EXERCISE 23.10 (25–35 minutes)

a. The solution can be determined through use of a T-account for

property, plant, and equipment.

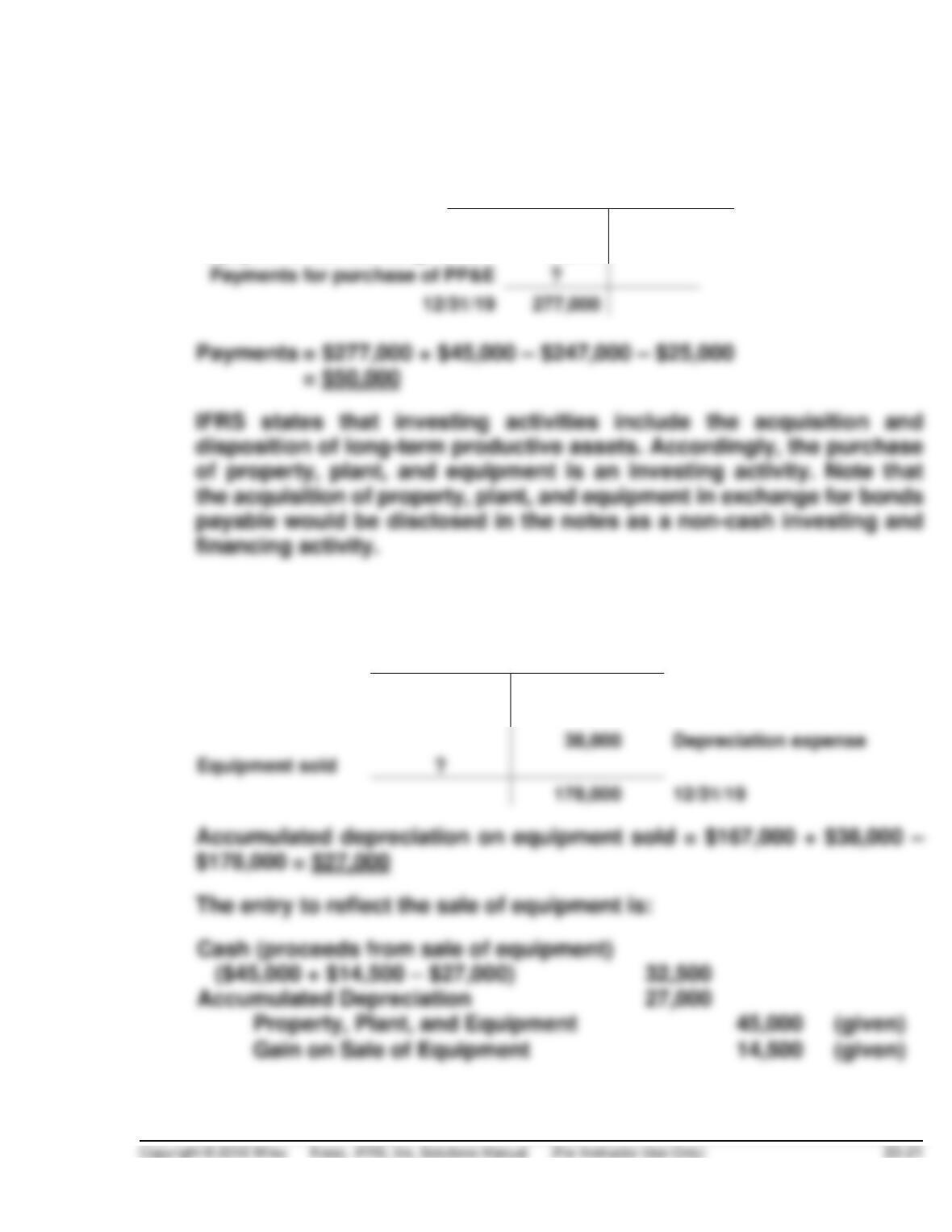

Property, Plant & Equipment

12/31/18

247,000

45,000

Equipment sold

Equipment from exchange of B/P

25,000

12/31/19

277,000

b. The solution can be determined through use of a T-account for accu-

mulated depreciation.

Accumulated Depreciation

167,000

12/31/18

Depreciation expense

Equipment sold

12/31/19

EXERCISE 23.10 (Continued)

The proceeds from the sale of equipment of $32,500 are considered

an investing activity. Investing activities include the acquisition and

disposition of long-term productive assets.

c. The cash dividends paid can be determined by analyzing T-accounts

for Retained Earnings and Dividends Payable.

