EXERCISE 5.18 (25–35 minutes)

(a) MENACHEM NV

Statement of Cash Flows

For the Year Ended December 31, 2019

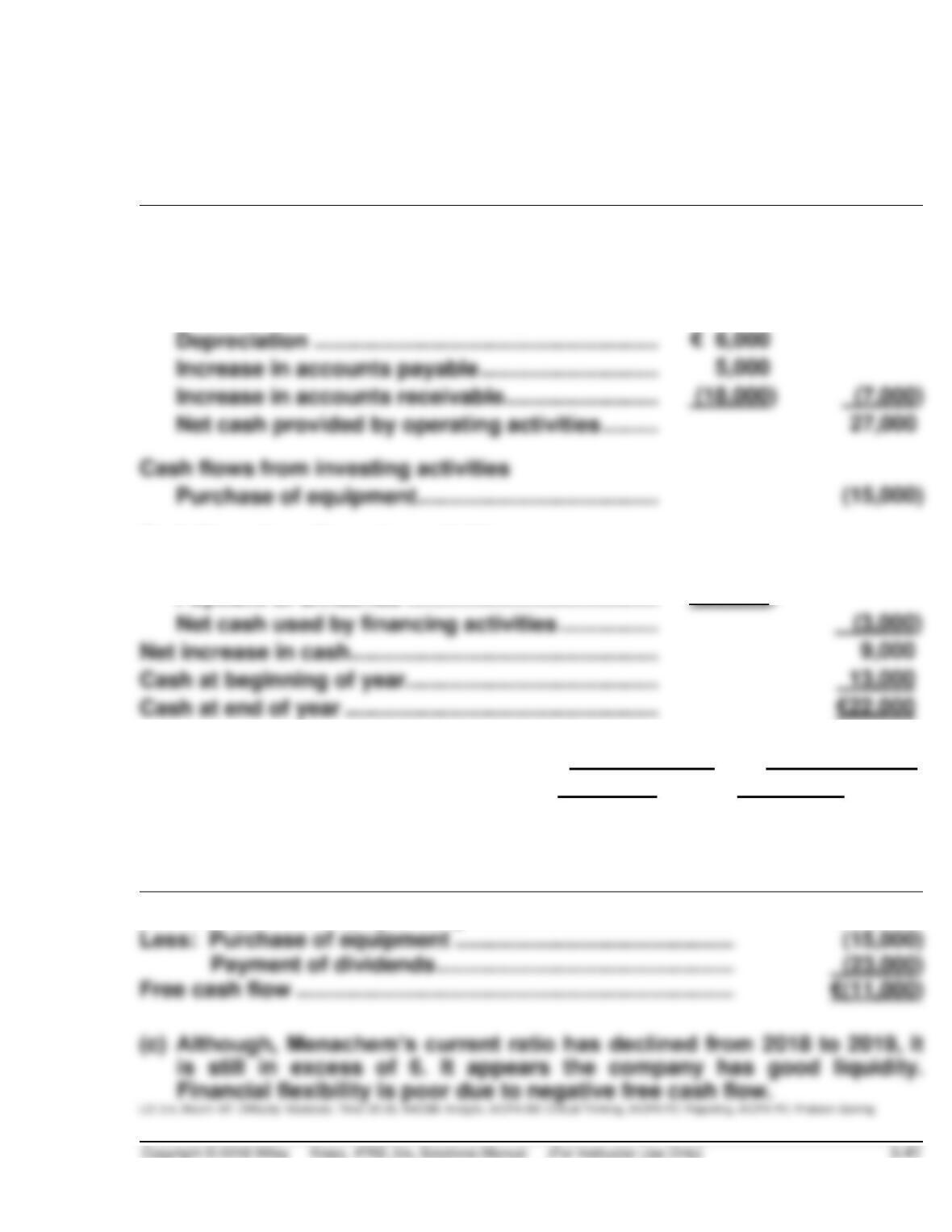

Cash flows from operating activities

Net income ……………………………………………………….

€34,000

Adjustments to reconcile net income

to net cash provided by operating activities:

Depreciation …………………………………………………….

Increase in accounts payable …………………………..

Increase in accounts receivable …………………………

Net cash provided by operating activities …………..

Cash flows from investing activities

Purchase of equipment ……………………………………..

Cash flows from financing activities

Issuance of ordinary shares …………………………..

20,000

Payment of dividends ……………………………………….

(23,000)

Net cash used by financing activities …………………

Net increase in cash ……………………………………………….

Cash at beginning of year ……………………………………….

Cash at end of year ………………………………………………..

2019

2018

(b) Current ratio

€128,000*

= 6.4

€101,000**

= 6.73

€ 20,000

€ 15,000

*(€106,000 + €22,000) ** *(€88,000 + €13,000)

Free Cash Flow Analysis

Net cash provided by operating activities ………………………..

€ 27,000

TIME AND PURPOSE OF PROBLEMS

Problem 5.1 (Time 30–35 minutes)

Purpose—to provide the student with the opportunity to prepare a statement of financial position, given a

set of accounts. No monetary amounts are to be reported.

Problem 5.2 (Time 35–40 minutes)

Problem 5.3 (Time 40–45 minutes)

Purpose—to provide an opportunity for the student to prepare a statement of financial position in good

Problem 5.4 (Time 40–45 minutes)

Problem 5.5 (Time 40–50 minutes)

Purpose—to provide the student with the opportunity to prepare a statement of financial position in good

the statement of financial position. A challenging problem.

Problem 5.6 (Time 35–45 minutes)

Purpose—to provide the student with an opportunity to prepare a complete statement of cash flows. A

condensed statement of financial position is also required. The student is also required to explain the

Problem 5.7 (Time 40–50 minutes)

Purpose—to provide the student with an opportunity to prepare a statement of financial position in good

form and a more complex cash flow statement.

SOLUTIONS TO PROBLEMS

PROBLEM 5.1

COMPANY NAME

Statement of Financial Position

December 31, 20XX

Assets

Non-current assets

Long-term investments

Bond sinking fund …………………………………….

$XXX

Land for future plant site …………………………..

XXX

$XXX

Property, plant, and equipment

Land ………………………………………………………..

$XXX

Less: Accum. depreciation—buildings ……….

XXX

Equipment ………………………………………………..

Less: Accum. depreciation—equipment ………

Total property, plant, and equipment …….

