CHAPTER 20

Accounting for Pensions and Postretirement Benefits

ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC)

Topics

Questions

Brief

Exercises

Exercises

Problems

Concepts

for

Analysis

1. Basic definitions and

concepts related to pension

plans.

1, 2, 3, 4,

5, 6, 7, 8,

9, 10, 12,

13, 16, 25

15

1, 2, 3,

4, 5, 6

2. Worksheet preparation.

3

3, 4, 6, 7,

9, 13, 15

1, 2, 7, 8, 9,

10, 11, 12

of pension expense.

13, 14, 16

6, 8

7, 10, 11,

12, 13, 14,

5, 6, 7, 8,

9, 10, 12

15

4. Financial statement

recognition, computation of

pension expense.

9, 21,

23, 24

2, 8, 9

3, 9, 11,

12, 13, 14

1, 2, 3, 4,

5, 6, 7, 8,

9, 10, 11

2, 5, 6

5. Reconciliation schedule.

26

10

8, 12, 13

6. Past service cost.

15, 16

5, 6

6

1, 2, 9

1, 4

13, 14, 15

6, 7, 8,

9, 10, 11,

12

8. Disclosure issues.

24, 26

8, 10, 11

3, 4

27, 28,

11, 12

16, 17, 18,

13, 14

19, 20, 21

ASSIGNMENT CLASSIFICATION TABLE (BY LEARNING OBJECTIVE)

Learning Objectives

Brief

Exercises

Exercises

Problems

Concepts

for

Analysis

1. Understand the fundamentals of

pension plan accounting.

1, 2, 4

1, 2, 5, 10, 11,

12, 14

6

1, 2, 3, 4,

5, 6

13, 15

9, 10, 11,

3. Explain the accounting for past

service costs.

5, 6

6. 11

2, 3, 9

6

4. Explain the accounting for

remeasurements.

7, 8

11, 12

statements.

12, 15

11, 12

postretirement benefits.

11, 12

16, 17, 18, 19,

20, 21

13, 14

1, 2, 3, 4, 5,

6, 7, 8, 9,

6

ASSIGNMENT CHARACTERISTICS TABLE

Item

Description

Level of

Difficulty

Time

(minutes)

E20.1

Pension expense, journal entry.

Simple

15–20

E20.2

Computation of pension expense.

Simple

10–15

E20.3

Preparation of pension worksheet.

Moderate

15–25

E20.4

Basic pension worksheet.

Simple

10–15

E20.5

Computation of actual return.

Simple

10–15

E20.6

Basic pension worksheet.

Moderate

15–25

E20.7

Pension worksheet, gains and losses

Moderate

20–25

E20.8

Disclosures: Pension expense and other comprehensive income.

Moderate

25–35

E20.9

Pension worksheet.

Moderate

20–25

E20.10

Pension expense, journal entries, statement presentation.

Moderate

20–30

E20.11

Pension expense, journal entries, statement presentation.

Moderate

20–30

E20.12

Computation of actual return, gains and losses, and pension

expense.

Complex

35–45

E20.13

Worksheet for E20.12.

Complex

40–50

E20.14

Pension expense, journal entries.

Moderate

15–20

E20.15

Pension worksheet—missing amounts.

Moderate

20–25

E20.16

Postretirement benefit expense computation.

Moderate

5–10

E20.17

Postretirement benefit worksheet.

Moderate

25–30

E20.18

Postretirement benefit expense computation.

Simple

10–12

E20.19

Postretirement benefit expense computation.

Simple

10–12

E20.20

Postretirement benefit worksheet.

Moderate

15–20

E20.21

Postretirement benefit worksheet—missing amounts.

Moderate

25–30

P20.1

2-year worksheet.

Moderate

40–50

P20.2

3-year worksheet, journal entries, and reporting.

Complex

45–55

P20.3

Pension expense, journal entries.

Complex

40–50

P20.4

Pension expense, journal entries for 2 years.