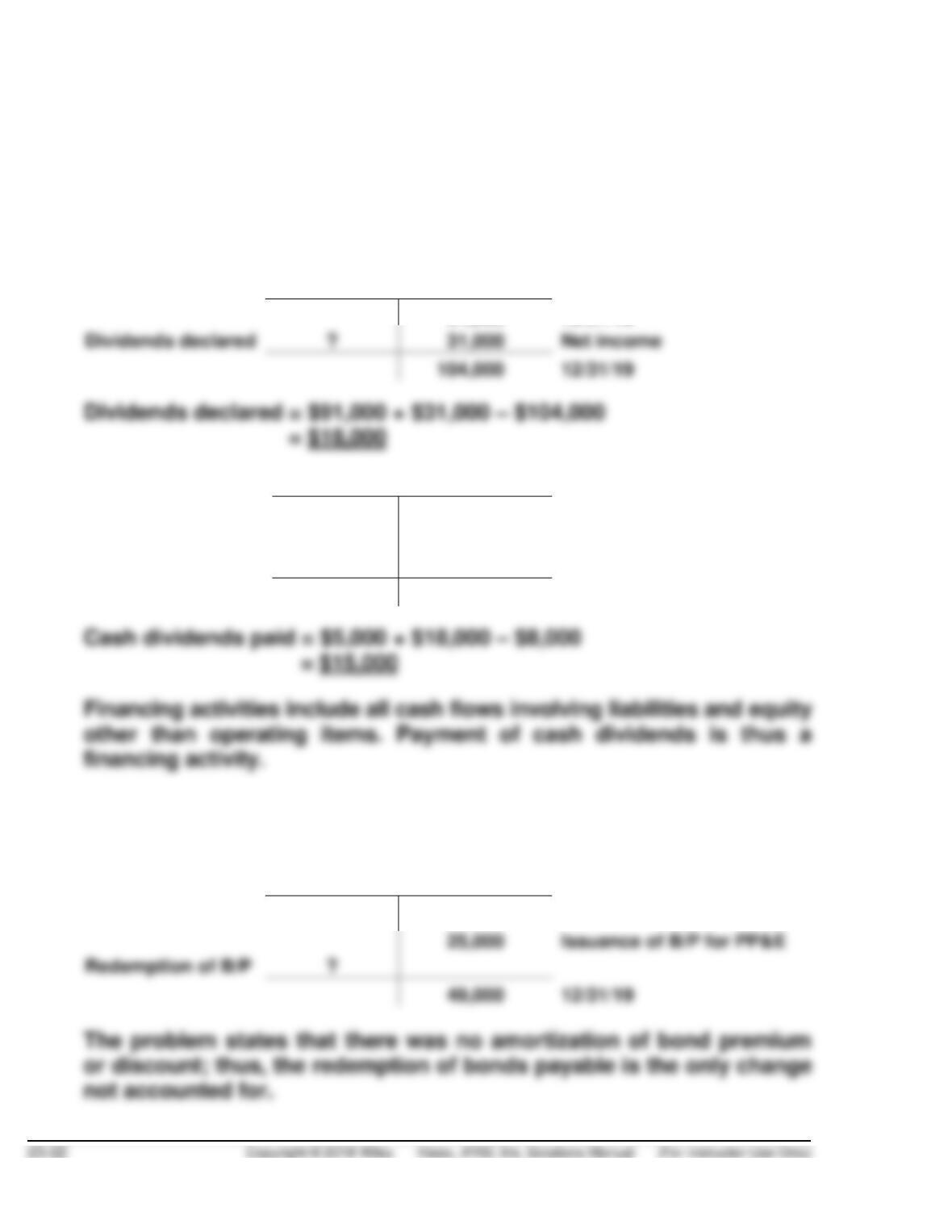

Retained Earnings

91,000

12/31/18

Dividends declared

31,000

Net income

12/31/19

Dividends Payable

5,000

12/31/18

18,000

Dividends declared

Cash dividends paid

?

8,000

12/31/19

d. The redemption of bonds payable amount is determined by setting up

a T-account.

Bonds Payable

46,000

12/31/18

25,000

Issuance of B/P for PP&E

Redemption of B/P

49,000

12/31/19

EXERCISE 23.10 (Continued)

Redemption of bonds payable = $46,000 + $25,000 – $49,000

= $22,000

EXERCISE 23.11 (30–35 minutes)

FAIRCHILD SA

Statement of Cash Flows

For the Year Ended December 31, 2019

(Indirect Method)

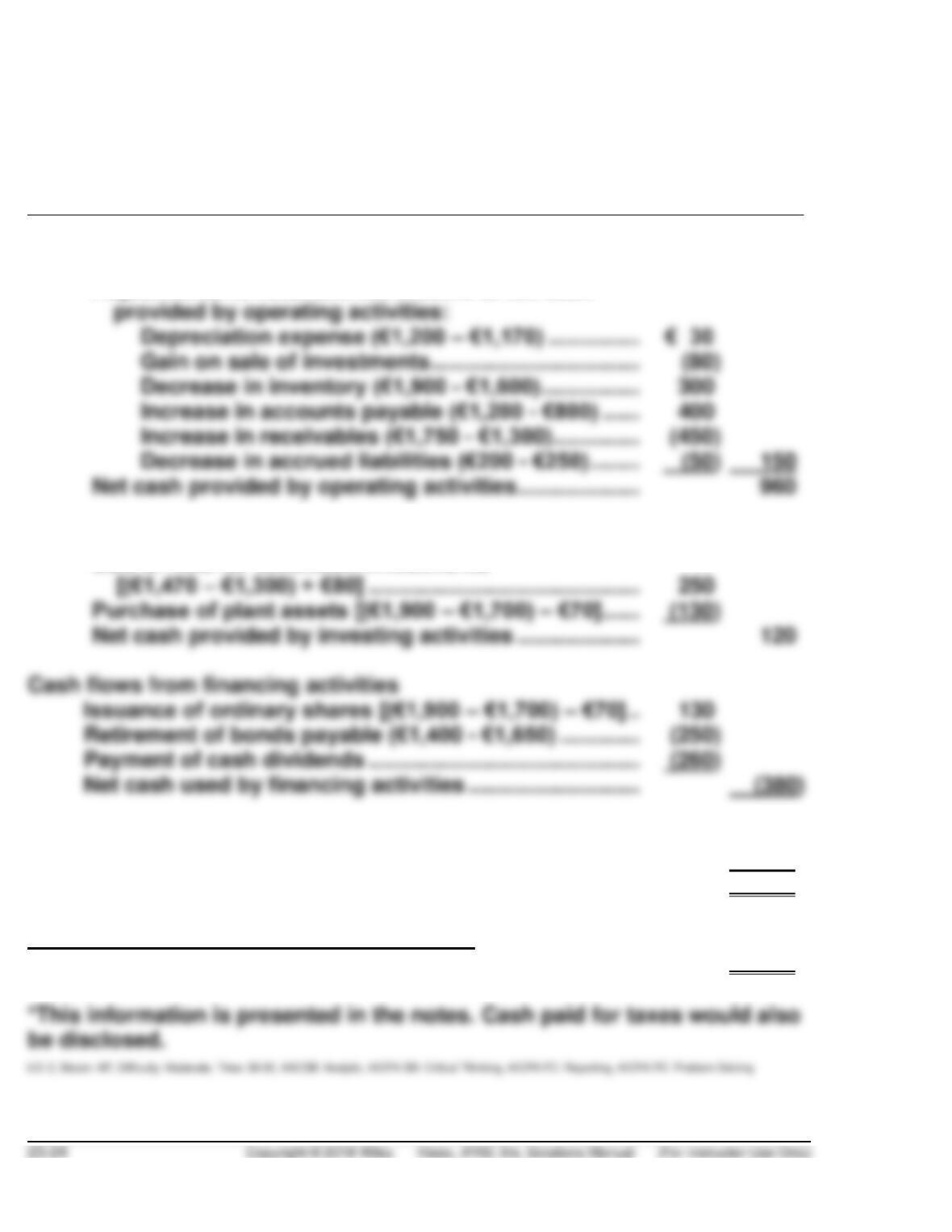

Cash flows from operating activities

Net income ……………………………………………………………

€ 810

Depreciation expense (€1,200 – €1,170) ……………

Gain on sale of investments …………………………….

