CHAPTER 3

The Accounting Information System

ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC)

Topics

Questions

Brief

Exercises

Exercises

Problems

1.

Transaction

identification.

1, 2, 3, 5

1, 2

1, 3, 4, 17

1

2.

Nominal accounts.

4, 7

3.

Trial balance.

6, 10

2, 3, 4

1, 2, 7

4.

Adjusting entries.

8, 11, 13, 14

3, 4, 5, 6, 7,

8, 9, 10

5, 6, 7, 8,

9, 10, 20

1, 2, 3, 4, 5, 6,

7, 8, 9, 11

5.

Financial statements.

11, 12, 15,

22, 23

1, 2, 4, 6, 7, 11

6.

Closing.

13, 14, 16

1, 4, 8, 9, 11

7.

Inventory and cost

of goods sold.

9

12, 14, 15

8.

Comprehensive

accounting cycle.

1, 2, 6, 11

*9.

Cash vs. accrual basis.

15, 16, 17

18, 19

*10.

Reversing entries.

*11.

Worksheet.

21, 22, 23

ASSIGNMENT CLASSIFICATION TABLE (BY LEARNING OBJECTIVE)

Learning Objectives

Questions

Brief

Exercises

Exercises

Problems

1. Describe the basic accounting

information system.

1, 2, 3,

4, 5, 7

2. Record and summarize basic

transactions.

3, 6

1, 2, 3, 4,

5, 6, 7

1, 2, 3,

4, 9, 17

1, 4

8, 11,

13, 14

3, 4, 5, 6,

7, 8, 9, 10

5, 6, 7, 8,

9, 10, 20

1, 2, 3, 4, 5,

6, 7, 8, 9,

5. Prepare financial statements for a

merchandising company.

9

13, 15

4

*6. Differentiate the cash basis of

accounting from the accrual basis of

accounting.

15, 16,

17

12

18, 19

10

reversed.

18

13

21, 22, 23

ASSIGNMENT CHARACTERISTICS TABLE

Item

Description

Level of

Difficulty

Time

(minutes)

E3.1

Transaction analysis–service company.

Simple

15–20

E3.2

Corrected trial balance.

Simple

10–15

E3.3

Corrected trial balance.

Simple

15–20

E3.4

Corrected trial balance.

10–15

E3.5

Adjusting entries.

Moderate

10–15

E3.6

Adjusting entries.

Moderate

15–20

E3.7

Analyze adjusted data.

Complex

15–20

E3.8

Adjusting entries.

Moderate

10–15

E3.9

Adjusting entries.

Moderate

15–20

E3.10

Adjusting entries.

Complex

25–30

E3.11

Prepare financial statements.

Moderate

20–25

E3.12

Prepare financial statements.

Moderate

20–25

E3.13

Closing entries.

Simple

10–15

E3.14

Closing entries.

Moderate

10–15

E3.15

Missing amounts.

Simple

10–15

E3.16

Closing entries for a corporation.

Moderate

10–15

Transactions of a corporation, including investment

and dividend.

Cash to accrual basis.

Moderate

15–20

Cash to accrual basis.

Moderate

10–15

Worksheet.

Simple

10–15

Worksheet and statement of financial position

presentation.

Partial worksheet preparation.

Moderate

10–15

P3.1

Transactions, financial statements–service company.

Moderate

25–35

P3.2

Adjusting entries and financial statements.

Moderate

35–40

P3.3

Adjusting entries.

Moderate

25–30

P3.4

Financial statements, adjusting and closing entries.

Moderate

40–50

P3.5

Adjusting entries.

Moderate

15–20

P3.6

Adjusting entries and financial statements.

Moderate

25–35

P3.7

Adjusting entries and financial statements.

Moderate

25–35

Adjusting and closing.

Moderate

30–40

Adjusting and closing.

Moderate

30–35

Cash and accrual basis.

Moderate

35–40

Worksheet, statement of financial position, adjusting and

closing entries.

ANSWERS TO QUESTIONS

1. Examples are:

(a) Payment of an accounts payable.

2. Transactions (a), (b), (d) are considered business transactions and are recorded in the accounting

records because a change in assets, liabilities, or equity has been effected as a result of a transfer

3. Transaction (a): Accounts Receivable (debit), Service Revenue (credit).

Transaction (b): Cash (debit), Accounts Receivable (credit).