XXX

Intangible assets

Copyrights ……………………………………………….

XXX

Patents …………………………………………………….

XXX

XXX

Current assets

Inventory (ending) …………………………………….

XXX

Prepaid rent ……………………………………………..

XXX

Accounts receivable …………………………………

Interest receivable …………………………………….

XXX

Advances to employees …………………………….

XXX

XXX

XXX

Total current assets …………………………….

Total assets …………………………………………

PROBLEM 5.1 (Continued)

Equity and Liabilities

Equity

Share capital

Preference shares (description) …………………..

$XXX

Ordinary shares (description) ………………………

Share premium—ordinary …………………………………

XXX

Retained earnings ……………………………………………

Less: Treasury shares ……………………………………..

Equity attributable to controlling shareholders ….

Non-controlling interest ……………………………………

Total equity ………………………………………………..

Non-current liabilities

Bonds payable …………………………..………………………….

$XXX

Pension liability …………………………………………………….

XXX

Total non-current liabilities …………………………...

XXX

Current liabilities

Notes payable ………………………………………………….

XXX

Payroll taxes payable ……………………………………….

XXX

Salaries and wages payable ……………………………..

Dividends payable ……………………………………………

XXX

Unearned service revenue ………………………………..

XXX

Total current liabilities ………………………………..

Total liabilities …………………………………………….

PROBLEM 5.2

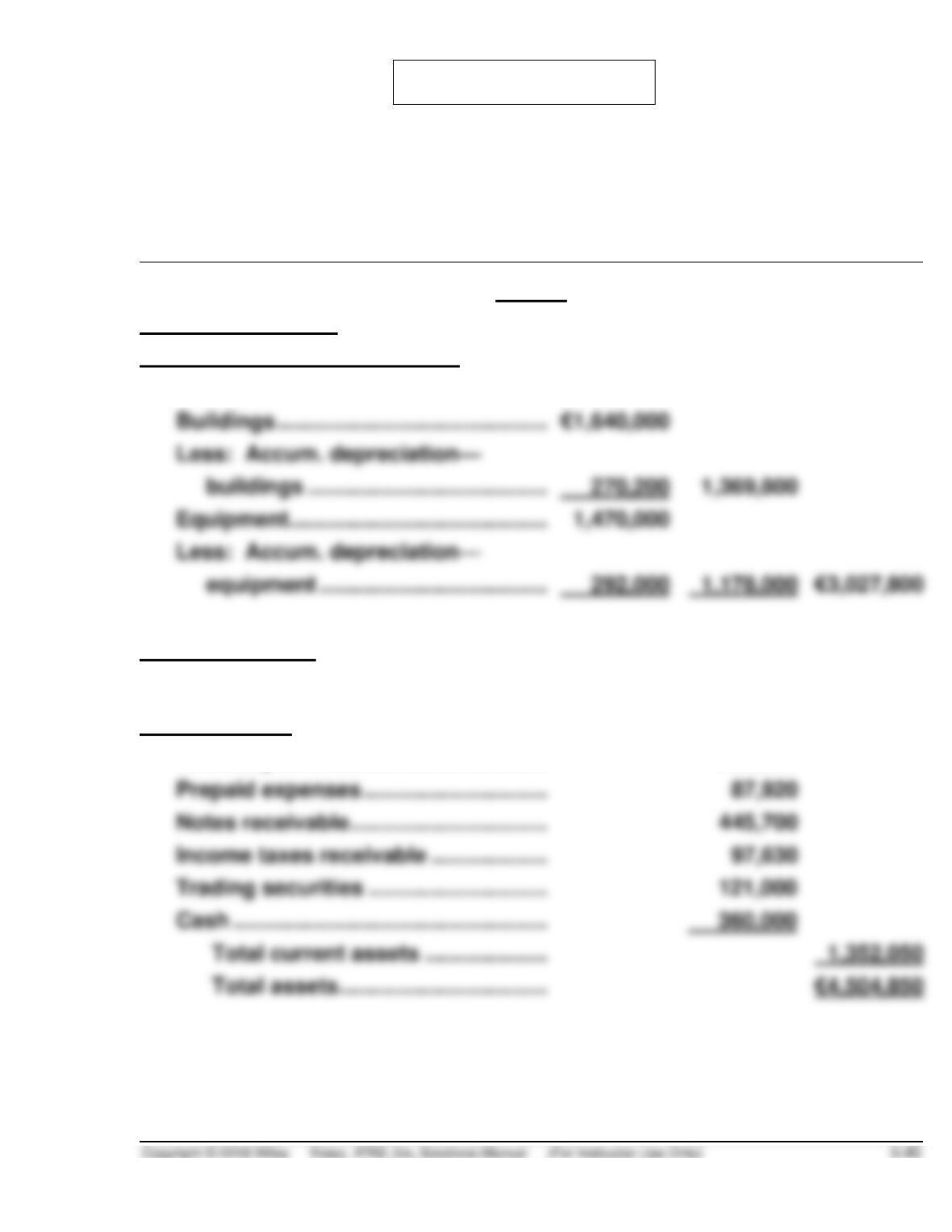

MONTOYA SA

Statement of Financial Position

December 31, 2019

Assets

Non-current assets

Property, plant, and equipment

Land …………………………………………….

€ 480,000

Buildings ………………………………………

buildings ………………………………….

Equipment …………………………………….

Intangible assets

Goodwill ……………………………………….

125,000

Current assets

Inventory ………………………………………

239,800

Prepaid expenses ………………………….

87,920

Notes receivable …………………………..

Income taxes receivable ………………..

Trading securities …………………………

Cash …………………………………………….

360,000

Total current assets …………………

Total assets ……………………………..