Decrease in inventory (€1,900 – €1,600) …………….

Increase in accounts payable (€1,200 – €800) ……

Increase in receivables (€1,750 – €1,300) …………..

Decrease in accrued liabilities (€200 – €250) ……..

150

Net cash provided by operating activities ………………..

Adjustments to reconcile net income to net cash

Cash flows from investing activities

Net cash provided by investing activities ………………..

Cash flows from financing activities

Retirement of bonds payable (€1,400 – €1,650) ………….

Payment of cash dividends ……………………………………..

Net cash used by financing activities ……………………….

(380)

Sale of held for collection investments

Net increase in cash ………………………………………………………..

700

Cash, January 1, 2019 ……………………………………………………..

1,100

Cash, December 31, 2019…………………………………………………

€1,800

Non-cash investing and financing activities*

Issuance of ordinary shares for plant assets …………….

€ 70

EXERCISE 23.12 (20–30 minutes)

FAIRCHILD SA

Statement of Cash Flows

For the Year Ended December 31, 2019

(Direct Method)

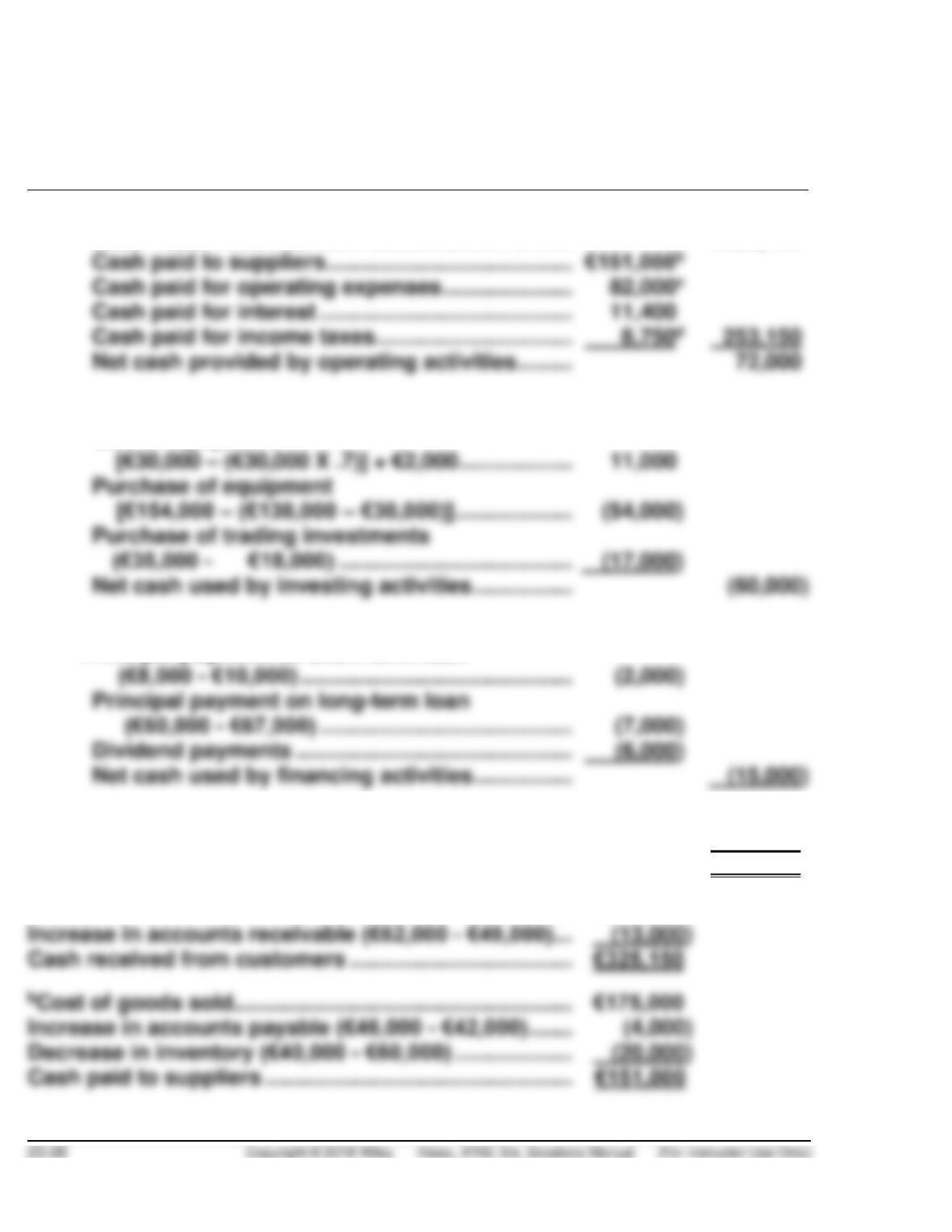

Cash flows from operating activities

Cash collections from customers …………………………

€6,450a

Less: Cash paid for merchandise ………………………..

€4,000b

Cash paid for income taxes………………………..

Net cash provided by operating activities …………….

Cash flows from investing activities

Net cash provided by investing activities ……………..

Cash flows from financing activities

Issuance of ordinary shares

[(€1,900 – €1,700) – €70] …………………………………..

130

Retirement of bonds payable ……………………………….

Payment of cash dividends ………………………………….

Net cash used by financing activities …………………..

Net increase in cash ……………………………………………………..

Cash, January 1, 2019 …………………………………………………..

Non-cash investing and financing activities

Issuance of ordinary shares for plant assets ………..

€ 70d

a€6,900 – (€1,750 – €1,300)

EXERCISE 23.13 (30–40 minutes)

ANDREWS AG

Statement of Cash Flows

For the Year Ended December 31, 2019

Cash flows from operating activities

Less: Cash received from customers ……………

€325,150a

Cash paid to suppliers ………………………………….

