*PROBLEM 17.12

(a) July 7, 2019

Call Option …………………………………………………….. 240

(b) September 30, 2019

Call Option …………………………………………………….. 1,400

(c) December 31, 2019

Unrealized Holding Gain or Loss—Income ……….. 400

Call Option (€2 X 200) ……………………………….. 400

Call Option (€180 – €65) …………………………….. 115

(d) January 4, 2020

Call Option (€1 X 200) ……………………………………… 200

Unrealized Holding Gain or Loss—Income …. 200

*Value of Call Option at Settlement:

Call Option

240

200

*PROBLEM 17.13

(a) July 7, 2019

Put Option ………………………………………………………. 240

Cash …………………………………………………………. 240

(b) September 30, 2019

(c) December 31, 2019

Unrealized Holding Gain or Loss—Income ………… 75

Put Option (€125 – €50) ………………………………. 75

*PROBLEM 17.14

(a) January 7, 2019

Put Option ……………………………………………………… 360

Cash ………………………………………………………… 360

(b) March 31, 2019

Put Option ……………………………………………………… 2,000

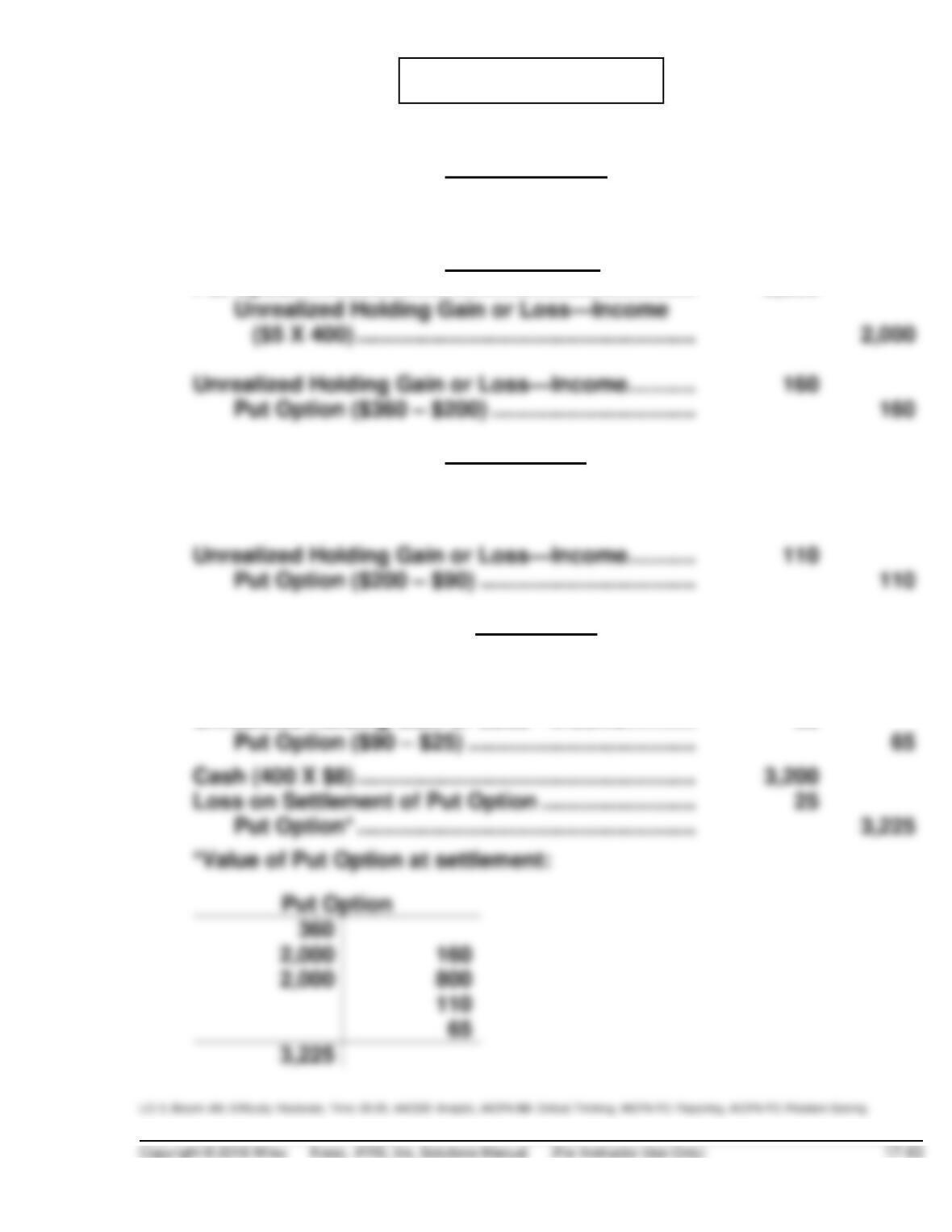

(c) June 30, 2019

Unrealized Holding Gain or Loss—Income ……….. 800

Put Option ($2 X 400) ………………………………… 800

(d) July 6, 2019

Put Option ($5 X 400) ………………………………………. 2,000

Unrealized Holding Gain or Loss—Income …. 2,000

Unrealized Holding Gain or Loss—Income ……….. 65

*PROBLEM 17.15

(a) (1) No entry necessary at the date of the swap because the fair value

of the swap at inception is zero.