4. Revenue and expense accounts are referred to as temporary or nominal accounts because each

period they are closed out to Income Summary in the closing process. Their balances are reduced

5. Andrea is not correct. The double-entry system means that for every debit amount there must be a

6. Although it is not absolutely necessary that a trial balance be taken periodically, it is customary

and desirable. The trial balance accomplishes two principal purposes:

(1) It tests the accuracy of the entries in that it proves that debits and credits of an equal amount

LO: 2, Bloom: C, Difficulty: Simple, Time: 3-5, AACSB: None, AICPA BB: None, AICPA FC: Reporting, AICPA PC: Communication

7. (a) Real account; statement of financial position.

(b) Real account; statement of financial position.

(c) Inventory is generally considered a real account appearing on the statement of financial position. It

Questions Chapter 3 (Continued)

8. At December 31, the three days’ salaries and wages due to the employees represent a current

9. (a) In a service company, revenues are service revenues and expenses are operating expenses.

In a merchandising company, revenues are sales revenues and expenses consist of cost of

10. (a) No change.

(b) Before closing, balances exist in these accounts; after closing, no balances exist.

11. Adjusting entries are prepared prior to the preparation of financial statements in order to bring the

accounts up to date and are necessary (1) to achieve a proper recognition of revenues and

12. Closing entries are prepared to transfer the balances of nominal accounts to capital (retained

earnings) after the adjusting entries have been recorded and the financial statements prepared.

13. Cost – Residual Value = Depreciable Cost: €4,000 – $0 = €4,000. Depreciable Cost ÷ Useful Life =

Depreciation Expense for One Year €4,000 ÷ 5 years = €800 per year. The asset was used for

14.

December 31

Interest Receivable ……………………………………………………………………………………

10,000

Interest Revenue ……………………………………………………………………………………

(To record accrued interest revenue on loan)

Questions Chapter 3 (Continued)

*15. Under the cash basis of accounting, revenue is recorded only when cash is received and

expenses are recorded only when paid. Under the accrual basis of accounting, revenue is

recognized when a performance obligation is satisfied and expenses are recognized when

*16. Salaries and wages paid during the year will include the payment of any salaries and wages

attributable to the prior year but unpaid at the end of the prior year. This amount is an expense of

*17. Although similar to the strict cash basis, the modified cash basis of accounting requires that

expenditures for capital items be charged against income over all the periods to be benefited. This

*18. Reversing entries are made at the beginning of the period to reverse accruals and some deferrals.

Reversing entries are not required. They are made to simplify the recording of certain transactions

*19. Disagree. A worksheet is not a permanent accounting record and its use is not required in the ac–

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 3.1

May

1

Cash ……………………………………………………………………………………

4,000

Share Capital-Ordinary …………………………..

4,000

3

Equipment ……………………………………………………….

1,100

Accounts Payable ……………………………………………………….

1,100

Rent Expense ……………………………………………………….

Cash ……………………………………………………….

Accounts Receivable ……………………………………………………….

Service Revenue ……………………………………………………….

BRIEF EXERCISE 3.2

Aug.

2

Cash ……………………………………………………………………………………

12,000

Equipment ……………………………………………………….

2,500

Agazzi, Capital ……………………………………………………….

14,500

7

Supplies ……………………………………………………….

Accounts Payable ……………………………………………………….

Cash ……………………………………………………………………………………

Accounts Receivable ……………………………………………………….

Service Revenue ……………………………………………………….

1,970

BRIEF EXERCISE 3.2 (Continued)

15

Rent Expense ……………………………………………………….

600

Cash ……………………………………………………….

19

Supplies Expense ……………………………………………………….

230

Supplies (€500 – €270) …………………………..

BRIEF EXERCISE 3.3

July

1

Prepaid Insurance ……………………………………………………….

15,000

Cash ……………………………………………………….

15,000

Dec.

31

Insurance Expense ……………………………………………………….

Prepaid Insurance

(€15,000 X 1/2 X 1/3) …………………………..

BRIEF EXERCISE 3.4

July

1

Cash ……………………………………………………………………………………

15,000

Unearned Insurance Revenue …………………………..

15,000

Insurance Revenue

(€15,000 X 1/2 X 1/3) …………………………..

BRIEF EXERCISE 3.5

Feb.

1

Prepaid Insurance ……………………………………………………….

72,000

Cash ……………………………………………………….