Cash paid for operating expenses …………………

Cash paid for interest …………………………………..

Cash paid for income taxes …………………………..

Net cash provided by operating activities ………

Cash flows from investing activities

Purchase of trading investments

Net cash used by investing activities …………….

Sale of equipment

Cash flows from financing activities

Dividend payments ………………………………………

Net cash used by financing activities …………….

Principal payment on short-term loan

Net decrease in cash ……………………………………………..

(3,000)

Cash, January 1, 2019 ……………………………………………

9,000

Cash, December 31, 2019……………………………………….

€ 6,000

aSales Revenue ……………………………………………………..

€338,150

Increase in accounts receivable (€62,000 – €49,000) …

Cash received from customers ………………………………

€175,000

Increase in accounts payable (€46,000 – €42,000) …….

Decrease in inventory (€40,000 – €60,000) ……………….

Copyright © 2018 Wiley Kieso, IFRS, 3/e, Solutions Manual (For Instructor Use Only) 23–27

EXERCISE 23.13 (Continued)

cOperating expenses ………………………………………………

€120,000

Increase in prepaid rent (€5,000 – €4,000) …………………

1,000

Depreciation expense

EXERCISE 23.14 (30–40 minutes)

ANDREWS AG

Statement of Cash Flows

For the Year Ended December 31, 2019

Cash flows from operating activities

Net income ………………………………………………………

€27,000

Adjustments to reconcile net income to net

cash provided by operating activities:

Depreciation expense ………………………………..

Amortization of copyright ………………………….

Gain on sale of equipment …………………………

Decrease in inventory ………………………………..

Increase in wages payable …………………………

Increase in accounts payable …………………….

Increase in prepaid rent ……………………………..

Increase in accounts receivable …………………

Decrease in income taxes payable ……………..

Cash flows from investing activities

Sale of equipment [(€30,000 X 30%) + €2,000] …….

11,000

Purchase of trading investments……………………….

Net cash used by investing activities …………………

Purchase of equipment

Amortization of copyright (€46,000 – €50,000) …………..

Increase in salaries and wages payable

Decrease in income taxes payable (€4,000 – €6,000) …

EXERCISE 23.14 (Continued)

Cash flows from financing activities

Principal payment on short-term loan ……………….

(2,000)

Principal payment on long-term loan …………………

(7,000)

Dividend payments ………………………………………….

(6,000)

Net cash used by financing activities ………………..

Net decrease in cash ………………………………………………..

Cash, January 1, 2019 ………………………………………………

Note to instructor: Supplemental disclosures of cash flow information is a

follows:

Cash paid during the year for:

Interest

€11,400

Income taxes

EXERCISE 23.15 (25–35 minutes)

DURAND SpA

Statement of Cash Flows

For the Year Ended December 31, 2019

Cash flows from operating activities

Net income ……………………………………………………..

€ 46,000*

Adjustments to reconcile net income to net

cash provided by operating activities:

Depreciation expense …………………………………

Loss on sale of investments ……………………….

Increase in current assets other than cash ……

Increase in current liabilities ……………………….

Net cash provided by operating activities ………….

Cash flows from investing activities

Sale of plant assets …………………………………………

8,000

Sale of held-for-collection investments …………….

Purchase of plant assets ………………………………….

EXERCISE 23.15 (Continued)

Cash flows from financing activities

Issuance of bonds payable………………………………..

75,000

Payment of dividends ……………………………………….

(10,000)

Net cash provided by financing activities …………..

65,000

Net increase in cash ………………………………………………….

5,000

Cash balance, January 1, 2019 ………………………………….

Cash balance, December 31, 2019 …………………………....

**Supporting computation

(purchase of plant assets)

Plant assets, December 31, 2018 ………………………

Less: Plant assets sold ……………………………………

Plant assets, December 31, 2019 ………………………

LO: 2, Bloom: AP, Difficulty: Moderate, Time: 25-35, AACSB: Analytic, AICPA BB: Critical Thinking, AICPA FC: Reporting, AICPA PC: Problem Solving

EXERCISE 23.16 (30–40 minutes)

(a) Computation of net cash provided by operating activities (amounts

in 000):

Net income (¥8,000 + ¥9,000) – ¥5,000 ……………….

¥12,000

Adjustments to reconcile net income to net

cash provided by operating activities:

Depreciation expense ………………………………

¥17,000*

Loss on sale of equipment

(¥6,000 – ¥3,000) …………………………………..

3,000

Decrease in prepaid expenses

Net cash provided by operating activities ………….

EXERCISE 23.16 (Continued)

(b)

Computation of net cash provided (used) by investing activities:

Sale of equipment ………………………………………………

Net cash used by investing activities …………………..

(c)

Computation of net cash provided (used) by financing activities:

Cash dividends paid …………………………………………..

Payment of notes payable …………………………………..

Issuance of bonds payable ………………………………….

Net cash used by financing activities …………………..

EXERCISE 23.17 (30–40 minutes)

(a) OCHOA GROUP

Statement of Cash Flows

For the Year Ended December 31, 2019 (¥ in 000)

Cash flows from operating activities

Net income ………………………………………………………

¥30,250

Adjustments to reconcile net income to net

cash provided by operating activities:

Depreciation expense ……………………………….

Gain on sale of investment ………………………..

Net cash provided by operating activities ………….

Cash flows from investing activities

Purchase of land ……………………………………………..

(11,000)

Sale of non-trading equity investments ……………..

12,875

Net cash provided by investing activities…………..

1,875

Cash flows from financing activities

Payment of dividends ………………………………………

Retirement of bonds payable …………………………...

Issuance of ordinary shares ……………………………..

10,000

Net cash used by financing activities ………………..

