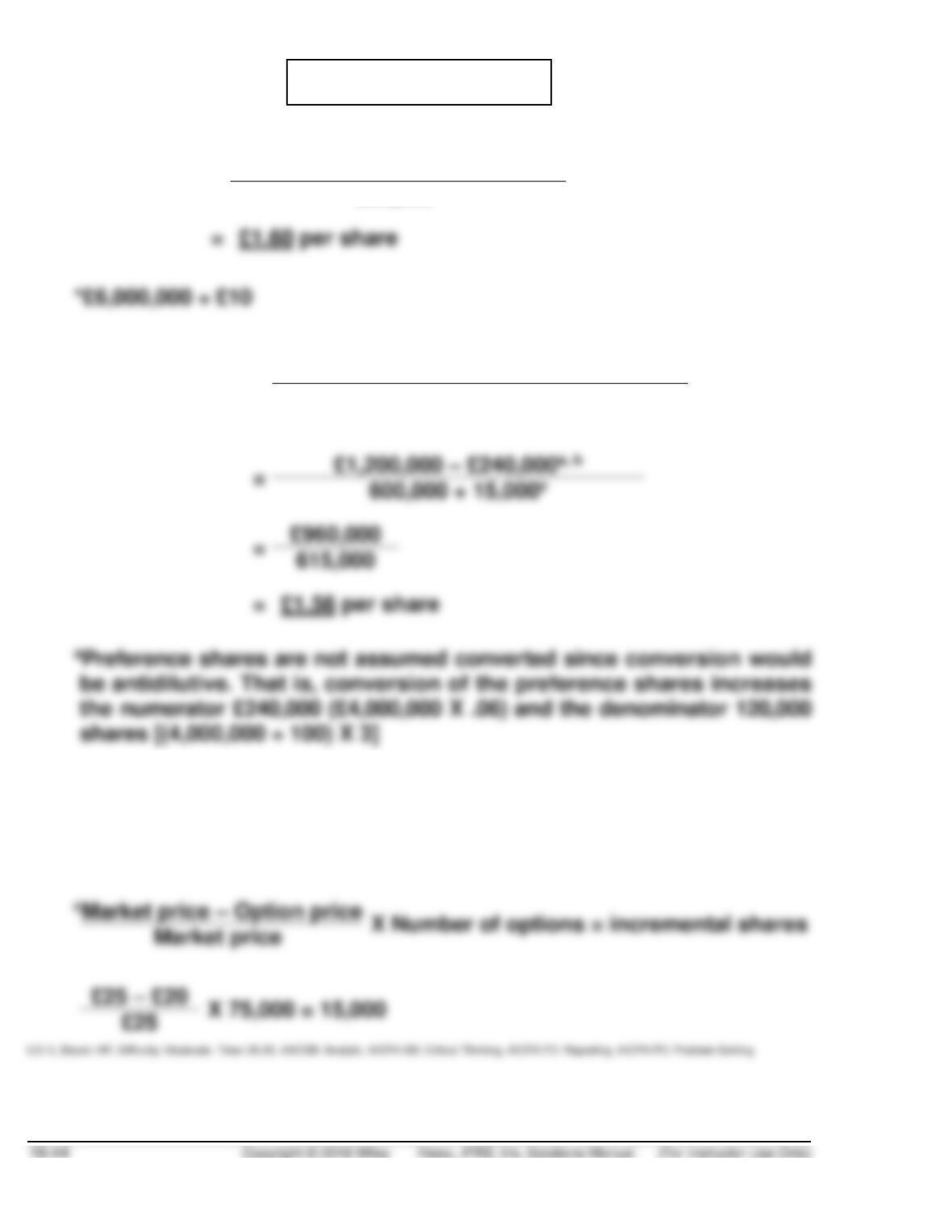

(a)

Basic EPS

=

£1,200,000 – (£4,000,000 X .06)

600,000*

(b)

Diluted EPS

=

(Net income – Preference dividends) +

Interest savings (net of tax)

Average ordinary shares + Potentially

dilutive ordinary shares

=

=

bThe convertible bonds are not assumed converted since conversion

would be antidilutive. That is, conversion of the bonds increases the

numerator £97,200 (£1,800,000 X .09 X .60) and the denominator 60,000

shares [(£2,000,000 ÷ £1,000) X 30 shares/bond]

PROBLEM 16.8

(a)

Weighted-Average Shares

Before Share

Dividend

After Share

Dividend

(b) AGASSI AG

Comparative Income Statement

For the Years Ended May 31, 2020 and 2019

2020

2019

Income from continuing operations before

taxes ………………………………………………………….

€1,400,000

€660,000

Discontinued operations loss,

PROBLEM 16.8 (Continued)

EPS calculations =

Net income – Preference dividends

Weighted-average ordinary shares

(c) 1. A corporation’s capital structure is regarded as simple if it

includes no potentially dilutive securities. Agassi AG has a simple

capital structure because it has not issued any convertible

securities, warrants, or share options, and there are no existing

rights or securities that are potentially dilutive to its earnings per

share.

2. A company having a complex capital structure would be required

to make a dual presentation of earnings per share; i.e., both basic

earnings per share and diluted earnings per share. This assumes

TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS

CA 16.1 (Time 15–20 minutes)

Purpose—to provide the student with an opportunity to answer a variety of questions related to

CA 16.2 (Time 15–20 minutes)

Purpose—to provide the student with an opportunity to discuss the ethical issues related to an earnings–

based compensation plan.