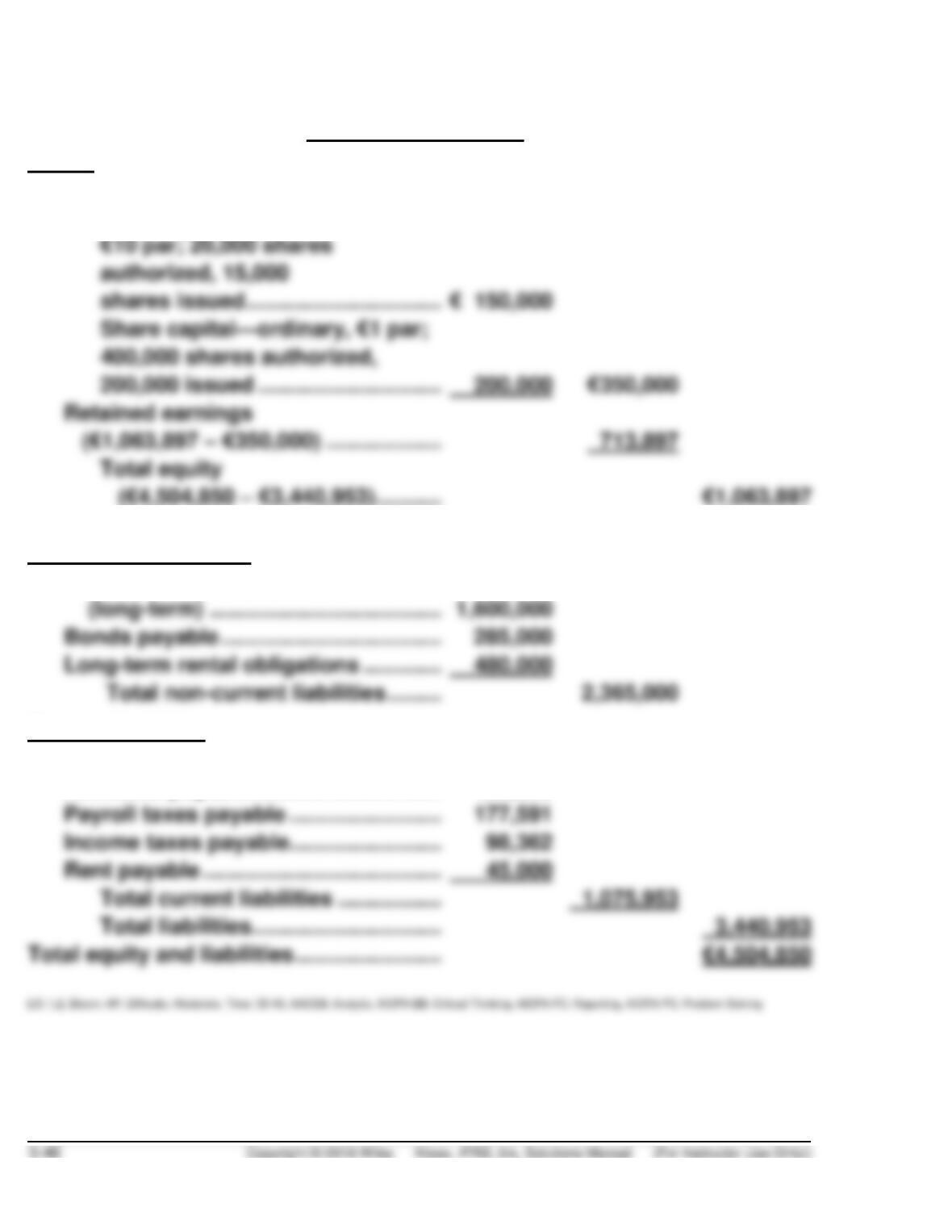

PROBLEM 5.2 (Continued)

Equity and Liabilities

Equity

Share capital

shares issued …………………………..

(€1,063,897 – €350,000) ………………..

(€4,504,850 – €3,440,953) …………

Share capital—preference

Non-current liabilities

Unsecured notes payable

(long-term) …………………………………

Bonds payable ……………………………….

285,000

Long-term rental obligations …………..

480,000

Total non-current liabilities ……….

Current liabilities

Notes payable to banks …………………..

265,000

Accounts payable …………………………..

490,000

Payroll taxes payable ……………………..

177,591

Income taxes payable……………………..

Rent payable ………………………………….

45,000

Total current liabilities ………………

Total liabilities …………………………..