72,000

June

30

Insurance Expense ……………………………………………………….

15,000

Prepaid Insurance

(£72,000 X 5/24) ……………………………………………………….

15,000

BRIEF EXERCISE 3.6

Nov.

1

Cash ……………………………………………………………………………………

2,400

Unearned Rent Revenue …………………………..

2,400

Dec.

31

Unearned Rent Revenue ……………………………………………………….

1,600

Rent Revenue

(€2,400 X 2/3) ……………………………………………………….

1,600

BRIEF EXERCISE 3.7

Dec.

31

Salaries and Wages Expense …………………………..

4,800

Salaries and Wages Payable

(€8,000 X 3/5) ……………………………………………………….

4,800

Jan.

2

Salaries and Wages Payable …………………………..

4,800

Salaries and Wages Expense* …………………………..

3,200

Cash ……………………………………………………….

8,000

BRIEF EXERCISE 3.8

Dec.

31

Interest Receivable ……………………………………………………….

300

Interest Revenue ……………………………………………………….

300

Feb.

Cash ……………………………………………………………………………………

Notes Receivable ……………………………………………………….

Interest Receivable ……………………………………………………….

300

Interest Revenue (€12,000 X 10% X 1/12) …………………………..

100

BRIEF EXERCISE 3.9

Aug.

31

Interest Expense …………………………..…………………………..

300

Interest Payable ……………………………………………………….

300

31

Accounts Receivable …………………………..…………………………..

Service Revenue ……………………………………………………….

31

Salaries and Wages Expense …………………………..

700

Salaries and Wages Payable …………………………..

700

31

Bad Debt Expense ……………………………………………………….

900

Allowance for Doubtful Accounts …………………………..

900

BRIEF EXERCISE 3.10

Depreciation Expense ……………………………………………………….

2,000

Accumulated Depreciation—Equipment …………………………..

2,000

Equipment ……………………………………………………….……………………..

Less: Accumulated Depreciation—Equipment …………………………

BRIEF EXERCISE 3.11

Sales Revenue ……………………………………………………….

808,900

Interest Revenue …………………………..…………………………..

13,500

Income Summary ……………………………………………………….

822,400

Income Summary ……………………………………………………….

780,300

Cost of Goods Sold……………………………………………………….

556,200

Operating Expenses ……………………………………………………….

189,000

Income Tax Expense ……………………………………………………….

Income Summary ……………………………………………………….

42,100

Retained Earnings ……………………………………………………….

Retained Earnings ……………………………………………………….

18,900

Dividends ……………………………………………………….

*BRIEF EXERCISE 3.12

(a)

Cash receipts from customers …………………………..

$142,000

+ Increase in accounts receivable

(€18,600 – €13,000) ……………………………………………………….

5,600

Service revenue …………………………..…………………………..

$147,600

(b)

Payments for operating expenses …………………………..

$ 97,000

(€23,200 – €17,500) ……………………………………………………….

Operating expenses ……………………………………………………….

$ 91,300

*BRIEF EXERCISE 3.13

(a)

Salaries and Wages Payable …………………………………………………….

4,200

Salaries and Wages Expense …………………………..

4,200

(b)

Salaries and Wages Expense …………………………..

7,000

Cash ……………………………………………………….

7,000

(c)

Salaries and Wages Payable …………………………………………………….

4,200

Salaries and Wages Expense (7,000 – 4,200) …………………………..

2,800

Cash ……………………………………………………….

7,000

SOLUTIONS TO EXERCISES

EXERCISE 3.1 (15–20 minutes)

Apr.

2

Cash ……………………………………………………………………………………

30,000

Equipment ……………………………………………………….

14,000

Kai Edo, Capital ……………………………………………………….

44,000

2

3

Supplies ……………………………………………………….

Accounts Payable ……………………………………………………….

7

Rent Expense ……………………………………………………….

Cash ……………………………………………………….

11

Accounts Receivable ……………………………………………………….

1,100

Service Revenue ……………………………………………………….

1,100

12

Cash ……………………………………………………………………………………

3,200

Unearned Service Revenue …………………………..

3,200

17

Cash ……………………………………………………………………………………

2,300

Service Revenue ……………………………………………………….

2,300

21

Insurance Expense……………………………………………………….

Cash ……………………………………………………….

30

Salaries and Wages Expense …………………………..

1,160

Cash ……………………………………………………….

