EXERCISE 10.7 (20–25 minutes)

(a)

Avoidable Interest

Weighted-Average

Accumulated Expenditures

X

Interest Rate

=

Avoidable Interest

€2,000,000

12%

€240,000

Capitalization rate computation

Interest

10% short-term loan

11% long-term loan

(b)

Actual Interest

Construction loan

€2,000,000 X 12% =

€240,000

Short-term loan

€1,600,000 X 10% =

160,000

Long-term loan

€1,000,000 X 11% =

110,000

interest.

Cost

€5,200,000

Interest capitalized

426,840

EXERCISE 10.8 (20–25 minutes)

(a)

Computation of Weighted-Average Accumulated Expenditures

Expenditures

Date

Amount

X

Capitalization

Period

=

Weighted-Average

Accumulated Expenditures

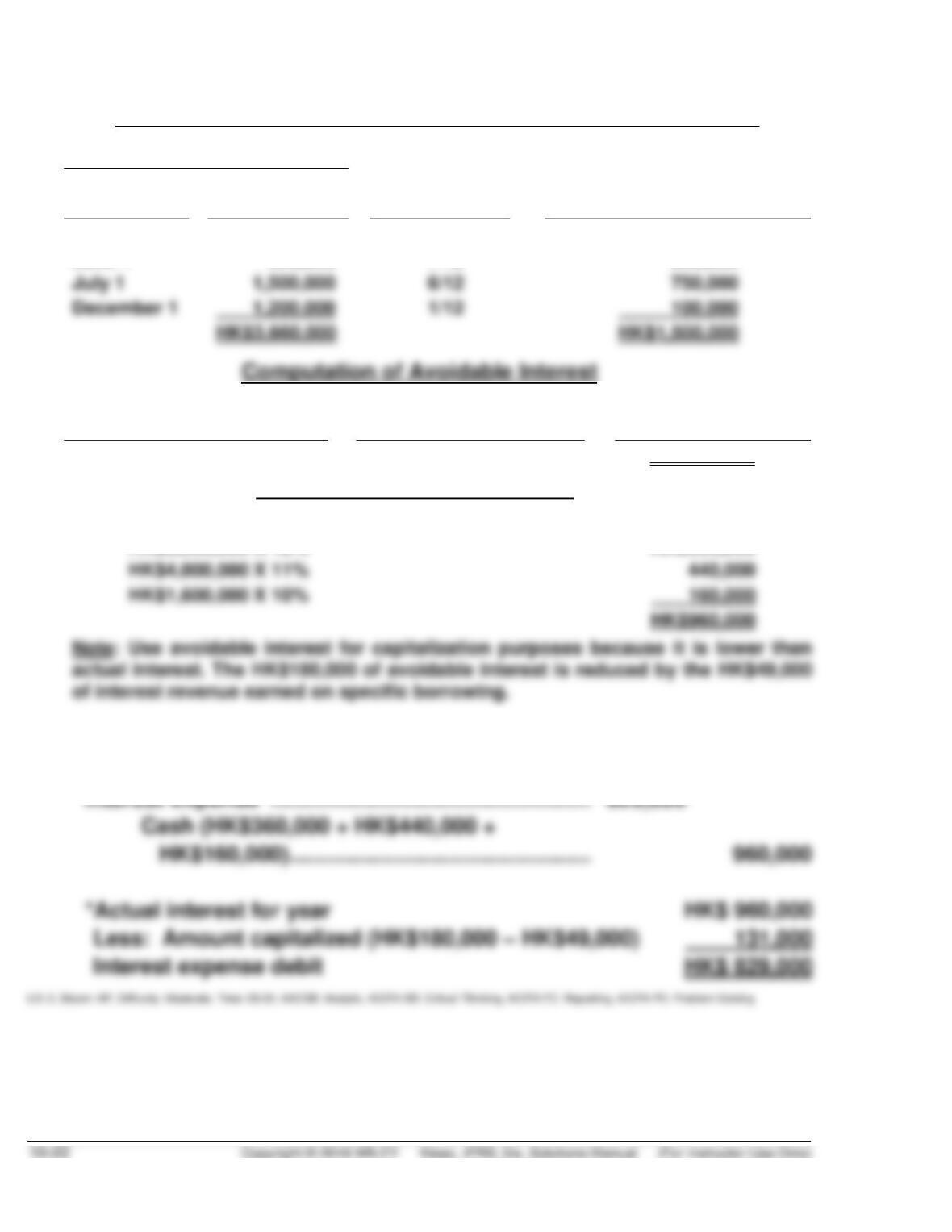

March 1

HK$ 360,000

10/12

HK$ 300,000

June 1

600,000

7/12

350,000

July 1

December 1

Weighted-Average

Accumulated Expenditures

X

Interest Rate

=

Avoidable Interest

HK$1,500,000

12% (Construction loan)