PROBLEM 5.3

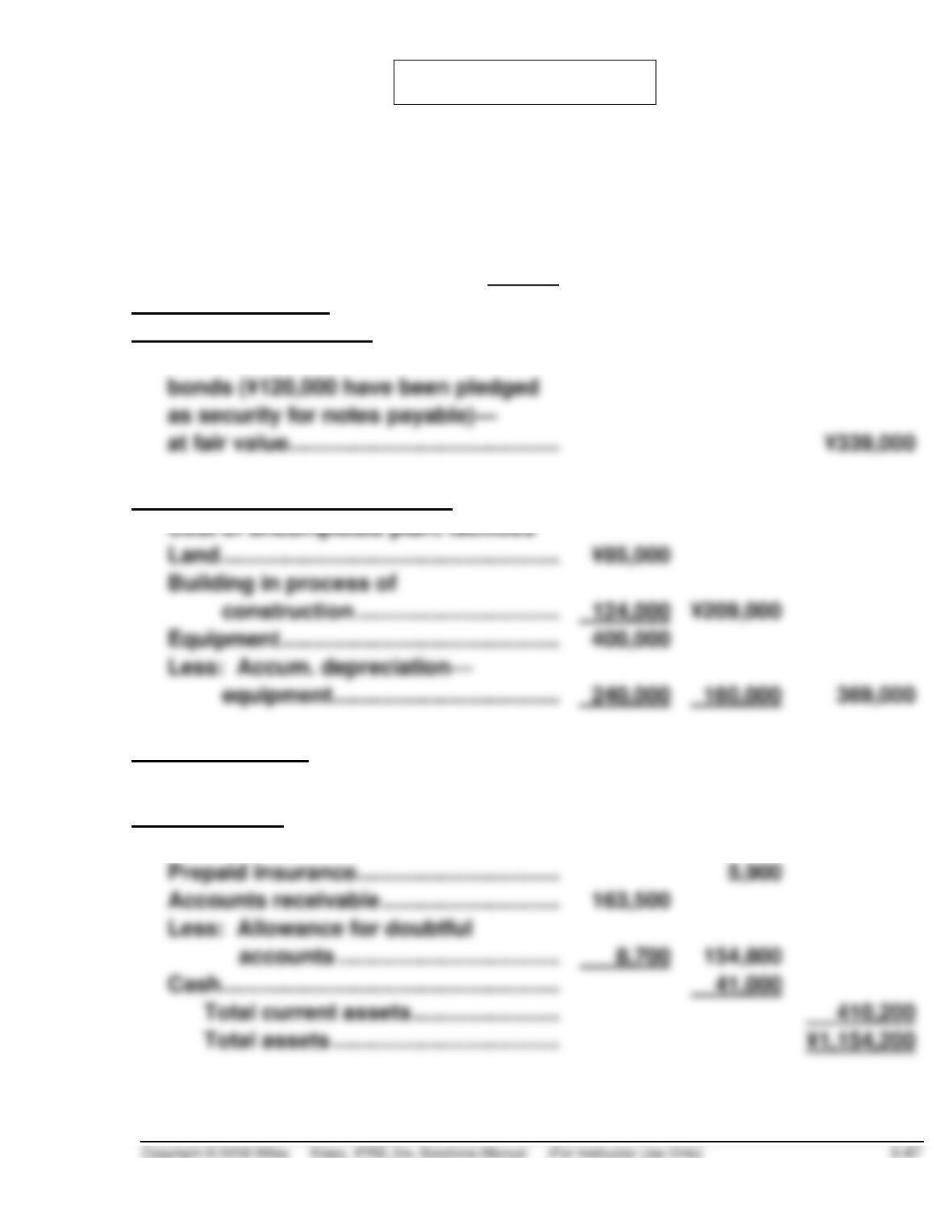

ASIAN-PACIFIC LTD

Statement of Financial Position

December 31, 2019

Assets

Non-current assets

Long-term investments

Investments in shares and,

Property, plant, and equipment

Cost of uncompleted plant facilities

Land …………………………..……………………

construction …………………………….

Equipment ……………………………………….

equipment ………………………………..

Intangible assets

Patents (at cost less amortization) …….

36,000

Current assets

Inventory (Average cost) …………………..

208,500

Prepaid insurance …………………………….

Accounts receivable …………………………

accounts ……………………………….

154,800

Cash ………………………………………………..

Total current assets …………………….

Total assets ………………………………..

¥1,154,200

PROBLEM 5.3 (Continued)

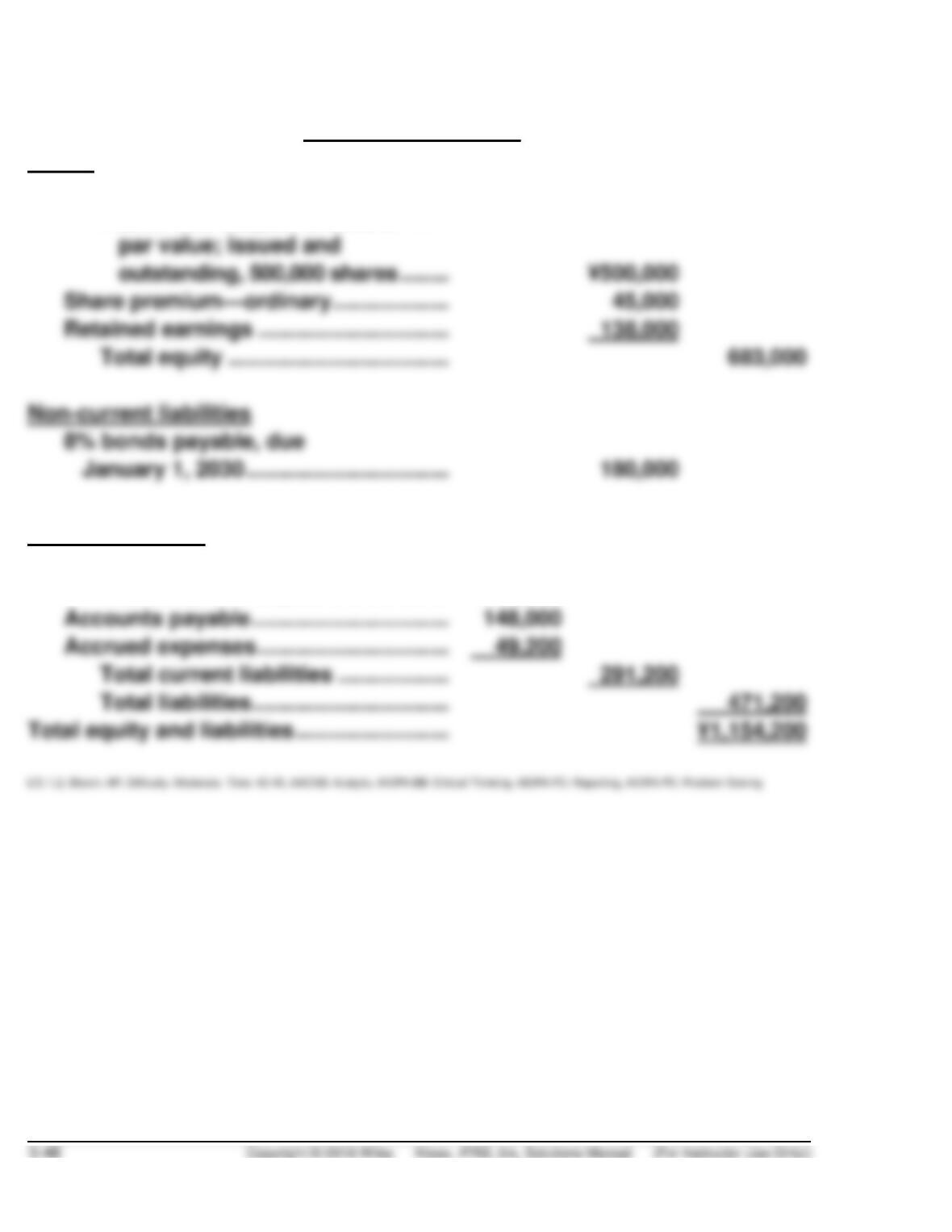

Equity and Liabilities

Equity

Share capital—ordinary

par value; issued and

outstanding, 500,000 shares ……..

Share premium—ordinary ……………….

Retained earnings ………………………….

Total equity ………………………………

Non-current liabilities

8% bonds payable, due

January 1, 2030 …………………………...

Authorized 600,000 shares of ¥1

Current liabilities

Notes payable, secured by

investments of ¥120,000 ………………..

¥ 94,000

Accounts payable …………………………..

Accrued expenses ………………………….

Total current liabilities ………………

Total liabilities …………………………..