1,160

EXERCISE 3.1 (Continued)

30

Supplies Expense ……………………………………………………….

120

Supplies ……………………………………………………….

120

30

Equipment ……………………………………………………….

Kai Edo, Capital ……………………………………………………….

EXERCISE 3.2 (10–15 minutes)

GERONIMO AG

Trial Balance

April 30, 2019

Debit

Credit

Cash ………………………………………………………………

€ 2,100

Accounts Receivable ………………………………………

2,750

Prepaid Insurance (€700 + €1,000) ……………………

1,700

Equipment ………………………………………………………

8,000

Accounts Payable (€4,500 – €1,000) ………………….

Property Tax Payable ………………………………………

Geronimo, Capital (€11,200 + €3,200) ………………..

Geronimo, Drawing …………………………………………

3,200

Service Revenue ……………………………………………..

Salaries and Wages Expense …………………………..

4,200

Advertising Expense (€1,100 + €300) ………………..

1,400

Property Tax Expense (€800 + €1,000) ………………

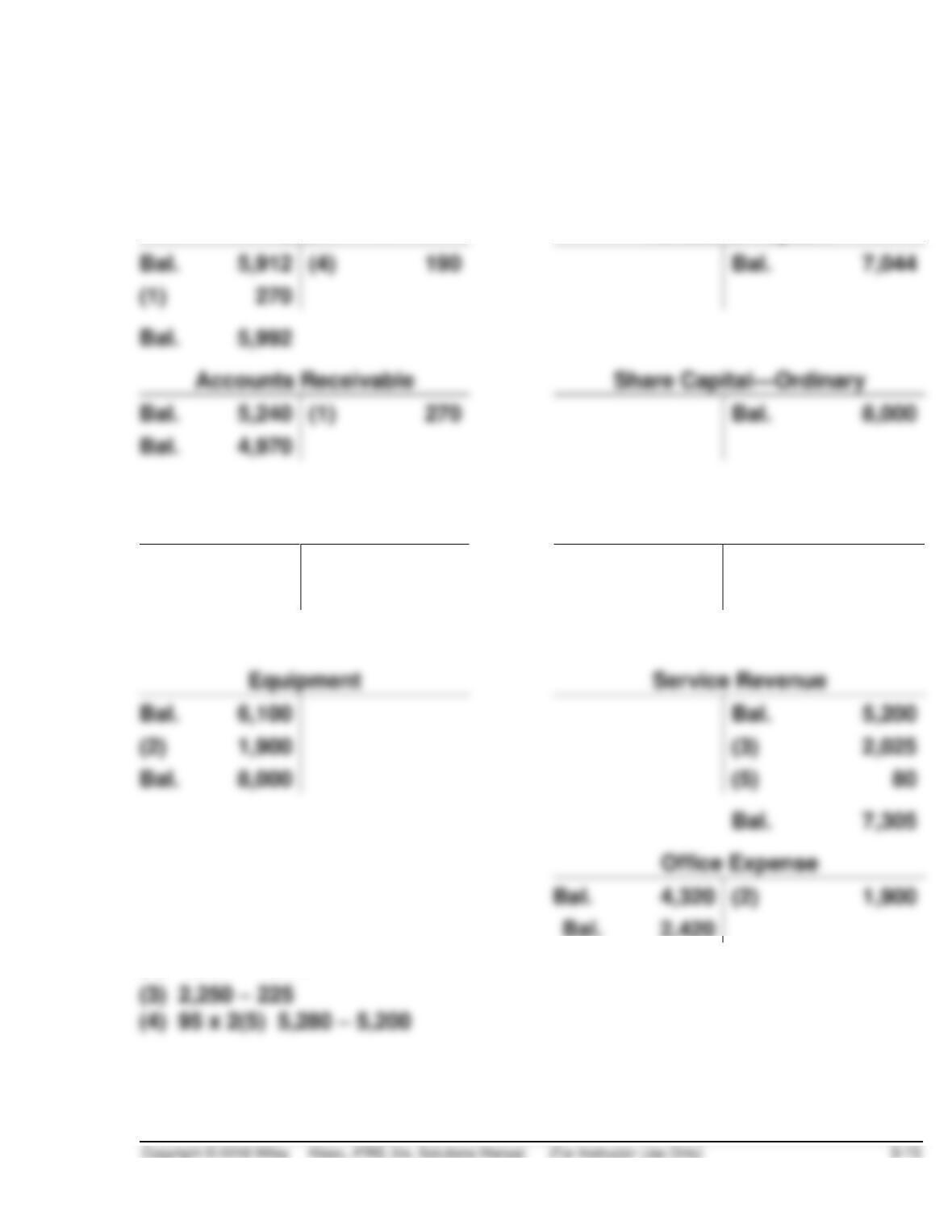

EXERCISE 3.3 (15–20 minutes)

The ledger accounts are reproduced below, and corrections are shown in

the accounts.

