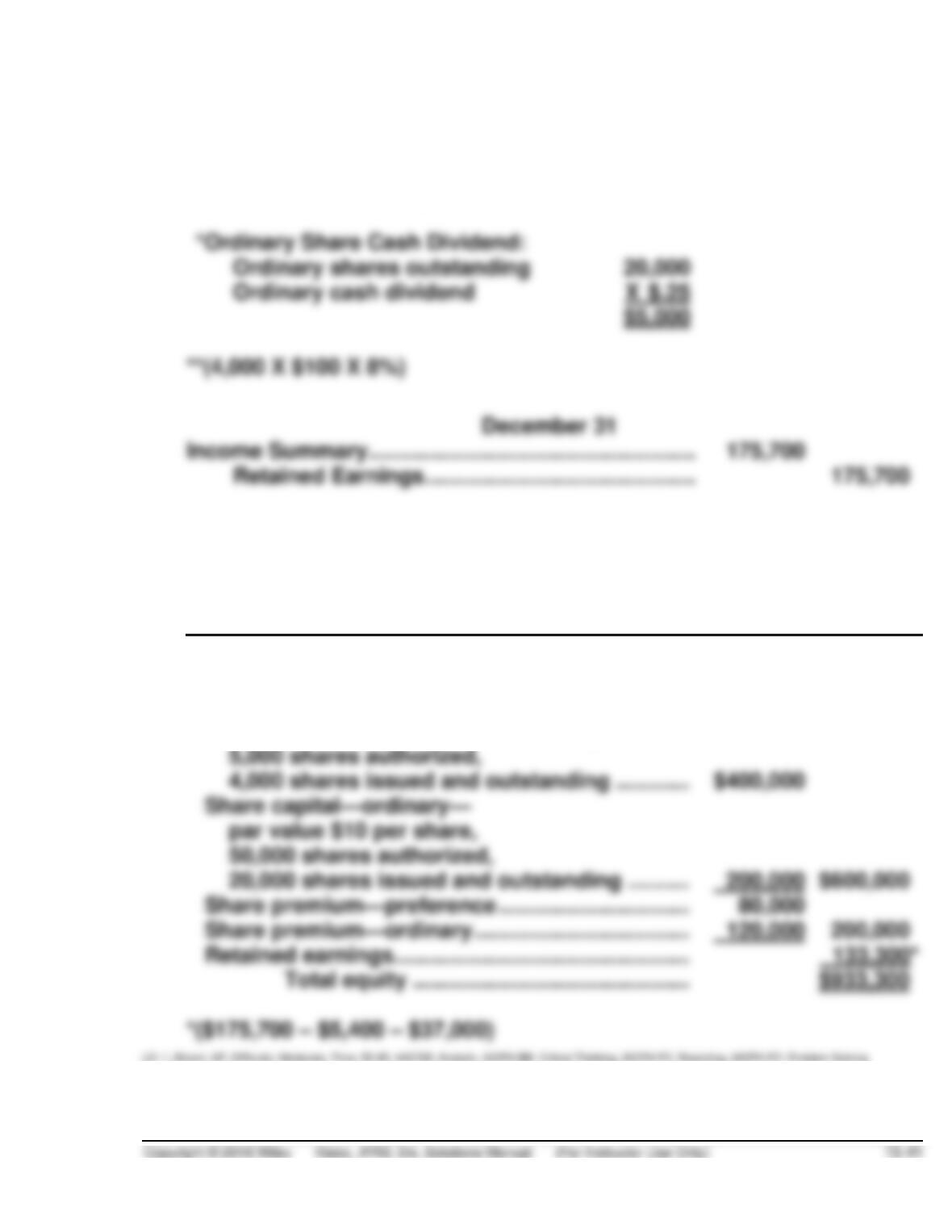

PROBLEM 15.1 (Continued)