HK$180,000

Computation of Actual Interest

Actual interest

HK$1,600,000 X 10%

HK$3,000,000 X 12%

HK$360,000

(b)

Buildings ………………………………………………………………..

131,000

Interest Expense* ……………………………………………………

829,000

HK$160,000) …………………………………………………

*Actual interest for year

Less: Amount capitalized (HK$180,000 – HK$49,000)

EXERCISE 10.9 (20–25 minutes)

(a)

Computation of Weighted-Average Accumulated Expenditures

Expenditures

Date

Amount

X

Capitalization

Period

=

Weighted-Average

Accumulated Expenditures

July 31

$300,000

3/12

$75,000

November 1

100,000

0

0

$75,000

Interest revenue

$100,000 X 10% X 3/12 = $2,500

Avoidable interest

Accumulated Expenditures

X

Avoidable Interest

$400,000 X 12% X 5/12 =

$30,000 X 8% =

2,400

Interest capitalized

$ 6,500 ($9,000 – $2,500)

EXERCISE 10.9 (Continued)

(b)

(1)

7/31

Cash ………………………………………………………

400,000

Notes Payable …………………………..

400,000

300,000

Investments (Trading) …………………………..

100,000

Cash …………………………..………………….

400,000

(2)

11/1

Cash ………………………………………………………

102,500

Interest Revenue

($100,000 X 10% X 3/12) ………………..

Machinery ………………………………………………

100,000

Cash …………………………..………………….

100,000

(3)

12/31

Machinery ………………………………………………

6,500

Interest Expense

($22,400 – $6,500) …………………………..

Cash ($30,000 X 8%) ……………………….

Interest Payable

EXERCISE 10.10 (20–25 minutes)

Situation I. R$40,000—The requirement is the amount Columbia should re–

port as capitalized interest at 12/31/2019. The amount of interest eligible for

capitalization is

EXERCISE 10.10 (Continued)

Situation II. R$39,000—The requirement is total interest costs to be capitalized.

IFRS identifies assets which qualify for interest capitalization: assets

Situation III. R$180,000—The requirement is to determine the amount of

interest to be capitalized on the financial statements at April 30, 2020. The

EXERCISE 10.11 (10–15 minutes)