(2) June 30, 2020

(3) June 30, 2020

Cash ………………………………………………………… 50,000

Interest Expense ………………………………….. 50,000

(4) June 30, 2020

(5) June 30, 2020

Unrealized Holding Gain or Loss—

Income …………………………..………………………. 200,000

Swap Contract ……………………………………… 200,000

*PROBLEM 17.15 (Continued)

(c) Financial statement presentation as of June 30, 2020

Statement of Financial Position

Liabilities

Notes Payable $9,800,000

(d) Financial statement presentation as of December 31, 2020

Statement of Financial Position

Assets

Swap Contract $ 60,000

Liabilities

Notes Payable 10,060,000

Unrealized Holding Gain—

Swap $ 60,000

Unrealized Holding Loss—

Note Payable (60,000)

Total $ 0

*PROBLEM 17.16

(a) April 1, 2019

Memorandum entry to indicate entering into the futures contract.

(b) June 30, 2019

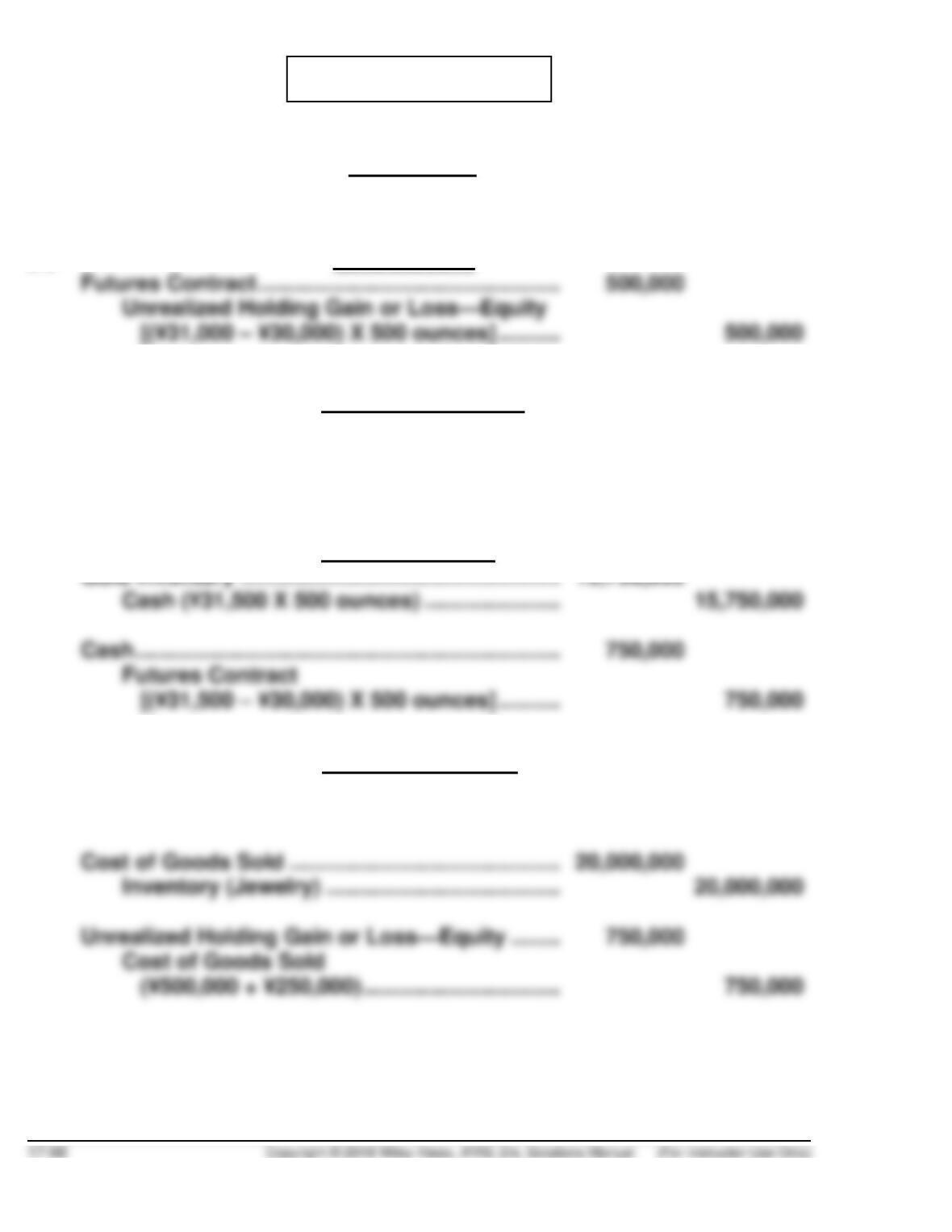

(c) September 30, 2019

Futures Contract …………………………………………. 250,000

Unrealized Holding Gain or Loss—Equity

[(¥31,500 – ¥31,000) X 500 ounces] ………. 250,000

(d) October 10, 2019

(e) December 20, 2019

Cash …………………………………………………………… 35,000,000

Sales Revenue ………………………………………. 35,000,000

*PROBLEM 17.16 (Continued)

