PROBLEM 8.4 (Continued)

3. Average cost.

Cost of Part X available.

Date of Invoice

No. Units

Unit Cost

Total Cost

April 1

100

R$5.00

R$ 500

April 4

400

April 11

April 18

200

April 26

600

April 30

200

(b) Assuming costs are computed for each withdrawal:

1. Specific identification.

2. First-in, first out.

PROBLEM 8.4 (Continued)

3. Average cost.

Purchased

Sold

Balance

Date

No. of

units

Unit

cost

No. of

units

Unit

cost

No. of

units

Unit

cost*

Amount

April 1

100

R$5.00

100

R$5.0000

R$ 500.00

April 4

400

5.10

500

5.0800

2,540.00

April 5

200

5.0800

1,016.00

April 11

300

5.30

500

5.2120

2,606.00

April 12

300

5.2120

1,563.60

April 18

200

5.35

500

5.2672

2,633.60

April 26

600

5.60

1,100

5.4487

5,993.60

April 27

300

5.4487

1,634.64

April 28

150

5.4487

April 30

200

5.80

350

5.6495

1,977.31

PROBLEM 8.5

(a) Assuming costs are not computed for each withdrawal (units received,

5,700, minus units issued, 4,700, equals ending inventory at 1,000 units):

1. First-in, first-out.

2. Average cost.

Cost of goods available:

Date of Invoice

No. Units

Unit Cost

Total Cost

Jan. 2

1,200

¥3.00

¥ 3,600

Jan. 10

600

3.20

1,920

Jan. 18

1,000

3.30

3,300

Jan. 23

1,300

3.40

4,420

Jan. 28

1,600

3.50

5,600

(b) Assuming costs are computed at the time of each withdrawal:

Under FIFO—Yes. The amount shown as ending inventory would be

PROBLEM 8.5 (Continued)

The calculations to determine the inventory on this basis are given below.