Cash

Accounts Payable

Bal.

5,912

(4)

Bal.

7,044

(1)

Accounts Receivable

Bal.

5,240

(1)

Bal.

8,000

Bal.

4,970

Supplies

Retained Earnings

Bal.

2,967

Bal.

2,000

Bal.

6,100

Bal.

(2)

1,900

(3)

2,025

Bal.

8,000

(5)

Bal.

4,320

(2)

1,900

Bal.

2,420

(1) 1,850 – 1,580

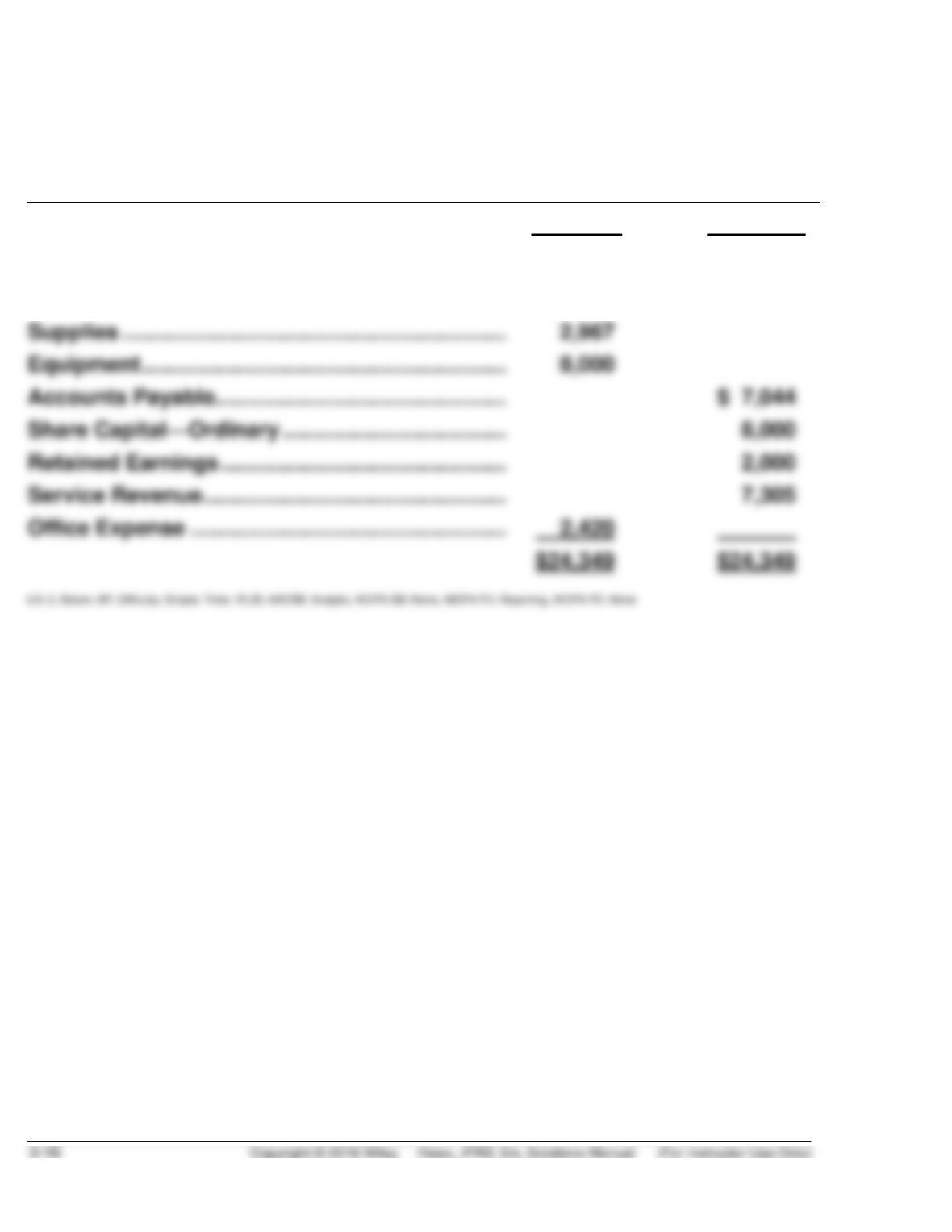

EXERCISE 3.3 (Continued)