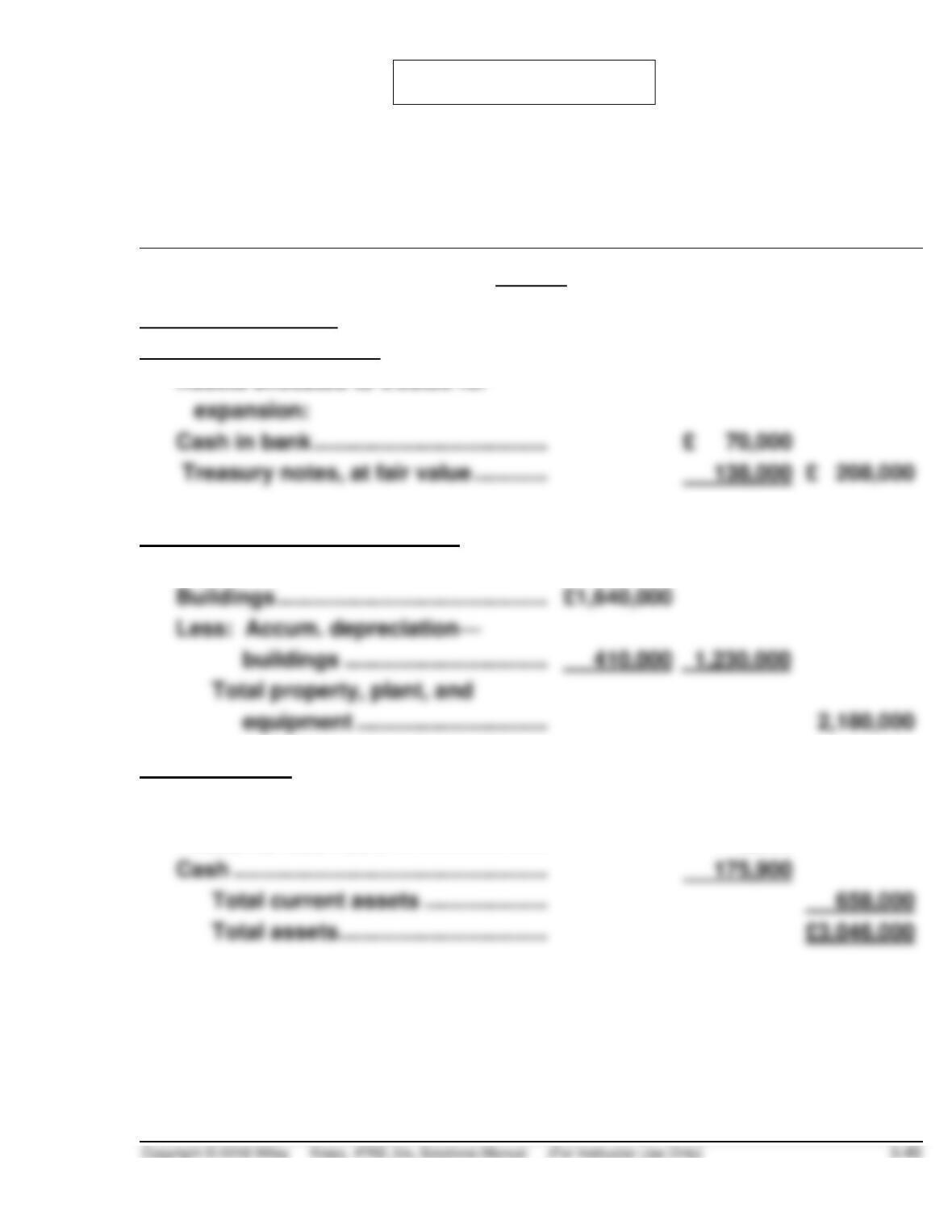

PROBLEM 5.4

KISHWAUKEE LTD

Statement of Financial Position

December 31, 2019

Assets

Non-current assets

Long-term investments

Cash in bank ……………………………………

Treasury notes, at fair value …………….

Assets allocated to trustee for

Property, plant, and equipment

Land ……………………………………………….

950,000

Buildings …………………………..…………….

Current assets

Inventory …………………………………………

312,100

Accounts receivable ………………………..

170,000

Cash ……………………………………………….

Total current assets ……………………

Total assets ………………………………..