1. First-in, first-out.

2. Average cost.

Received

Issued

Balance

Date

No. of

units

Unit

cost

No. of

units

Unit

cost

No. of

units

Unit

cost*

Amount

Jan. 2

1,200

¥3.00

1,200

¥3.0000

¥3,600

Jan. 7

700

$3.0000

500

3.0000

1,500

Jan. 13

500

600

3.1091

1,865

Jan. 18

1,000

300

1,300

3.2281

4,197

Jan. 23

1,300

3.3773

5,066

Jan. 26

800

700

3.3773

2,364

Jan. 31

1,300

1,000

3.4626

3,463

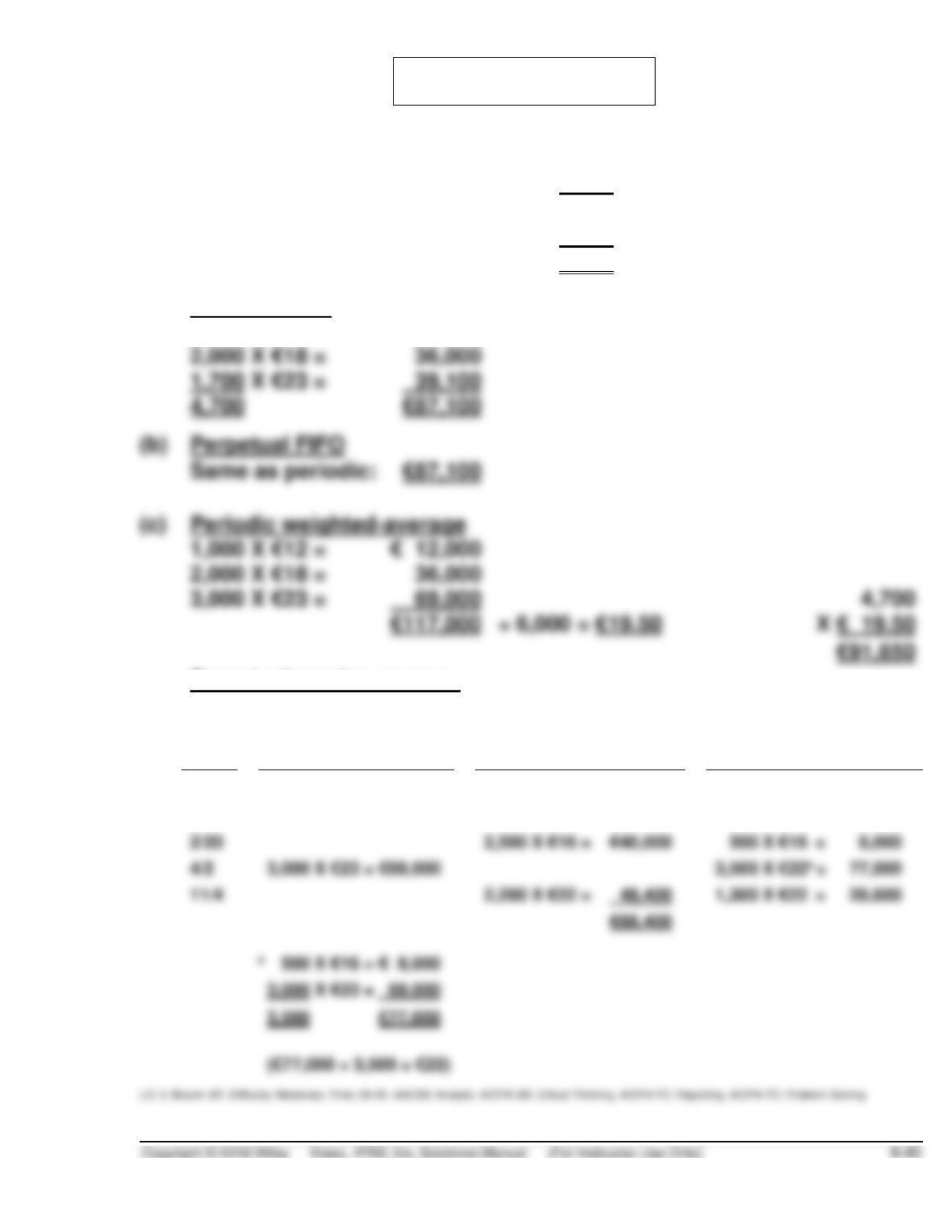

PROBLEM 8.6

(a)

Beginning inventory …………………

1,000

Purchases (2,000 + 3,000) ………….

5,000

Units available for sale ……………..

6,000

Sales (2,500 + 2,200) …………………

4,700

Goods on hand …………………………

1,300

Periodic FIFO

1,000 X €12 =

€12,000

2,000 X €18 =

1,700 X €23 =

(b)

Perpetual FIFO

(c)

Periodic weighted-average

1,000 X €12 =

2,000 X €18 =

3,000 X €23 =

(d)