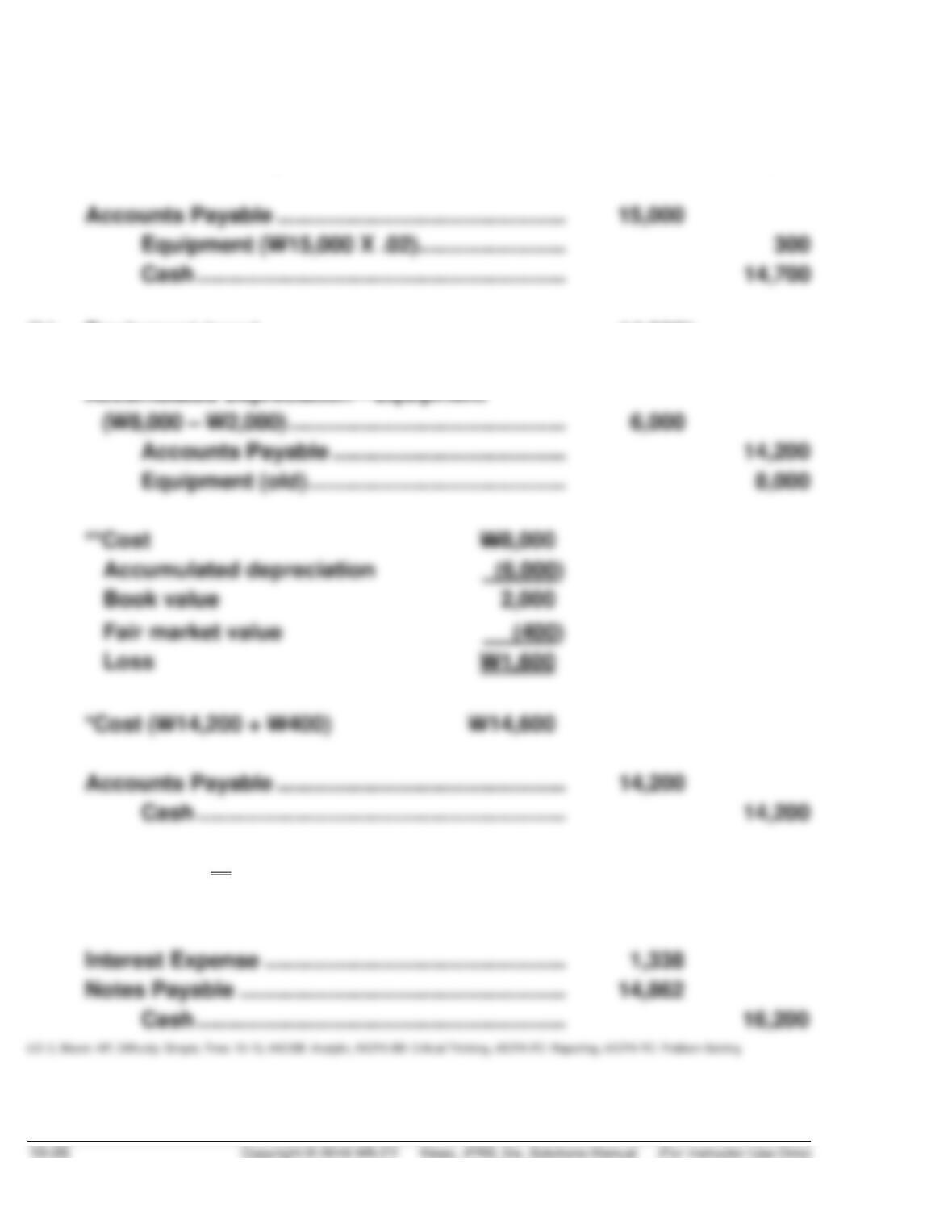

(a)

Equipment ……………………………………………………….

15,000

Accounts Payable …………………………………………..

15,000

Accounts Payable …………………………………………………..

15,000

Equipment (W15,000 X .02) …………………………..

Cash …………………………..…………………………..

(b)

Equipment (new) …………………………………………………….

14,600*

Loss on Disposal of Equipment …………………………..

1,600**

Accounts Payable …………………………………………..

Equipment (old) ………………………………………………

**Cost

Accumulated depreciation

*Cost (W14,200 + W400)

Accounts Payable …………………………………………………..

Cash …………………………..…………………………..

14,200

(c)

Equipment (W16,200 X .91743) …………………………..

14,862

Notes Payable ………………………………………………..

14,862

Interest Expense …………………………………………………….

1,338

Notes Payable ……………………………………………………….

14,862

Cash …………………………..…………………………..

16,200

EXERCISE 10.12 (15–20 minutes)

(a)

Land ………………………………………………………………………

81,000

Deferred Grant Revenue …………………………..

81,000

(b)