December 31

Retained Earnings …………………………………………… 37,000

Cash Dividend Payable—Ordinary …………….. 5,000*

Cash Dividend Payable—Preference ………….. 32,000**

(b) PHELPS CORPORATION

Partial Statement of Financial Position

December 31, 2019

Equity

Share capital—preference—

par value $100 per share,

8% cumulative and nonparticipating,

PROBLEM 15.2

(a) Feb. 1 Treasury Shares (€19 X 2,000) ………….. 38,000

Cash ………………………………………. 38,000

(b) CLEMSON SE

Partial Statement of Financial Position

April 30, 2019

Equity

Share capital—ordinary,

€5 par value, 20,000 shares issued,

19,900 shares outstanding ……………………. €100,000

Share premium—ordinary………………………… €300,000

**Treasury shares (beginning balance) ………. € 0

February 1 purchase (2,000 shares) …………. 38,000

March 1 sale (800 shares) ……………………….. (15,200)

March 18 sale (500 shares) ……………………… (9,500)

April 22 sale (600 shares)………………………… (11,400)

PROBLEM 15.3

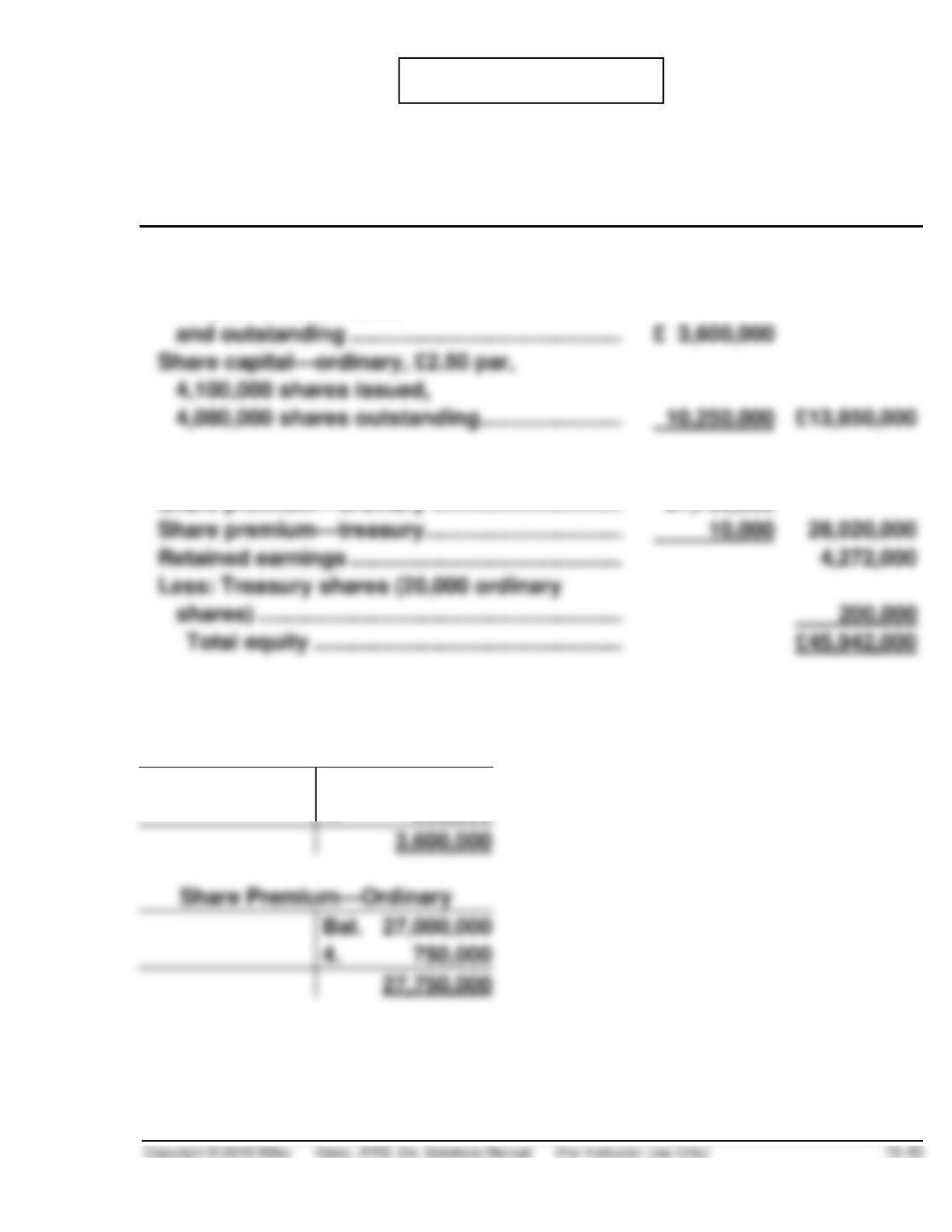

HATCH PLC

Partial Statement of Financial Position

December 31, 2019

Equity

Share capital—preference, £20 par, 8%,

180,000 shares issued

Share premium—preference ……………………… 260,000

Share premium—ordinary …………………………. 27,750,000

Supporting balances are indicated in the following T-Accounts.

Share Capital—Preference

Bal. 3,000,000

1. 600,000

3,600,000

Share Premium—Ordinary

Bal. 27,000,000

4. 750,000

27,750,000

PROBLEM 15.3 (Continued)