Perpetual moving average

Date

Purchased

Sold

Balance

1/1

1,000 X €12 =

€12,000

2/4

2,000 X €18 = €36,000

3,000 X €16 =

48,000

2/20

2,500 X €16 =

€40,000

500 X €16 =

8,000

4/2

3,000 X €23 = €69,000

3,500 X €22a =

77,000

€88,400

3,000 X €23 = 69,000

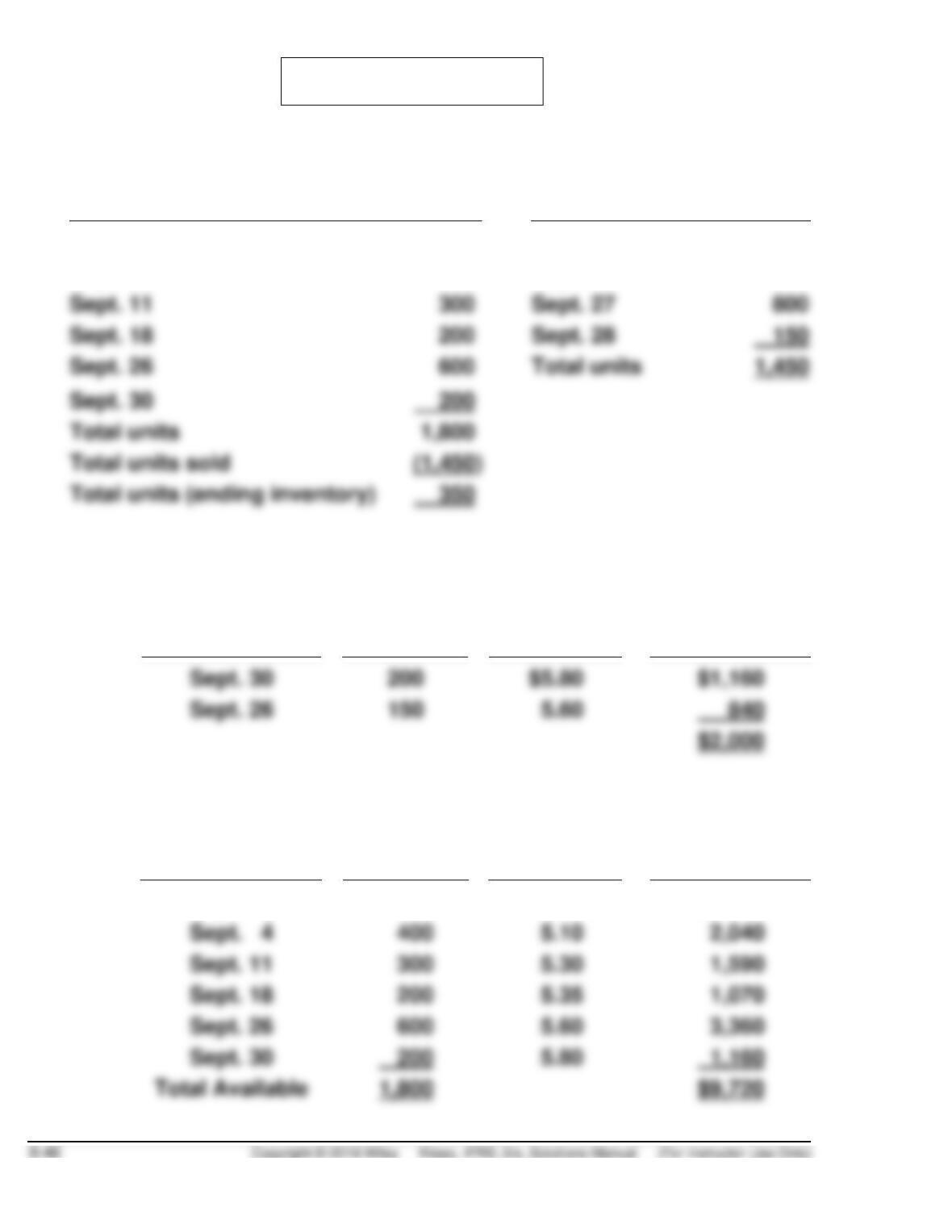

*PROBLEM 8.7

(a)

Purchases

Total Units

Sales

Total Units

Sept. 1 (balance on hand)

100

Sept. 5

300

Sept. 4

400

Sept. 12

200

Sept. 11

300

Sept. 27

800

Sept. 18

200

Sept. 28

Sept. 30

200

Total units

Total units sold

(1,450)

Assuming costs are not computed for each withdrawal:

1. First-in, first-out.

Date of Invoice

No. Units

Unit Cost

Total Cost

Sept. 30

$5.80

$1,160

Sept. 26

840

2. Average cost.

Cost of Part X available.

Date of Invoice

No. Units

Unit Cost

Total Cost

Sept. 1

100

$5.00

$ 500

Sept. 4

400

Sept. 11

300

Sept. 18

200

Sept. 26

600

Sept. 30

200

*PROBLEM 8.7 (Continued)

3. Under LIFO,

100 units @ 5.00 = 500

(b) Assuming costs are computed for each withdrawal:

1. First-in, first out.

2. Average cost.

Purchased

Sold

Balance

Date

No. of

units

Unit

cost

No. of

units

Unit

cost

No. of

units

Unit

cost*

Amount

Sept. 1

100

$5.00

100

$5.0000

$ 500.00

Sept. 4

400

5.10

500

5.0800

2,540.00

Sept. 5

200

5.0800

1,016.00

Sept. 11

300

5.30

500

5.2120

2,606.00

Sept. 12

300

5.2120

1,563.60

Sept. 18

200

5.35

500

5.2672

2,633.60

Sept. 26

600

5.60

1,100

5.4487

5,993.60

Sept. 27

300

5.4487

1,634.64

Sept. 28

150

5.4487

817.33

Sept. 30

200

5.80

350

5.6495

1,977.33

*PROBLEM 8.7 (Continued)

Inventory Sept. 30 is $1,915.

*The balance on hand is listed in detail after each transaction.

3. Note: If LIFO kept in units and dollars, LIFO inventory would be:

Purchased

Sold

Balance*

Date

No. of

units

Unit

cost

No. of

units

Unit

cost

No. of

units

Unit

cost

Amount

Sept. 1

100

$5.00

100

$5.00

$ 500

Sept. 4

400

5.10

100

5.00

2,540

400

5.10

Sept. 5

300

$5.10

100

5.00

100

5.10

Sept. 11

300

5.30

100

5.00

100

5.10

2,600

300

5.30

Sept. 12

200

5.30

100

5.00

100

5.10

1,540

100

5.30

Sept. 18

200

5.35

100

5.00

100

5.10

2,610

100

5.30

200

5.35

Sept. 26

600

5.60

100

5.00

100

5.10

100

5.30

5,970

200

5.35

600

5.60

Sept. 27

600

5.60

800

5.35

100

5.00

100

5.10

1,540

100

5.30

Sept. 28

5.30

100

5.00

150

50

5.10

50

5.10

Sept. 30

200

5.80

100

5.00

50

5.10

200

5.80

*PROBLEM 8.8

(a) Assuming costs are not computed for each withdrawal (units received,

5,700, minus units issued, 4,700, equals ending inventory at 1,000 units):