Moderate

30–40

P20.5

Computation of pension expense, journal entries for 3 years.

Complex

45–55

P20.6

Pension expense, journal entries, and net gain or loss.

Complex

45–60

P20.7

Pension worksheet.

Moderate

35–45

P20.8

Comprehensive 2-year worksheet.

Complex

45–60

P20.9

Comprehensive 2-year worksheet.

Moderate

40–45

P20.10

Pension worksheet—missing amounts.

Moderate

25–30

P20.11

Pension worksheet.

Moderate

35–45

P20.12

Pension worksheet.

Moderate

35–45

P20.13

Postretirement benefit worksheet.

Moderate

30–35

Postretirement benefit worksheet—2 years.

Moderate

40–45

CA20.1

Pension terminology and theory.

Moderate

30–35

CA20.2

Pension terminology.

Moderate

25–30

CA20.3

Basic terminology.

Simple

20–25

CA20.4

Major pension concepts.

Moderate

30–35

CA20.5

Implications of International Accounting Standard No 19.

Complex

50–60

CA20.6

Non-vested employees—an ethical dilemma.

Moderate

20–30

ANSWERS TO QUESTIONS

**1. A pension plan is an arrangement whereby a company undertakes to provide its retired

employees with benefits that can be determined or estimated in advance from the provisions of a

document or from the company’s practices.

**2. A defined contribution plan specifies the employer’s contribution to the plan usually based on a

formula, which may consider such factors as age, length of service, employer’s profit, or

compensation levels.

A defined benefit plan specifies a determinable pension benefit that the employee will receive at

**3. The employer is the organization sponsoring the pension plan. The employer incurs the costs

and makes contributions to the pension fund. Accounting for the employer involves: (1) allocating

the cost of the pension plan to the proper accounting periods, (2) measuring the amount of

pension obligation resulting from the plan, and (3) disclosing the status and effects of the plan in

the financial statements.

**4. When the term “fund” is used as a noun, it refers to assets accumulated in the hands of a

**

Questions Chapter 20 (Continued)

5. An actuary’s role is to ensure that the company has established an appropriate funding pattern to

meet its pension obligations, to make predictions and assumptions about future events and

conditions that affect pension costs, and to assist the accountant in measuring facets of the pen-

**6. In measuring the amount of pension benefits under a defined benefit pension plan, an actuary

**7. One measure of the pension obligation is the vested benefit obligation. This measure uses only

current salary levels and includes only vested benefits; that is, benefits the employee is already

entitled to receive even if the employee renders no additional services under the plan.

**8. Cash-basis accounting recognizes pension cost as being equal to the amount of cash paid by

the employer to the pension fund in any period; pension funding serves as the basis for expense

recognition under the cash basis.

Accrual-basis accounting recognizes pension cost as it is incurred and attempts to recognize

pension cost in the same period in which the company receives benefits from the services of its

employees.

9. The net defined benefit obligation (asset) is the deficit or surplus related to a defined pension

plan. The deficit or surplus is the defined benefit obligation less the fair value of plan assets (if

Questions Chapter 20 (Continued)

10. The three components of the change in the net benefit obligation (asset) and their reporting are:

Service cost. Service cost is either current service cost or past service cost. Current service cost

Net interest. Net interest is the net amount computed by multiplying the discount rate by the plan

assets and the defined benefit obligation. If the plan has a net defined benefit obligation at the

Remeasurements. Remeasurements are gains and losses related to the defined benefit

obligation (changes in discount rate or other actuarial assumptions) and gains or losses on the

11. The components of pension expense are:

(1) Service cost component—the actuarial present value of benefits attributed by the pension

benefit formula to employee service during the period, including past service costs

(amendments and curtailments).