Share Capital—Ordinary

Bal. 10,000,000

3. 250,000

10,250,000

Bal. 4,500,000

10. 2,100,000

4,272,000

Share Premium—Preference

Bal. 200,000

2. 60,000

260,000

6. 100,000

200,000

1. Jan. 1 30,000 X £20

2. Jan. 1 30,000 X £2

3. Feb. 1 50,000 X £5

LO: 1,2,3, Bloom: AP, Difficulty: Moderate, Time: 25-30, AACSB: Analytic, AICPA BB: Critical Thinking, AICPA FC: Reporting, AICPA PC: Problem Solving

PROBLEM 15.4

-1-

Cash ……………………………………………………………………….. 10,000

-2-

Machinery (500 X €16) ………………………………………………. 8,000

-3-

Cash ……………………………………………………………………….. 10,800

Share Capital—Preference …………………………………. 5,000

Share Premium—Preference (€5,974 – €5,000) …….. 974

PROBLEM 15.4 (Continued)

-4-

Furniture and Fixtures …………………………………………….. 6,500

Share Capital—Preference ………………………………… 2,500

PROBLEM 15.5

(a) Treasury Shares (380 X £40)…………………………. 15,200

Cash ……………………………………………………. 15,200

(d) Cash (110 X £38) ………………………………………….. 4,180

Share Premium—Treasury …………………………... 620

Treasury Shares …………………………………… 4,800*

PROBLEM 15.6

(a) -1-

Treasury Shares (280 X $97) ……………………………….. 27,160

Cash ……………………………………………………………. 27,160

-2-

-3-

Dividends Payable ……………………………………………… 90,400

Cash …………………………..………………………………. 90,400

-4-

-5-

Treasury Shares (500 X $105) ……………………………… 52,500

Cash …………………………..………………………………. 52,500

-6-

Cash (350 X $96) ………………………………………………… 33,600

PROBLEM 15.6 (Continued)