SCARLATTI CORPORATION

Trial Balance (Corrected)

April 30, 2019

Debit

Credit

Cash ……………………………………………………………….

$ 5,992

Accounts Receivable ……………………………………….

4,970

Supplies ……………………………………………………….

2,967

Equipment ……………………………………………………….

8,000

Accounts Payable…………………………………………….

$ 7,044

Share Capital—Ordinary …………………………………..

Retained Earnings ……………………………………………

Service Revenue ………………………………………………

Office Expense ………………………………………………..

2,420

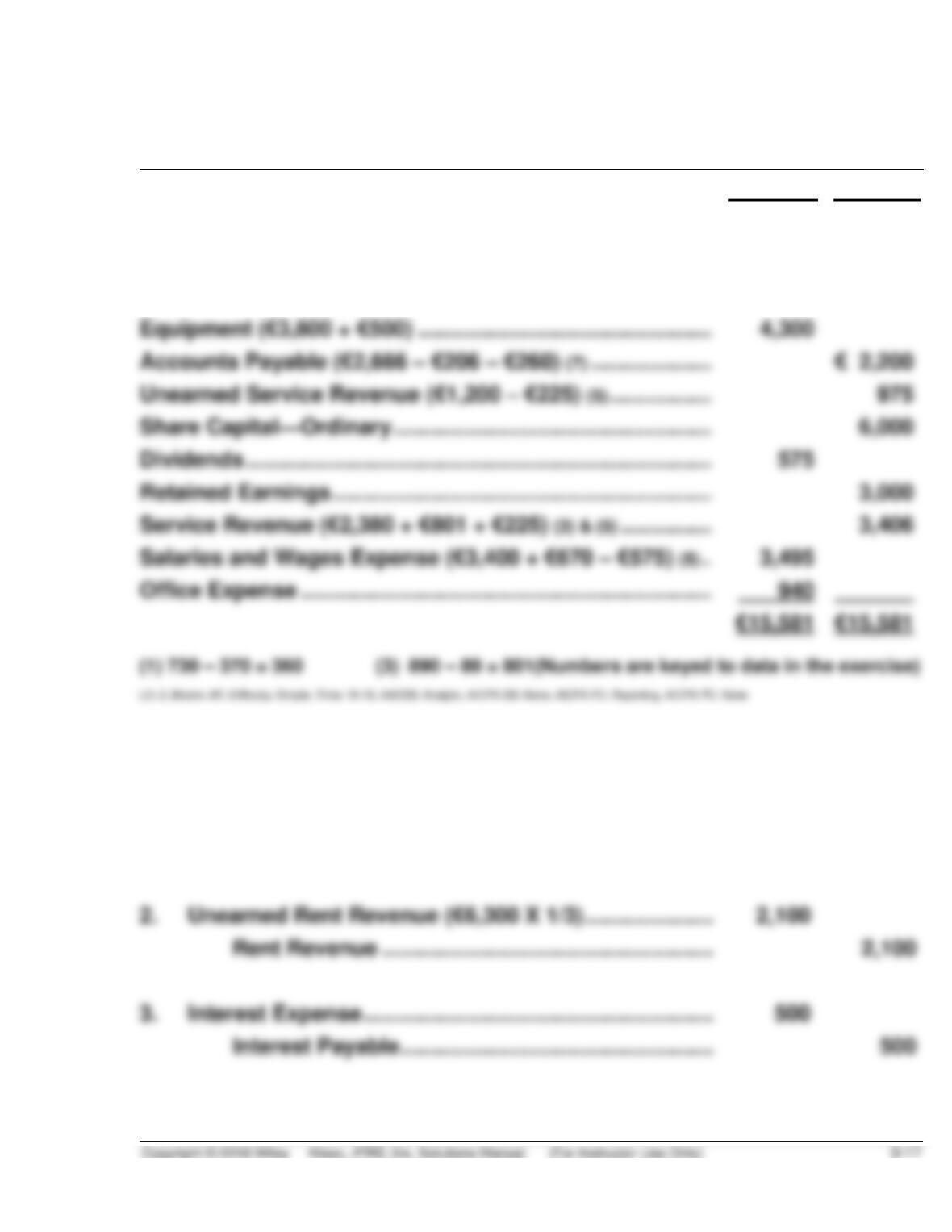

EXERCISE 3.4 (15–20 minutes)