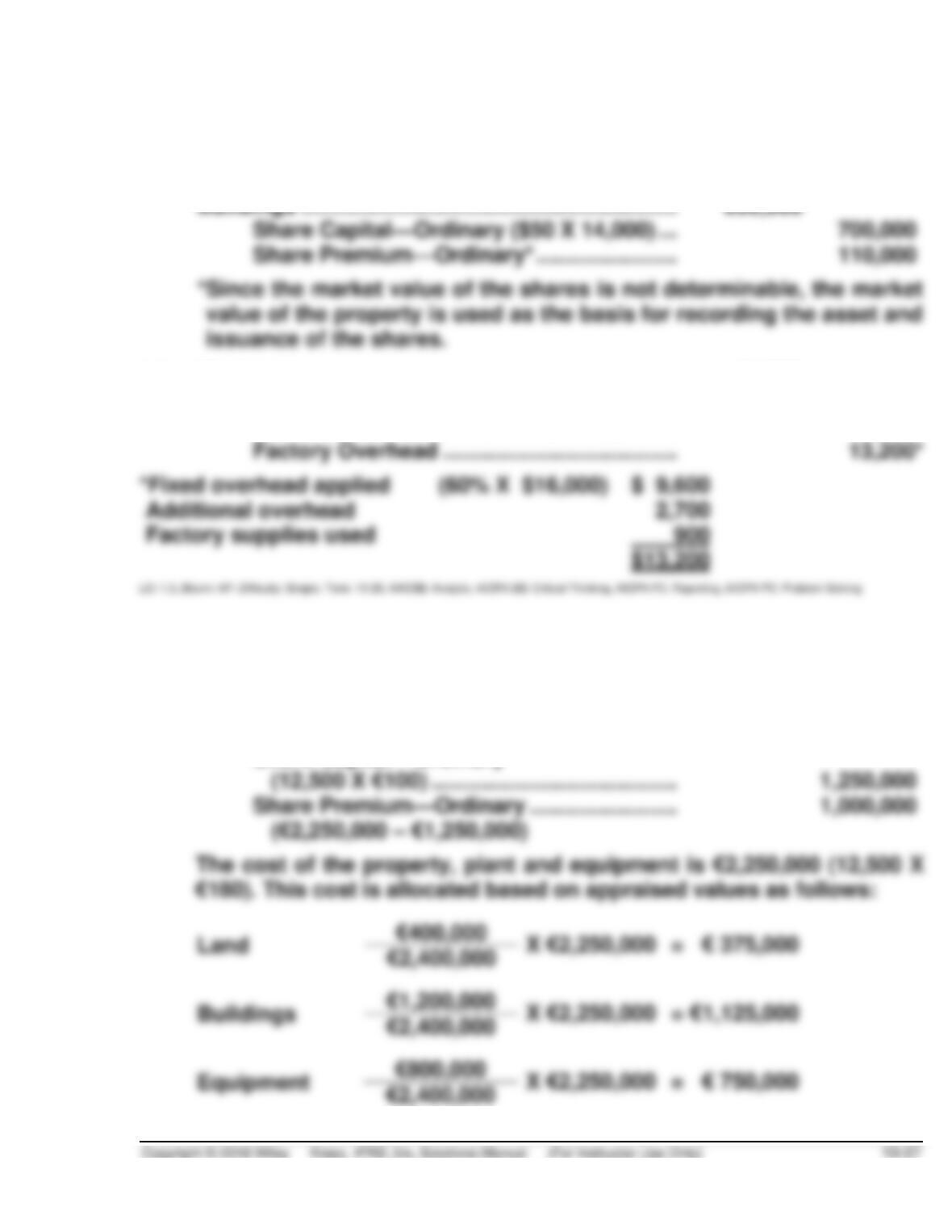

Land ………………………………………………………………………

180,000

Buildings ……………………………………………………….

Share Capital—Ordinary ($50 X 14,000) ……………

Share Premium—Ordinary* …………………………..

(c)

Machinery ……………………………………………………….

41,700

Materials ……………………………………………………….

12,500

Direct Labor ……………………………………………………

16,000

Factory Overhead …………………………………………..

13,200*

*Fixed overhead applied (60% X $16,000)

Additional overhead

Factory supplies used

EXERCISE 10.13 (20–25 minutes)

1.

Land ………………………………………………………………………

375,000

Buildings ……………………………………………………….

1,125,000

Equipment ……………………………………………………….

750,000

Share Premium—Ordinary …………………………..

(€2,250,000 – €1,250,000)

Share Capital—Ordinary

EXERCISE 10.13 (Continued)

2.

Buildings (€105,000 plus €161,000) …………………………..

266,000

Equipment ……………………………………………………….

135,000

Land Improvements …………………………..……………………

122,000

Land ………………………………………………………………………

Cash …………………………..…………………………..