LO: 1, Bloom: K, Difficulty: Simple, Time: 5-7, AACSB: None, AICPA BB: None, AICPA FC: Reporting, AICPA PC: Communication

12. The service cost component of pension expense is determined as the actuarial present value

of benefits attributed by the pension benefit formula to employee service during the period. The

plan’s benefit formula provides a measure of how much benefit is earned and, therefore, how

Questions Chapter 20 (Continued)

13. Net interest is defined as the amount that accrues by multiplying the net defined benefit

Net Interest = [Defined Benefit Obligation X Discount Rate] – [Plan Assets X Discount Rate]

Because payment of the pension obligation is deferred, companies record the pension liability

on a discounted basis. As a result, the liability accrues interest over the service life of the

employee (passage of time), which is essentially interest expense. Similarly, companies earn a

14. Computation of actual return on plan assets

Fair value of plan assets at end of period $10,150,000

Deduct: Fair value of plan assets at beginning of period 9,200,000

15. Service cost is the actuarial present value of benefits attributed by the pension benefit formula to

employee service during the period. Actuaries compute service cost at the present value of

the new benefits earned by employees during the year. Past service cost is the change in the

16. When a defined benefit plan is either initiated or amended, credit is often given to employees for

years of service provided before the date of initiation or amendment. The cost of these retroactive

17. Also included in past service costs are the reduction in benefits, arising from curtailments. A

curtailment is a significant reduction in the benefit obligation due to a significant reduction in the

Questions Chapter 20 (Continued)

18. Sarah is not correct in her assertion. Remeasurements arise from sudden and large changes in

the fair value of plan assets or changes in actuarial assumptions that affect the amount of the

19. An asset gain occurs when the actual return on the plan assets is greater than the interest

revenue on plan assets while an asset loss occurs when the actual return is less than the

interest revenue on the plan assets.

LO: 1, Bloom: K, Difficulty: Simple, Time: 3-5, AACSB: None, AICPA BB: None, AICPA FC: Reporting, AICPA PC: Communication

20. Liability gains and losses are unexpected gains or losses from changes in the defined benefit

obligation. Liability gains (resulting from unexpected decreases) and liability losses (resulting

21. If pension expense recognized in a period exceeds the current amount funded, a liability account

referred to as Pension Liability arises; the current portion is reported as a current liability, if due

in 12 months. Otherwise, report as non-current.

If the current amount funded exceeds the amount recognized as pension expense, an asset

*22. Bill is not correct. Liability gains and losses, although not included in pension expense, are

recorded in other comprehensive income in the period that they arise. Total comprehensive

23. Jacob AG would report a pension liability of €27,000 (€125,000 – €98,000).

LO: 1, Bloom: AP, Difficulty: Simple, Time: 5-7, AACSB: Analytic, AICPA BB: Critical Thinking, AICPA FC: Reporting, AICPA PC: Problem Solving

*24. Joshua plc would report a pension asset of £10,000 (£345,000 – £335,000).

*

Questions Chapter 20 (Continued)

25. (a) A contributory plan is a pension plan under which employees contribute part of the cost.

In some contributory plans, employees wishing to be covered must contribute; in other

contributory plans, employee contributions result in increased benefits.

*26. Compromises by the IASB to full capitalization or recognition in the financial statements of

relevant pension data resulted in nonrecognition of the defined benefit obligation and plan assets

27. Postretirement benefits other than pensions include healthcare and other welfare benefits

provided to retirees, their spouses, dependents, and beneficiaries. The other welfare benefits

28. The major differences between pension benefits and postretirement benefits are listed below:

Differences between Postretirement Healthcare Benefits and Pensions

Item

Pensions

Healthcare Benefits

Funding

Generally funded.

Generally NOT funded.

Benefit

Well-defined and level dollar amount.

Generally uncapped and great

variability.

Beneficiary

Retiree (maybe some benefit to

surviving spouse).

Retiree, spouse, and other

Benefit Payable

Monthly.

As needed and used.

Level of cost varies geographically

and fluctuates over time.