CA 16.3 (Time 15–20 minutes)

Purpose—to provide the student with an understanding of the proper accounting and conceptual merits

CA 16.4 (Time 25–35 minutes)

CA 16.5 (Time 25–35 minutes)

Purpose—to provide the student with an understanding of how earnings per share is affected by

CA 16.6 (Time 25–35 minutes)

Purpose—to provide the student with some familiarity with the applications dealing with earnings per

CA 16.7 (Time 25–35 minutes)

Purpose—to provide the student with an opportunity to articulate the concepts and procedures related

to antidilution. Responses are provided in a written memorandum.

SOLUTIONS TO CONCEPTS FOR ANALYSIS

CA 16.1

(1) Both convertible debt and debt issued with share warrants are accounted for as compound

instruments. IFRS requires that compound instruments be separated into their liability and equity

(2) Companies are not permitted to adjust compensation expense when share options become

(3) The treasury-share method is used to include options and warrants in EPS computations. The

proceeds from the assumed exercise of the options or warrants are assumed to be used to

acquire treasury shares at the market price.

(4) Companies report compensation expense for employees share purchase plans because the cost

of employee services must be measured as the services are performed. The total compensation

CA 16.2

(a) Devers recognizes that altering the estimate will benefit Adkins’ and other executive officers of

the company. Current shareholders and investors will be forced to pay out the bonuses, with the

altered estimate as a critical factor.

CA 16.3

(a) 1. The objective of issuing warrants to existing shareholders on a pro-rata basis is to raise

2. The purpose of issuing share warrants to certain key employees, usually in the form of a

non-qualified share option plan, is to increase their interest in the long-term growth and

CA 16.3 (Continued)

3. Warrants to purchase its ordinary shares may be issued to purchasers of a company’s

bonds in order to stimulate the sale of the bonds by increasing their speculative appeal and

aiding in overcoming the objection that rising price levels cause money invested for long

2. Warrants may be offered to key employees below, at, or above the market price of the

shares on the day the rights are granted except for incentive share-option plans. If a share-

option plan is to provide a strong incentive, warrants that can be exercised shortly after they

3. Income tax laws impose no restrictions on the exercise price of warrants issued to

purchasers of a company’s bonds. The exercise price may be above, equal to, or below the

current market price of the company’s shares. The longer the period of time during which

(c) 1. Financial statement information concerning outstanding share warrants issued to a

2. Financial statement information concerning share warrants issued to key employees should

include the following: status of these plans at the end of each period presented, including

3. Financial statement disclosure of outstanding share warrants that have been issued to

purchasers of a company’s bonds should include the prices at which they can be exercised,

CA 16.4

(a) Generally, the requirements indicate that employee share options be treated like all other types of

compensation and that their value be included in financial statements as part of the cost of

employee services. This requires that all types of share options be recognized as compensation

(b) According to Ciesielski’s commentary, the bill in the U.S. Congress would only record expense

for the options granted to the top five executives. They also are recommending that the SEC

(c) Here is an excerpt from a presentation given by Dennis Beresford (former FASB chair) on the

concept of neutrality, which says it well.

The FASB often hears that it should take a broader view, that it must consider the economic

There is a common element in those assertions. The goals are desirable but the means require

that the Board abandon neutrality and establish reporting standards that conceal the financial

impact of certain transactions from those who use financial statements. Costs of transactions

exist whether or not the FASB mandates their recognition in financial statements. For example,

CA 16.4 (Continued)

Neutrality does not mean that accounting should not influence human behavior. We expect that

changes in financial reporting will have economic consequences, just as economic

consequences are inherent in existing financial reporting practices. Changes in behavior naturally

follow from more complete and representationally faithful financial statements. The fundamental

question, however, is whether those who measure and report on economic events should

somehow screen the information before reporting it to achieve some objective. In FASB

Concepts Statement No. 8, Chapter 2 Qualitative Characteristics of Accounting Information, the

Board observed:

Indeed, most people are repelled by the notion that some “big brother,” whether

CA 16.5

(a) Dividends on outstanding preference shares must be subtracted from net income or added to net

loss for the period before computing EPS on the ordinary shares. This generalization will be

modified by the various features and different requirements preference shares may have with

respect to dividends. Thus, if preference shares are cumulative, it is necessary to subtract their current

(b) When options and warrants to buy ordinary shares are outstanding and their exercise price (i.e.,

proceeds the corporation would derive from issuance of ordinary shares pursuant to the warrants

(c) In arriving at the calculation of diluted EPS where convertible debentures are assumed to be

converted, their interest (net of tax) is added back to net income in the numerator element of the

CA 16.6

(a) Earnings per share, as it applies to a corporation with a capitalization structure composed of only

(b) Treatments to be given to the listed items in computing earnings per share are:

1. Outstanding preference shares with a par value liquidation right issued at a premium,

2. The exercise of an ordinary share option results in an increase in the number of shares

outstanding, and the computation of earnings per share should be based on the weighted–

3. The replacement of a machine immediately prior to the close of the current fiscal year will

4. Dividends declared on preference shares should be deducted from income from continuing

5. Acquiring treasury shares will reduce the weighted-average number of shares outstanding

used in the EPS denominator.

6. When the number of ordinary shares outstanding increases as a result of a 2-for-1 share

7. The existence of a provision for a contingent liability on a possible lawsuit created out of

retained earnings will not affect the computation of earnings per share since the