541,000

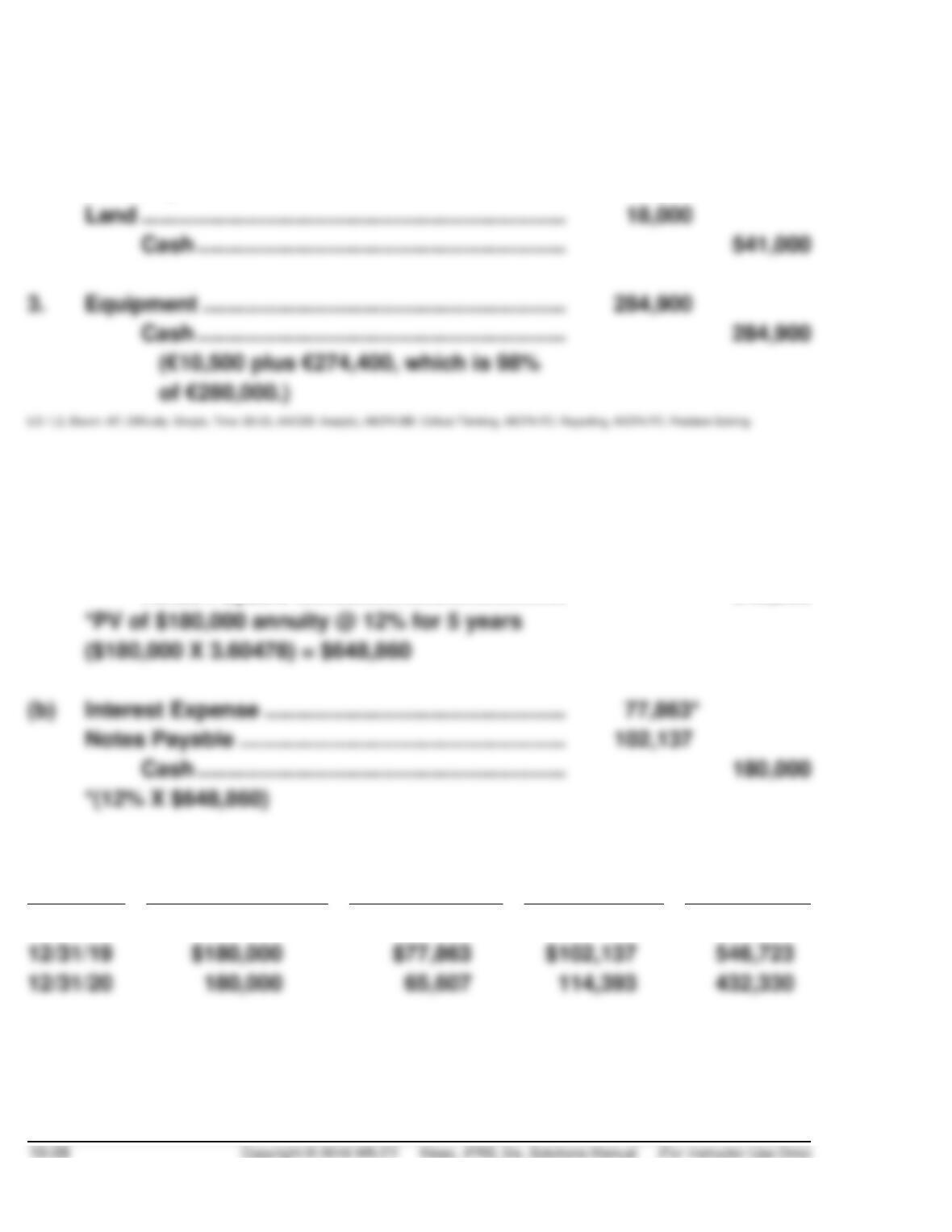

3.

Equipment ……………………………………………………….

284,900

Cash …………………………..…………………………..

284,900

of €280,000.)

EXERCISE 10.14 (15–20 minutes)

(a)

Equipment ……………………………………………………….

648,860*

Notes Payable ………………………………………………..

648,860

*PV of $180,000 annuity @ 12% for 5 years

($180,000 X 3.60478) = $648,860

(b)

Notes Payable ……………………………………………………….

102,137

Cash …………………………..…………………………..

180,000

*(12% X $648,860)

Year

Note Payment

12% Interest

Reduction

of Principal

Balance

1/2/19

$648,860

12/31/19

EXERCISE 10.14 (Continued)

(c)

Interest Expense …………………………………………………….