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 20.1

Service cost HK$316,000,000

Interest on DBO 342,000,000

BRIEF EXERCISE 20.2

Ending plan assets €2,000,000

Beginning plan assets (1,680,000)

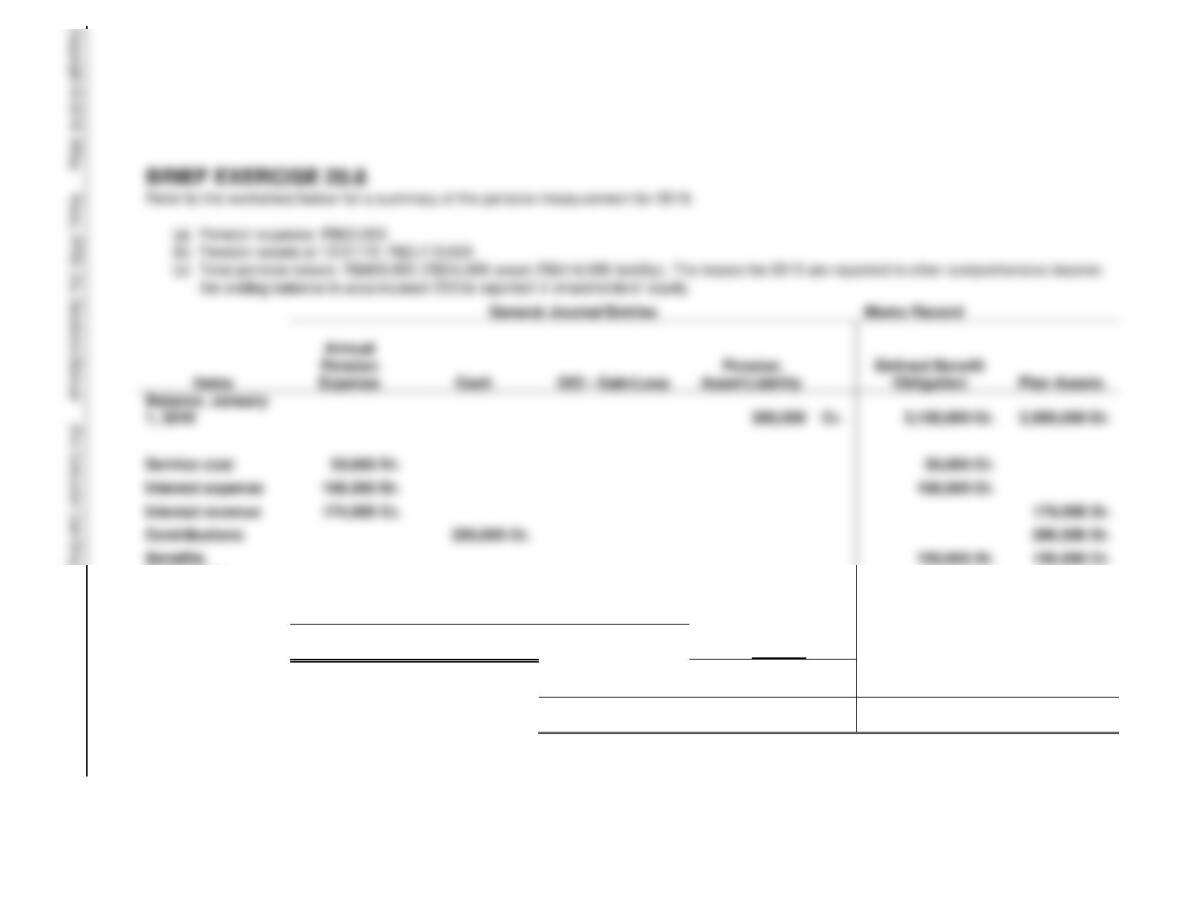

BRIEF EXERCISE 20.3

UDDIN COMPANY

General Journal Entries

Memo Record

Items

Pension

Expense

Cash

Pension

Asset/

Liability

Defined

Benefit

Obligation

Plan

Assets

1/1/19

250,000 Cr.

250,000 Dr.

Service cost

27,500 Dr.

27,500 Cr.

Interest revenue

25,000 Cr.