EXERCISE 23.17 (Continued)

Net increase in cash …………………………………………………

24,250

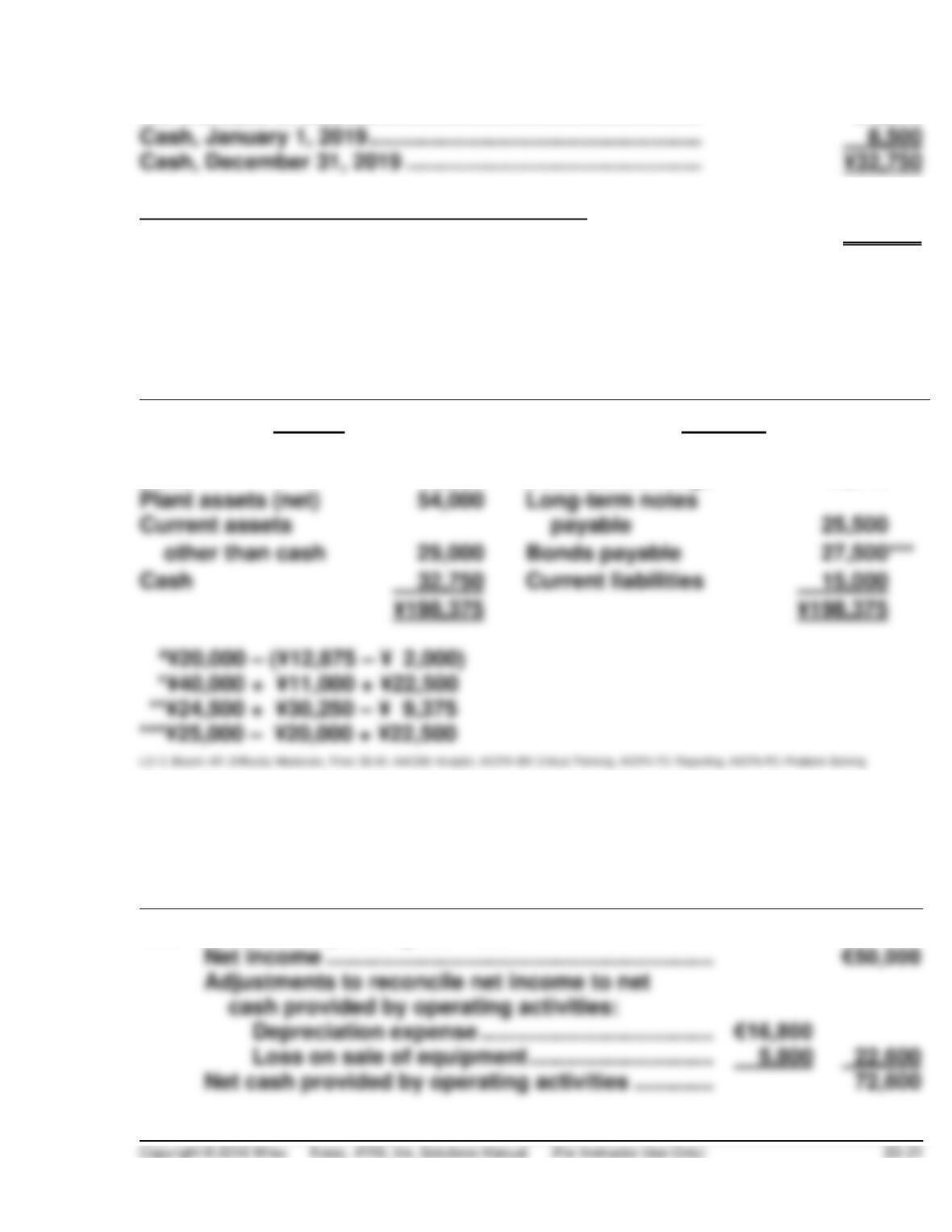

Cash, January 1, 2019 ………………………………………………

Cash, December 31, 2019 …………………………………………

¥32,750

Non-cash investing and financing activities*

Issuance of bonds for land ……………………………….

¥22,500

*This information is presented in the notes to the

financial statements.

(b) OCHOA GROUP

Statement of Financial Position

December 31, 2019

Assets

Equities

Investments

¥ 9,125

a

Share capital—ordinary

¥ 85,000

Land

73,500

*

Retained earnings

45,375

**

Plant assets (net)

Long-term notes

Current assets

payable

other than cash

Bonds payable

Cash

32,750

Current liabilities

¥198,375

*¥40,000 + ¥11,000 + ¥22,500

***¥25,000 – ¥20,000 + ¥22,500

EXERCISE 23.18 (25–30 minutes)

POPOVICH SA

Statement of Cash Flows (partial)

For the Year Ended December 31, 2019

Cash flows from operating activities

Net income ………………………………………………………

Adjustments to reconcile net income to net

cash provided by operating activities:

Depreciation expense ………………………………..

EXERCISE 23.18 (Continued)

Cash flows from investing activities

Purchase of equipment …………………………………….

(62,000)

Sale of equipment

[(€66,000 – €25,200) – €5,800] ………………………..

Major repairs on equipment………………………………

(21,000)

Cost of equipment constructed …………………………

Net cash used by investing activities ………………..

Cash flows from financing activities

Payment of cash dividends ………………………………

Decrease in cash ……………………………………………………..

(38,400)

Cash, January 1, 2019 ………………………………………………

Cash, December 31, 2019………………………………………….

EXERCISE 23.19 (20–25 minutes)

Retained Earnings ……………………………………………………

15,000

Financing—Cash Dividends ……………………………..

15,000

Retained Earnings ……………………………………………

50,000

16,800

Accumulated Depreciation—Equipment ……………

16,800

Equipment ……………………………………………………………….

131,000

Investing—Major Repairs to Equipment …………….

21,000

Investing—Purchase of Equipment …………………..

62,000

Investing—Construction of Equipment ……………..

48,000

Accumulated Depreciation—Equipment …………………….

35,000

Equipment ……………………………………………………….

66,000

EXERCISE 23.20 (20–25 minutes)

1.

Bonds Payable ………………………………………………..

300,000

Share Capital—Ordinary …………………………..

300,000

(Non-cash financing activity)

2.

360,000

Retained Earnings ……………………………………

3.

Accumulated Depreciation—Buildings ……..

4.

Accumulated Depreciation—Equipment ……………

30,000

Equipment ………………………………………………………

5,000

Investing—Purchase of Equipment …………..

5.

Retained Earnings ……………………………………………

123,000

Cash Dividend Payable …………………………….