65,607

Notes Payable ……………………………………………………….

Cash ……………………………………………………….

(d)

Depreciation Expense ……………………………………………..

Accumulated Depreciation—Equipment …………..

*($648,860 ÷ 10)

EXERCISE 10.15 (15–20 minutes)

(a)

Equipment ……………………………………………………….

105,815.80*

Cash ……………………………………………………….

30,000.00

Notes Payable ………………………………………………..

75,815.80

*PV of £20,000 annuity @ 10% for

5 years (£20,000 X 3.79079)

Down payment

(b)

Notes Payable ……………………………………………………….

12,418.42

Interest Expense (see schedule) …………………………..

7,581.58

Cash ……………………………………………………….

20,000.00

£20,000.00

£12,418.42

EXERCISE 10.15 (Continued)

(c)

Notes Payable ……………………………………………………….

13,660.26

Interest Expense …………………………………………………….

Cash …………………………..…………………………..

EXERCISE 10.16 (25–35 minutes)

LOGAN INDUSTRIES

Acquisition of Assets 1 and 2

Use appraised values to break-out the lump-sum purchase.

Description

Appraisal

Percentage

Lump-Sum

Value on

Books

Acquisition of Asset 3

Use the cash price as a basis for recording the asset with a discount recorded

on the note.

Machinery ……………………………………………………….

Cash …………………………..…………………………..

Notes Payable ………………………………………………..

EXERCISE 10.16 (Continued)

Acquisition of Asset 4

Since the exchange lacks commercial substance, the gain of €16,000 is not

recognized. Instead the gain of €16,000 (€80,000 – €64,000) is used to reduce

the basis of the asset acquired.

Machinery (€70,000 – €16,000) …………………………..

Accumulated Depreciation—Machinery ……………………

Cash ………………………………………………………………………

Machinery ………………………………………………………

Acquisition of Asset 5

In this case the Equipment should be placed on Logan’s books at the

market value of the shares. The difference between the shares’s par value

and their fair value (based on market price) should be credited to Share

Premium.

Equipment (100 X €11 per share) …………………………..

Share Capital—Ordinary…………………………..

Share Premium—Ordinary …………………………..

EXERCISE 10.16 (Continued)

Schedule of Weighted-Average Accumulated Expenditures

Date

Amount

Current Year

Capitalization

Period

Weighted-Average

Accumulated

Expenditures

February 1

€ 180,000

9/12

€135,000

February 1

120,000

9/12

June 1

360,000

5/12

September 1

480,000

2/12

November 1

100,000

0/12

Note that the capitalization period is only 9 months in this exercise.

Avoidable Interest

X

=

Land ………………………………………………………………………

180,000

Buildings ……………………………………………………….

1,114,600

Cash …………………………..…………………………..

1,240,000

Interest Expense …………………………………………….

54,600

EXERCISE 10.17 (10–15 minutes)

Alatorre SpA

Machinery (€320 + €85) ……………………………………………

405

Accumulated Depreciation—Machinery ……………………

140

Loss on Disposal of Machinery …………………………..

Machinery ………………………………………………………

Cash ……………………………………………………….

*Computation of loss:

Book value of old machine (€290 – €140)

Fair value of old machine

Mills Business Machine AG

Cash ………………………………………………………………………

320

Inventory …………………………..……………………………………

85

Cost of Goods Sold …………………………………………………

270

Inventory …………………………..…………………………..

EXERCISE 10.18 (20–25 minutes)

(a)

Exchange has commercial substance:

Depreciation Expense ……………………………………………..

800

Accumulated Depreciation—Equipment …………..

800

(£12,700 – £700 = £12,000;

£12,000 ÷ 5 = £2,400;

£2,400 X 4/12 = £800)

Equipment ……………………………………………………….

Accumulated Depreciation—Equipment …………………..

Gain on Disposal of Equipment ……………………….

500*

Equipment …………………………..…………………………

12,700

Cash …………………………..…………………………..