25,000 Dr.

17,500 Dr.

Journal entry

27,500 Dr.

BRIEF EXERCISE 20.4

Pension Expense……………………………………………. 61,000,000

Pension Asset/Liability…………………………….. 9,000,000

Cash ……………………………………………………….. 52,000,000

LO: 1, Bloom: AP, Difficulty: Simple, Time: 5-7, AACSB: Analytic, AICPA BB: Critical Thinking, AICPA FC: Reporting, AICPA PC: Problem Solving

BRIEF EXERCISE 20.5

Pension expense

BRIEF EXERCISE 20.6

Current service cost …………………………………………………. €26,000

BRIEF EXERCISE 20.7

Actual return ……………………………………………………………. €1,500

Copyright © 2018 Wiley Kieso, IFRS, 3/e, Solutions Manual (For Instructor Use Only) 20 -12

Asset Loss

(174,000 – 160,000)

14,000 Dr.

14,000 Cr.

Liability Loss

414,000 Dr.

414,000 Cr.*

Journal entry for

2019

62,000 Dr.

200,000 Cr.

428,000 Dr.

290,000

Cr.

Accumulated OCI

12/31/18

0

Balance, Dec. 31,

2019

428,000 Dr.

490,000

Cr.

3,600,000 Cr.

3,110,000 Dr.

*R$3,600,000 – (R$3,100,000 + R$50,000 + R$186,000 – R$150,000)

LO: 4,5, Bloom: AP, Difficulty: Moderate, Time: 20–30, AACSB: Analytic, AICPA BB: Critical Thinking, AICPA FC: Reporting, AICPA PC: Problem Solving

Cash

Balance, January

1, 2019

200,000

3,100,000 Cr.

2,900,000 Dr.

Service cost

50,000 Dr.

Interest expense

Interest revenue

Contributions

200,000 Cr.

Benefits

BRIEF EXERCISE 20.9

Statement of Comprehensive Income

Revenues …………………………………………………………………. €125,000

BRIEF EXERCISE 20.10

Defined benefit obligation …………………………………………………. €(510,000)

BRIEF EXERCISE 20.11

Service cost ……………………………………………………………………… $40,000

BRIEF EXERCISE 20.12

Postretirement expense ……………………………………….. 240,900

Cash …………………………………………………………….. 160,000

SOLUTIONS TO EXERCISES

EXERCISE 20.1 (15–20 minutes)

(a) Computation of pension expense:

Service cost …………………………………………….. $60,000

Interest expense ($500,000 X .10) ………………. 50,000

EXERCISE 20.2 (10–15 minutes)

Computation of pension expense:

Service cost ……………………………………………………….. €90,000

20–15 Copyright © 2018 Wiley Kieso, IFRS, 3/e, Solutions Manual (For Instructor Use Only)