(b) WASHINGTON COMPANY

Partial Statement of Financial Position

December 31, 2020

Equity

Share capital—ordinary, $100 par value,

authorized 8,000 shares; issued 4,800 shares,

4,650 shares outstanding ……………………………… $480,000

PROBLEM 15.7

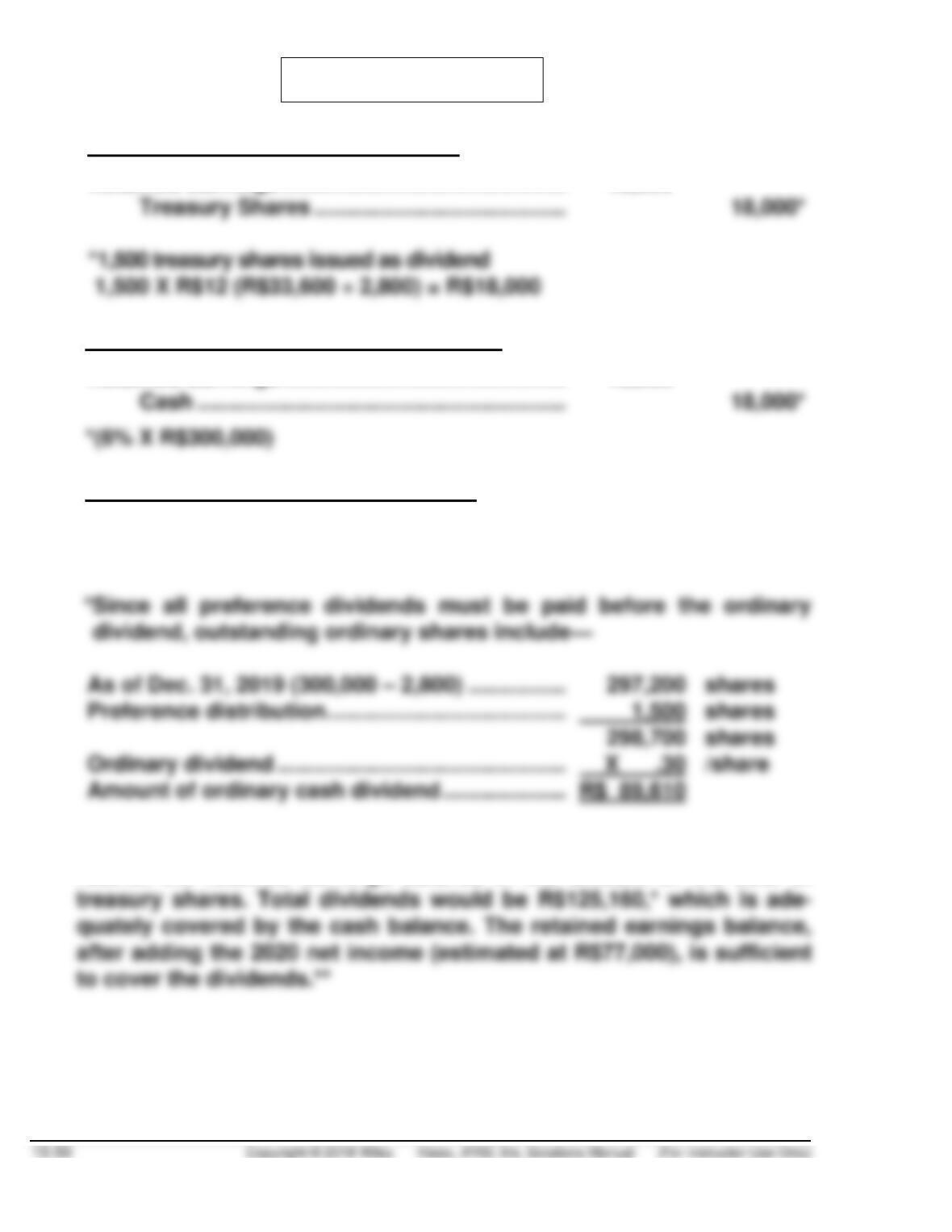

(a)

For preference dividends in arrears:

Retained Earnings ………………………………………….

18,000

Treasury Shares …………………………..…………

18,000*

*1,500 treasury shares issued as dividend

1,500 X R$12 (R$33,600 ÷ 2,800) = R$18,000

For 6% preference current year dividend:

Retained Earnings ……………………………………….

18,000

Cash ……………………………………………………

18,000*

*(6% X R$300,000)

For R$.30 per share ordinary dividend:

Retained Earnings ……………………………………….

89,610

Cash ……………………………………………………

89,610*

As of Dec. 31, 2019 (300,000 – 2,800) …………….

297,200

shares

Preference distribution …………………………………

shares

298,700

shares

Ordinary dividend ………………………………………..

/share

(b) The suggested cash dividend could be paid even if the jurisdiction did

restrict the retained earnings balance in the amount of the cost of

PROBLEM 15.7 (Continued)

*Preference dividends in arrears (6% X R$300,000) …

R$ 18,000

Current preference dividend (6% X R$300,000) ………

18,000

Ordinary dividend (R$.30 X 297,200) ……………………..