123,000

EXERCISE 23.21 (45–55 minutes)

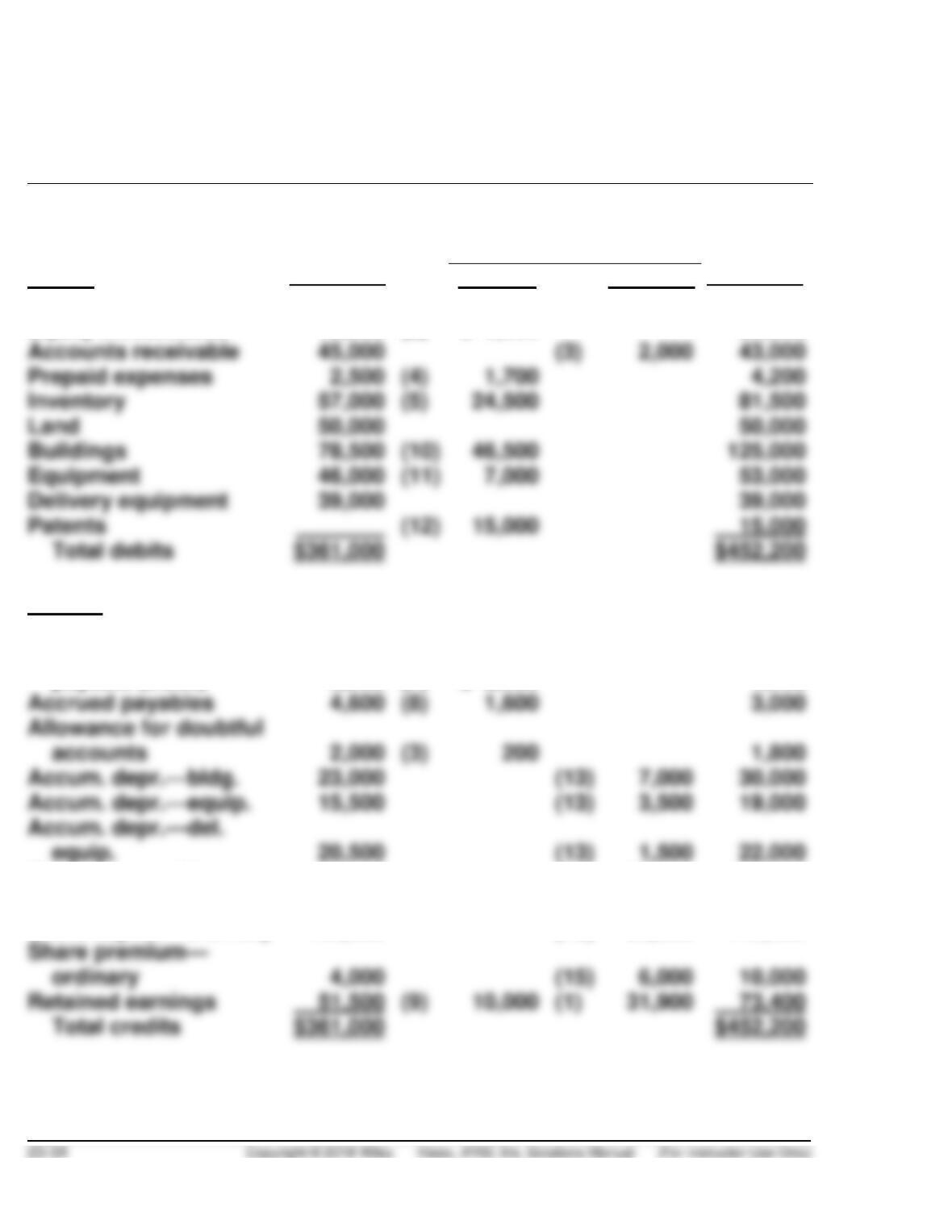

LOWENSTEIN CORPORATION

Worksheet for Preparation of Statement of Cash Flows

For the Year Ended December 31, 2019

Balance

at

12/31/18

2019

Reconciling Items

Balance

at

12/31/19

Debits

Debit

Credit

Cash

$ 24,000

(17)

$ 7,500

$ 16,500

Equity investments

19,000

(2)

$ 6,000

25,000

Accounts receivable

45,000

(3)

43,000

Prepaid expenses

2,500

(4)

4,200

Inventory

57,000

(5)

81,500

Land

50,000

50,000

Buildings

78,500

(10)

46,500

125,000

Equipment

46,000

(11)

53,000

Delivery equipment

39,000

39,000

Patents

(12)

15,000

15,000

Credits

Accounts payable

$ 16,000

(6)

$10,000

$ 26,000

Short-term notes

payable (trade)

6,000

(7)

$ 2,000

4,000

Accrued payables

4,600

(8)

3,000

Allowance for doubtful

accounts

2,000

(3)

1,800

Accum. depr.—bldg.

23,000

(13)

30,000

Accum. depr.—equip.

15,500

(13)

19,000

Accum. depr.—del.

equip.

20,500

(13)

22,000

Mortgage payable

53,400

(14)

19,600

73,000

Bonds payable

62,500

(16)

12,500

50,000

Share capital—ordinary

102,000

(15)

38,000

140,000

Retained earnings

51,500

(9)

10,000

(1)

31,900

73,400

EXERCISE 23.21 (Continued)

Statement of Cash Flows Effects

Operating activities

Net income

(1)

31,900

Depreciation

(13)

12,000

Dec. in accounts

receivable (net)

(3)

Inc. in prepaid expenses

(4)

Inc. in inventory

(5)

24,500

Inc. in accounts payable

(6)

10,000

Dec. in notes payable

(7)

Dec. in accrued payables

(8)

1,600

Investing activities

Purchase of trading equity investments

(2)

6,000

Purchase of building

(10)

46,500

Purchase of equipment

(11)

Purchase of patents

(12)

15,000

Financing activities

Payment of cash dividends

(9)

10,000

Issuance of mortgage payable

(14)

19,600

Sale of ordinary shares

(15)

44,000

Retirement of bonds

(16)

Totals

Decrease in cash

(17)

TIME AND PURPOSE OF PROBLEMS

Problem 23.1 (Time 40–45 minutes)

Purpose—to develop an understanding of the procedures involved in the preparation of a statement of

cash flows. The student is required to prepare the statement using the indirect method.