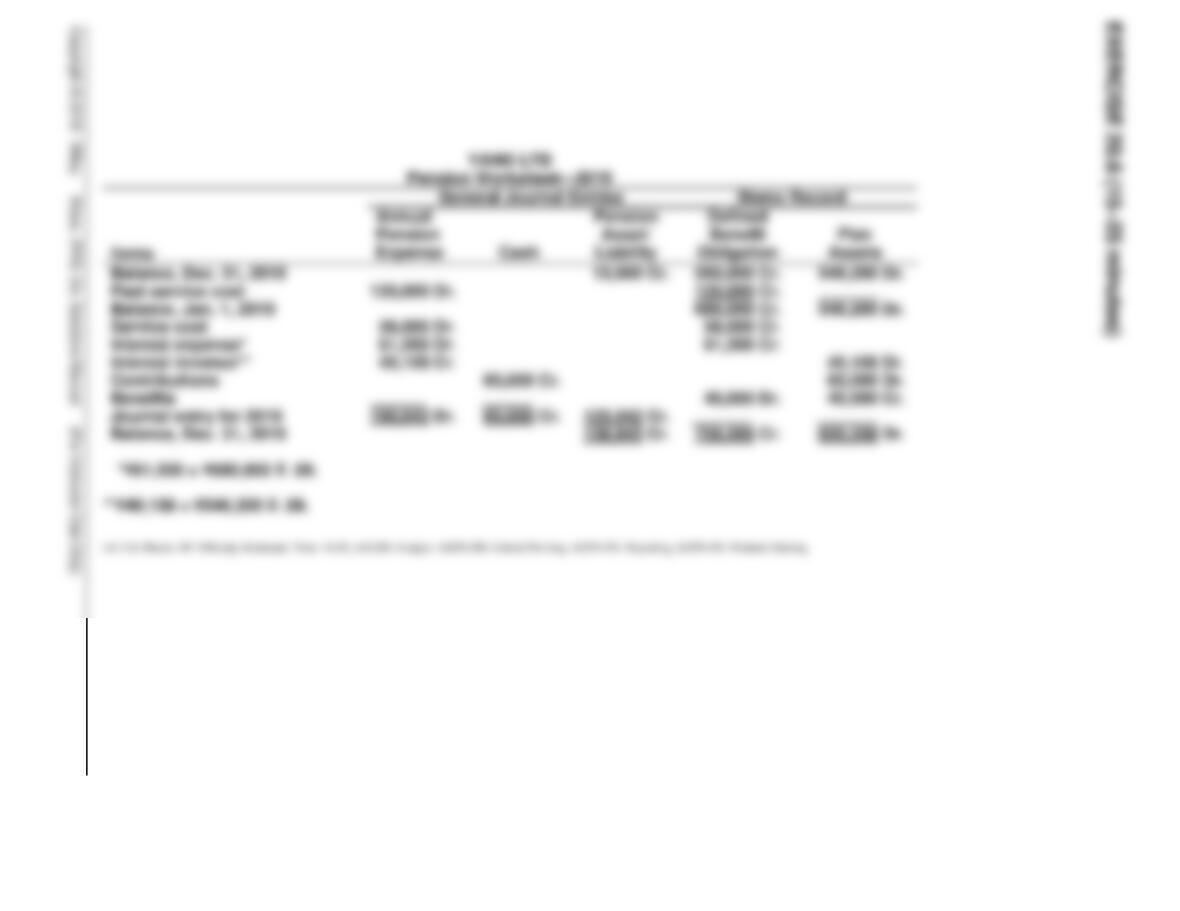

EXERCISE 20.3 (15–25 minutes)

VELDRE SpA

Pension Worksheet—2019

General Journal Entries

Memo Record

Items

Annual

Pension

Expense

Cash

Pension

Asset/Liability

Defined

Benefit

Obligation

Plan Assets

Balance, January 1, 2019

60,000 Cr.

700,000 Cr.

640,000 Dr.

Service cost

Interest expense*

Interest revenue**

Contributions

105,000 Dr.

Benefits

Journal entry for 2019***

Balance, Dec. 31, 2019

51,000 Cr.

820,000 Cr.

769,000 Dr.

*£39,200 = £490,000 X 8%.

**£39,200 = £490,000 X 8%.

LO: 2, Bloom: AP, Difficulty: Simple, Time: 10-15, AACSB: Analytic, AICPA BB: Critical Thinking, AICPA FC: Reporting, AICPA PC: Problem Solving

EXERCISE 20.5 (10–15 minutes)

(a) Computation of Actual Return on Plan Assets

Fair value of plan assets at 12/31/19 ………………….. ₺ 2,725,000

Fair value of plan assets at 1/1/19 ……………………… (2,400,000)

EXERCISE 20.7 (20–25 minutes)

(a)

EXERCISE 20.7 (Continued)

(b) Pension Expense ……………………………………………….. 218,000

OCI – G/L …………………………………………………………… 137,000

EXERCISE 20.8 (25–35 minutes)

(a) Note to financial statements disclosing components of 2019 pension

expense:

Note X: Net pension expense for 2019 is composed of the following