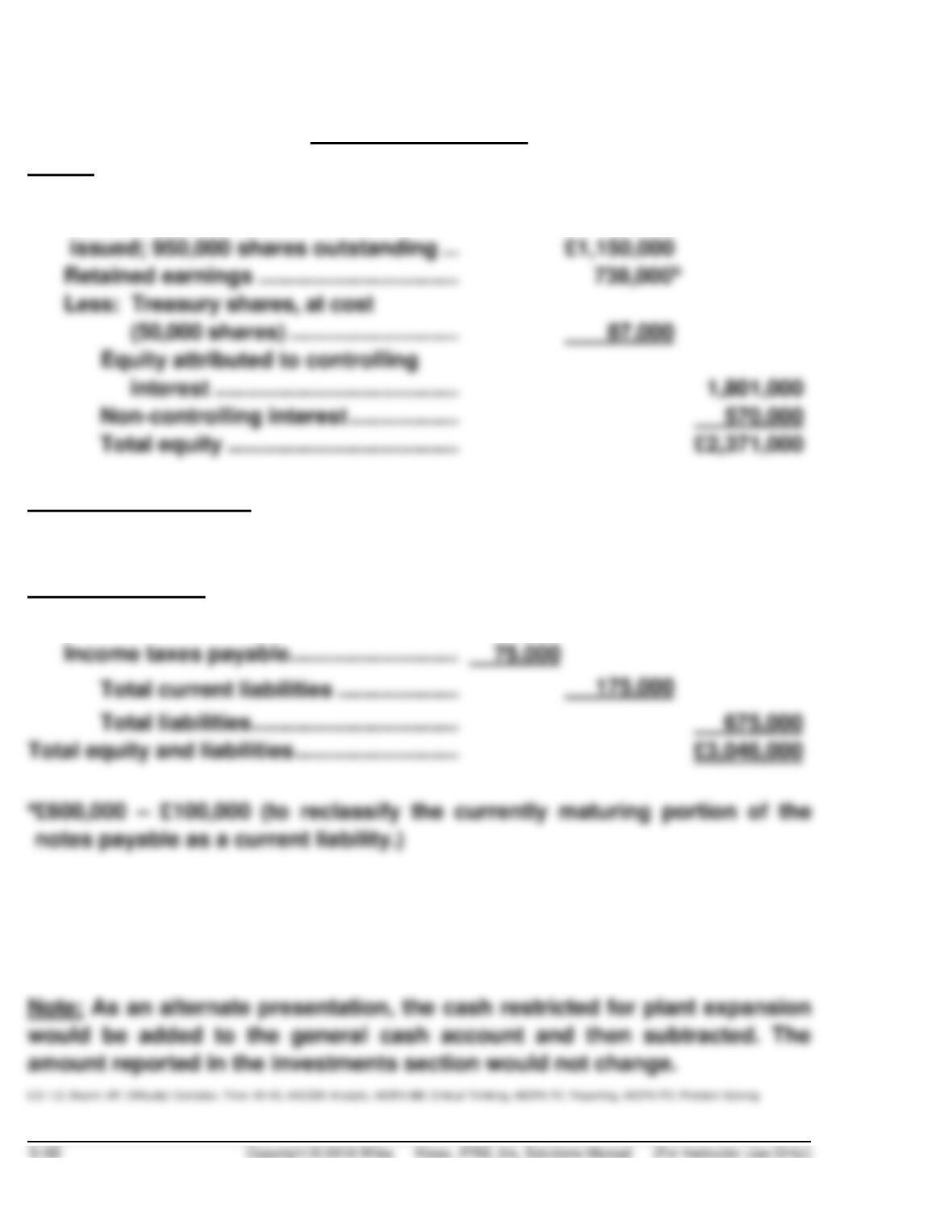

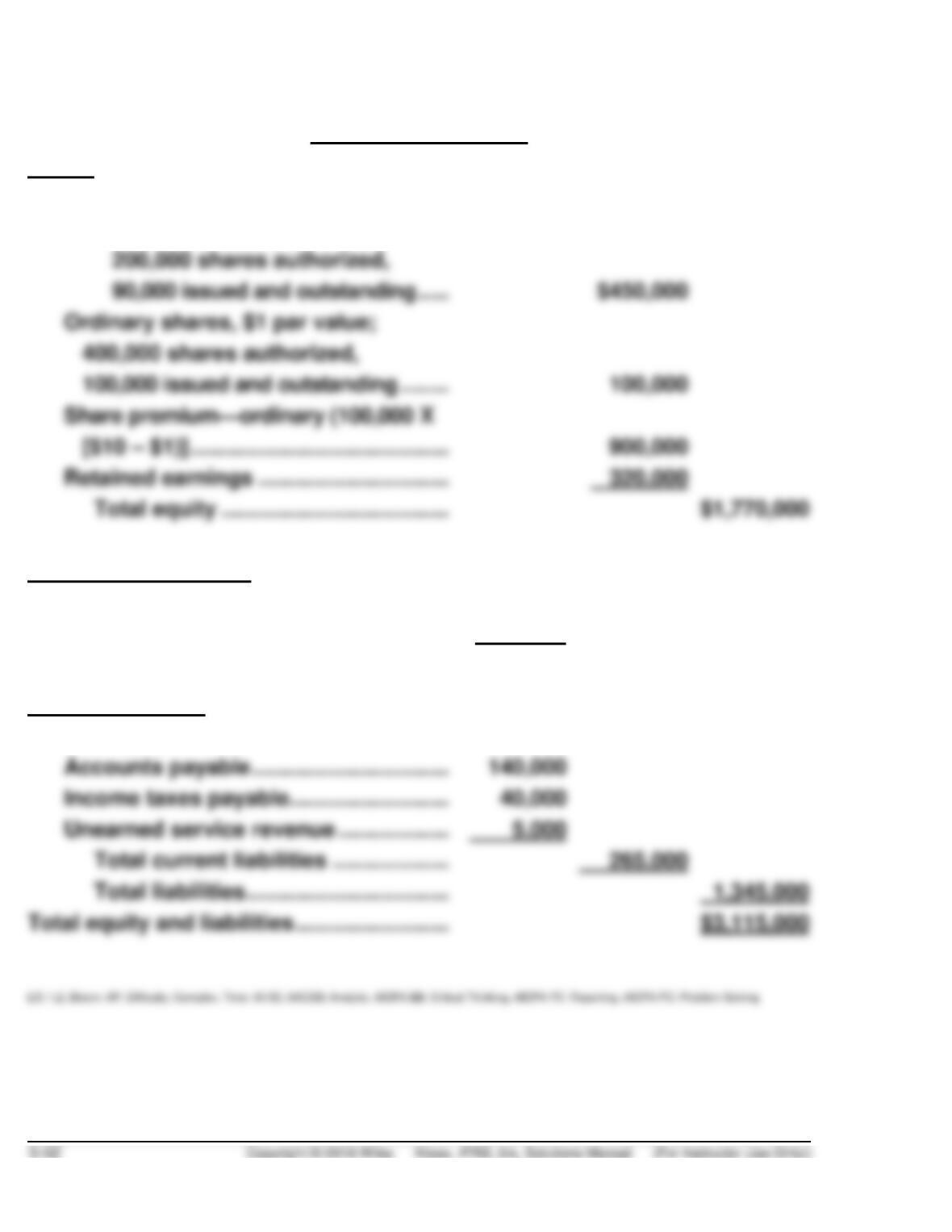

PROBLEM 5.4 (Continued)

Equity and Liabilities

Equity

issued; 950,000 shares outstanding …..

Retained earnings ……………………………..

Less: Treasury shares, at cost

(50,000 shares) …………………………

Non-controlling interest ………………..

Total equity ………………………………….

Share capital—ordinary, no par;

1,000,000 shares authorized and

Non-current liabilities

Notes payable …………………………………..

500,000a

Current liabilities

Notes payable—current installment ……

£100,000

75,000

Total liabilities ………………………………

b£858,000 – £120,000 (to remove the value of goodwill from retained earnings.

Note 2 indicates that retained earnings was credited. Note that the goodwill

account is also deleted.)