Problem 23.2 (Time 50–60 minutes)

Purpose—to develop an understanding of the procedures involved in the preparation of a statement of

Problem 23.3 (Time 50–60 minutes)

Problem 23.4 (Time 45–60 minutes)

Purpose—to develop an understanding of the procedures involved in the preparation of a statement of

Problem 23.5 (Time 40–50 minutes)

Purpose—to develop an understanding of the procedures involved in the preparation of a statement of

Problem 23.6 (Time 30–40 minutes)

Purpose—Using comparative financial statement data, the student is required to prepare the statement

Problem 23.7 (Time 30–40 minutes)

Purpose—to develop an understanding of both the direct and indirect method. The student is first asked

Problem 23.8 (Time 30–40 minutes)

Purpose—to develop an understanding of the indirect method. In the second part, the student is asked

PROBLEM 23.1

SULLIVAN CORP.

Statement of Cash Flows

For the Year Ended December 31, 2019

Cash flows from operating activities

Net income …………………………………………….

$370,000

Adjustments to reconcile net income

to net cash provided by operating

activities:

Depreciation ……………………………………

$147,000

(a)

Gain on sale of equipment ……………….

(b)

Equity in earnings of Myers Co. ……….

(c)

Decrease in accounts receivable ………

Increase in inventories …………………….

Increase in accounts payable …………..

Decrease in income taxes payable ……

(20,000)

Net cash provided by operating

activities …………………………..….

Cash flows from investing activities:

Proceeds from sale of equipment ……………

40,000

Loan to TLC Co. ……………………………………..

(300,000)

Principal repayment of loan receivable ……

50,000

Net cash used by investing

activities …………………………..….

(210,000)

Cash flows from financing activities:

Dividends paid ……………………………………….

(100,000)

Net cash used by financing

activities …………………………..….

(100,000)

Net increase in cash ……………………………………….

Cash, January 1, 2019 …………………………………….

PROBLEM 23.1 (Continued)

Separate schedule presented in the notes:

Non-cash investing and financing activities:

Issuance of lease liability for building …………….

$400,000

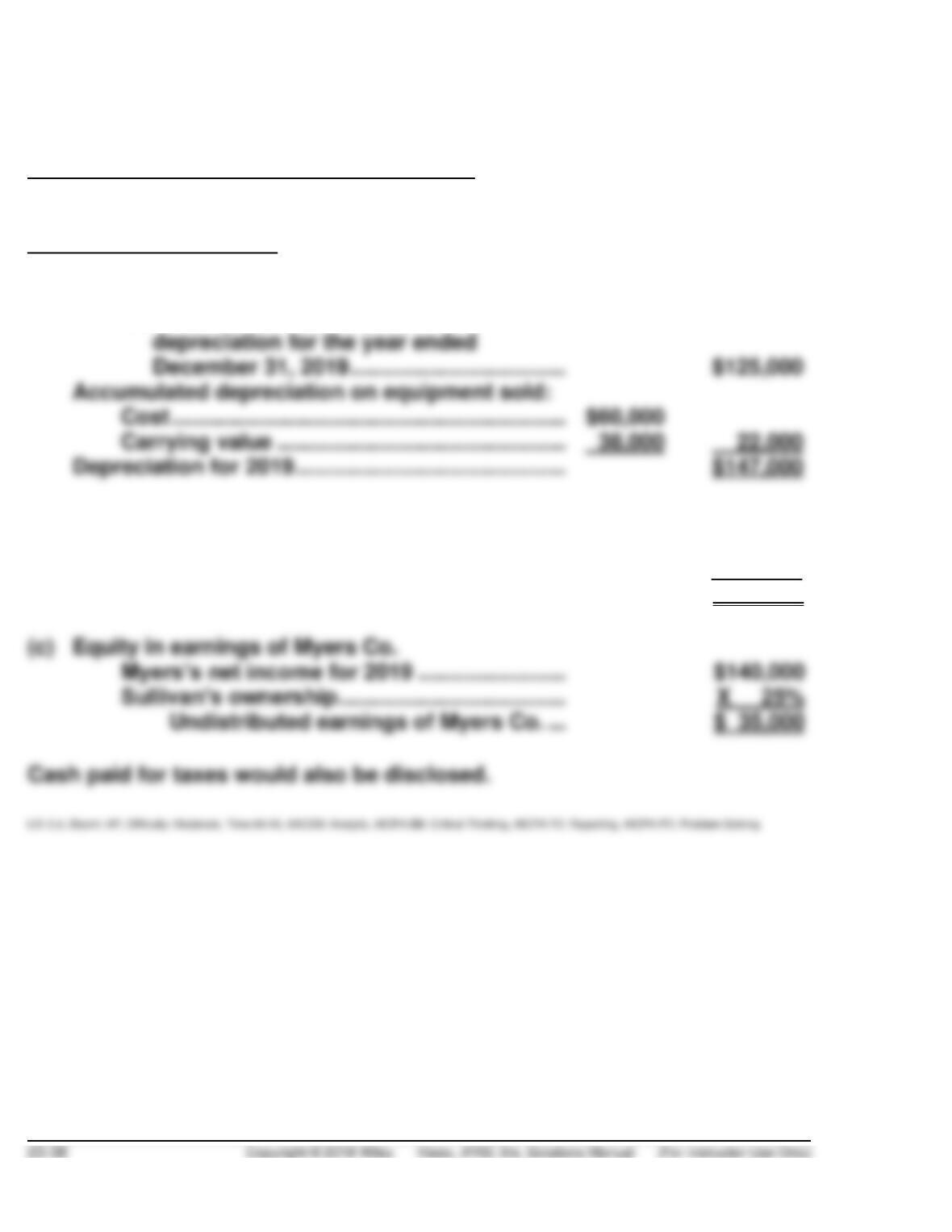

Explanation of Amounts

(a) Depreciation

Net increase in accumulated

depreciation for the year ended

December 31, 2019 ……………………………..

$125,000

Accumulated depreciation on equipment sold:

Cost …………………………..…………………………..

$60,000

Carrying value ………………………………………..

22,000

Depreciation for 2019 …………………………..…………

(b) Gain on sale of equipment

Proceeds ………………………………………………..

$ 40,000

Carrying value ………………………………………..

(38,000)

Gain on sale of equipment ………………….