(f) SUZUKI JEWELRY GROUP

Partial Statement of Financial Position

At June 30, 2019

Current Assets

(g) SUZUKI JEWELRY GROUP

Income Statement

For the Quarter Ended December 31, 2019

Sales revenue …………………………………………………………… ¥35,000,000

Cost of goods sold……………………………………………………. 19,250,000*

*PROBLEM 17.17

(a) (1) October 15, 2019

Inventory …………………………………………………. 240,000

(2) October 31, 2019

Unrealized Holding Gain or Loss—Income …. 125

Put Option (£300 – £175) ………………………. 125

(3) November 30, 2019

Unrealized Holding Gain or Loss—Income …. 70

Put Option (£175 – £105) ………………………. 70

*PROBLEM 17.17 (Continued)

(4) December 31, 2019

Unrealized Holding Gain or Loss—Income …. 65

Put Option (£105 – £40) ………………………… 65

(b) OIL PRODUCTS PLC

Partial Balance Sheet

At November 30, 2019

Assets

OIL PRODUCTS PLC

Income Statement

For the Month Ended November 30, 2019

Other Income (Loss)

£ (70)

(c) OIL PRODUCTS PLC

Partial Balance Sheet

At December 31, 2019

*PROBLEM 17.17 (Continued)

OIL PRODUCTS PLC

Income Statement

For the Month Ended December 31, 2019

Other Income (Loss)

Unrealized Holding Loss (Inventory) …………….. £(12,000)

Unrealized Holding Gain—put option …………….. £11,935

*Put Option

300

TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS

CA 17.1 (Time 25–30 minutes)

Purpose—To provide the student with an opportunity to discuss issues related to debt and equity

CA 17.2 (Time 25–30 minutes)

CA 17.3 (Time 20–30 minutes)

Purpose—To provide the student with an understanding of the accounting applications dealing with

CA 17.4 (Time 20–25 minutes)

Purpose—To provide the student with an understanding of the conceptual basis for the distinction

CA 17.5 (Time 15–25 minutes)

Purpose—To allow the student to discuss the equity method of accounting for investments and to provide

rationale for this method of accounting.

CA 17.6 (Time 25–35 minutes)

CA 17.7 (Time 25–35 minutes)

Purpose—To provide the student an opportunity to examine the ethical issues related to fair value

accounting.

SOLUTIONS TO CONCEPTS FOR ANALYSIS

CA 17.1

Situation 1 IFRS requires that investments that are actively traded be reported on the statement

of financial position at their fair value amount. Any changes in the fair value of trading

investments from one period to another are included in earnings. Therefore, the €4,200

decrease will be reported on the income statement as an unrealized holding loss.

Situation 4 When a reduction in the fair value of an investment is considered to be an

CA 17.2

(a) The reporting of these investments at fair value provides the financial statement user with more

relevant financial information. The fair value of the investments is essentially the present value of

CA 17.2 (Continued)

(b) Lexington Company should record the following journal entry and report the following amounts on

its statement of financial position.

December 31, 2019

Unrealized Holding Gain or Loss—Income ……………………………… 1,100

(c) No, Lexington Company did not properly account for the sale of the Summerset Company

shares. The cost basis of the Summerset shares is still $9,500. Therefore, Lexington should have

(d) December 31, 2020

Fair Value Adjustment …………………………………………………………. 1,500

Unrealized Holding Gain or Loss—Income ……………………… 1,500

the equity investment portfolio.

Investments

Cost

Fair Value

Unrealized

Gain (Loss)

Greenspan Corp. shares

$20,000

$19,900

($ (100)

Previous fair value adjustment balance—Cr.

( (1,100)

CA 17.3

Situation 1 The carrying value of the held-for-collection investment will be the fair value on the

date of the transfer.

Situation 2 When a decrease in the fair value of an investment is considered to be permanent,

CA 17.4

(a) A company maintains the different investment portfolios because each portfolio serves a different

investment objective. Since each portfolio serves a different objective, the possible risks and

(b) The criteria which should be considered when determining how to properly classify investments

are: (1) the company’s business model for managing their financial assets, and (2) the

contractual cash flow characteristics of the financial asset. If management is planning to sell the

investment in the near future and to earn its profit on the basis of any price change, then the

investment should be classified as a trading investment. On the other hand, if a company’s

business model is to hold debt assets in order to collect contractual cash flows and the

contractual terms give specified dates to cash flows that are solely payments of principal and

interest, then the investment should be classified as a held-for-collection investment.