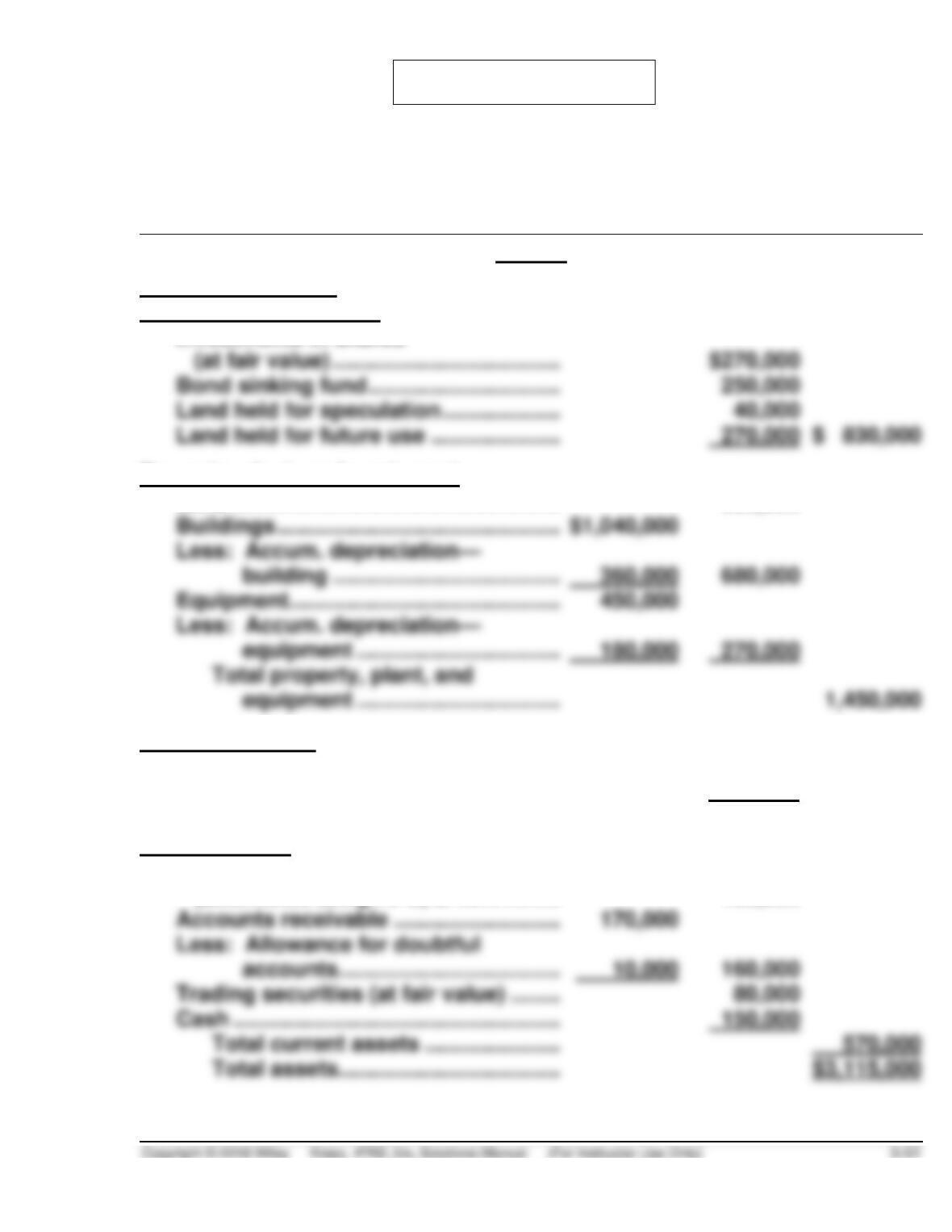

PROBLEM 5.5

SARGENT CORPORATION

Statement of Financial Position

December 31, 2019

Assets

Non-current assets

Long-term investments

Bond sinking fund …………………………..

250,000

Land held for speculation …………………

Land held for future use …………………..

270,000

$ 830,000

Investments in shares

Property, plant, and equipment

Land ……………………………………………….

500,000

Buildings …………………………………………

$1,040,000

Equipment ……………………………………….

equipment ……………………………..

180,000

270,000

Intangible assets

Franchise …………………………..……………

165,000

Goodwill ………………………………………….

100,000

265,000

Current assets

Inventory, at lower of cost

(determined using FIFO) or NRV ………..

180,000

Accounts receivable ………………………..

170,000

Less: Allowance for doubtful

Trading securities (at fair value) ……….

Cash ……………………………………………….

150,000

Total current assets ……………………

570,000

PROBLEM 5.5 (Continued)

Equity and Liabilities

Equity

Share capital

Retained earnings …………………………..

320,000

Total equity ………………………………….

Preference shares, $5 par value;

Non-current liabilities

Notes payable …………………………………..

$120,000

7% bonds payable, due 2027 ……………..

960,000

Total non–current liabilities ………………

1,080,000

Current liabilities

Notes payable …………………………………..

80,000

Accounts payable …………………………..

Income taxes payable………………………..

40,000

Unearned service revenue …………………

5,000

Total current liabilities ………………….

PROBLEM 5.6

(a) LANSBURY INC.

Statement of Cash Flows

For the Year Ended December 31, 2019

Cash flows from operating activities

Net income …………………………………………………..

$32,000

net cash provided by operating activities

Depreciation expense ……………………………..

Gain on sale of investments …………………….

Increase in account receivable

($41,600 – $21,200) ……………………………….

(20,400)

(12,800)

Net cash provided by operating activities ………

Adjustments to reconcile net income to

Cash flows from investing activities

Sale of investments ………………………………………

15,000

Purchase of land ………………………………………….

(18,000)

Net cash used by investing activities …………….

(3,000)

Cash flows from financing activities

Issuance of ordinary shares ………………………….

20,000

Retirement of notes payable ………………………….

Payment of cash dividends …………………………..

(8,200)

Net cash used by financing activities …………….

(4,200)

Net increase in cash …………………………………………..

12,000

Cash at beginning of year …………………………………..