10,000

*Cost of old asset

£12,700

Accumulated depreciation

(£7,200 + £800)

(8,000)

Book value

4,700

Fair value of old asset

Gain (on disposal of plant asset)

£ 500

**Cash paid

£10,000

Fair value of old melter

5,200

EXERCISE 10.18 (Continued)

(b)

Exchange lacks commercial substance:

Depreciation Expense ……………………………………………..

800

Accumulated Depreciation—Equipment …………..

800

Equipment ……………………………………………………….

Accumulated Depreciation—Equipment …………………..

Equipment ……………………………………………………..

Cash ……………………………………………………….

**Cash paid

Fair value of old asset

EXERCISE 10.19 (15–20 minutes)

(a) Exchange lacks commercial substance.

Santana SA:

Equipment ……………………………………………………….

Accumulated Depreciation—Equipment …………………..

Equipment………………………………………………………

Cash ……………………………………………………….

Valuation of equipment

Book value of equipment given

New equipment

EXERCISE 10.19 (Continued)

OR

Fair value received

R$15,500

Less: Gain deferred

4,500*

*Fair value of old equipment

Book value of old equipment

(9,000)

Delaware Company:

Cash ………………………………………………………………………

2,000

Equipment (R$13,500 + R$2,500*) …………………………..

Accumulated Depreciation—Equipment ……………………

Equipment ………………………………………………………

*Computation of loss:

Book value of old equipment

Fair value of old equipment

EXERCISE 10.19 (Continued)

(b)

Exchange has commercial substance

Santana SA

Equipment ……………………………………………………….

15,500*

Accumulated Depreciation—Equipment …………………..

19,000

Equipment ……………………………………………………..

Cash ……………………………………………………….

Gain on Disposal of Equipment ……………………….

*Cost of new equipment:

Cash paid

R$ 2,000

Fair value of old equipment

Cost of new equipment

R$15,500

**Computation of gain on disposal of equipment:

Fair value of old equipment

R$13,500

Book value of old equipment

(R$28,000 – R$19,000)

(9,000)

Gain on disposal of equipment

R$ 4,500

Delaware Company

Cash ………………………………………………………………………

2,000

Equipment ……………………………………………………….

13,500*

Accumulated Depreciation—Equipment (Old) ……………..

10,000

Loss on Disposal of Equipment …………………………..

Equipment ……………………………………………………..

*Cost of new equipment:

Fair value of equipment

R$15,500

Less: Cash received

Cost of new equipment

R$13,500

**Computation of loss on disposal of equipment:

Fair value of equipment (Old)

Book value of old equipment

EXERCISE 10.20 (15–20 minutes)

(a)

Exchange has commercial substance

Equipment ……………………………………………………….

53,900

Accumulated Depreciation—Equipment …………………..

Gain on Disposal of Equipment ……………………….

Equipment …………………………..…………………………

Cash (HK$7,000 + HK$1,100) …………………………..

Valuation of equipment

Cash

HK$ 7,000

Installation cost

Market value of used equipment

Computation of gain

Cost of old asset

HK$62,000

Accumulated depreciation

Book value

Gain on disposal of equipment

(b)

Fair value not determinable

Equipment ……………………………………………………….

50,100*

Accumulated Depreciation—Equipment …………………..

Equipment …………………………..…………………………

Cash …………………………..…………………………..

*Basis of new equipment

Book value of old equipment

HK$42,000

Cash paid (including installation costs)

EXERCISE 10.21 (15–20 minutes)

(a) 1. Carrying amount = £320,000 (£400,000 – £80,000)

(b) 1. Deferred grant revenue balance = £80,000 (£100,000 – £20,000)

EXERCISE 10.22 (10–15 minutes)

(a) January 2, 2019

Cash (€5,000,000 X .74726) ……………………. 3,736,300

Note Payable …………………………………. 3,736,300

EXERCISE 10.23 (20–25 minutes)

(a) Any addition to plant assets is capitalized because a new asset has

been created. This addition increases the service potential of the

plant.

diture increases the future service potential of the asset.

(d) Conceptually, the book value of the old electrical system should be

removed. However, practically it is often difficult if not impossible to

determine this amount. In this case, one of two approaches is followed.

One approach is to capitalize the replacement on the theory that suffi–

of the plant facility.

(e) See discussion in (d) above. In this case, because the useful life of

the asset has increased, a debit to Accumulated Depreciation would