R$105,000

Estimated net income………………………………………….

Total balance available ………………………………………..

If restricted by cost of treasury shares …………………

PROBLEM 15.8

Transactions:

(a) Assuming Myers declares and pays a €1 per share cash dividend.

(1) Total assets—decrease €4,000 [(€20,000 ÷ €5) X €1]

(b) Myers declares and issues a 10% share dividend when the market price

of the stock is €14.

(1) Total assets—no effect

(c) Myers declares and issues a 100% share dividend when the market

price of the stock is €15 per share.

(1) Total assets—no effect

(d) Myers declares and distributes a property dividend

(1) Total assets—decrease €14,000 (2,000 X €7)—€6,000 gain less

€20,000 dividend.

PROBLEM 15.8 (Continued)

Note:

The journal entries made for the above transaction are:

Investments in ABC Shares (€10 – €7) X 2,000 ………..

6,000

Unrealized Holding Gain or Loss-Income …………

6,000

Retained Earnings (€10 X 2,000) …………………………..

20,000

(To record distribution of property dividend)

(e) Myers declares a 2-for-1 share split

(1) Total assets—no effect

PROBLEM 15.9

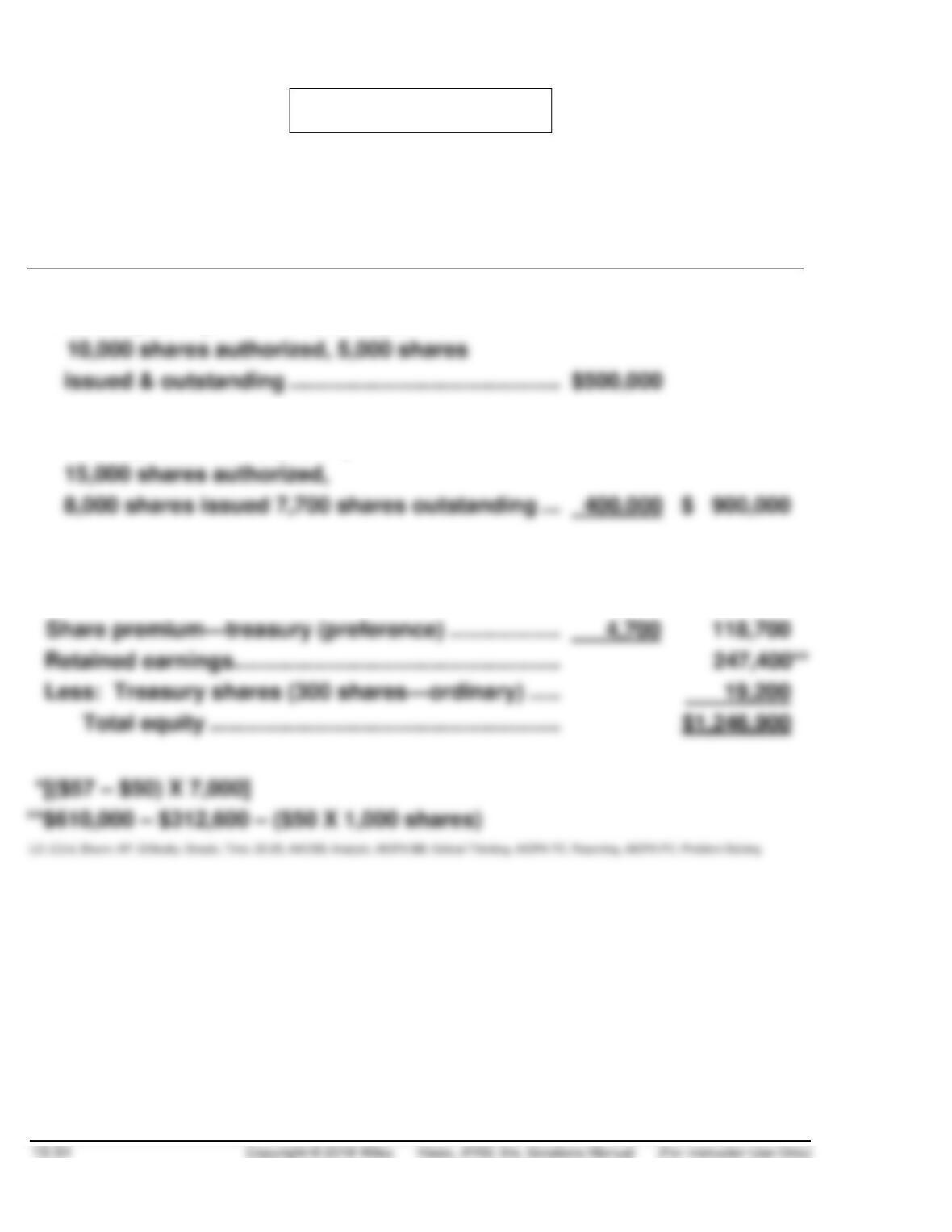

VICARIO CORPORATION

Partial Statement of Financial Position

December 31, 2021

Equity

Share capital—preference, $100 par value

Share capital—ordinary, $50 par value

15,000 shares authorized,

8,000 shares issued 7,700 shares outstanding ….

Share premium—preference ……………………………….

65,000

Share premium—ordinary …………………………………..

49,000*

Retained earnings …………………………..………………….

Less: Treasury shares (300 shares—ordinary) ……

PROBLEM 15.10

To: Ortago S.A. Board of Directors

From: Good Student, Financial Advisor

Date: Today

Subject: Report on the effects of a share dividend and a share split

INTRODUCTION

As financial advisor to the Board of Directors for Ortago S.A., I have been

asked to report on the effects of the following options for creating interest