1. First-in, first-out.

Date of Invoice

No. Units

Unit Cost

Total Cost

Jan. 28

1,000

$3.50

$3,500

1,000

$3.00

$3,000

3. Average cost.

Cost of goods available:

Date of Invoice

No. Units

Unit Cost

Total Cost

Jan. 2

1,200

$3.00

$ 3,600

Jan. 10

600

3.20

1,920

Jan. 18

1,000

3.30

3,300

Jan. 23

1,300

3.40

4,420

Jan. 28

1,600

3.50

5,600

(b) Assuming costs are computed at the time of each withdrawal:

*PROBLEM 8.8 (Continued)

Under Average Cost—No. A new average cost would be computed

The calculations to determine the inventory on this basis are given below.

1. First-in, first-out.

2. Last-in, first-out.

Received

Issued

Balance

Date

No. of

units

Unit

cost

No. of

units

Unit

cost

No. of

units

Unit

cost*

Amount

Jan. 2

1,200

$3.00

1,200

$3.00

$3,600

Jan. 7

700

$3.00

500

3.00

1,500

Jan. 10

600

3.20

500

3.00

600

Jan. 13

500

3.20

500

3.00

100

3.20

Jan. 18

1,000

3.30

300

3.30

500

3.00

100

4,130

700

3.30

Jan. 20

700

3.30

100

3.20

300

3.00

200

3.00

600

Jan. 23

1,300

3.40

200

3.00

5,020

1,300

3.40

Jan. 26

800

3.40

200

500

3.40

Jan. 28

1,600

3.50

200

3.00

500

3.40

7,900

1,600

Jan. 31

1,300

3.50

200

3.00

500

3.40

3,350

300

Inventory, January 31 is $3,350.

*PROBLEM 8.8 (Continued)

3. Average cost.

Received

Issued

Balance

Date

No. of

units

Unit

cost

No. of

units

Unit

cost

No. of

units

Unit

cost*

Amount

Jan. 2

1,200

$3.00

1,200

$3.0000

$3,600

Jan. 7

700

$3.0000

500

3.0000

1,500

Jan. 10

600

3.20

1,100

3.1091

3,420

Jan. 13

500

600

3.1091

1,865

Jan. 18

300

1,300

3.2281

4,197

Jan. 20

1,100

200

3.2281

646

Jan. 23

1,300

3.40

1,500

3.3773

5,066

Jan. 26

800

700

3.3773

2,364

Jan. 28

1,600

3.50

2,300

3.4626

7,964

Jan. 31

1,300

1,000

3.4626

3,463

*PROBLEM 8.9

(a)

Beginning inventory ………………….

1,000

Purchases (2,000 + 3,000) ………….

5,000

Units available for sale ……………..

6,000

Sales (2,500 + 2,200) …………………

4,700

Goods on hand …………………………

1,000 X NT$12 =

2,000 X NT$18 =

1,700 X NT$23 =

4,700

NT$87,100

(b)

Perpetual FIFO

Same as periodic:

NT$87,100

(c)

Periodic LIFO

3,000 X NT$23 =

1,700 X NT$18 =

4,700

NT$99,600

(d)

Perpetual LIFO

Date

Purchased

Sold

Balance

1/1

1,000 X NT$12

=

NT$12,000

2/4

2,000 X NT$18 = NT$36,000

1,000 X NT$12

2,000 X NT$18

2/20

2,000 X NT$18

=

4/2

3,000 X NT$23 = NT$69,000

3,000 X NT$23

11/4

2,200 X NT$23

=

*PROBLEM 8.9 (Continued)

(e)

Periodic weighted-average

1,000 X NT$12 =

NT$ 12,000

2,000 X NT$18 =

3,000 X NT$23 =

(f)

Perpetual moving-average

Date

Purchased

Sold

Balance

1/1

1,000 X NT$12 =

NT$12,000

2/4

2,000 X NT$18 = $36,000

3,000 X NT$16 =

48,000

2/20

2,500 X NT$16 =

NT$40,000

8,000

4/2

3,000 X NT$23 = $69,000

3,500 X NT$22a =

11/4

2,200 X NT$22 =

1,300 X NT$22 =

NT$88,400

3,000 X NT$23 = 69,000