OAKLEY NV

Trial Balance

June 30, 2019

Debit

Credit

Cash (€2,870 + €360 – €65 – €65) (1) & (4) ………………………….

€ 3,100

Accounts Receivable (€3,231 – €360) …………………………..

2,871

Supplies (€800 – €500) (2) ………………………………………………..

300

Equipment (€3,800 + €500) ……………………………………………..

4,300

Accounts Payable (€2,666 – €206 – €260) (7) …………………….

Unearned Service Revenue (€1,200 – €225) (5) ………………….

Share Capital—Ordinary …………………………………………………

Dividends ………………………………………………………………………

575

Retained Earnings ……………………………………………………….

Service Revenue (€2,380 + €801 + €225) (3) & (5) ………………..

Salaries and Wages Expense (€3,400 + €670 – €575) (5) …….

3,495

Office Expense ………………………………………………………………

EXERCISE 3.5 (10–15 minutes)

1.

Depreciation Expense (€250 X 3) …………………………..

750

Accumulated Depreciation—Equipment …………………………..

750

2.

Unearned Rent Revenue (€6,300 X 1/3) …………………………..

Rent Revenue …………………………..…………………………..

3.

Interest Expense ……………………………………………………….

500

Interest Payable ……………………………………………………….

500

EXERCISE 3.5 (Continued)

4.

Supplies Expense …………………………..…………………………..

2,150

Supplies (€2,800 – €650) ……………………………………………………

2,150

5.

Insurance Expense (€300 X 3) ………………………………………………….

Prepaid Insurance ……………………………………………………….

900

EXERCISE 3.6 (10–15 minutes)

1.

Accounts Receivable ……………………………………………………….

750

Service Revenue ……………………………………………………….

750

2.

Utilities Expense ……………………………………………………….

520

Accounts Payable ……………………………………………………….

520

3.

Depreciation Expense ……………………………………………………….

400

Accumulated Depreciation—Equipment …………………………..

400

Interest Expense ……………………………………………………….

500

Interest Payable ……………………………………………………….

500

4.

Insurance Expense ($15,000 X 1/12) …………………………..

Prepaid Insurance ……………………………………………………….

1,250

5.

Supplies Expense ($1,600 – $400) …………………………..

Supplies ……………………………………………………….

1,200

EXERCISE 3.7 (15–20 minutes)

(a)

Ending balance of supplies …………………………...

£ 900

Add: Adjusting entry …………………………………….

950

Deduct: Purchases …………………………..…………..

850

Beginning balance of supplies ……………………….

£1,000

(b)

Total prepaid insurance (£400 X 12) ……………….

Amount used (6 X £400)…………………………………

2,400

(c)

The entry in January to record salaries paid was

Salaries and Wages Expense …………………………..

Salaries and Wages Payable …………………………..

Cash ……………………………………………………….

The “T” account for salaries and Wages payable is

Salaries and Wages Payable

Paid

900

Beg. Bal.

?

January

End Bal.

800

The beginning balance is therefore

and Wages Payable …………………………………………….

Plus: Reduction of Salaries

and Wages Payable ……………………………………………..

and Wages Payable ……………………………………………..

Ending balance of Salaries

EXERCISE 3.7 (Continued)

(d)

Service revenue …………………………..………..

£2,000

Cash received ……………………………………….

Ending Unearned revenue January 31, 2019 …………….

Plus: Unearned service revenue reduced ………………..

EXERCISE 3.8 (10–15 minutes)

(1)

Salaries and Wages Expense …………………………………………………..

2,900

Salaries and Wages Payable ……………………………………………..

2,900

Accounts Payable ……………………………………………………….

(3)

Interest Expense ($60,000 X 8% X 1/12) …………………………..

Interest Payable ……………………………………………………….

(4)

Telephone and Internet Expense ………………………………………………

Accounts Payable ……………………………………………………….