RECOMMENDATION

In order to meet the needs of Ortago S.A. the board should choose a

DISCUSSION OF OPTIONS

The three above-mentioned options would all result in an increased

number of ordinary shares outstanding. Because the shares would be

PROBLEM 15.10 (Continued)

A 20% SHARE DIVIDEND

This option would increase the shares outstanding by 20 percent, which

translates into 800,000 additional shares of €10 par value.

The problem with this type of share dividend is that IFRS requires these

shares to be accounted for at their par value.

A 100% SHARE DIVIDEND

This option would double the number of €10 par value ordinary shares

currently issued and outstanding. While this type of dividend is

considered, in substance, a share split, Retained Earnings is nonetheless

The following journal entry would be made to record the declaration of this

dividend:

PROBLEM 15.10 (Continued)

A 2-FOR-1 SHARE SPLIT

This option doubles the number of shares issued and outstanding; however,

it also cuts the par value per share in half. No accounting treatment beyond

CONCLUSION

To generate the greatest interest in Ortago S.A. shares while maintaining

the present balances in the equity section of the statement of financial

PROBLEM 15.11

(a)

May 5, 2019

Retained Earnings ………………………………………. 1,800,000

Dividends Payable ………………………………… 1,800,000

(b)

November 30, 2019

Retained Earnings ………………………………………. 1,800,000

Ordinary Share Dividend

(c)

EARNHART CORPORATION

Partial Statement of Financial Position

December 31, 2019

Equity

Share capital—ordinary $10 par value,

PROBLEM 15.11 (Continued)

Statement of Retained Earnings

For the Year Ended December 31, 2019

Balance, January 1 …………………………….

$24,000,000

Add: Net income ………………………………

4,700,000

28,700,000

Less: Dividends on ordinary shares:

Cash………………………………………..

Share (see note) ……………………….