20,000

Cash at end of year ……………………………………………

$32,000

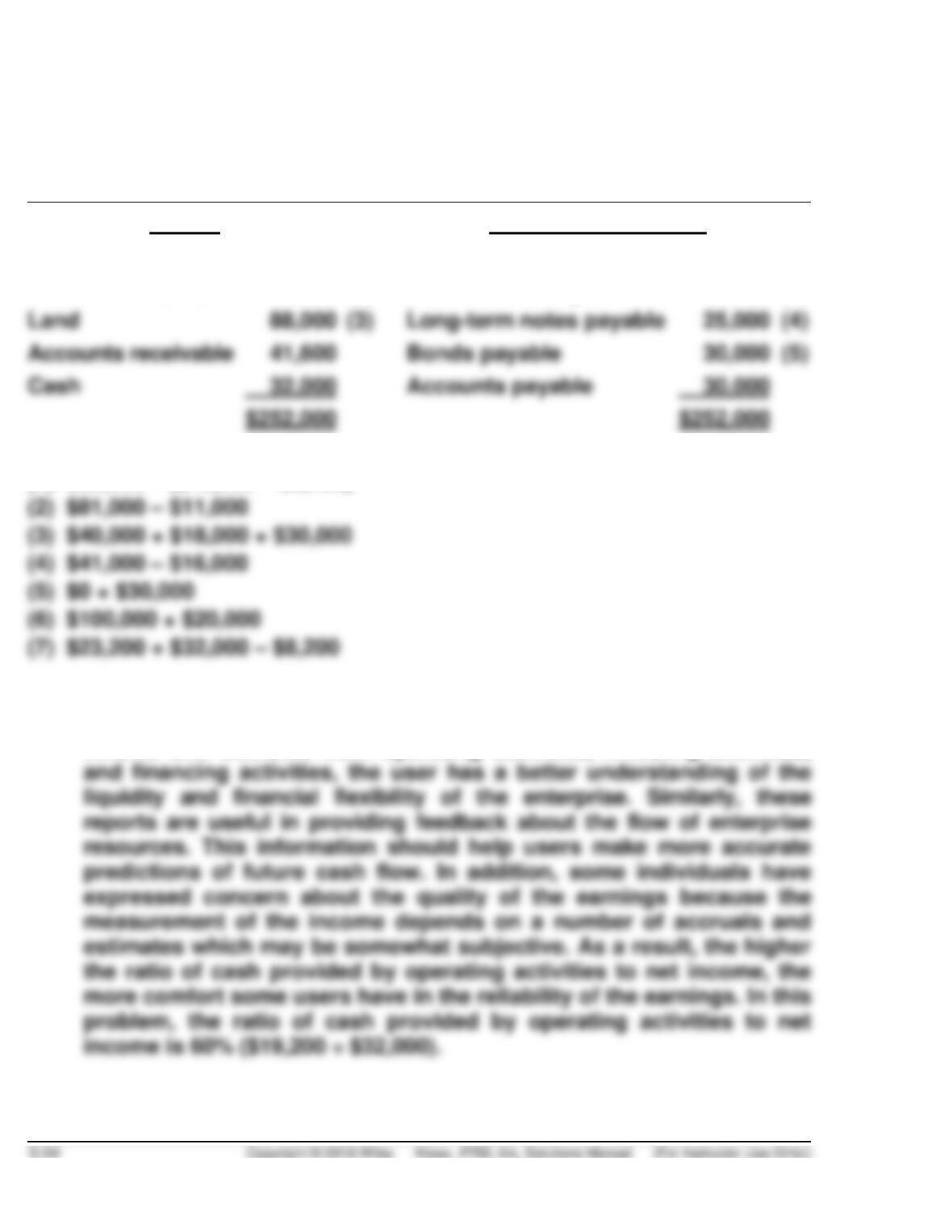

PROBLEM 5.6 (Continued)

(b) LANSBURY INC.

Statement of Financial Position

December 31, 2019

Assets

Equity and Liabilities

Investments

$ 20,400

(1)

Share capital—ordinary

$120,000

(6)

Plant assets (net)

70,000

(2)

Retained earnings

47,000

(7)

Land

88,000

(3)

Long-term notes payable

25,000

(4)

Accounts receivable

41,600

Bonds payable

30,000

(5)

Cash

32,000

Accounts payable

30,000

$252,000

$252,000

(1) $32,000 – ($15,000 – $3,400)

(c) Cash flow information is useful for assessing the amount, timing, and

uncertainty of future cash flows. For example, by showing the specific

inflows and outflows from operating activities, investing activities,

PROBLEM 5.6 (Continued)

An analysis of Lansbury’s free cash flow indicates it is negative as shown

below:

Free Cash Flow Analysis

Net cash provided by operating activities …………………………

$19,200

Less: Purchase of land ………………………………………………….

Dividends …………………………………………………………….

PROBLEM 5.7

(a) LUO LTD

Statement of Cash Flows

For the Year Ended December 31, 2019

Cash flows from operating activities

Net income ……………………………………………………

¥35,000

net cash provided by operating activities

Depreciation expense ……………………………….

Loss on sale of investments ……………………..

Increase in accounts payable

(¥40,000 – ¥30,000) ……………………………..

10,000

Increase in accounts receivable

(¥42,000 – ¥21,200) ……………………………..

(20,800)

6,200

Net cash provided by operating activities ……….

Adjustments to reconcile net income to

Cash flows from investing activities

Sale of investments (¥32,000 – ¥5,000) …………..

27,000

Purchase of land ……………………………………………

(38,000)

Net cash used by investing activities ……………..

(11,000)

Cash flows from financing activities

Issuance of ordinary shares …………………………..

30,000

Payment of cash dividends …………………………...

(10,000)

Net cash provided by financing activities………..

Net increase in cash …………………………..……………….

Cash at beginning of year ……………………………………

PROBLEM 5.7 (Continued)

(b) LUO LTD

Statement of Financial Position

December 31, 2019

Assets

Equity and Liabilities

Plant assets (net)

¥ 69,000

(1)

Share capital—ordinary

¥130,000

(4)

Land

108,000

(2)

Retained earnings

48,200

(5)

(1) ¥81,000 – ¥12,000

(c) An analysis of Luo’s free cash flow indicates it is negative as shown

below:

Free Cash Flow Analysis

Net cash provided by operating activities …………………………

¥ 41,200

Less: Purchase of land ……………………………………………………

Dividends ……………………………………………………….

PROBLEM 5.7 (Continued)

(d) This type of information is useful for assessing the amount, timing, and

uncertainty of future cash flows. For example, by showing the specific

inflows and outflows from operating activities, investing activities, and

financing activities, the user has a better understanding of the liquidity

and financial flexibility of the enterprise. Similarly, these reports are