$ 2,000

(c) Equity in earnings of Myers Co.

Myers’s net income for 2019 ……………………

Sullivan’s ownership ……………………………….

Undistributed earnings of Myers Co. …

$ 35,000

PROBLEM 23.2

HINCKLEY SA

Statement of Cash Flows

For the Year Ended December 31, 2019

Cash flows from operating activities

Net income …………………………..…………………

€14,750 (a)

Adjustments to reconcile net income

to net cash provided by operating

activities:

Loss on sale of equipment ……………….

(b)

Gain from flood damage …………………..

*

Depreciation expense ………………………

1,900

(c)

Patent amortization (€6,250 – €5,000) …

Gain on sale of investments ……………..

Increase in accounts receivable (net) ..

Net cash provided by operating activities …

Cash flows from investing activities

Sale of investments (€3,000 + €1,700) ……….

4,700

Sale of equipment …………………………………..

2,500

Purchase of equipment …………………………...

(20,000)

(d)

Proceeds from flood damage to building ….

32,000

Net cash provided by investing activities …

19,200

Cash flows from financing activities

Payment of dividends ……………………………..

Net cash used by financing activities ……….

(6,000)

Increase in cash …………………………………………….

20,500

Cash, January 1, 2019 …………………………………….

PROBLEM 23.2 (Continued)

Supplemental disclosures of cash flow information:

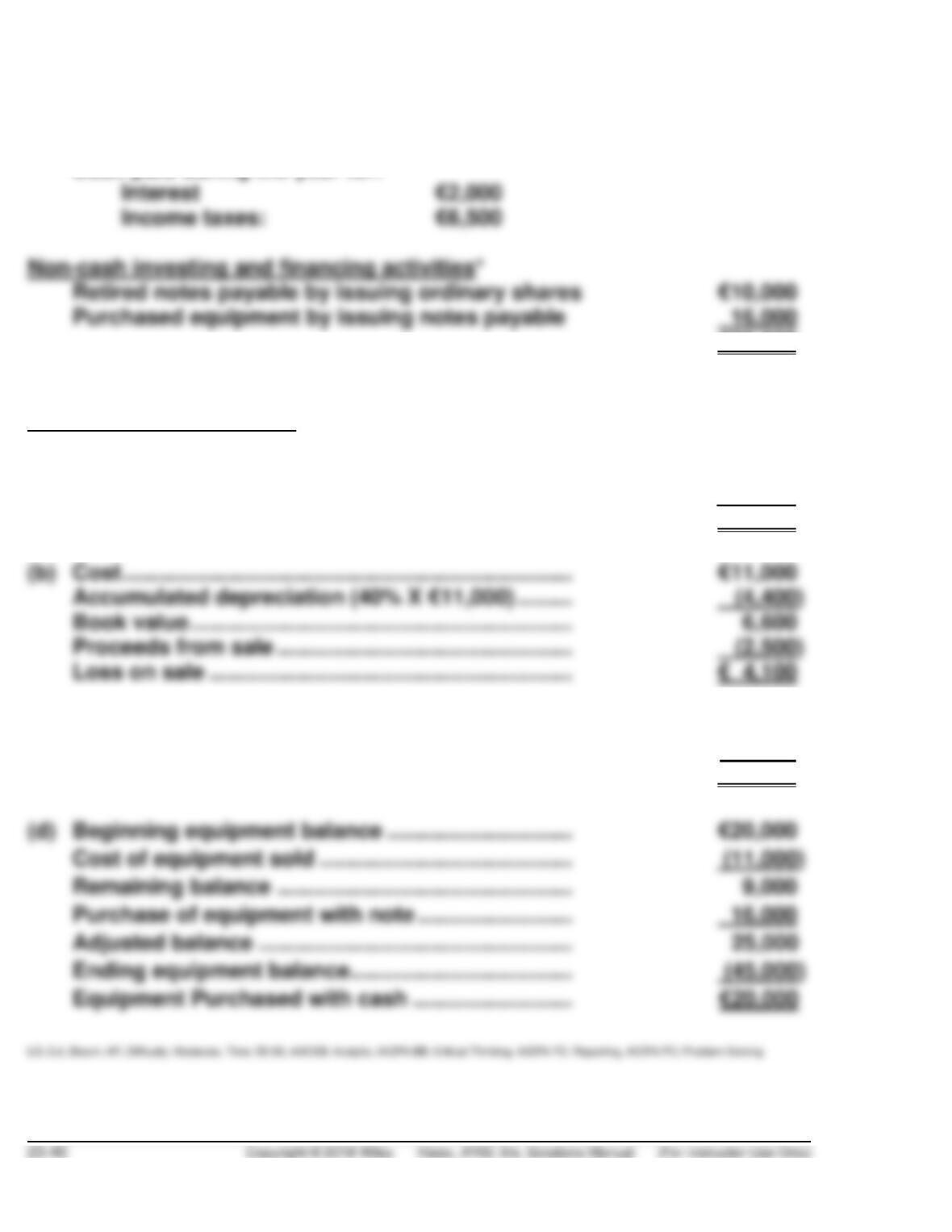

Cash paid during the year for:

Interest

Income taxes:

Non-cash investing and financing activities*

Retired notes payable by issuing ordinary shares

€10,000

Purchased equipment by issuing notes payable

16,000

€26,000

*Presented in the notes to the financial statements.

Supporting Computations:

(a) Ending retained earnings ………………………………..

€20,750

Beginning retained earnings …………………………...

(6,000)

Net income ……………………………………………………..

€14,750

(b) Cost ……………………………………………………………….

€11,000

Accumulated depreciation (40% X €11,000) ………

(4,400)

Book value ……………………………………………………..

Proceeds from sale …………………………………………

Loss on sale …………………………………………………..

€ 4,100

(c) Accumulated depreciation on equipment sold ….

€ 4,400

Decrease in accumulated depreciation …………….

(2,500)

Depreciation expense ……………………………………..

€ 1,900

(d) Beginning equipment balance …………………………

€20,000

Cost of equipment sold …………………………………..

Remaining balance …………………………………………

Purchase of equipment with note …………………….

Adjusted balance ……………………………………………

Ending equipment balance ………………………………

Equipment Purchased with cash ……………………..