3,600,000

Note: The 6% share dividend (180,000 shares) was declared on November 30,

PROBLEM 15.12

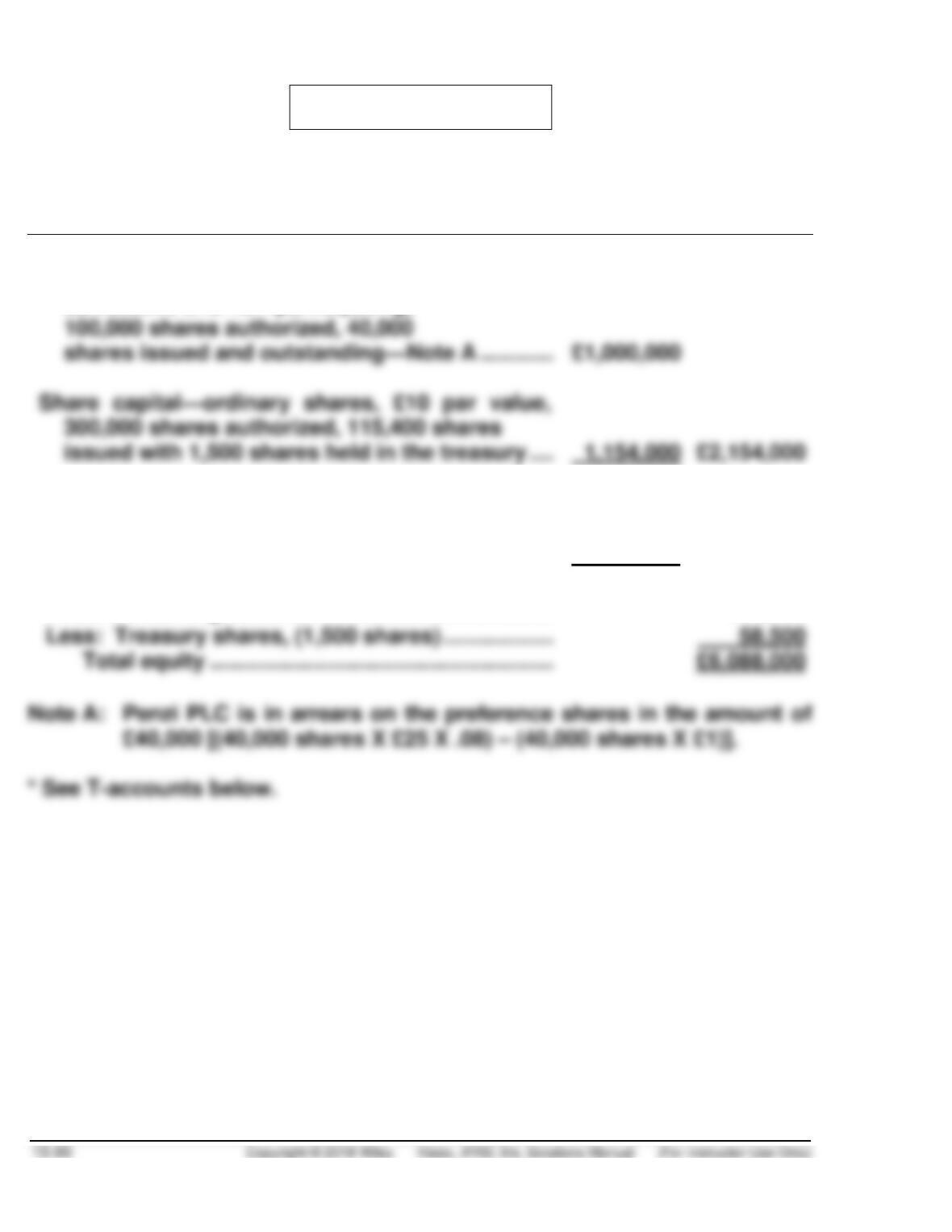

PENZI PLC

Partial Statement of Financial Position

June 30, 2020

Equity

8% Share capital—preference, £25 par value,

cumulative and non-participating,

100,000 shares authorized, 40,000

shares issued and outstanding—Note A …………

Share capital—ordinary shares, £10 par value,

issued with 1,500 shares held in the treasury ….

£2,154,000

Share premium—preference ……………………………..

760,000

Share premium—ordinary …………………………………

2,595,000*

Share premium—treasury …………………………………

1,500

3,356,500

Retained earnings …………………………..………………..

636,000

Less: Treasury shares, (1,500 shares) ………………

Total equity ………………………………………………..

£6,088,000